Abstract

The present study is an attempt to investigate in Indian context two important issues with respect to base metals (these are primarily non-ferrous metals), first to test whether the market for base metals is efficient like other financial markets and second to explore a possibility of any co-integration in prices amongst these base metals. To this end, we collect daily closing prices of five base metals, viz. aluminum, copper, zinc, lead and nickel for the study period Jan 1, 2016, to Dec 31, 2020. The methodology involves three different co-integration tests and two different ‘Day of the Week’ (market efficiency) tests. The results of the study showed that co-integration existed only when aluminium was taken as dependent variable with other metals as forcing variables. Also, no co-integration existed for other four base metals and these results were confirmed by both Engle-Granger and Gregory-Hansen tests; however, Johansen test failed to reveal any co-integration amongst any of these metals. Furthermore, test of market efficiency using ‘Day of the Week’ methodology, with Dummy OLS and GARCH(p,q) approaches, revealed that market for all the metals was efficient except copper. The study also tested model building pre-requisites of stationarity and serial correlation of variables and found these to be satisfactory. The results of the study thus revealed that copper’s prices showed market inefficiency which if exploited could provide a big opportunity for investors, traders and speculators to make profits. Market for remaining four metals was found to be efficient thus making profits difficult; however, these metals can be considered in combination with other financial assets to explore the unexplored opportunities in these markets.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In a typical commodity market, energy, agriculture and metals constitute three core segments and account for bulk of the trading in these markets. Within the commodity market, the metals space, comprises approximately twenty different metals which are further classified as precious metals (gold, silver, platinum), ferrous- or iron-based metals (iron, manganese etc.) and base metals or non-ferrous metals (aluminium, zinc, copper etc.). The empirical research in the metals space is primarily cornered by precious metals with other metals including base metals having failed in creating much enthusiasm amongst the researchers (Shahani and Bhardwaj 2020). There are three possible reasons why researchers tend to avoid other metals and focus mainly on precious metals for their empirical analysis; first, unlike gold and silver, other metals are still not recognized as an asset class by the ordinary investors and only the highly experienced ones with a lot of experience in commodity segment, do consider investing in such metals while most investors simply focus on traditional and popular precious metals; second, their role as a portfolio and risk diversifier has not been adequately demonstrated. The researchers often point out that only after such metals demonstrate high degree of inter-linkages with other traditional assets like stocks and bonds and also respond to shocks as others assets have responded, these metals could become an investable asset class which also creates a lot of research interests (Ciner et al., 2020). The last reason why investors and researchers tend to shy away from these class of commodities is that the prices of these metals are heavily dependent upon their production and any shortfall makes a big impact on their prices thus making them extremely risky as an investment class. However, some researchers do give a counter argument and according to them if the prices of these metals are vulnerable to their production, so is also the case with agricultural crops; however, this has not resulted in investors and researchers showing any less interest in this commodity class which is only next to precious metals.

Keeping in view the above and with prevailing research gap, we have designed our study focusing on this sub-segment of metals, i.e. base metals, and the study makes an attempt to answer some important issues which have been passively raised in the above section and these include firstly to test whether the market for these base metals is efficient like the other markets especially the stock markets, and secondly to empirically determine whether the movement of the five metal prices, namely aluminium, copper, zinc, nickel and lead is cointegrated; this being one of the biggest concerns amongst the investing class. The study has collected data for these five metals as daily closing prices for 5-year period: Jan 1, 2016, to Dec 31, 2020, from the MCX Commodity Market of India. These daily closing prices(\({P}_{t}\)) are converted to natural log returns, i.e. ln.(\({P}_{t}\)/\({P}_{t-1}\)), as warranted by the nature of the distribution of the time series of these five metals. Also, since the period also includes COVID-19 pandemic period, the possibility of break in the data of these five metals has also been explored under the study.

Coming to the demand for base metals, this is primarily a function of global supplies; however, this demand is highly uncertain thanks to rapid urbanization and industrialization which have resulted in imbalances in consumption of these metals thereby making their prices extremely volatile (Gil-Alana and Tripathy 2014). Blaming global demand price variability, Arbatli and Vasishtha (2012) in their study found this to be main reason for rise in metal prices. Researchers also feel that there is a whole gamut of industries which depend upon base metals and therefore they strongly feel that there is one-to-one relation between growth of industrial production and metal prices. Gil-Alana and Tripathy (2014) also found in their study a positive relation between rise in speculative activities in BRICS nations and price volatility in base metals. A study by IMF (2014) forecasted that a decline of 1% in growth of emerging economies’ could result in fall in metal prices by 9% with 1-year lag. Cheung and Morin (2007) in their study went further and argued that the price surge in metals in Asian markets was such that industrial activity alone cannot provide adequate explanation for the same.

