Abstract

The complexities surrounding connected cars, especially the integration of Telematics Control Units (TCUs), intensify uncertainties within their value chains. Disputes arise regarding rightful licensees and applicable rates. Standard Essential Patent (SEP) holders push for royalties from end-product manufacturers, pegged to final product prices. Conversely, manufacturers and suppliers argue for licensing directed at suppliers, restricting royalties to the TCU’s price. This discord unfolded in the legal tussle involving Nokia (SEP holder), Daimler (car manufacturer), and its supplier, litigated in German courts. This context underscores the significance behind the EU Commission’s proposal on SEP licensing issued in April 2023. Addressing escalating disputes and uncertainties surrounding Fair, Reasonable, and Non-Discriminatory (FRAND) royalty rates, the proposal aims to establish transparency and predictability in SEP licensing. In our study, we have devised a proposal aimed at reshaping this landscape. We challenge the conventional linkage of SEP royalties solely to end-product prices within intricate value chains. Instead, we advocate tying SEP royalties to the economic value attributed to the SEP, specifically focusing on connectivity within Internet of Things (IoT) applications. Our proposal suggests granting licences to the party responsible for designing the IoT component, irrespective of its role in the value chain. This functionalistic approach also proposes establishing the royalty base through technical, measurable factors like data consumption. This model offers objectivity in determining FRAND rates, potentially fostering constructive negotiations and offering environmental benefits.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Standard essential patents (SEPs) are important in the Internet of Things (IoT) and especially in the automotive industry, where the use of connectivity standards is becoming increasingly prevalent. As cars become more connected, they require access to a range of different communications protocols and technologies, and this has led to a rise in the number of lawsuits related to SEP licensing in the automotive industry.

The emergence of connected vehicles has the potential to revolutionise the automotive industry and can provide benefits to manufacturers, consumers, and society as a whole. According to McKinsey, advanced industries, on-demand mobility and data-driven services could generate up to $2 trillion in revenue by 2030, with data connectivity services accounting for a significant portion of this amount, ranging between $450 billion to $750 billion per year.Footnote 1 The growth of connected vehicles has been enabled by mobile telecommunications standards, particularly cellular standards, which provide the necessary infrastructure for new connectivity-based products and services to emerge in the automotive industry. However, as new sources of value are created by connected vehicles, the issue of how to monetise them and who should benefit from them becomes critical. This transformation is disrupting traditional value chains and leading to new business models in the industry.Footnote 2

Despite these challenges, the use of connectivity standards in the automotive industry is expected to continue to grow. As such, it is crucial that the issues related to SEP licensing are addressed in a way that ensures fair and reasonable access to these important technologies.

The EU Commission’s proposal on SEP licensing reflects the pressing need to address escalating disputes and uncertainties surrounding FRAND royalty rates in the value chain.Footnote 3 The Commission emphasises the promotion of transparency and predictability in SEP licensing.Footnote 4 With a focus on benefitting EU industry, consumers, and particularly SMEs, the Commission acknowledges the surge in SEP disputes within the automotive sector and foresees similar challenges emerging in other IoT sectors that adopt connectivity and standards.Footnote 5

To effectively mitigate these issues, the initiative aims to provide detailed information on SEPs and existing FRAND terms, streamlining licensing negotiations. Additionally, it aims to enhance awareness of SEP licensing throughout the value chain. This endeavour underscores the vital importance of researching FRAND royalty rates within the value chain, aligning with the EU Commission’s objectives to foster fair and equitable licensing practices for the benefit of all stakeholders.

2 Connected Car History

Historically, automotive companies relied on proprietary technologies. However, the advent of connected vehicles in 1996 and subsequent integration of 3G/4G functionalities led to a shift towards standards-based frameworks,Footnote 6 where connectivity became vital for applications like navigation, infotainment, and over-the-air updates.Footnote 7

As the automotive industry witnesses the pervasive inclusion of embedded solutions, nearly all manufacturers plan to incorporate them into their new vehicles. This trend aligns with predictions that a vast majority of new vehicles sold globally will feature embedded connectivity. This shift in the automotive landscape, turning vehicles into significant digital platforms, is causing intense competition between the automotive ecosystem based on embedded connectivity and the existing mobile ecosystem relying on smartphone connectivity and associated application platforms like iOS and Android.Footnote 8

Automobile companies may need to shift their approach to licensing and become more directly involved in order to take advantage of new software-based technologies, and offer the latest advancements to customers. This shift has already led to new relationships between traditional car companies and technology companies, with licensing agreements being made between established car companies and small software companies developing standardised IoT features.Footnote 9 It has also created opportunities for licensing agreements between large established car companies and small software companies that develop standardised IoT features. These smaller companies, being more agile and creative, may be able to formulate licensing plans and strategies more effectively to incorporate their technologies into cars.

The price differential between cars and other types of consumer devices that typically implement standardised technologies means that a percentage-based model for licensing fees may not be feasible. As a result, some licensors, such as Avanci,Footnote 10 offer a flat-rate licensing model for cars rather than percentage-based models that many of its members advocate for smartphones.Footnote 11 This discourse holds significance for the determination of FRAND rates concerning SEPs linked to the IoT in automotive applications.

3 Problem Statement

This paper deals specifically with the question of the royalty base, which is about how much an SEP licence should cost. SEP holders ideally prefer to grant a licence to the end-product manufacturer based on the value of the end-product, but the end-product manufacturer may disagree with the royalty base and with the mere taking of the licence. He may argue that the rightful licensee is actually the component supplier who provides him with the SEP-integrated component, and the appropriate royalty base is the component price itself.

On the other hand, the component suppliers, who are often of different tiers, may consider themselves entitled to a licence, not just for the sake of legally providing the 4G component for the end-product manufacture, but in fact in order to be able to innovate and develop freely, and sell independently to other potential customers.Footnote 12 However, they would unlikely agree to pay at an end-product royalty base.

It is worth mentioning that while the level of licensing (i.e. who should take a licence) and the royalty base are two distinct notions,Footnote 13 the arguments put forth to privilege one level or base with regard to the other tend to follow a similar pattern, i.e. those in favour of licensing all parties, including the component maker, generally support a component-based royalty rate,Footnote 14 while those advocating for access to all tend to support end-product-based licensing.Footnote 15 However, the fact that patentees’ participation in the economic benefits of the technology is fulfilled at the end of the value chain does not necessarily imply that the licence agreement has to be exclusively concluded with the producer of the end-product. Indeed, this debate is largely driven by pricing considerations, as applying the royalty to the higher-value end-product can potentially generate a larger amount compared to applying it to the lower-priced component.

4 Research Objective and Approach

In practice, three primary licensing options are possible. The first option is a licence to the end-product manufacturer at an end-product rate, which is mostly the SEP holders’ preference. The second is a licence to component suppliers at a component-based rate, which is mostly the end-product manufacturer’s preference. And the third is a licence to the component manufacturer at an end-product rate which is also demanded by SEP holders.

These options were exactly the principal offers and counter-offers exchanged in the Nokia v. Daimler case (Daimler). To maintain focus and avoid prolonged debate, we limit our discussion to these three primary offers exchanged between the parties and the corresponding judgments made in the Daimler case.Footnote 16 This way, by staying in the practical context, we will be able to create a base step by step for our functionalistic approach which will be presented subsequently. We propose a potential solution to contribute to the ongoing discussion and facilitate a mutually beneficial resolution to the current dispute. By doing so, we aim to provide insights and guidance to the parties involved in SEP licensing negotiations, as well as to policymakers, scholars, and practitioners in the field.

