Abstract

The main objective of this study is to analyze the impact of disaggregated energy consumption (coal, natural gas, petrol, and electricity) on the economic growth of BRICS countries (Brazil, Russia, India, China, and South Africa) from 1990 to 2020. The study implements the Augmented Mean Group (AMG) and Cross-Sectional Augmented Autoregressive Distributed Lag (CS-ARDL) techniques for empirical analysis. The cointegration results indicate a consistent long-term link between coal consumption, gas, petrol, electricity, and economic growth. The CS-ARDL estimates show that disaggregated energy consumption has a positive short- and long-term effect on economic growth, and the AMG approach supports these findings. These results suggest that the economic growth of BRICS countries is positively influenced by increased consumption of different types of energy sources. The panel Granger causality test result confirms the causal link between coal consumption and economic growth, electricity and economic growth, and petroleum and economic growth, supporting the feedback hypotheses, while natural gas consumption and economic growth support the neutral hypothesis. These findings suggest that energy conservation initiatives can be implemented in BRICS countries without negatively impacting economic growth.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Numerous beneficial advancements, from which billions of people have benefited, are the evident outcomes of globalization and market liberalization. However, the significance of the energy sector in this development process cannot be overlooked. However, the importance of the energy sector in this development process cannot be overlooked. Light, power, and heat are fundamental factors in the construction and operation of metropolises and enterprises that create jobs and goods. Therefore, energy is considered to be the “oxygen” for the economic growth process. The use of energy, a key input for production, has expanded substantially in many countries worldwide over the past couple of decades (Azam & Raza, 2022). Similarly, Azam (2020) has expounded that energy is undeniably a vital source for socio-economic development. Nevertheless, the economic growth process is energy-demanding in the economy, so the significance of energy in an economic surge is widely acknowledged (Stern & Cleveland, 2004). Empirical research has remained one of the fascinating research subjects in energy economics studies for nearly four decades, though economic theories are silent, particularly on the link between energy usage and economic growth. In their study, Lindenberger and Kummel (2002) noted that energy as a driver of production is either neglected or given only minor consideration in traditional economic theory. This is because energy’s involvement in overall factors costs is insignificant compared to the total cost shares of other production factors such as capital and labor.

In ancient times, individuals exploited their identifiable physical labor for power. However, with technological advancement, conventional energy sources were supplanted by electricity. Stern (2011) studied that the shift has been from domestic biomass such as firewood and agricultural waste to mechanized fuels, for instance, natural gas, LPG, and electricity. The study by Stern (2011) further adds that in low-income economies, energy use per unit of economic output has lessened significantly due to technological revolution and the shift from lower-quality fuels (i.e., coal) to the consumption of better-quality fuels (i.e., electricity). Indeed, energy has become an influential factor for economic growth and development because it stimulates the efficiency and productivity of any economy. Moreover, prevalent industrialization, urbanization growth, and rapid population size have expanded energy consumption globally.

Energy is now widely recognized as being critical to national economic development and progress. As a result, the availability of meaningful energy is crucial for society’s long-term economic progress. Therefore, the relationship between energy usage and economic growth is considered to be the main focus of significant investigation because energy is one of the key driving forces of the growth process across the world’s economies (Pokharel, 2007; Saidi & Hammami, 2015). Coal, natural gas, electricity, and petroleum are all energy resources that greatly benefit development and economic progress. Moreover, these essential energy resources are increasingly being consumed as important inputs in consumption and production processes worldwide. As energy is a central part of the consumption, production, and growth process, a well-defined identification of the causal association between energy usage and economic progress is required.

Electricity is a secondary energy source largely derived from the conversion of primary energy sources such as fossil fuels (i.e., coal, oil, and natural gas) and wind energy. While coal has historically been the primary fuel used in electricity generation, the contributions of nuclear power and natural gas have been increasing. Conversely, the use of oil in electricity generation has decreased since the 1970s due to significant increases in oil prices. In general, energy from traditional energy sources (natural gas, coal, petroleum, and fossil fuels) and various renewable energy sources (solar, waste, wood, wind, and hydroelectric) are equally important for the growth process. However, there are ongoing debates about the extensive and unchecked use of energy consumption that leads to environmental degradation.