Although there is limited empirical research on base metals, research on base metals has gained some momentum during the last one and a half decades with coming of fresh evidence especially after the global financial crisis of 2008 that this segment of commodity market now possesses important asset characteristics like high volatility in their prices, short- and long-run persistence (Gil-Alana and Tripathy 2014; Sinha and Mathur 2013; Tiwari and Gupta; 2009; Hammoudeh and Yuan 2008), hedging and safe haven characteristics (Agyei-Ampomah et al. 2014), spillover aspects of return or volatility (Ciner et al. 2020; Todorova et al. 2014) and asymmetric nature of returns (Lien and Yang 2008).

Kang et al. (2019) aiming to understand diversification properties of base metals investigated the co-movement between metals traded on Chinese futures market of metals (SFE) and London Metal Exchange (LME). The results revealed changing frequency patterns with respect to the co-movement of metals with stronger co-movement seen only amongst zinc and copper. They concluded that the benefits of diversification were available only in the short run with long run showing no diversification benefits. Exploring the co-movement between base metals and stock prices, Jacobsen et al. (2019) found that not only relation was strong but base metals also had the capacity to predict the stock prices. Choudhary et al. (2015) in their study which focused on only one base metal, copper, found that both price and volatility of copper were strongly influenced by the movement of the BSE Sensex and there was cause-effect between the two set of prices. In another related research, Aktaş et al. (2016) also targeting copper correlated the movement of the stocks of mining companies to the prices of related metals and the results revealed positive movement from copper prices to stocks of copper mining companies.

Spillover in return and volatility amongst base metals has also been explored in some of the recent studies like Ciner et al. (2020) where they found that spillover both in return and volatility was actually quite high in base metals space somewhat similar to financial markets and therefore recommended that this market segment may be considered by the investors for inclusion in their portfolio just as they are holding equities and bonds. Similar results were seen in the past by Todorova et al. (2014) who actually worked upon high-frequency data and found significant spillover in base metals in the long run. Again, spillover of growth on base metals has been explored by Wang and Wang (2019) and they found that for China a 1% rise in industrial production was associated with increase in price of base metals which varied anywhere between 3 and 7% amongst metals. Furthermore, a shock in industrial growth could explain 7–13% of the variation in different metal prices.

Studies have also been undertaken to explore the relation between spot and future prices of base metals and here a broader viewpoint of researchers is that there is a rise in the linkages between spot and forward prices when stock markets are performing well. An interesting study on price discovery of base metals was carried out by Purohit et al. (2015) where they found that in Indian context, spot prices were playing the role of price discovery instead of future prices, with positive co-integration in the long run.

Thus, that research on base metals has started gaining momentum and some interesting findings have also emerged in this relatively unexplored area; however, what has been actually missed out in many research studies is the investigation of efficiency of the market of these base metals, i.e. whether all available information on base metals is fully incorporated in their prices making it impossible to make profit using analysis of past data, a term very commonly associated with other financial markets like the stocks, foreign exchange and bond markets. Thus, considering this aspect, this is one of the key areas where we have focused in our study. Another important dimension which we found requires more attention is the long run co-movement of prices in metals space, i.e. co-integration. We have tried to cover this aspect in a rather comprehensive manner in our study by including three different types of co-integration tests to confirm whether any co-integration and co-movement exists amongst these base metals in the long run.

Hence, in light of the above, our approach would be to examine the following twin objectives; first is to test the market efficiency of the five base metals using calendar effect (day of the week) methodology. This would also ascertain whether or not there is any specific movement in returns and return volatility which can be attributed to any particular ‘day of the week’. In other words, to ascertain whether return (or return volatility) on any of the 5 days of the week is statistically different from other days of the week. The tool employed is Standard Dummy Variable Approach procedure along with GARCH(p,q) approach to identify specific movement in returns and return volatility. The second objective is to examine possible co-integration between price movement of the base metals and as mentioned earlier this is achieved by applying three different methods, viz. Engle-Granger, Johansen and Gregory-Hansen (G-H) procedures. The use of more than one co-integration procedure confirms and cross checks the co-integration amongst the base metals. Furthermore, the G-H procedure identifies the co-integration in the presence of a single structural break thus making the results more reliable. The study also tests for the supplementary objective wherein we attempt to make a comparative assessment of return and risk aspects of five base metals based upon their daily closing returns.

Distribution characteristics and statistical properties

Table 1 provides information about the mean, median, standard deviation, skewness, kurtosis and other parameters pertaining to the daily returns on spot prices of five base metals, viz. aluminium, lead, copper, nickel and zinc for the period Jan 1, 2016–Dec 31, 2020: 1264 data points. The first parameter under consideration is mean return for which we have applied the formula:- \(\frac{\left[\sum_{t=1}^{n}\left(\frac{{P}_{t,m}-{P}_{t-1,m} }{{P}_{t-1,m} }\right)\right]}{{n}_{m}}\), \({P}_{t,m}\) is the Closing price of base metal ‘m’ in time period ‘t’, ‘\({n}_{m}\)’ are the number of observations of base metal ‘m’.