This study falls within the purview of European jurisdiction, with the primary focus directed towards European law, encompassing both EU law and national law. However, in certain specific contexts, particularly when exploring aspects related to the smallest saleable patent practising unit (SSPPU), the study incorporates insights from U.S. jurisprudence. This inclusion is motivated by the advanced and diverse nature of U.S. legal precedents, as well as their prominent status in the literature. Omitting reference to U.S. case law would render the discussions incomplete, given its substantial relevance and contribution to the overall understanding of the subject matter. We, however, believe that the findings drawn from U.S. case law are also applicable to the EU context.

5 Nokia v. Daimler and the Value Chain Structure

Nokia filed a lawsuit against Daimler for alleged patent infringement. The patent in question is related to a crucial method for transmitting data in a telecommunications system that is essential for LTE, the fourth-generation mobile communications standard that was standardised by the 3rd Generation Partnership Project (3GPP),Footnote 17 of which the European Telecommunications Standards Institute (ETSI) is a member. In 2014, Nokia notified ETSI of its application for the patent and emphasised that it was essential for the LTE standard. Furthermore, Nokia issued a FRAND declaration to ETSI, in which it committed to offering licences to third parties on FRAND terms, emphasising its dedication to fair and reasonable practices.

Daimler, the renowned German manufacturer of passenger cars, offers various mobility and financial services to its customers, including vehicles equipped with Telematics Control Units (TCUs), which allow them to connect to the internet via the LTE network. This technology empowers the users to enjoy internet-based services such as satellite navigation, music and data streaming, as well as to receive over-the-air updates from Daimler without the need to visit a workshop or dealership. The TCU is essential for registering and operating the vehicles, as it enables the legally required emergency call system (eCall) to function seamlessly.Footnote 18 With this advanced technology, Daimler is committed to enhancing the driving experience and safety of its customers.

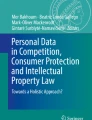

The TCUs are not manufactured by Daimler itself but, as shown in Fig. 1, in a multi-tier production chain. Daimler obtains the TCUs from its direct suppliers (Tier 1 suppliers). The Tier 1 suppliers, for their part, obtain the network access devices (NADs) required for the production of the TCUs from other suppliers (Tier 2 suppliers). The Tier 2 suppliers in turn receive the chips they need for the NADs from Tier 3 suppliers. After the Tier 1 supplier provides the TCU to the original equipment manufacturer (OEM), it is integrated into the vehicle. The broadband chipset enables cellular communications, while downstream equipment handles other functions beyond cellular standards.

Theoretical value chain structure (left) and chain structure in connected car industry (right)

The litigation between Nokia and Daimler began in 2019 following a failure in the initial negotiations between the car manufacturer and the mobile company. Daimler and some of its suppliers, including Continental, Huawei, Burry, and TomTom, complained to the European Commission that Nokia was exploiting its market power with its SEPs.Footnote 19 Nokia initiated a counter-offensive, suing Daimler for infringement of several patents before the regional courts of Mannheim, Munich and Düsseldorf. Then invalidity suits against Nokia patents were brought at the European Patent Office and the German Federal Patent Court. Daimler and its suppliers had emphasised that not the car manufacturer, but rather its Tier 1 and Tier 2 suppliers should take the Nokia patents licence, while Nokia had long refused to do this.

6 Royalty Rate Base

In 2010, Eric StasikFootnote 20 conducted a highly cited survey aiming to determine the patent licensing expectations of the largest contributors to the LTE (4G) standard.Footnote 21 All companies interviewed in the survey expected to license their patents as a percentage of the sales price of an end-user device, rather than the price of any specific component.Footnote 22 Similarly, Putnam and Williams examined the licensing practices of the leading contributors to 2G, 3G, and 4G standards and found no evidence that a component or a combination of components were used as a metering device for the calculation of the royalty rate.Footnote 23 This led them to conclude that in the telecom sector, licensors and user equipment sellers do not rely on any specific component to measure the value of licensed technology. Even Qualcomm, a leading component processor manufacturer, negotiates licence payments based on the user equipment price in addition to the component price.Footnote 24 This finding is notable because it indicates that the value of licensed technology in the telecom industry is primarily based on the end-product rather than any individual component. However, it does not follow automatically that this approach should be applied in the connected car industry. The connected car’s hybrid nature, often likened to a “smartphone on wheels”, poses challenges in defining a standardised approach for this unique sector.

Pricing debates have given rise to the creation of two opposing blocks, in the academic literature as well as in practice.Footnote 25 Those in favour of component-based licensing and those in favour of end-product-based licensing present completely contrasting arguments, and we examine these arguments before presenting our own stance in the next section. It is important to note that there may be some overlap between the licensing level and royalty base in the arguments presented by both sides.

6.1 Total Economic Value of Connectivity

According to the European Commission, licensing terms must bear a clear relationship to the economic value of the patented technology.Footnote 26 In this context, determining a FRAND value should require considering the present value added of the patented technology. That value should be irrespective of the market success of the product which is unrelated to the patented technology.Footnote 27 In addition, a FRAND valuation should ensure continued incentives for SEP holders to contribute their best available technology to standards.Footnote 28

The meaning and the magnitude of the added value depend on the context of valuation and the market. Heiden explains that a good or service in an economic system may create value to social actors, producers, consumers, and society as a whole, and he accordingly examines three different values, i.e. total market value, total economic value, and net social value.Footnote 29

Briefly speaking, total economic value as the value provided by a good or service in terms of satisfying individual needs is often expressed in monetary terms and is determined by factors including supply and demand, production costs, and the perceived utility of the good or service. Total market value focuses on the price at which a good or service can be bought or sold in a particular market, and net social value englobes the overall impact of a project or decision on society as a whole, taking into account a range of social and environmental factors.Footnote 30 Economic value is an important concept in economics and business because it helps to determine the price that consumers are willing to pay for a product and the profits that companies can expect to earn from producing and selling it.

The estimation of the value of technology is challenging basically because pure technology markets in which market prices can be obtained do not exist. This is especially the case for enabling technologies and multi-technology products, including automobiles or mobile subscriptions.Footnote 31 When the value of technology cannot be defined by market transactions, it must be determined through an inspection of the contribution it has to the value for the consumer, that is, its value-in-use (VIU). Technology-based innovation generally generates value through either improvement to existing products and services, providing efficiency and performance benefits to existing value propositions (e.g. anti-lock brakes, more fuel-efficient diesel engines, or advanced navigation systems), or creation of new products, services, or business models (e.g. ride-sharing apps, over-the-air updates, and autonomous driving).Footnote 32

One may argue that what is paid to a TCU designer by a car manufacturer should be considered as an indication of the TCU’s economic value, that is, the price that the consumer is willing to pay. This is in fact Daimler’s argument, suggesting the car manufacturer as the consumer and the supplier as a licensee where the licence fee should be based on the sales price of the supplier.Footnote 33 This view leads to the same result as the component-based royalty rate.

