Abstract

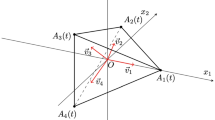

This article deals with the boundary crossing probability of a geometric Brownian motion (GBM) process when the boundary itself is a GBM process. An exact formula is obtained for the probability that the first exit time of \( S\left( t \right) \) from the stochastic interval \( \left[ {H_{1} \left( t \right),H_{2} \left( t \right)} \right] \) is greater than a finite time \( T \) using a partial differential equation approach. Applications and numerical results are provided. The possibility of an extension to higher dimension is also discussed. In particular, the steps to obtain the probability that \( S_{1} \left( t \right) \), \( S_{2} \left( t \right) \) and \( S_{3} \left( t \right) \) remain above \( S_{4} \left( t \right) \), \( \forall 0 \le t \le T \), are outlined, while pointing out that the entailed numerical issues make the relevance of an analytical approach questionable.

Similar content being viewed by others

References

Levy, P.: Processus Stochastiques et Mouvement Brownien. Gauthier-Villars, Paris (1948)

Doob, J.L.: Heuristic approach to the Kolmogorov–Smirnov theorem. Ann. Math. Stat. 20, 393–403 (1949)

Anderson, T.W.: A modification of the sequential probability ratio test to reduce the sample size. Ann. Math. Stat. 31, 165–197 (1960)

Salminen, P.: On the first hitting time and last exit time for a Brownian motion to/from a moving boundary. Adv. Appl. Prob. 20, 411–426 (1988)

Groeneboom, P.: Brownian motion with a parabolic drift and airy Functions. Prob. Theory Rel. Fields 81, 79–109 (1989)

Novikov, A., Frishling, V., Kordzakhia, N.: Approximations of boundary crossing probabilities for a Brownian motion. J. Appl. Prob. 34, 1019–1030 (1999)

Breiman L.: First exit time from a square root boundary, Proc. 5th Berkeley Symp. Math. Statist. Prob., 2 (1966), 9-16

Shepp, L.A.: A first passage problem for the Wiener process. Ann. Math. Stat. 38, 1912–1914 (1967)

Sato, S.: Evaluation of the first-passage time probability to a square root boundary for the Wiener process. J. Appl. Prob. 14, 850–856 (1977)

Guillaume, T.: On the computation of the survival probability of Brownian motion with drift in a closed time interval when the absorbing boundary is a step function. J. Prob. Stat. 2015, 22 (2015). (Article ID 391681)

Guillaume, T.: Computation of the survival probability of Brownian motion with drift in a closed time interval when the absorbing boundary is an affine or an exponential function of time. Int. J. Stat. Prob. 5, 119–138 (2016)

Scheike, T.H.: A boundary crossing result for Brownian motion. J. Appl. Prob. 29, 448–453 (1992)

Daniels, H.E.: Approximating the first crossing time density for a curved boundary. Bernoulli 2, 133–143 (1996)

Wang, L., Pötzelberger, K.: Boundary crossing probability for Brownian motion and general boundaries. J. Appl. Prob. 34, 54–65 (1997)

Wang, L., Pötzelberger, K.: Crossing probabilities for diffusion processes with piecewise continuous boundaries. Methodol. Comput. Appl. Prob. 9, 21–40 (2007)

Abundo, A.: Some conditional crossing results of Brownian motion over a piecewise-linear boundary. Stat. Prob. Lett. 58, 131–145 (2002)

Park, C., Beekman, J.A.: Stochastic barriers for the Wiener process. J. Appl. Prob. 20, 338–348 (1983)

Che, X., Dassios, A.: Stochastic boundary crossing probabilities for the Brownian motion. J. Appl. Prob. 50, 419–429 (2012)

Bielecki, T.R., Rutkowski, M.: Credit Risk: Modeling, Valuation and Hedging. Springer, Berlin (2004)

Stroock, D.W., Varadhan, S.R.S.: Multidimensional Diffusion Processes. Springer, New York (1979)

Karatzas, I., Shreve, S.: Brownian Motion and Stochastic Calculus. Springer, New-York (1991)

Duffy, D.G.: Transform Methods for Solving Partial Differential Equations. Chapman & Hall, Boca Raton (2004)

He, H., Keirstead, W.P., Rebholz, J.: Double lookbacks. Math. Finance 8, 201–228 (1998)

Rebholz, J.: Planar diffusions with applications to mathematical finance. Ph.D. thesis, University of Berkeley (1994)

Zhou, C.: An analysis of default correlations and multiple defaults. Rev. Financ. Stud. 14, 555–576 (2001)

Kou, S., Zhong, H.: First passage times of two dimensional Brownian motion. Adv. Appl. Prob. 48, 1045–1060 (2016)

Duffy, D.G.: Green’s Functions with Applications. Chapman & Hall, Boca Raton (2001)

Jeanblanc, M., Yor, M., Chesney, M.: Mathematical Methods for Financial Markets. Springer, London (2009)

Guillaume, T.: Step double barrier options. J. Deriv. 18, 59–79 (2010)

Kunitomo, N., Ikeda, M.: Pricing options with curved boundaries. Math. Finance 2, 275–298 (1992)

Kronrod, A.S.: Doklady Akad. Nauk SSSR 154, 283–286 (1964)

Calvetti, D., Golub, G.H., Gragg, W.B., Reichel, L.: Computation of Gauss–Kronrod quadrature rules. Math. Comput. 69(2000), 1035–1052 (2000)

Carslaw, H.S., Jaeger, J.C.: Conduction of Heat in Solids. Oxford University Press, Oxford (1959)

Guillaume, T.: On the multidimensional Black–Scholes partial differential equation. Ann. Oper. Res. https://doi.org/10.1007/s10479-018-3001-1

Craig, I.J.D., Sneyd, A.D.: An alternating-direction implicit scheme for parabolic equations with mixed derivatives. Comput. Math Appl. 16, 341–350 (1988)

Acknowledgements

The author thanks the anonymous referees for their comments and suggestions which contributed to improve the initial manuscript.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Guillaume, T. On the First Exit Time of Geometric Brownian Motion from Stochastic Exponential Boundaries. Int. J. Appl. Comput. Math 4, 120 (2018). https://doi.org/10.1007/s40819-018-0556-0

Published:

DOI: https://doi.org/10.1007/s40819-018-0556-0