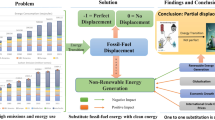

Undeniably, ensuring a stable supply of energy is vital for boosting national economic development worldwide. However, energy use tends to be higher in BRICS countries due to their sizable economies. Despite some studies having looked at the relationship between energy usage and economic growth in BRICS nations, there remains a prominent gap in research at a detailed level. Specifically, there is limited analysis of different energy sources such as coal, petroleum, natural gas, and electricity in relation to economic growth within the BRICS countries. This highlights the need for more comprehensive inquiries to better understand the complexities of energy dynamics using disaggregated energy consumption data and their impact on economic growth in these BRICS countries. The broad objective of this study is to evaluate the causal nexus between energy at the disaggregated levels covering coal, electricity, natural gas, and petroleum because the intensity, weaknesses, opportunities, and dangers of their usage necessitate scientific exploration. To the best of the researcher’s knowledge, no such empirical study exists on the topic under inquiry on BRICS economies. The existing statistics reveal that BRICS present about 18% of the global trade, 30% of the territory, 23% of the GDP, and 42% of the population. The outcomes will guide the policymakers in terms of appropriate and effective energy policy for achieving sustainable economic development and growth. Energy means, i.e., natural gas, coal, petroleum, and power use, are all linked to global economic growth and development. Furthermore, this research will greatly aid research into the association between energy usage and economic development when using coal, electricity, natural gas, and petroleum. Also, this research study adds to the existing literature on the disaggregated version of the energy usage covering coal, gas, electricity, and petrol and economic growth relationship. The effects of coal, natural gas, petrol, electricity, labor force, and FDI on the economic growth (as shown in Fig. 1) of the BRICS nations are highlighted in this paper.

Graphical abstract

The current study is divided into five sections. The “Introduction” section provides a brief introduction to the study. The “Literature Review” section presents a survey of theoretical and empirical literature. The “Data and Empirical Methodology” section covers the data description, empirical model, and estimation procedure. The “Results and Discussion” section presents the empirical results and includes a discussion. Finally, the “Concluding Remarks” section concludes the study.

Literature Review

Existing empirical studies reveal four perspectives on the causal relationship between energy use and economic progress. The first perspective is that energy usage Granger causes economic progress, known as the “growth hypothesis.” Many earlier studies support this hypothesis (Apergis & Payne, 2010; Aydin, 2018; Chu, 2012; Mighri & Ragoubi, 2020; Stern, 2000; Warsame et al., 2024). The second perspective suggests that economic growth Granger causes energy usage, known as the “conservation hypothesis.” Several previous studies support this viewpoint (Akinlo, 2021; Anoruo, 2017; Chu, 2012). The third perspective proposes that both economic growth and energy usage have bidirectional causality, known as the “feedback hypothesis” or bidirectional causality. Several previous researchers have supported this hypothesis (Ali et al., 2023; Chu, 2012; Farhani & Rahman, 2020; Lin et al., 2018; Park & Yoo, 2014; Shahbaz et al., 2014; Wang et al., 2023a; Yazdi & Mastorakis, 2014). The fourth perspective indicates no causality between economic development and energy usage, called the “neutrality hypothesis,” and previous research supports this viewpoint (Chu, 2012; Ocal et al., 2013).

Many studies have been dedicated to increasing attention to the link between energy usage and economic growth in both rich and poor nations over the last four decades. Though the association between energy use and economic progress has been explored considerably, the empirical findings on causality are oddly elusive. To present a comprehensive overview of the existing relevant literature, this study covers four subsections covering the electricity-economic growth nexus, petroleum-economic growth nexus, natural gas-economic growth nexus, and coal-economic growth nexus.