Connected vehicle services encompass a broad cross-section of growing interrelated value propositions for their consumers and manufacturers, including convenience, safety, security, time savings, cost savings, entertainment, comfort, and vehicle management features, among others. Therefore, it seems to be more relevant to regard the connected car buyer as the main consumer, and the price that the buyer is willing to pay is an indication of the TCU economic value. Nevertheless, the value of the connected car, i.e. its market price, should not be simply considered as the royalty base due to the fact that this price is often impacted by the adjunct optional equipment attached to the product. An example can be gold-plated smartphones, or luxury connected cars equipped with pricy decorations, which makes it impossible to determine what part of the market price represents SEP value, and what part the value of the additional or optional attachments.

6.2 Full Functionality of SEPs

Those in favour of component-based licensing assert that components, such as modems, best represent a standard’s functionality and the value of standardised technology. They argue that communications standards for cellular 3G, 4G, 5G, and wireless are implemented at the component level, specifically at the baseband chip level.

On the other hand, advocates of end-product-based licensing contend that end-products, such as smartphones, accurately reflect the true value of the standardised technologies as their functionality is fully realised in the end-product device. They maintain that the standard value depends on its downstream use, and that basing royalties on the final downstream device acknowledges this distinction. They often point to the price difference between an iPad and an iPhone, both with almost the same features but with different connectivity capabilities, and thereby different prices, to illustrate this point.Footnote 34

Proponents of component-based licensing express concern that licensing at the end-product level would allow SEP holders to capture value created by unrelated components (e.g. cameras in a mobile device) or technologies (e.g. software that relates to the operating system of a smartphone), leading to unjustifiable over-compensation and hold-up. In the same context but in a different direction, supporters of end-product-based licensing believe that component-based licensing would devalue SEPs, harm innovators, and disincentivise participation in standard development, as enforceable royalties may be driven down.

We recall that in the connected car industry, contrary to smartphones, the car as the end-product does not reflect the true value of the standardised telecommunications technology, as it comprises numerous elements one of which is the TCU. It is actually the TCU, i.e. the component, that reflects such a value as its functionality is fully realised thanks to the cellular technology.

6.3 Smallest Saleable Patent Practising Unit

Proponents of the licence to all (component-based licensing) argue that the smallest saleable patent practising unit (SSPPU) is the right royalty base. They argue that determining the value of patented technology should follow a similar methodology to the calculation of damages in patent law. In essence, this approach considers the value associated with the infringement of the specific patented component in question. They argue that U.S. patent damages law requires the use of SSPPU in the calculation of damages where a product has multiple components.Footnote 35

The courts have stated that the SSPPU is simply a step towards meeting the requirement of apportionment, and patent holders must estimate what portion of the value of a multi-component product is attributable to the patented technology.Footnote 36

The U.S. antitrust agencies acknowledge the use of the SSPPU approach for setting FRAND royalties. The FTC recommended the SSPPU where the invention’s contribution is a large and complex product.Footnote 37 It referred to Cornell v. Hewlett-PackardFootnote 38 where the court chose the processor as the base where it was the smallest priceable unit. The U.S. Department of Justice (DOJ) also stated, in the Business Review Letter on the Institute of Electrical and Electronics Engineers’ (IEEE) policy of 2015 (the 2015 Letter), that the SSPPU method proposed by the IEEE may be appropriate in calculating a royalty that is correctly tied to the patented invention, particularly when the product is complex and incorporates many patented technologies.Footnote 39 The DOJ concluded that the update of the policy of 2015 on a reasonable rate provides a clearer definition of a “reasonable rate” which may help speed up licensing negotiations and limit patent infringement litigation. It helps ensure that reasonable royalties for essential patents compensate the patent holder for the value attributable to the patents, which is consistent with the U.S. case law.Footnote 40

On the other hand, proponents of access to all (end-product-based licensing) refuse the SSPPU as a royalty base. They refer to the update of the DOJ on the Business Review to the IEEE Policy. In this update (the 2020 Letter), the DOJ emphasised that the 2015 Letter was not an endorsement of the IEEE policy and this misinterpretation has influenced some competition authorities outside the U.S., leading to several enforcement actions against SEP holders, while it has no basis under U.S. law.Footnote 41 The 2020 Letter highlighted that the DOJ had never mandated the SSPPU as the only basis for royalty determination; otherwise the implementers are less likely to accept royalty payments based on the entire market value, since they can always (after a judicial proceeding) receive the smaller adjudicated royalty. In the 2020 Letter, the DOJ fully changed its view, stating that while there are a variety of ways parties might value patented technology, the end-product is the basis in real-world licences, and it is the most effective method of estimating an asserted patent’s value. The DOJ stressed that the recommendation of the IEEE’s policy for using the SSPPU in the absence of other bases would bear on the parties’ licensing negotiations and discourage them from using an end-product basis.Footnote 42

The 2020 Letter stated that the SSPPU is one of the possible tools for courts to set a royalty rate and particularly for jury-trial litigation.Footnote 43 Similarly, the Ninth Circuit in FTC v. Qualcomm reiterated that “no court has held that the SSPPU concept is a per se rule for ‘reasonable royalty’ calculations; instead, the concept is used as a tool in jury cases to minimize potential jury confusion when the jury is weighing complex expert testimony about patent damages”.Footnote 44 In this respect, the rule for calculating damages does not necessarily have to mirror the rule guiding negotiations between parties for licensing agreements.Footnote 45

This discussion makes it evident that the DOJ changed its policy in this regard, as in 2015 it was inclined towards implementers, but in 2020 the policy shifted towards SEP holders. In addition, Putnam argues that the concept of the SSPPU is an arbitrary approach to limiting a patentee’s damages and lacks a basis in economic theory or data.Footnote 46 In complex devices where components work synergistically, the SSPPU fails to capture the incremental value added by the invention, rendering it inadequate to measure an invention’s economic impact.Footnote 47 For instance, in the telecom sector, some licensees of SEP portfolios propose that the royalty base should be limited to the baseband processor. However, this strategy attempts to manipulate the size of the total payment by defining the royalty base improperly, without any economic analysis of the causal relationship between inventive input and economic output.Footnote 48 Additionally, improvements to a single input affect the value of the output, as well as the contributions made by other inputs. This increase in value is not necessarily reflected in the price of the improved input itself, especially when the input’s manufacturer does not account for a royalty or other cost of using the invention. Finally, the terms of actual licences can reveal essential information about how industry participants view the causal relationship between licensed inventions and their increment to output. For example, in the telecom sector, agents often choose the value of user equipment that includes a baseband processor as a royalty metering device, recognising that standard-implementing inventions often operate synergistically to increase the user equipment’s value.Footnote 49 Putnam concludes that the question of whether a given component is saleable, at what price, when and by whom, is influenced by a range of supply chain decisions and other business considerations that are causally unrelated to the use and impact of the invention.Footnote 50

These complexities make it challenging to define and measure an intermediate royalty base and require careful consideration in cases where such comparisons are necessary. In addition, the precondition to use the SSPPU as an evaluator of a licensed patent is that the component that allegedly embodies the patented invention is saleable. In fact, to determine the appropriate royalty base for a component, it should be assessed whether it is independently saleable on the open market. If this is the case and its price is known, the royalty can be based on that price. In contrast, if the component is only intended for use in end-products or has been designed by end-product manufacturers, the component price becomes just one element among others in the agreement between the commander and the supplier, which may also involve payment terms, warranties, quantities, lead times, and other commercial details. In such circumstances, licensors generally do not have access to an accurate and verifiable price of components.