Table 1 reveals that daily mean return is highest for nickel at 0.000739 which on annualized percentage basis becomes 26.97%, followed by zinc at 24.67%, copper 23.18%, aluminium 17.6% p.a. and finally lead at 12.05% p.a. The analysis of mean return leads to two important considerations; first, none of the metals has given a negative average return for the period under study and second, the average returns of at least three of the five base metals, nickel, zinc and copper, is fairly close to one another. Both these considerations are extremely important for investors intending to invest in base metals as these metals are giving a reasonable return which is quite comparable with other popular assets but noteworthy aspect here is that the performance of these metals is fairly close to one another giving diversification benefits.

The second parameter under consideration is standard deviation, which is considered as a proxy for risk in a layman’s language. The results of this parameter reveal that aluminium has the lowest standard deviation followed by zinc and lead while nickel carries the highest standard deviation thus making this metal riskiest of all the five base metals. It is interesting to note that metal Nickel also had the highest daily mean return amongst all five metals as seen above and this high risk-high return feature makes nickel a suitable investment only for those investors who want to take high risk to get high returns but this may not be the ideal choice for a risk averse investor.

Hence, for those investors who intend to take only calculated risk, the ideal investment would be a return which is adjusted for risk and this takes us to our third parameter, coefficient of variation (CV), a ratio which considers both the risk and return aspects and is obtained by dividing standard deviation by average return; (C.V = σ/µ) and here the most ideal metal would be the one which has lowest CV. Now, the C.V statistics in Table 1 reveals that zinc actually has the lowest coefficient of variation out of all the five base metals and this makes investment in zinc quite appropriate for an ideal investor who wants a balance between both risk and return parameters. The next preferred candidate is nickel while lead appears to be the least preferred metal in this category.

The same pattern is also visible in the daily return graph of these five metals (Figs. 1, 2, 3, 4 and 5). The daily pattern of returns for metal zinc (Fig. 5) is quite evenly distributed with daily return being in the range of \(\pm\) 0.5 and has just one spike. On the other hand, metals like aluminium or copper have quite a number of spikes indicating high variability or risk. In the pattern of daily return on nickel (Fig. 4), although here the number of spikes is more than zinc, these spikes are relatively shorter in dimension as compared to spikes of aluminium, lead or copper.

Daily returns on aluminium spot prices for the period Jan 1, 2016–Dec 31, 2020. Ret on Aluminium (Daily)

Daily returns on copper spot prices for the period Jan 1, 2016–Dec 31, 2020. Return on Copper (Daily)

Daily returns on lead spot prices for the period Jan 1, 2016–Dec 31, 2020. Ret on Lead (Daily)

Daily returns on nickel spot prices for the period Jan 1, 2016–Dec 31, 2020. Ret on Nickel (Daily)

Daily returns on zinc spot prices for the period Jan 1, 2016–Dec 31, 2020. Ret on Zinc (Daily)

Table 1 also provides information about distribution characteristics of five base metals and this includes Skewness, kurtosis and Jarque–Bera (JB) statistics. Out of five distributions, copper distribution is negatively skewed while the rest are positively skewed. Furthermore, in terms of skewness, only two distributions, namely nickel and zinc are fairly close to the skewness of a normal distribution. On the other hand, ‘Kurtosis’ of all the distributions appear to be larger than that of normal distribution making all the five metal distributions as leptokurtic, a distribution with fatter tails with a lot of outliers. We also computed JB statistics, a test of normality of distributions and found that null hypothesis of normality was rejected by all the five distributions (‘p’ values of all the metals was found to be statistically significant).

Research methodology and test of hypothesis

Developing a co-integration model

Co-integration, a long-term relation between two time series, was established after a spurious regression was detected by Newbold and Granger (1974) in their pioneering work which eventually paved the way for integration of two or more nonstationary time series. The earliest model of co-integration was given by Engle and Granger (1987), a two-step procedure and proves the co-integration of variables through stationarity of residuals.

Considering the objectives of the study, under the present set-up, we would be carrying out a detailed investigation of whether or not there is any long-term relation amongst the movement of base metals in India and to this end we have applied three different models, Engle-Granger model (1987), Johansen co-integration model (1998), and Gregory-Hansen co-integration model (1996). The need for three different models arises as all the three models have their own merits and limitations, whereas Engle-Granger model, a two-step procedure, can be applied only to two variables, the Johansen model of co-integration can be applied for multiple (> 2) variables, but this model does not incorporate structural break in time series for which we have added the third model; Gregory-Hansen co-integration model which tests for co-integration in the presence of single structural break in time series. Eviews 12 software has been used for all the three models.