Electricity Consumption-Economic Growth Nexus

The prevailing literature on the connection between energy use and economic progress primarily began with the pioneering study of Kraft and Kraft (1978). Specifically, the authors evaluated the causality between economic growth and energy usage for the USA time series data from 1947 to 1974 and found a unidirectional connection from GNP to energy use. Wolde-Rufael (2006) results indicate a long-term association between per capita electricity use and nations’ economic progress. Granger causality was found for 12 countries out of 17 African countries from 1971 to 2001. For the remaining six countries, a positive unidirectional causality from economic development to electricity usage, a reverse causality for three nations, and a two-way causality for the rest of the three nations were detected. Narayan and Prasad (2008) found support favoring electricity usage causing real GDP in eight countries from the OECD, namely, Portugal, Italy, Australia, the Slovak Republic, Iceland, Korea, the UK, and the Czech Republic, out of 30 OECD countries. The results of the causality test by Odhiambo (2009a) for Tanzania from 1971 to 2006 reveal a one-sided causality that runs from power usage to economic development. Thus, the findings suggest that energy usage increases economic progress in Tanzania. On the other hand, Odhiambo (2009b) used South African data from 1971 to 2006 and observed a two-way causal association between power usage and economic growth.

The empirical findings of Lean and Smyth (2010) observed one-way causation from power usage to economic development in five ASEAN countries from 1980 to 2006. Ciarreta and Zarraga (2010) found a long-term equilibrium link between power usage and economic development for 12 European countries during 1970 to 2007. Belaid and Abderrahmani (2013) observed short-run and close-run causation between power usage and economic development in Algeria from 1971 to 2010. Bayar and Özel (2014) finds that electricity usage significantly impacts growth in emerging economies during 1970 to 2011. Moreover, bidirectional causality was also detected between economic growth and electricity usage. Mighri and Ragoubi (2020) observed a long-term link between power use and economic development in Tunisia from 1971 to 2013. In their study, Ali et al. (2022) found that both clean and non-clean energy use significantly affect economic growth in PIMC countries from 1980 to 2019. In their study, Güler et al. (2022) showed that there is a stronger inverse effect of electricity use on economic growth in 30 European countries from 2015Q1 to 2021Q3. Empirical results from Dumitrescu and Hurlin’s Granger causality test by Ali et al. (2023) observed a two-way causality between renewable energy use and growth in emerging Asian economies during 1975–2020, supporting the feedback hypothesis. Wang et al. (2023b) confirmed a two-way causal relationship between renewable energy consumption and economic growth, supporting the feedback hypothesis in seven selected Northeast Asian economies from 1970 to 2020.

Petroleum Consumption-Economic Growth Nexus

Several earlier research studies have examined the causal link between petroleum (oil) usage and economic development. For example, Aqeel and Butt (2001) study shows that growth leads to an expansion in petroleum usage in Pakistan from 1995 to 1996. The empirical finding of Wolde-Rafael (2004) study on disaggregated energy series shows no Granger causality between oil use and real GDP in Shanghai over the period 1952–1999. Lee and Chang (2005) study indicate a one-way causation from oil use to GDP in Taiwan from 1954 to 2003. Asghar (2008) assessed the causal linkage between different sources of energy usage and economic progress for a sample of 5 South Asian nations, namely, Pakistan, Sri Lanka, India, Nepal, and Bangladesh. The study finds causality from petroleum consumption to GDP in Nepal from 1971 to 2003. The study of Odhiambo (2010) revealed a causal run in one direction from oil prices to economic growth in South Africa from 1969 to 2007. Chu and Chang (2012) analyzed whether energy usage encourages economic development in the G-6 countries (i.e., The US, Japan, Canada, UK, Germany, and France) from 1971 to 2010. The study finds uni-causation from economic development to oil usage in the US, while in G-6 countries, oil use does not cause economic progress except in Japan and Germany. The empirical outcomes of Chu (2012) study showed the feedback hypothesis for 7 nations, the growth hypothesis for 5 nations, the neutrality hypothesis for 24 nations, and the conservation hypothesis for 13 nations, and in total 49 countries during 1970–2010. In a similar study, Dantama et al. (2012) revealed that petroleum usage’s influence on economic development was significantly positive in Nigeria during 1980–2010.