6.3.1 Is a TCU Saleable?

In the automotive industry, a TCU is an embedded system on board a vehicle that wirelessly connects the vehicle to cloud services or other vehicles using V2X standards over a cellular network. The TCU gathers telemetry data from the vehicle, including information about its position, speed, engine data, and connectivity quality, by interfacing with various sub-systems over data and control busses within the vehicle. Additionally, it may offer in-vehicle connectivity using Wi-Fi and Bluetooth, and provide the eCall function in applicable markets.Footnote 51

A TCU comprises several components such as a satellite navigation unit, an external mobile communications interface, an electronic processing unit, a microcontroller, a microprocessor or Field-Programmable Gate Array (FPGA), and a memory. The TCU tracks a vehicle’s latitude and longitude and sends them to a centralised database server. The TCU can also process the information and store GPS coordinates in its memory when no mobile coverage is available and do the same thing for the vehicle’s sensor data.Footnote 52

In the Daimler case, Daimler argued that the TCU component is a saleable terminal as a mobile station based on its technical functions, but the Mannheim court rejected this argument.Footnote 53 The court explained that connectivity components such as a TCU are only utilised when installed in a vehicle and connected or interacting with other electronic components. The invention’s relevance is not fully realised in the component alone and can only be realised through installation and connection with other components in the vehicle, where all benefits can only be achieved after the connectivity module is installed in the vehicle. In this context, the court concluded that the TCU cannot be considered as saleable terminal equipment and cannot therefore be the basis for royalty calculations; instead, it is the smallest technical unit.Footnote 54

Whether or not a TCU is considered a saleable component depends on various factors, such as its technical specifications and intended use. In general, if a TCU is designed and manufactured to be installed and used specifically in a particular type of vehicle or as part of a larger system, it cannot be considered a saleable component. The TCU may then be seen as a component of the larger system and its value may be included in the overall value of the system, rather than as a standalone product. On the other hand, if it is designed and manufactured to be sold as a standalone product that can be installed and used independently of other devices, then it may be considered a saleable component. A Google search shows that the market for 5G ready-to-use TCUs will be valued at a significant $33,105.5 million by the end of 2023 and is expected to grow at a rate of 26.6% from 2023 to 2033.Footnote 55 This indicates that there are many suppliers in the market for telematics units, not just limited to Tier 1 suppliers, and that these products are in high demand.

6.4 Transaction Costs

Transaction costs are a useful indicator to identify a better royalty base as, in addition to being desirable to society, reducing the costs related to the negotiations for a licence is in line with the EU Commission’s goal.Footnote 56

From the perspective of minimising transaction costs, defining an optimal licensing level of cost is of great importance. But selecting such a level for SEPs requires careful consideration of various factors, given that transaction costs depend largely on the technology at issue and the type of product.Footnote 57

In a complex value chain with patents at different levels, licensing at a single level can save on transaction costs by reducing the number and the complexity of negotiations. When SEP holders own several patented technologies included in the same standard, licensing at a unique level in the value chain can prevent double-dipping and over-compensation, as required by patent exhaustion. There may, however, be asymmetric information about patents between SEP holders and licensees, which may result in royalties being charged for the same patents at multiple levels. This can lead to under-compensation if SEP users in the middle of a supply chain refuse to take a licence, claiming that all relevant SEPs are implemented at the end-product level, while end-product manufacturers also refuse, claiming that all SEPs are implemented at the component level in the middle.Footnote 58

Langus and Lipatov suggest that SEP holders typically target the level where most of their SEPs are implemented and trust them to choose the licensing level that minimises transaction costs and maximises total output.Footnote 59 To evaluate this approach in an IoT context, comparing licensing costs at different levels can provide a useful benchmark. In the IoT, licensing at the component level may be preferable if there are fewer licensees in the middle than at the manufacturers’ end-product level, potentially leading to lower costs. In this context, Geradin highlights the importance of considering the vast number of OEMs in the IoT space, cautioning that licensing at the end-product level could increase transaction costs and result in inefficiencies.Footnote 60 Henkel similarly argues that licensing should take place at the upstream level where transaction costs are minimised,Footnote 61 emphasising the smaller number of component makers and accordingly fewer licence agreements, thus minimising transaction costs. On the other hand, Heiden et al. raise the point that component makers may struggle to pay a FRAND rate and may lack the necessary information to enforce licensing agreements at the middle level.Footnote 62 Additionally, due to the difficulty in identifying which patents apply where, downstream licensing becomes a more appealing option for reducing transaction costs. They also argue that moving licensing upstream may lead to challenges in setting SEP royalties based on different use-cases, resulting in higher monitoring and auditing costs.Footnote 63

Factors that favour downstream licensing include reducing double marginalisation, limiting the exposure of integrated firms, and managing risk. Licensing at the midstream level can have advantages too, particularly when there is a high risk of hold-up.Footnote 64 When selecting the licensing level, it is essential to consider the use-case and industry-specific factors. If a large portion of patents applies to both levels of the value chain, it may be beneficial to only license downstream to minimise transaction costs. In contrast, licensing midstream may be preferable when midstream suppliers have limited bargaining power and cannot pass along royalties charged by licensors to their downstream customers.Footnote 65 To deal with uncertainty, licensors can commit not to enforce their patents on firms operating upstream of the licensing level, or they can include have-made rights and exceptions in their licences to protect midstream firms. It is also important to prevent a complex web of licensing agreements by not dividing up SEP portfolios.

7 Discussion and Proposal

We recall that determination of the royalty rate in multi-tier IoT value chains is challenging and the interests of the licensor and licensee may fall into deep conflict. The licensor would like to license to the end-product manufacturer in the hope of having a more interesting licence agreement, while component makers who are practically engaged in the design and production of the component see their right to have a licence, but in a component base which may not be attractive from the licensor’s point of view.

In contrast to the IoT, licensing for cellular standards in the mobile communications industry has long been established where licences are typically concluded with end-product handset manufacturers like Samsung and Apple, rather than component manufacturers such as chipset makers.Footnote 66 Some suggest applying the same practice to the IoT value chains. The proponents of this practice (end-product-based licensing) argue that SEPs have been licensed traditionally at the end-product level, which is, according to them, the most appropriate representation of the value of the standard.Footnote 67 They find it more straightforward to give a licence to a party who is directly in contact and engaged with the end-consumer as the ultimate payer for the product. In their logic, if the end of the chain gets a licence, he can set the end-price accordingly and sell the good directly to the consumer.

Conversely, for the advocates of a licence to all (component-based licensing), licensing at the end-product level is not necessarily the best practice in other sectors, including vehicle manufacturing, where OEMs expect to receive third-party rights-free components. The distinction between mobile and connected car industries becomes more vivid if one notes that in the car industry, the end-product maker (e.g. as we saw in Daimler) typically does not design the cellular components it needs, while in the mobile industry, end-product manufacturers (e.g. Apple or Samsung) perform the full design of the product. In fact, a car manufacturer may neither have the knowledge about the SEP in question, nor any incentive to develop the technology. In addition, the end-product market price, which is the royalty rate base in the access-to-all approach, is not necessarily determined by the mere number of SEPs used in the final product but is often increased by the adjunct optional equipment attached to the product. Here, an example can be connected cars equipped with pricy decorations or enhanced comfortability options that make it far more difficult to determine what part of the market price represents the SEPs’ value, and what part the value of the additional or optional attachments.