Engle and Granger (1987), co-integration model

Our first model, Engle-Granger test of co-integration, is a two-step procedure and is also popularly called the test of residuals. The first step involves generation of residuals, ut, by regressing the co-integrating variables Y1 and Y2 at their level prices (Eq. (1(a)) The residuals so generated are lagged once to obtain ut-1 and also differenced once to obtain Δut and another regression is fitted between the these transformed residuals (Eq. (1(a)). Thus, we obtain following two stages:

-

Stage 1: Running the OLS on following variables:

$${\mathrm{Y}}_{1\mathrm{t}}={\upbeta }_{1}+{\upbeta }_{2}{Y}_{2t}+{\mathrm{u}}_{\mathrm{t}}$$(1a) -

Stage 2: Running a second regression of residuals as under

$${\Delta \mathrm{u}}_{\mathrm{t}} = {\mathrm{\alpha }}_{1} {\mathrm{u}}_{\mathrm{t}-1} + {\mathrm{e}}_{1\mathrm{t}}$$(1b)

Null hypothesis: No co-integration of variables (or nonstationary of residuals).

Alternate hypothesis: Variables are co-integrated (or residuals are stationary).

Decision criteria: | α1 |> critical value of Engle-Granger tables, reject the null hypothesis.

The biggest disadvantage of Engle-Granger co-integration model is that being a two-step procedure, it enables errors to be carried forward and hence the results of this model need to be supplemented by other co-integration procedures.

Johansen co-integration model (1988)

The Johansen (1988) model is based upon a simple VAR Model shown as Eq. (2) below:

μ = constant k = no. of lags of the variable Yi, et the error term and ∅1,∅2, ∅3 ………. are the coefficients of VAR terms. ‘t’ is the time period and ‘i’ is ith variable.

The above model (ii) may be written as

Now, let \(\alpha\) i = (∅i,1–1) represent a matrix of coefficients signifying long-term relation among the variables; \(\alpha\) i is the fundamental matrix of the co-integration.

Since all the vectors in the above matrix \({}^{^{\prime}}{a}^{^{\prime}}\) need not be co-integrated we focus on the rank of the matrix \({}^{^{\prime}}{a}^{^{\prime}}\). If there is no co-integration, \({}^{^{\prime}}{a}^{^{\prime}}\) has a rank ‘0’ and in case of co-integration amongst variables, we compute characteristic roots and eigen values. The biggest advantage of Johansen model of co-integration is that unlike Engle Granger, it avoids choosing a dependent variable and then subsequently running an OLS regression but instead is based upon an maximum likelihood estimation (MLE), a procedure which estimates the parameters by maximizes the likelihood function; however, the model requires a sample of sufficient size to give accurate results. A very important merit of the Johansen’s model is that it treats every variable as endogenous variable (Wassell and Saunders 2000). Some researchers like Gonzalo and Lee (1998) have however reported that there can be situations when Engle-Granger gives more robust results than Johansen’s test; hence, they recommend test of co-integration must be carried out using both Engle-Granger and Johansen methodologies.

Gregory-Hansen co-integration model (1996)

The third model of co-integration applied in our study is Gregory-Hansen co-integration model and this model checks for co-integration in the presence of a structural break. The Gregory-Hansen test is also a residual-based test and somewhat similar to Engle-Granger and works by computing the usual ADF and also Philips test statistics at all possible break points and then selects the smallest values which is considered break in time series. The reason for including this model for our co-integration analysis is that the sampled period includes COVID-19 pandemic period and hence the chances of a structural break in time series are quite high and such a model is expected to give a superior result in case a break is detected in time series. The other two models, viz. Engle-Granger and Johansen, may become inappropriate in case there is a break in time series as these models assume that co-integrating vector is time invariant. Although, G-H model is seen as an improvement over the previous two models, this model too has its own limitation in terms of increase in the chances of committing a type 2 error due to break detection capacity thereby resulting in a spurious unit root behavior making rejection of null of no co-integration somewhat difficult (Shahani, Kumar and Goel 2020).

Gregory-Hansen co-integration model has three variants: (i) level shift, (ii) level shift with trend and (iii) regime shift (or shift in both slope and intercept). We construct the following three Eqs. (4, 5 and 6), one for each of these three model versions:

-

Model I: level shift only:

$${Y}_{t}={\beta }_{1}+{{\beta }^{*}}_{1}{D}_{1,t}+{\beta }_{2}{X}_{i,t}+{u}_{1t}$$(4) -

Model II: level shift with trend:

$${Y}_{t}={\beta }_{1}+{{\beta }^{*}}_{1}+{D}_{1,t}+{\beta }_{2}{X}_{i,t}+{\beta }_{3}T+{u}_{2t}$$(5) -

Model III:regime shift:

$${Y}_{t}={\beta }_{1}+{{\beta }^{*}}_{1}{D}_{1}+{\beta }_{2}{X}_{t}+{{\beta }^{*}}_{2}{D}_{2}{X}_{i,t}+{u}_{3t}$$(6)