The empirical results of Fuinhas and Marques (2012) study indicate that oil usage causes economic progress in the long and short run. Similarly, economic progress caused oil consumption in Portugal in the long and short run from 1965 to 2009. In their study, Bhattacharya and Bhattacharya (2014) observed one-way causation from petroleum usage to economic progress both in the long run and short run in both China and India during 1980–2010. Nasiru et al. (2014) find one-way causation from oil usage to economic progress in Nigeria from 1980 to 2011. The findings of Park and Yoo (2014) study support two-way causation between oil usage and economic progress in Malaysia during 1965–2011. Lim et al. (2014) revealed two ways of connection between oil use and economic progress in the Philippines during 1965–2012. Finally, the empirical findings of Akinlo’s (2021) study support Nigeria’s conservation hypothesis over the period 1980–2016, indicating that oil preservation methods may not inevitably hurt economic growth. Kocaslan and Yilanci (2010) study indicated that oil use had an inverse effect on economic development in Turkey during 1970–2007 in the long run. Similarly, the study of Mahmoudinia et al. (2013) found a one-way causal effect of oil product usage on economic progress. In contrast, the effect of oil product usage on economic development in Iran, in the long run, is negative during 1973–2006.

Natural Gas Consumption-Economic Growth Nexus

Many prior studies have evaluated the nexus between natural gas and economic growth. For example, Yang (2000) found one-way Granger causality from natural gas usage to economic progress in Taiwan during 1954–1997. Fatai et al. (2004) observed causation between economic growth and various disaggregated data of energy resources (natural gas, coal, electricity, and oil) in New Zealand during 1960–1999. Lee and Chang (2005) also observed the presence of a one-way causation from gas use to economic progress in Taiwan during 1954–2003. Zamani (2007) found that in the long run, bidirectional causation between natural gas usage and economic progress existed in Iran from 1967 to 2003. Ewing et al. (2007) revealed that unforeseen shocks in natural gas have the maximum effect on the variation of output in the US from 2001:1 to 2005:6. Reynolds and Kolodziej (2008) found that the relationship between natural gas and GDP showed alternative Granger causalities in the Former Soviet Union during 1987–1996. In a study by Kum et al. (2012) on G-7 countries, the linkage between natural gas usage and economic development during 1970–2008 was assessed. In the case of Italy, the causal association is running from natural gas usage to economic progress, while for Germany, the US, and France, bidirectional causation between gas usage and economic progress was observed.

Similarly, Yazdi and Mastorakis (2014) found causality between gas usage and economic growth in Iran during 1975–2011 and thereby confirmed the feedback hypothesis between gas usage and economic progress. The causality analysis of Shahbaz et al. (2014) implies that the feedback hypothesis is proven between gas usage and economic progress in France during the period 1970–2010. The empirical findings of Aydin (2018) study reveal a long-run association between gas usage and economic progress, and natural gas usage has a substantial and positive effect on economic development in the long run in the top 10 gas-consuming economies from 1994–2015. Farhani and Rahman (2020) observed that natural gas usage and some other regressors contributed to France’s economic progress from 1990 to 2014. Bulkani et al. (2021) found that natural gas usage negatively affected Indonesia’s economic growth from 1980 to 2018. Hasan and Raza (2022) observed that natural gas consumption and income (economic growth) have a bidirectional link in Bangladesh during 1990–2019.

Coal Consumption-Economic Growth Nexus

The extant literature shows that some studies have explored the causal association between coal usage and economic development; for example, the empirical finding of Wolde-Rafael (2004) study indicated a one-way causality from coal use to economic development in Shanghai for the period 1952–1999. Lee and Chang (2005) outcomes confirmed that a bidirectional causal association between GDP and coal usage was detected during the period 1954–2003 in Taiwan. Asghar (2008) study suggests one-way causation running from coal usage to economic progress in Pakistan during 1971 to 2003 among five South Asian countries. Reynolds and Kolodziej (2008) study suggest that coal consumption to GDP relationships show alternative Granger causalities in the Former Soviet Union from 1987–1996. The panel causality tests of Apergis and Payne (2010) study indicate two ways of causation between coal usage and economic development in the long and short run for 15 emerging market economies during 1980–2006. The study of Jinke and Zhongxue (2011) indicates a one-way causal association between economic progress and coal usage in China. One-way causation from coal usage to economic progress was found in India from 1965–2006. However, Dantama et al. (2012) study shows that the estimated coefficient of coal is positive but statistically insignificant in Nigeria during 1980–2010. The findings of Bhattacharya and Bhattacharya (2013) discovered that two-way causation exists between economic development and coal usage in India.