7.1 Examples of Licensing at a Component Level

Despite the general practice of licensing SEPs at the end-product level, there are some cases where licensing occurs at the component level. For instance, Motorola has licensed some of its telecom SEPs to several chipset and component suppliers, including Qualcomm; and Ericsson has licensed not only to smartphone manufacturers, but also to component suppliers such as Qualcomm.Footnote 68 It is worth noting that SEP licensing can also involve licensing between component suppliers, as exemplified by Qualcomm’s licensing of its modem chip to other chip producers.Footnote 69 However, it is important to acknowledge that these licensing agreements between competitors often occur through cross-licensing schemes that are unrelated to our Daimler context where the SEP holders are not vertically integrated in the market. In such a context, the case of Blu-ray is an interesting example as it shows how licensing arrangements can be influenced by the complexity of the value chain and can happen at both the upstream and downstream level.

Blu-ray licensing typically targets end-product makers, i.e. manufacturers of Blu-ray player sets or recorder sets. However, licensing in some cases occurs at the upstream level too, such as with drive manufacturers, software providers in the PC industry and so forth, as well as disc pressers in the content industry. This occurs due to the complexities involved in the Blu-ray value chain which involves multiple players across different industries. By licensing at upstream levels, the Blu-ray licensing organisation can ensure that all essential patents are licensed and that the value chain operates smoothly. This approach helps minimise potential conflicts and ensures that all players involved in the Blu-ray ecosystem have the necessary licences to operate within the standard.Footnote 70

The SEP Expert Group explains that SEPs have varying licensing schemes depending on technology standards.Footnote 71 For consumer products like TV sets, CD/DVD players, and mobile phones, licensing at the end-product level has been typical. However, for standards such as MPERG1/2/4, HEVC, and other audio and video compression technology, licensing can differ depending on the types of products that incorporate these SEPs,Footnote 72 or the licensing mechanism through various patent pools.Footnote 73

It should be noted that in terms of setting the royalty, the component base and end-product base share the same principle, i.e. both suggest that the rate should be calculated based on the product price. However, while the end-product has a very clear market price, there is often no such price for the component itself.Footnote 74

This section showed that although there are some general licensing schemes for SEPs, different practices exist depending on technology standards and the complexity of value chains.

7.2 Importance of Industry Practice

Industry practices are considered to be a factor by courts when determining licensing issues. In the Intellectual Ventures v. Vodafone case,Footnote 75 the court determined that licensing to network operators was not consistent with prevailing industry practices in the sector, where licensing to end-product manufacturers was the norm. The case involved a dispute over licensing terms for a portfolio of SEPs related to wireless communications. Intellectual Ventures was the owner of the patents and had offered Vodafone a licensing deal, which Vodafone had rejected. The court’s ruling was based on a number of factors, including the fact that licensing to network operators was not consistent with prevailing industry practices in the sector. The court noted that the customary practice in the wireless communications sector was for SEP holders to license to end-product manufacturers rather than network operators. The court also found that the terms of the licensing offer made by Intellectual Ventures to Vodafone were not in line with prevailing licensing practices in the industry and were therefore not FRAND.

At this stage, one may wonder how a case would unfold if it involved two different industries, such as for connected cars that involve both the automotive and telecommunications industry. We need to know if licensing practices in one industry can be extended to the other. There are differing views on this matter. One perspective suggests that device-level licensing is reasonable for smartphones since end-product manufacturers, or more correctly OEMs, possess knowledge of the relevant cellular technologies, which allows them to negotiate with SEP holders on an equal footing. Additionally, connectivity is central to the functionality of mobile devices and OEMs may themselves hold SEPs, which could lead to mutually beneficial cross-licensing arrangements. Conversely, for industries where connectivity is not core to the end-product’s functionality, such as home appliances or medical devices, the default may well be upstream licensing, namely licensing at the level of the value chain where the relevant patents are first implemented.Footnote 76

The clash of views was evident in the Daimler case where different German courts took different positions. The Mannheim court ruled that upstream licensing was common practice in the automotive industry but did not obligate Nokia, the SEP holder, to adopt a corresponding approach.Footnote 77 The Munich court ruled that to the extent that Daimler’s products are increasingly moving from the area of classic automobile construction to the area of mobile communications, Nokia is not obliged to respect the practice and customs in the automotive industry, but instead Daimler must accept telecom customs as a matter of principle. Therefore, if in the latter the common practice is to license to the end-product manufacturer, Daimler must generally accept this against itself.Footnote 78 However, the Düsseldorf court emphasised the importance of each level being responsible for the legal conformity of the technical solution they develop.Footnote 79

7.2.1 Contradictory Judgments over Prevailing Industry Practice

Even if a common practice for the telecom industry/ETSI could be agreed upon, there still exists another substantial problem as one may ask if such a practice can be applied to other industries, including the automotive industry, which use cellular communications but have different practices and business models. This was in fact one of the preliminary queries posed to the ECJ, as the Düsseldorf court sought clarification on whether customary trading practices play a decisive role in determining the licensing level.Footnote 80

Given the vast number of subcomponents involved, the standard practice in the automotive industry is to license at supplier level rather than the OEM, as in this way the subcomponents are free from third-party rights when delivered to the OEM. The Düsseldorf court justified this practice by noting that the level in the chain that selects a specific technical solution is responsible for the legal conformity of the solution it develops itself and is therefore better positioned to determine whether such a solution infringes third-party property rights.Footnote 81 Since a typical motor vehicle contains up to 30,000 components, it would be very hard for a car manufacturer to verify whether the technical solutions installed in the car and supplied by third parties infringe third-party property rights.Footnote 82 The more complex the supplier part is and the further removed the technology is from the actual field of activity of the car manufacturer, the more acute the problem becomes, such as for the TCUs and NADs in question here.

The Munich court in Daimler held that Nokia is not obligated to respect Daimler’s customary practices or to engage in the licensing practices that are in line with previous habits and customs in the automotive industry, including Daimler’s classic business model.Footnote 83 In contrast, it is Daimler that needs to respect the practices and customs of the mobile communications industry as its products are moving away from the domain of conventional automotive engineering and getting more into the area of mobile communications. If the prevailing practice there is to license end-product manufacturers, Daimler must accept it.Footnote 84

The Munich court’s decision had implications for Daimler, as it required it to be aware of the prevailing licensing practice in the mobile industry, and to align its customary practice with those in that market.

Likewise, the Mannheim court in Daimler ruled that the automotive industry’s practices do not compel Nokia to adopt a corresponding approach.Footnote 85 When some Daimler suppliers cited various well-known licences executed with suppliers, the court challenged that those agreements do no cover connectivity in vehicles.Footnote 86 Dismissing the suppliers’ argument,Footnote 87 the court referred to the Avanci patent pool’s practices under which several car manufacturers have obtained licences for connectivity standards at the end-product level.

This discussion makes it clear that although industry practices are informative in understanding licensing approaches across different sectors, they cannot simply be applied to other industries. Determining which practices should be applied to complex value chains, such as those in connected cars, is challenging. Even in cases with the same facts and circumstances, like Daimler, German courts have diverged and suggested different approaches.