Model I, which is level shift model (Eq. (6)), displays the breakpoint, i.e. a break in linear relationship amongst the variables as a change in intercept and is represented by Dummy (D1). For this model, intercept before the break shall be β1 while intercept after the break shall be β1 + β*1. Dummy (D1) is defined as equal to ‘1’, if ‘t’ \(\ge\) Break Date and ‘0’ otherwise. Furthermore, in case of Model I, slope does not undergo any change. For Model II which is level shift model with a trend (Eq. (v)), the model has been obtained by adding a trend variable ‘T’ to Model I, the objective being to remove the trend (if any). Thus, by including this term (T), we can focus on level shift and the trend variable (T) would take care of any shift which might have occurred due to trend. Again ‘T’ is same as time period ‘t’. Model III under Gregory-Hansen co-integration (Eq. (vi) is a Regime Shift Model and has been obtained by adding a shift in the slope to Model I. The slope shift again has been represented by a Dummy Variable (D2). Thus, Model III includes two dummies; D1 for a shift in intercept and D2 for shift in slope. Both Dummies are defined alike, i.e. Dummy = ‘1’, if ‘t’ \(\ge\) Break Date and ‘0’ otherwise (see Shahani et al. 2020).

Null hypothesis for all G-H models: no co-integration at break point.

Alternate hypothesis: co-integration exists at a single breakpoint.

The computed values are compared with test criteria values which have been obtained from Augmented Dickey Fuller ADF (\(\tau )\) and Philip-Perron test statistics as \({\mathrm{Z}}_{t}\) (\(\tau ) \mathrm{and }{\mathrm{Z}}_{a}\) (\(\tau )\)

Decision criteria: If all the three absolute computed values, |ADF (\(\tau )|\), | \({\mathrm{Z}}_{t}\) (\(\tau )\) | and \(|{\mathrm{Z}}_{a}\) (\(\tau )\)|, are > critical, reject the null hypothesis. Rejection of null would mean that the linear combination of variables exhibit long run stable characteristics (co-integration).

Developing a model to test for market efficiency of base metal prices

A market is said to be efficient if the change in prices follow a random behaviour, i.e. past information on prices cannot be used to predict current prices. To test market efficiency of our five base metals, we have applied calendar effect (or ‘day of the week effect’) methodology. This would determine ‘day of the week’ effect for returns in base metals, i.e. whether or not the returns of any particular day of the week are different from other week days. We apply OLS Dummy Variable Approach with Monday’s return; \({\alpha }_{1}\) in Eq. (8) being considered as the base return. The dependent variable being the log return of the mth base metal under consideration, \({D}_{i,t}\) is the Dummy for the ith day (i = 2; Tuesday to i = 5; Friday) with corresponding slope coefficient as \({\mathrm{\alpha }}_{2,\mathrm{i}}\),‘t’ is the time period and ut as the residual error term. The equation for ‘day of the week’ effect for returns in base metals is given as under:

Null hypothesis (HO1): \({\mathrm{\alpha }}_{2,\mathrm{i}}\) = 0; (i = 2 to 5) (The market for mth base metal is efficient or there is no ‘day of the week’ effect on return of mth base metal).

Alternate hypothesis (HA1): \({\mathrm{\alpha }}_{2,\mathrm{i},\mathrm{m}}\) ≠ 0; (i = 2 to 5) (There is ‘day of the week’ effect on return on mth base metal or coefficient of any one or more days is statistically significant).

The rejection of null would be a signal that market efficiency does not exist.

Furthermore, in a modelling exercise, it is always desirable to test any hypothesis using more than one methodology; here, we decided to test our ‘day of the week effect’ additionally using GARCH (p,q) approach. Furthermore, since GARCH(p,q) model has both mean and variance equations, this methodology would also help us in knowing ‘day of the week effect’ both for return on base metals and also volatility of these metals as given in the “‘Day of the week’ effect for returns and return volatility in base metals” section below.

Day of the week’ effect for returns and return volatility in base metals

Under GARCH(p,q) standard model our mean equation (viii) is the AR(1) equation where natural log of return on metal; \({\mathrm{ln}.\mathrm{Ret}}_{\mathrm{m},\mathrm{t}}\) is regressed against its first lag. The variance equation under GARCH includes three terms: a constant term; \(\uplambda\) 1, square of the error term of previous periods or the ARCH term \({{\mathrm{u}}^{2}}_{t-j}\) with coefficient \({\uplambda }_{2,\mathrm{j}}\) and previous period’s variance of the error term, or the GARCH term \({h}_{t-i}\) with coefficient \({\uplambda }_{2,\mathrm{j}}\). Furthermore, to test ‘Day of the week’ effect for returns and return volatility in base metals, we have modified the standard GARCH(1,1) model and included the Dummy term (\({\mathrm{D}}_{\mathrm{i},\mathrm{t}}\)) both in mean and variance equation. A significant dummy for the mth metal for any day in mean or variance equation would imply that return or volatility of returns in the mth base metal is different from rest of the days of the week or market for the same is inefficient. The GARCH(p,q) mean and variance equation is given below as Eqs. (8) and (9) respectively.

Hypothesis for ‘Day of the week’ effect for returns

-

HO2: \({\upbeta }_{2,\mathrm{i},\mathrm{m}}\) = 0; ‘Day of the week’ effect does not exist.

