Abstract

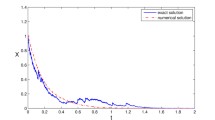

This paper deals with a class of two-step Milstein methods for stochastic differential equations with Poisson jumps. The mean-square convergence and linear mean-square stability of the proposed methods are discussed. In addition, the linear mean-square stability regions of the two-step Milstein methods are compared with those of one-step \(\theta \)-Milstein methods. Numerical examples demonstrate the mean-square convergence and the linear mean-square stability of the presented methods.

Similar content being viewed by others

References

Buckwar E, Winkler R (2006) Multistep methods for SDEs and their application to problems with small noise. SIAM J Numer Anal 44(2):779–803

Deng S, Fei W, Liu W, Mao X (2019) The truncated EM method for stochastic differential equations with Poisson jumps. J Comput Appl Math 355:232–257

Elaydi S (2005) An introduction to difference equations. Springer, New York

Gardoń A (2004) The order of approximations for solutions of Itô-type stochastic differential equations with jumps. Stoch Anal Appl 22(3):679–699

Hairer SP, NØrsett E, Wanner G (1993) Solving ordinary differential equations. I: nonstiff problems, 2nd edn. Springer, Berlin

Hanson FB (2007) Applied stochastic processes and control for jump-diffusions: modeling, analysis, and computation. Society for Industrial and Applied Mathematics, Philadelphia

Higham DJ, Kloeden PE (2006) Convergence and stability of implicit methods for jump-diffusion systems. Int J Numer Anal Model 3(2):125–140

Higham DJ, Kloeden PE (2007) Strong convergence rates for backward Euler on a class of nonlinear jump-diffusion problems. J Comput Appl Math 205(2):949–956

Hu L, Gan S (2011) Stability of the Milstein method for stochastic differential equations with jumps. J Appl Math & Informatics 29(5–6):1311–1325

Huang C, Li M, Chen Z (2021) Compensated projected Euler–Maruyama method for stochastic differential equations with superlinear jumps. Appl Math Comput 393:125760

Jury E (1964) Theory and applications of the Z-transform method. John Wiley & Sons, New York

Platen E, Bruti-Liberati N (2010) Numerical solution of stochastic differential equations with jumps in finance. Springer, Berlin

Protter P (1992) Stochastic integration and differential equations: a new approach. Springer, Berlin

Ren Q (2022) Compensated two-step Maruyama methods for stochastic differential equations with Poisson jumps. Int J Comput Math 99(3):520–536

Ren Q, Tian H (2020) Compensated \(\theta \)-Milstein methods for stochastic differential equations with Poisson jumps. Appl Numer Math 150:27–37

Sobczyk K (1991) Stochastic differential equations with applications to physics and engineering. Kluwer Academic, Dordrecht

Tan J, Men W (2017) Convergence of the compensated split-step \(\theta \)-method for nonlinear jump-diffusion systems. Adv Differ Equ 189

Tocino A, Senosiain MJ (2015) Two-step Milstein schemes for stochastic differential equations. Numer Algorithms 69(3):643–665

Yang X, Zhao W (2016) Strong convergence analysis of split-step \(\theta \)-scheme for nonlinear stochastic differential equations with jumps. Adv Appl Math Mech 8(6):1004–1022

Acknowledgements

The authors would like to thank the editor and referees for their valuable comments and suggestions which helped us to improve the paper.

Author information

Authors and Affiliations

Corresponding author

Additional information

Communicated by Pierre Etore.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The work of Q. Ren is supported by National Natural Science Foundation of China (no. 11801146), The youth backbone teacher cultivation project of Henan University of Technology (21420123), The youth support project for basic research of Henan University of Technology (2018QNJH17) and the High-Level Personal Foundation of Henan University of Technology (no. 2017BS023). The work of H. Tian is supported in part by the National Natural Science Foundation of China under Grant nos. 11671266 and 11871343, and Science and Technology Innovation Plan of Shanghai under Grant no. 20JC1414200.

Rights and permissions

About this article

Cite this article

Ren, Q., Tian, H. Mean-square convergence and stability of two-step Milstein methods for stochastic differential equations with Poisson jumps. Comp. Appl. Math. 41, 125 (2022). https://doi.org/10.1007/s40314-022-01824-3

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1007/s40314-022-01824-3

Keywords

- Stochastic differential equation

- Poisson jump

- Two-step Milstein method

- Mean-square stability

- Mean-square convergence