7.3 Proposal

Despite the apparent difference between these two licensing approaches in the value chain, i.e. component-level licensing and end-product licensing, they share the same view towards setting the rate, that is, they pay a great deal of attention to the “geometry” of the chain in the sense that they suggest the royalty should be paid either upstream (component maker) or downstream (end-product manufacturer) only because of their place in the chain regardless of their role in the creation of the component or in implementing the technology. That is why there is a great deal of work in the literature around the relation between the components (upstream) and end-products (downstream), and on whether or not the SEP holder is integrated in the downstream market and so forth.

7.3.1 Licensing Level

We believe that there could be a third approach following which no matter what the position of a player is in the chain, his rights in terms of the licence and his duties in terms of the royalty can be defined by his function in the creation of the component. And it is in this functionalistic context that we propose that the royalty must be paid by whoever implements the connectivity technology into the device, where implementation of a technology in a product means the design of that product using that technology carried out by a designer who owns and supplies all the specifications, including the working drawings, which are complete and sufficient so that no substantial additional design, specification or drawing is needed for making the component.

The functionalistic approach revolves around determining the rights and obligations of individuals within a system by considering their specific functions or roles in the creation process. Rather than focusing solely on hierarchical positions, this approach emphasises the contributions made by each player towards the development of a component. It suggests that regardless of their position in the production chain, individuals should have their rights and duties delineated based on their functional involvement. For instance, in the implementation of connectivity technology in a device, the functionalistic approach advocates for royalties to be paid by the entity responsible for integrating the technology into the final product. This payment is based on its role in designing and providing comprehensive specifications for the component, ensuring that all necessary details for its manufacture are included.

Within such a framework, we can formulate our approach as follows: the party who carries out the design of a component using a wireless communications technology which is to be integrated later into an end-product is seen as the implementer of the SEP, thereby the one who must be considered as the legitimate licensee.

It should be noted that the distinction between design and manufacture in our approach is crucial as a designed TCU may be manufactured directly by its designer or later by someone else in the chain. The manufacturer level in our view is not, however, decisive in determining who should assume the royalty. If we apply our approach to the Daimler case, we can suggest that whoever had designed the TCU (as the component using the LTE technology) should take the licence, whether it was the Tier 1 or Tier 2 supplier, or even Daimler itself (if it had been the designer in the Daimler context, although it was not).

This approach is logically supported by the following facts:

Full functionality representation of SEPs: In the connected car industry, contrary to smartphones, the car does not represent the true value of the implemented cellular technology, as it is composed of numerous pieces one of which is the TCU. It is actually the TCU that reflects such a value as its functionality is fully realised by the cellular technology.

Licence for the party who legitimately needs it: It is only the design that defines the component characteristics that ultimately determine its functionality in the end-product. When the design is completed, the component manufacture just follows a procedure to assemble the electronic elements on a board and embed them all in a deliverable form that can be attached to the internal structure of the end-product. With regard to the TCU, the designer defines the requirements and capabilities of the device, including supported network protocols and the type of data needed to be transmitted. The TCU designer also specifies the device Quality of Service (QoS) parameters, such as bandwidth required, the level of traffic prioritisation for different types of data, and the maximum latency or packet loss allowed to ensure that the device operates efficiently and effectively within the specified network environment.Footnote 88 Therefore, the implementer’s (designer’s) function is crucial in bringing a technology from concept to reality and making it available for use by consumers and businesses. They are responsible for ensuring that the technology meets the necessary standards and requirements, and for making it accessible and usable by the target audience.

Innovation promotion: The design is the first step in the commercial success of the implementation of a technology in an end-product. If the implementation is successful, the market will demand further development of the implementation. In such a circumstance, the designer must be able to develop his design freely and independently. If a licence is granted to the end-product maker, the supplier’s innovation will be restrained by the interests of the licensee whose commercial interests may be different.

Social benefit and device efficiency: If the component’s technical characteristics can be introduced into the calculation of the royalty rate such that for a more efficient component its designer pays a lower royalty rate, he will normally be incentivised to design more efficient devices if in addition to all benefits that such a device can bring for society, it subsequently allows him to pay a lower royalty. This subject is broadly discussed in the following section.

7.3.2 Royalty Base

After agreeing that the designer is the right entity to take the licence, the issue of the licensing level is resolved. The next step is to define a basis for the royalty based on the technological characteristics of the component. As mentioned earlier, the price is the ultimate rationale in most SEP licensing litigation, if not all; and all the back-and-forth disputes over who should take the licence arise because, due to the lack of clarity in terms of the rate base, a possibility always exists for the parties to negotiate in the hope of having a greater piece of the cake.Footnote 89 If this possibility becomes restrained (or ideally blocked) by suggesting a range for the rate, the parties will be less keen to consider litigation.

In the following, we will show how a base for royalty can be defined by taking the component’s technical characteristics into account.

7.3.3 Technology-Based FRAND Rate

We believe that for licensing in the IoT context to be FRAND, the royalty rate collected from the technology implementer (device designer) should be defined proportionate to technically measurable factors that the component at issue requires in order to perform as designed. For this purpose, these factors should be specific parameters or criteria within a technical context that can be quantified or assessed objectively and be able to provide precise measurements and comparisons between different products. In the IoT, technically measurable factors may be represented by the Quality of Service (QoS),Footnote 90 which encompasses metrics including bandwidth requirements or other quantifiable characteristics that determine the performance or functionality of a device and its level of use from the Long Term Evolution (LTE) technology. To determine royalty rates for technology implementers to ensure fairness and proportionality in licensing agreements, one or several of the parameters involved in the QoS evaluation can be taken into account to quantify the demand of the component for service. Among them, the best option seems to be the required bandwidth which is a measure of the device’s capacity to transmit data. In this context, the device demand is defined as its requirement for data exchange with respect to what the LTE technology offers to a reference user.

The mobile phone industry is historically the first client for which the LTE technology was originally developed to serve, and its development over decades has been fulfilled in order to enhance the mobile phone communications experience by passing from 2G in 1998 to 5G today. This fact lets us consider the mobile phone industry as the reference user of the LTE technology among all its other users, including the IoT, and the rate paid by them as the reference rate.

Within this framework, the FRAND royalty rate would be set such that the rate paid by a component designer would be proportional to the component demand for data transmission and calculated based on the reference rate paid by the reference user for the level of data exchange defined for the reference device. Such a logic can be mathematically described as follows:

where \({R}_{IoT}\) is the royalty rate to be paid by the component designer, \({R}_{ref}\) is the reference rate paid by the reference network users, i.e. mobile phone manufacturers; \({X}_{IoT}\) and \({X}_{ref}\) denote the data exchange rate requirements defined for the IoT device and the mobile phone, respectively.

In this context, if the IoT device requires the same data exchange rate as that for mobile phones, i.e. \({X}_{IoT}={X}_{ref}\), then \({R}_{IoT}={R}_{ref}\): it is FRAND if the SEP holder asks the component designer for the same royalty as that paid by the mobile phone manufacturers. On the other hand, a \({X}_{IoT}{X}_{ref}\) leads to \({R}_{IoT}{R}_{ref}\), and vice versa.