-

HA2: \({\upbeta }_{2,\mathrm{i},\mathrm{m}}\) ≠ 0; existence of ‘Day of the week’ effect.

Hypothesis for ‘Day of the week’ effect for volatility

-

\({H}_{O3}\): \({\uplambda }_{4,i,m}\)= 0; Day of the week’ effect does not exist.

-

\({H}_{O3}\): \({\uplambda }_{4,i,m}\ne\) 0; existence of ‘Day of the week’ effect.

Empirical results of the study

The section discusses the empirical results of the study (Tables 1, 2, 3, 4, 5, 6, 7, 8 and 9) which is spread over three parts: part I (Tables 2, 3 and 4) gives a discussion on the results of co-integration tests between five base metals using three different models; part II (Tables 5 and 6) shows the results of ‘Day of the Week’ effect for returns and return volatility of five base metals using Dummy Variable and GARCH(p,q) models; and finally part III (Tables 7, 8 and 9) gives the results of our supplementary tests which includes test for stationarity and serial correlation.

We begin with part I, with the results of the first Model of co-integration; Engle-Granger (1987) two-step co-integration test procedure for our five base metals. These results are shown as computed tau ‘t’ statistics with associated probabilities from Engle-Granger tables and computed ‘z’ statistic values from normalized autocorrelation coefficient. The results reveal that null hypothesis of no co-integration is rejected when aluminium is dependent variable while null is accepted all other base metals. The results are similar for both the ‘tau’ ‘t’ and ‘z’ statistics as reflected by their ‘p’ values (Table 2).

Coming over to second co-integration model where we have applied the Johansen (1998) test procedure for the same five base metals and the test results of the same are shown in Table 3 (Table 3(a) as co-integration trace test and 3(b) as co-integration Max Eigen value test). In Tables 3(a and b), the null hypothesis is stated in column I as hypothesized number of co-integrating relations. Looking at the Tables 3(a) and 3(b) we find the Null Hypothesis of No Co-integration is accepted for all metals inferring that the test could not detect any co-integration amongst any pair of metals. Furthermore, here too both the statistics, trace and Max Eigen value, give identical results of no cointegration.

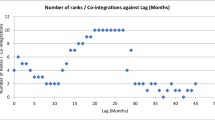

Our last test for co-integration is Gregory and Hansen (1996) co-integration and the results of the same are given in Table 4 (a to e). For each of the five base metals, the results are given for three different versions of this test: level shift, level shift with trend and regime shift. The computations under GH tes follows ADF (t) and Philip Perron Za and Zt statistics; critical values of the same are given below Table 4 (e). The results reveal that four of the five base metals, namely copper, nickel, zinc and lead, do not show any co-integration while some co-integration is visible for metal aluminium.

Furthermore, GH test being a breakpoint co-integration test, Table 4 (a to e) also provides additional information about the breakpoint of all the metals and as the results reveal these breakpoints differ considerably during the 5-year period of study. Quite interestingly, the breakpoint of only one base metal, i.e. zinc, falls during the COVID-19 pandemic period while other metals have breakpoints prior to this pandemic period. This clearly shows that impact of pandemic on these base metals was not as alarming as for other categories of financial markets especially stock markets. As shown by many studies, stocks during this period were not only more volatile than normal times but also witnessed increased contagion and crisis-sensitive spillovers from other market segments; however, same could not be said for our base metals and this becomes an important information for our potential investors in this asset class (see Managi, et al. 2022; Zhang and Hamori 2021; Hung and Vo 2021; Mensi et al. 2021).

Next, comparing the results of co-integration of all three tests, we find some similarity in the results of Engle-Granger and GH tests where co-integration is detected when aluminium is considered as dependent while other metals as forcing variables; however, these results do not match with Johansen methodology test results. Additionally, GH test also gives the likely break points in the time series of each of the five metals thereby making it superior of all the three cointegration tests.

Coming to results of part II, we have tested for the efficiency of our market for five base metals and tool employed for this purpose is ‘Day of the Week’ for which the study has employed two methodologies: OLS Dummy Variable and GARCH(p,q) approaches. The results reveal that for OLS Dummy Variable Model (Table 5), only in case of copper, there appears to be a ‘Day of the week’ effect with Dummy for Monday (the constant or the base term assumed under the model) and Friday’s return being statistically significant and not for other days of the week. ‘Day of the Week’ effect was not detected for other four metals, viz. aluminium, lead, nickel and zinc, with all the dummy variables being statistically insignificant for all the days of the week.