The study by Ocal et al. (2013) found no causal relationship between coal usage and GDP in Turkey from 1980 to 2006, supporting the neutrality hypothesis for Turkey. However, the empirical findings of Shaari et al. (2013) suggest that coal usage does not Granger-cause economic development in Malaysia from 1980 to 2010. Bhattacharya and Bhattacharya (2014) indicated a two-way causation between economic development and coal usage in India from 1980 to 2010, both in the short and long run. In the case of China, one-way causation from economic development to coal usage was observed in both the short and long run. Anoruo (2017) found one-way causation from economic progress to coal usage for 15 African countries. Lin et al. (2018) confirmed feedback between coal usage and economic progress in China from 1969 to 2015, while a one-way Granger causation from coal use to economic development was observed in India. The empirical results of Chen et al. (2022) reveal that energy (coal consumption) played an important role in driving China’s economic growth from 2005 to 2012. Wang et al. (2023a) implemented the Dumitrescu and Hurlin Granger causality test and established a causal link between non-renewable energy use and GDP in five emerging Asian economies from 1975 to 2020, supporting the feedback hypothesis.

Data and Empirical Methodology

This study aims to investigate the impact of energy usage (coal, natural gas, electricity, and petroleum) on the economic growth of BRICS countries. In 2021, the BRICS countries had a total GDP of 23.5 trillion US dollars and consumed 37.79% of the world’s total energy, with China playing a leading role with 22.71% of energy consumption. In 2019, global energy consumption was distributed as follows: oil consumption accounted for 30.91%, coal for 25.31%, natural gas for 22.69%, waste and biofuels for 7.92%, hydro for 6.05%, nuclear for 4.02%, and others for 3.08% (Khan & Osińska, 2021). The selected variables are important due to their widespread usage. Furthermore, the analysis covers the period from 1990 to 2020 due to data availability. A brief summary of the variables, data, and their sources is provided in Table 1.

Empirical Model

The multivariate regression model within the economic growth theory framework by Solow (1956) and Mankiw et al. (1992) and also used in many prior studies including Wang et al. (2023a), Azam (2022), Ali et al. (2022), Azam and Khan (2022), and Aydin (2018) can be written as follows.

where gdp represents economic growth, coal is coal consumption, electric is the electricity consumption, petrol is petroleum consumption, gas is the natural gas use, fdi is net foreign direct investment inflows, labfr is labor force, and ε is an error term. The selection of variables in this study is based on their usage in daily life mainly for production. Chen et al. (2022) observed that coal usage is the key driver for China’s production and its economic growth. Similarly, Hasan and Raza (2022) revealed that gas consumption is the main factor in Bangladesh’s economic activities while Güler et al. (2022) assessed that the European economy mostly relies on electricity usage. Akinlo (2021) found out that least developing countries mostly used petroleum for their economic production.

Estimation Procedure

The globalization of the world’s economy has promoted interconnectivity and the transfer of shocks from one economy to another. Therefore, interdependence among countries is possible. The study proceeds with Pesaran (2007) cross-sectional dependence (CSD) test. The CSD test is important to ensure unbiased estimates and estimator efficiency. We further applied the Covariate Augmented Dickey-Fuller (CADF) and Cross-sectionally augmented Im, Pesaran and Shin (CIPS) tests, to ascertain the stationarity properties of the variables. However, once variables are stationary, a cointegration test is required to determine the possibility of a long-run association. In this contribution, the Westerlund (2007) test investigates the existence of cointegration. Like the Pesaran test, the Westerlund (2007) test is robust amidst CSD. However, it performs better than the traditional first-generation cointegration tests, including the Kao and Chiang (1999) and Pedroni (2000) cointegration tests.