This definition for the royalty rate allows the incorporation of the device functionality into the calculation. For example, a connected car uses cellular connectivity frequently and to a fuller capacity than a smart refrigerator which would use connectivity only occasionally and with limited functionality. To show how the proposed base can treat functionality differently, two numerical examples are provided in the following.Footnote 91

Example 1: A TCU in a connected car can generate a tremendous amount of data, but not all these data need to be transferred to the cloud other than a very tiny fraction of which would be at the highest value of around 200 megabytes an hour, hence \({X}_{IoT}\) = 200. On the other hand, the average data consumption of a mobile phone is about 30 megabytes an hour, hence, \({X}_{ref}\) = 30. Therefore, the order of magnitude of the royalty rate which the licensor can expect to gain from the component designer can be estimated as follows:

That is, six times the reference royalty rate that is paid by iPhone or Samsung for their smartphone industry.

Example 2: The amount of data produced by a connected refrigerator, which may vary depending on the specific model and usage patterns, could range from a few megabytes per day to several gigabytes per month. Like connected cars, the data generated by a connected refrigerator are usually stored and processed locally, with only a small amount of data being transmitted to cloud-based servers for remote monitoring and analysis, which is some value in the order of ten megabytes per month, i.e. 0.015 megabytes an hour (\({X}_{IoT}\) = 0.015). Therefore, the SEP holder may expect a royalty in the order of the following rate:

This suggests that the order of magnitude of the royalty rate that can be sought by the licensor from the SEP implementer in the smart refrigerator chain is about one two-thousandth of the reference royalty rate paid by the mobile phone manufacturers.

7.3.4 Value of Innovation

SEP holders can argue for a greater share than the \({R}_{IoT}\) calculated above with the justification that the IoT success is the outcome of their innovation in creating the cellular technology. One needs to distinguish between two innovations here: the historical, which was made when inventing 4G (licensor’s innovation), and the actual IoT which is made now by inventing the idea of connected devices (manufacturer’s innovation, e.g. Daimler).

The success of connected devices in the market is not the mere result of wireless communications technologies integrated in the device, but is the outcome of the brilliant idea made by the people who envisaged that such a product can win in the market.

When LTE or Wi-Fi developers presented their technologies two decades ago, they had no idea that one day their inventions might have such vast applications. If IoT devices owe something to LTE and wireless technology, it is merely because these technologies provide a ground where new ideas, including the IoT, could take root and evolve, just like the idea of the internet itself; and if we go further back in history, we can think of electricity. Without electricity, the internet or LTE, none of this new IoT would be achievable. However, it does not mean that the inventors of internet-related technologies (like https protocol or VPN) or LTE can claim a direct financial share in the victory of an innovation (e.g. connected cars) of which they were never an active part. What is fair is that SEP innovators should enjoy a benefit proportional to their contribution to the success of the IoT. The presented formula can also be interpreted as an attempt to relate the share of the SEP holder in the success of the IoT (\({R}_{IoT}\)) to the extent that the IoT owes to the technology developed by the SEP holder (\({X}_{IoT}\)).

7.3.5 Future Development

It should be noted that the proposed formulation is one of the possibilities to implement a pro rata royalty rate. What is important is to set a base for the rate proportional to the technical characteristics of the component. Issues such as using what reference rate values with which this proportionality is better computed, or whether or not this value is publicly available, are beyond the scope of this research. The EC in the Proposal on an SEP Regulation suggests that the aggregate royalty (i.e. total maximum price) should be set using a standard before or shortly after its publication.Footnote 92 If this takes place, this definite aggregate rate can replace our reference rate. On the other hand, each generation of the LTE has a nominal data transmission capacity that is listed in the patent claim. This nominal value can also replace the reference exchange rate in the above formula. But until then, the above suggested reform seems the most efficient given the state of the art for the time being in the connected car industry and other IoT sectors.

7.4 Comparison of Existing Approaches with Our Approach

The main existing approaches outlined in the literature can be summarised as follows:

-

1.

Royalty based on product economic value: In the IoT context where connectivity standards are the product, the challenge lies in determining the total value of connectivity. This approach proves unhelpful as the product price does not necessarily reflect the value of connectivity. For example, two smartphones with different prices may offer the same connectivity level.

-

2.

Royalty based on full product functionality with integrated connectivity: As elaborated earlier, this approach determines the royalty based on the total value of the end-product, reflecting its full functionality with integrated connectivity. We believe that the final price of a product is influenced by a combination of various tangible and intangible components, all of which contribute to its overall value.

-

3.

Royalties based on smallest saleable patent practising unit: In our context, this requires proving that the component in question (the TCU in the connected car example) is really saleable independently on the market. In reality, however, TCUs manufactured in a value chain are designed to be compatible with and imbedded in a specific end-product, and their special architecture does not allow them to be compatible with other end-products (vehicles).

In contrast, our approach proposes that royalties should be proportionate based on the QoS provided by the component designer/implementer. We consider the total economic value of connectivity but focus on the characteristics of the device rather than the price of the end-product. Among many factors, we suggest considering data transfer to the cloud as a measurable metric, with potential environmental benefits. Furthermore, our approach provides a framework for determining relative royalty rates. For example, a TCU component designer/implementer should pay more than an SEP chipset implementer in a smartphone but less than an IoT component implementer in a refrigerator. This logic is based on the differing usage of connectivity technology across products, with TCUs transferring more data to the cloud. This quantitative approach enables the establishment of meaningful and equitable FRAND royalty rates, providing a starting point for negotiations between SEP holders and a wide range of connectivity implementers in the IoT sector.

7.5 Evaluation of Our Approach Under the EU Commission’s Proposal on an SEP Regulation

The EU Commission highlighted that a combination of uncertainty and high transaction costs are the overarching problems in the SEP/FRAND context. Our approach aims to address these two problems by proposing a functionalistic model for determining licensing and royalty obligations. By defining rights and duties based on the function of each player in the creation of the component, this approach seeks to streamline negotiations and reduce the transaction costs associated with SEP licensing. The Commission stated that there are a number of principal drivers of the above problems as outlined in the following, where for each item we discuss the advantages of our proposed approach.

7.5.1 Challenges Faced by SEP Holders and Implementers

Our approach acknowledges the challenges faced by both SEP holders and implementers, as highlighted by the EU Commission. It proposes a solution where royalty obligations are determined by the party responsible for implementing the connectivity technology in the device, that is, the party who designs the component and defines the QoS for it accordingly, thus potentially alleviating some of the negotiation burdens faced by both parties.

7.5.2 Lack of Information About FRAND Royalties

Our approach seeks to address the lack of information about FRAND royalties by proposing a mechanism where royalty rates are proportional to the QoS requirements of the component. This ensures that implementers can assess the reasonableness of an SEP holder’s royalty demand based on objective technical criteria.

7.5.3 Time- and Cost-Intensive Legal Proceedings

Our approach aims to mitigate the time- and cost-intensive nature of legal proceedings in the SEP context by promoting a model where the determination of the royalty is proportionally determinable based on the usage of the technology at issue. Under this approach, parties know the proportional range of the rate and, therefore, they know from which rate they may start their negotiations. We believe that this could potentially reduce the need for protracted legal disputes.

7.5.4 Impact on the Market and Innovation

Our approach recognises the potential impact of SEP licensing issues on market competitiveness and innovation, echoing the concerns raised by the EU Commission. By proposing a more streamlined and transparent approach to the determination of the royalty, this model seeks to foster innovation and ensure sustainable competitiveness in the market. In addition, we recognise the innovation of implementers who have the innovative capacity to design a new SEP-encumbered component. This approach acknowledges the hidden or less evident innovation on the part of the implementer.