Coming to the ‘Day of the week effect’ for five metals using GARCH (p,q) methodology, the results of which are given in Table 6. The table results are divided into two parts; the upper part of the table pertains to the results under the mean equation and lower part, the variance equation. From market efficiency point of view, the results of upper part, i.e. mean equation, are more important and the table reveals that except for copper where ‘Day of the Week’ was found to be statistically significant for Monday (base term assumed), the same was not detected for any of the other four metals. On the other hand, ‘Day of the Week’ effect based upon volatility of returns shown under lower part of Table 6 was clearly observed amongst different metals during different days of the week. However, considering the fact that ‘Day of the Week’ effect based upon volatility is not considered a yardstick of measurement of efficiency of a market, we would not be using this criteria for determining whether a metal market is efficient or not; however, volatility is an important consideration for both hedgers and speculators who now frequently take positions in new instruments now available which bet exclusively on volatility.

Thus, after analysing the results of ‘Day of the Week’ test, we come to the conclusion that there is market efficiency with respect to four of the five base metals, namely aluminium, lead, nickel and zinc and the only metal for which the ‘Day of the Week’ does exist is copper as confirmed both by Dummy OLS and GARCH (p,q) approaches. This has a strong implication for investors and speculators as there is a scope of exploitation of market inefficiency to make trading profits by taking position in copper on those days of the week; the returns of this metal do not match the returns during other days of the week.

Moving over to the last set of results given as Tables 7, 8 and 9 which relate to the results of the supplementary tests for model building and these tests include stationarity, serial correlation and Optimal Lag Criteria tests. Table 7 gives the results of our stationarity test for which we have applied ADF Unit root test ‘intercept with trend model’ and the results are displayed for computed ADF ‘t’ values both at level as well as at 1st difference with corresponding ‘p’ values shown in parenthesis. These results reveal that all the five base metals accept the null hypothesis of ‘Presence of Unit Root’ at level and reject the same only at 1st difference.

Next, we have the result of serial correlation and the same are displayed in Table 8. The test applied is the popular BG-LM* test procedure (see Eq. (x)) and the two statistics; ‘F’ statistics and observed R squares along with their probabilities (p values), accept the null hypothesis of ‘No Serial Correlation’ for all the five base metals. The last table under supplementary tests is Table 9 giving results of our Optimal Lag Selection Criteria forming the basis of lag length for our GARCH(p,q) and other tests. A comparative assessment of six different criteria based upon prediction error and commonly used for comparing model quality shows that four of these criteria (AIC, SC HQ and FPE) give an optimal lag as ‘2’ for our model which we have considered for model building and also carrying out supplementary tests.

Conclusion and study recommendations

The present study which focused on empirical investigation of base metals was undertaken with two compelling motives: first to test whether the market for base metals is efficient like other financial markets (see Chopra et al. 2015; Sunal, et al. 2014; Poshakwale 1996) and second to explore whether there exists a possibility of any co-integration between price movement of these base metals. To achieve these twin objectives, data on daily closing prices was collected from MCX India website for five base metals, viz. aluminium, copper, zinc, lead and nickel, for the study period Jan 1, 2016, to Dec 31, 2020. Furthermore, three different co-integration tests and two different ‘Day of the Week’ (Market Efficiency) tests were carried out under the study. The results of the study showed that co-integration existed only when aluminium was taken as dependent variable with other metals as forcing variables. No co-integration existed for other four base metals and these results were confirmed by both Engle-Granger and Gregory-Hansen tests; however, Johansen test failed to reveal any co-integration amongst any of these metals. Since it was difficult to arrive at any concrete conclusion regarding co-integration as tests were giving contradictory results, our conclusion would be that there was a very little chance that any co-integration to exist amongst base metals. Furthermore, test of market efficiency which was carried out using ‘Day of the Week’ methodology, and by adopting Dummy OLS and GARCH(p,q) approaches, the conclusion was that market for all the metals was efficient except copper.

The results of the study has brought about some important implications for investors and policy makers. Firstly, our analysis clearly showed that 4 out of 5 base metal markets are efficient just like other financial markets, thus making it difficult (if not impossible) to make trading profits from existing information available on these metals. However, results also revealed that one of these metals, copper’s market, is inefficient which provides a big opportunity for investors, traders and speculators to make profits. This is because Monday’s return on copper was found to be statistically different from return on this metal for other days of the week giving an idea about unexploited trading opportunities in this metal on Monday.

Furthermore, although the market for rest of the four base metals was found to be efficient, still it would be worth exploring whether the same also holds for other global markets especially those countries where conditions are similar to India. Also, with co-integration being proved only between aluminium with other base metals as forcing variables, the opportunities for investors in terms of scope of investment and trading benefits in case of aluminium exist in short run; however, any visible gains in short run would tend to evaporate in long run. On the other hand, investors and policy makers may be interested in exploring further deep into these base metal markets vis-à-vis other financial markets with respect to their co-movement, asymmetry, hedging and safe haven opportunities. Also, with respect to market efficiency angle, although four of the five metals were proved to be efficient on standalone basis, but when combined with other markets could create a potentially unexplored opportunity for traders, speculators and investors.