In the panel data set, before conducting the unit root test for all variables, this study first checked for slope homogeneity (SH) and cross-sectional dependence (CSD) test. Pesaran and Yamagata (2008) proposed a technique for slope-homogeneity, while Pesaran (2007) introduced an SH test for the existence of slope homogeneity in panel data models. Using the tests mentioned above is a prerequisite before confirming the presence of a unit root. The mathematical form of the SH test is given as follows:

To investigate the relationship among the variables, i.e., cointegration analysis, this study used the method of Westerlund (2007). The advantage of Westerlund technique is that it covers the existence of slope homogeneity and cross-sectional dependence. However, following the conventional methods for the analysis will give biased results (Kapetanios et al., 2011). Moreover, the traditional techniques provide partial output, leading to wrong policy implication suggestions. Therefore, this research analyzed the long- and short-run output analysis using Chudik and Pesaran (2015) CD-ARDL. The mathematical form is given as follows:

The problem with Eq. (4) is that it cannot solve the problems of the existence of a unit root, unobservable factors, slope-homogeneity, and cross-sectional-dependence. Therefore, modifying the above equation leads to the following:

Using cross-section averages, Eq. (5) resolves the concerns in the above discussion and eliminates the threshold effect (Chudik & Pesaran, 2015).

Equation (5) shows the averages and lags, while Eq. (6) shows the long-run coefficients.

The mean group is given in Eq. (7) as below:

The short- and long-run coefficient analysis is calculated in Eq. (8) and given as follows:

Equation (8a) shows the Error Correction Model with a negative value indicating convergence to equilibrium. The Augmented Mean Group (AMG) test is applied for robustness verification. This test deals with unobserved factors, homogeneity, cross-sectional independence, and non-stationarity of variables. This study also used the Dumitrescu and Hurlin (2012) test to check the causality among variables.

Results and Discussion

Table 2 provides a summary of the descriptive statistics for all variables, while Table 3 presents the results of the cross-sectional dependence test, which confirms the dependency among variables. The null hypothesis of no cross-section independence is rejected. The high mean absolute value indicates high dependence, confirming that shocks in one BRICS country will affect the others. The high value of each variable demonstrates high dependency, indicating that shocks in one country will affect the others.

Table 4 indicates the results of the slope homogeneity test, with low p-values rejecting the null hypothesis of slope homogeneity. These results confirm the heterogeneity in cross-sectional coefficients.

Table 5 presents the unit root results using CADF and CIPS tests, confirming that all variables are non-stationary at level I (0) and stationary at the first difference, I (1), at various significance levels. Westerlund’s (2007) co-integration analysis demonstrates the long-run relationship of all variables in the study. Both Westerlund’s (2007) and CS-ARDL approaches address cross-section independence and slope homogeneity in the panel data (Khan et al., 2020).

Table 6 confirms co-integration analysis using the method of Westerlund (2007), showing long-run results. The lower p-value indicates a long-run association among the variables in this study. The findings confirm that Gt and Ga are the group means statistics, while Pt and Pa are the overall panel statistics.

Table 7 shows the short-run and long-run outcomes using Chudik and Pesaran (2015) CS-ARDL. No study has been conducted on disaggregated forms of energy usage on economic progress for BRICS nations. This study’s results show that electricity has a significant positive influence in the short run. If measures encouraging less electricity usage have an impact on growth, then consumption must be a factor in economic growth. Electricity conservation regulations would not have an effect on growth if consumption does not create economic growth or if consumption causes economic growth. Finally, if findings support that electricity and economic growth are correlated, any strategy to cut back on power use in an effort to lower emissions would have an effect on BRICS GDP. At the same time, natural gas and petrol also substantially positively influence economic development at 10% and 5% significance levels, respectively. The results of this study revealed that natural gas has little significance in the short run, but this significantly increased in the long run, confirming that gas also promotes economic growth, and this result is in line with the findings of Aydin (2018) research. Emissions from natural gas are 50% and 20% lower than those from petroleum and coal. A cleaner energy source is natural gas than coal or oil in this regard. In addition, natural gas outperforms renewable energy sources in terms of efficiency and dependability (Lee & Chang, 2005). Rahman (2021) also revealed that energy usage and economic progress have a positive relationship and bidirectional causality for the sample of BRICS nations, and the results of this study are in line with the author’s findings.