7.5.5 Need for EU-Wide Rules on Transparency

Our approach aligns with the Commission’s proposal for EU-wide rules on transparency regarding SEPs and FRAND terms and conditions. By promoting a functionalistic model for determining the royalty determination, our approach advocates for greater transparency and harmonisation within the EU, facilitating the work of national courts and promoting consistency in FRAND determination.

7.6 Final Remarks

We believe that our proposed approach can lead to more legal and commercial certainty and to less litigation. Once the IoT component designer is a licensee and the royalty basis is not only qualitatively FRAND, but also quantitatively proportional to the product technical statistics and its share in the network use, there would no longer be any incentive for a party to litigate if the result is already predictable.

As mentioned earlier, the existing approaches see the value chain from a pure geometrical viewpoint with parties defined based on their place along the production stream, i.e. upstream, midstream, and downstream. This view imposes solutions regardless of the function that each party assumes in terms of implementing SEPs. What courts have done so far was to choose one level as the licensee based on the existing law and accordingly define a base for the royalty, or to propose case-by-case approaches where parties have ultimately resolved their disputes after spending years in litigation, or bilaterally behind closed doors. This is a defective cycle opposed to transparency which has led to endless useless negotiations, litigation, and a lack of legal and commercial certainty.

Under our functionalistic approach the supply chain is seen differently. There is no need to separate the licensing level from the royalty base which typically often overlap. The appropriate licensee is the IoT component designer whatever his place in the value chain, and the royalty base is clear. Remember that our approach will naturally minimise the number of transactions too, as a licensed component maker can participate in several value chains. Given that transaction costs directly depend on the number of transactions, with a reduced number of transactions, the total transaction cost will be reduced as well.

As predominantly designers manufacture components too, our approach outcome aligns with the theory of labour division proposed by Henkel.Footnote 93 He argues that the division of labour, as a keystone of modern industrial production, suggests that responsibility for patent licensing should rest with those parties who understand the technologies that embody the relevant patents.Footnote 94 In many cases outside the smartphone context, this party will be the component maker, not the OEM. A connected car manufacturer has very likely no knowledge of the complex cellular technologies that TCUs may include, and it would be wholly irrational to expect it to invest in acquiring such expertise. In the case of complex multi-component products, the OEM at the end of the value chain may, due to the division of labour, be limited to designing the mere end-product and assembling hundreds or even thousands of components. A car manufacturer may assemble as many as 30,000 components sourced from various suppliers. It is thus no wonder that car manufacturers have traditionally relied on an approach whereby suppliers are expected to deliver their parts free of third-party IPRs; the car manufacturer lacks the knowledge as to whether each of the thousands of components may infringe on third-party IPRs.

On the other hand, a component maker who is the designer of the component clearly has the necessary knowledge about the technology used; hence, it is more efficient that the responsibility over clearing IPRs on his products lies with him. In terms of industry practice, it should be noted that at the advent of the smartphone with Apple’s iPhone in 2007, the complete design was made by Apple itself. In this context, the end-product royalty base was reasonably a prevailing industry practice.

The rapid pace of technological advancements has led to a significant increase in electronic waste. Proportional royalties can help reduce the amount of electronic waste by encouraging designers to create devices that are more energy-efficient and have longer lifespans. When the royalty rate is proportional to the volume of network infrastructure that a device occupies, it can encourage designers to create mechanisms that consume less bandwidth, require less energy, and use fewer rechargeable batteries, or make batteries last longer before the need for replacement. This will lead to more energy-efficient systems that eventually produce less CO2 emissions, contribute to the reduction of waste material, and promote the conservation of natural resources.

8 Conclusion

Connected cars pose a unique challenge for SEP licensing due to the integration of TCUs into vehicles, leading to complexities within the connected car value chains. These multi-tiered structures raise questions about who should obtain licences and at what rates. SEP holders typically prefer licensing to end-product manufacturers, as this yields higher royalties based on a percentage of the final product’s price. Conversely, end-product manufacturers and their suppliers argue that licences should go to the suppliers, with royalties limited to the TCU’s price. This situation played out in the legal dispute between Nokia (the SEP holder), Daimler (the car manufacturer), and its supplier before German courts.

When parties fail to reach an agreement, they often seek court intervention to resolve the licensing base debate. They ask the authority to determine the FRAND-compliant offer, whether before a competition authority or a court. The FRAND commitment provides a strong legal foundation for courts and competition authorities to step in and establish FRAND terms for licences. Regardless of its legal nature, the FRAND commitment serves as the primary legal basis for authority/court involvement in these disputes.

Licensing levels are often linked to the royalty base because licensing downstream can result in higher royalties. However, we propose a different approach to considering the royalty base. We discuss the EU Commission’s requirement that SEP royalties be based on the economic value created by the SEP, which, in the IoT context, is connectivity. We challenge the idea that the end-product price necessarily represents connectivity’s price, considering the various unrelated components that influence an IoT product’s price. Transaction cost criteria may not definitively determine the best level and corresponding royalty base.

This analysis leads to a new proposal for determining the right licensee and an appropriate royalty base for IoT devices within multi-tier value chains. Rather than focusing on the geometric placement of parties downstream or upstream, we consider their roles in the chains. We argue that licences should be granted to the IoT component’s designer, the party with knowledge of the technology and design capabilities. This entity is entitled to a licence providing legal certainty to work with the technology and develop new components or products, regardless of whether they are the end-product manufacturer or component supplier.

We then propose a proportional functionalistic approach to establish a royalty base for IoT components, using technical, measurable factors. We recommend quantifying FRAND rates based on the characteristics of IoT devices, specifically their data consumption, as a more objective measure than qualitative factors like fairness. We introduce a formula to illustrate the calculation method, using data consumption as the basis for determining the royalty rate. This approach offers a starting point for negotiations while potentially benefiting the environment with positive secondary effects.

Notes

McKinsey Center for Future Mobility (2018), p. 4.

Heiden (2019), p. 1.

Commission Staff Working Document, Impact Assessment Report, accompanying the document Proposal for a Regulation of the European Parliament and of the Council on standard essential patents and amending Regulation (EU) 2017/1001, Brussels, 27 April 2023. (hereinafter: Commission Staff Working Document on Proposal on SEP Regulation), available at: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52023SC0124&qid=1682711318413.

Ibid., p. 6.

Ibid., pp. 6–7.

Nagpal (2021).

Juillet (2022).

Hanlon and Pous (2018).

McKinsey & Company (2021).

The creation of Avanci, a one-stop licensing platform, emerged from negotiations between SEP holders, automakers, and suppliers. Launched in September 2016, Avanci focused on streamlining licensing for cellular SEPs in the automotive and smart meter sectors. Major SEP holders like Ericsson, Qualcomm, InterDigital, KPN, and ZTE joined the platform. Avanci’s unique royalty structure is based on usage context, involving factors such as wide-area connectivity, usage volume, and required bandwidth. See Avanci (2016).

Heiden et al. (2020), pp. 30–31.

This was the case in Nokia v. Daimler, where several tier 1 suppliers asked for a licence. See Mueller (2019).

Nikolic (2021), p. 151.