References

Aktaş R, Acar M, Güzel F (2016) Testing of the relationship between metal prices and stock prices through Granger causality: an application in Borsa İstanbul. Proceedings of ISERD International Conference

Agyei-Ampomah S, Gounopoulos D, Mazouz K (2014) Does gold offer a better protection against losses in sovereign debt bonds than other metals?. J Bank Financ 40:507–521

Chopra K, Vazirani R, Shahani R (2015) Empirical test of the random walk characteristics of the stock returns of select South Asian markets. arthaVaaN. University of Delhi, p 51

Choudhary N, Nair GK, Purohit H (2015) Volatility in copper prices in India. Annal Finan Econ 10(02):1550008

Ciner C, Lucey B, Yarovaya L (2020) Spillovers, integration and causality in LME non-ferrous metal markets. J Commod Mark 17:100079

Engle RF, Granger CW (1987) Co-integration and error correction: representation, estimation, and testing. Econometrica: journal of the Econometric Society 55:251–276

Gil-Alana LA, Tripathy T (2014) Modelling volatility persistence and asymmetry: a study on selected Indian non-ferrous metals markets. Resour Policy 41:31–39

Gonzalo J, Lee TH (1998) Pitfalls in testing for long run relationships. J Econ 86(1):129–154

Gregory AW, Hansen BE (1996) Practitioners’ corner: tests for cointegration in models with regime and trend shifts. Oxford Bull Econ Stat 58(3):555–560

Hammoudeh S, Yuan Y (2008) Metal volatility in presence of oil and interest rate shocks. Energy Econ 30(2):606–620

Hung NT, Vo XV (2021) Directional spillover effects and time-frequency nexus between oil, gold and stock markets: evidence from pre and during COVID-19 outbreak. Int Rev Financ Anal 76:101730

IMF (2014) Changing growth trends carry new global spillovers, IMF Survey online at www.imf.org/external/pubs/ft/survey/so/2014/pol072914a.htm?id=632854

Jacobsen B, Marshall BR, Visaltanachoti N (2019) Stock market predictability and industrial metal returns. Manag Sci 65(7):3026–3042

Johansen S (1988) Statistical analysis of co-integration vectors. J Econ Dyn Control 12(2–3):231–254

Kang SH, Tiwari AK, Albulescu CT, Yoon SM (2019) Time-frequency co-movements between the largest nonferrous metal futures markets. Resour Policy 61:393–398

Lien D, Yang L (2008) Asymmetric effect of basis on dynamic futures hedging: Empirical evidence from commodity markets. J Bank Financ 32(2):187–198

Managi S, Yousfi M, Zaied YB, Mabrouk NB, Lahouel BB (2022) Oil price, stock market and US business conditions in the era of COVID-19 pandemic outbreak. Econ Anal Pol 73:129–139

Mensi W, Hammoudeh S, Vo XV, Kang SH (2021) Volatility spillovers between oil and equity markets and portfolio risk implications in the US and vulnerable EU countries. J Int Finan Markets Inst Money 75:101457

Poshakwale S (1996) Evidence on weak form efficiency and day of the week effect in the Indian stock market. Finance India 10(3):605–616

Purohit H, Bodhanwala S, Choudhary N (2015) Empirical study on price discovery role in non-precious metals market in India. SAMVAD 10:15–25

Shahani R, Bhardwaj U (2020) Co-integration dynamics amongst the three MCX commodity indices: linear and non linear approaches. IIMS Journal of Management Science 11(3):155–168

Shahani R, Kumar,S, Goel A (2020) Does the energy-food nexus still exist: empirical evidence from the Indian agriculture sector post food crisis of 2006. Available at SSRN 3598282

Sinha P, Mathur K (2013) A study on the price behavior of base metals traded in India (No. 47028). University Library of Munich, Germany

Sunal G, Jain C, Kuthaila V, Shahani R (2014) The efficiency in the Indian market in the weak form: random walk and calendar effect investigation Indian at the crossroads, LexisNexis 95–104

Tiwari S, Gupta K (2009) Relative analysis of volatility of bullion commodity derivatives with respect to MCX Metal Index. Manag Insight 5(2):9–15

Todorova N, Worthington A, Souček M (2014) Realized volatility spillovers in the non-ferrous metal futures market. Resour Policy 39:21–31

Wang T, Wang C (2019) The spillover effects of China’s industrial growth on price changes of base metal. Resour Policy 61:375–384

Wassell CS, Saunders PJ (2000) Time series evidence on social security and private saving: the issue revisited. Unpublished Manuscript, Department of Economics, Central Washington University

Zhang W, Hamori S (2021) Crude oil market and stock markets during the COVID-19 pandemic: evidence from the US, Japan, and Germany. Int Rev Financ Anal 74:101702

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The contents of this research paper have not been published or submitted for publication to any other journal/book or anywhere else.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Shahani, R., Singhal, U. Do efficient commodity markets co-move: evidence from Indian base metals market. Miner Econ 36, 413–425 (2023). https://doi.org/10.1007/s13563-022-00353-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13563-022-00353-z