In this study, the outcomes show that coal energy use and economic growth have a positive relationship in the long run as well as in the short run at a 1% significance level. These results are consistent with the findings of Kartal et al. (2023), who suggested that coal and economic growth have a strong bidirectional relationship at a 10% significance level and recommended reducing coal consumption to minimize the impact on environmental quality. In a similar study by Chang et al. (2017), the authors found no clear causal relationship between coal and economic growth. Despite the fact that many nations still have significant coal reserves, their economic growth is heavily dependent on energy usage. Given the link between economic growth and coal consumption, conservation measures aimed at reducing coal use could be implemented with little to no negative effects on growth.

Energy consumption by gas is considered a very crucial factor among energy consumption determinants. The findings of this study revealed that gas and economic growth have positive combinations both in the long and short run. These findings of this study are consistent with the outcomes of the study of Bildirici and Bakirtas (2014), but the authors were unable to find any causal relationship between gas and economic growth for BRICS. The authors were of the view that only bidirectional causality exists for Brazil and Russia. This study also finds a positive impact of electricity usage on economic growth, both in the long and short run. These results are consistent with the findings of Aydin (2019), who conducted a study on OECD countries and found a bi-causal relationship between electricity and economic growth using the DH test. Additionally, the study found evidence of a temporary feedback hypothesis for the sampled countries using the Croux and Reusens test. The consumption of petrol is considered a crucial factor for driving economic activities in a country. This study has found that petrol has a statistically significant and positive impact on the economic growth of BRIC countries. These results are consistent with a study by Le and Sarkodie (2020), which found similar results for emerging and developing countries. The authors also revealed that there is a feedback hypothesis between petrol consumption and economic growth, as causality runs in both directions.

The Augmented Mean Group (AMG) analysis, first published by Teal and Eberhardt (2010), is used as a robustness test to validate the results obtained using CS-ARDL. The AMG analysis addresses issues of cross-sectional dependency and slope uniformity (Teal & Eberhardt, 2010). The results, as shown in Table 8, confirm the findings of the CS-ARDL, indicating that disaggregated energy consumption has a significantly positive impact on the economic progress of BRICS countries.

The Variance Inflation Factor (VIF) test was used to check for multicollinearity among the variables in this study. The results in Table 9 show that there is no multicollinearity among the variables, as each VIF value is less than 10. This indicates that the choice of variables is accurate, ensuring that the model specification and parameter estimation are reliable (Neter et al., 1985; Salmerón-Gómez et al., 2016).

The panel Granger causality test by Dumitrescu and Hurlin (2012) was used to determine the direction of causality, as presented in Table 10. At a 5% significance level, the DH test findings indicate that all the key variables, except gas, have a distinct directional causation relationship and exhibit either neutral or feedback hypothesis. These results on the disaggregated energy consumption and economic growth nexus suggest that any strategy aimed at these variables to achieve maximum economic growth will yield positive results.

Concluding Remarks

The CS-ARDL model reveals all the variables used in this study for long and short-run analysis. The major findings of this study are that all forms of energy consumption, along with the labor force and inward FDI, have a significant impact on the economic growth of BRICS nations. Petroleum has a substantially positive effect on economic growth, while electricity promotes growth in the long and short run. Coal is the most significant among all variables, whereas natural gas has a long-run positive connection with economic progress. These results are further confirmed by the AMG technique used for robustness checks. Previous research on the influence of energy and economic development used total energy usage and ignored energy at the disaggregated level. Thus, this study empirically investigates the causal nexus between energy at the disaggregate levels covering coal, electricity, natural gas, and petroleum because their usage intensity, weaknesses, opportunities, and dangers necessitate scientific exploration.

This study employed the second- and third-generation panel cointegration methodologies. The cross-sectional dependency and slope heterogeneity tests confirmed that the panels are correlated and exhibit slope heterogeneity. This study implemented Westerlund cointegration analysis to verify the long-run association between the variables. To measure the long and short-run effects of the variables, CS-ARDL was used. The results confirmed a connection between the disaggregated levels covering coal, electricity, natural gas, petroleum, and economic growth. Coal was found to have the most significant impact on economic development in both the short and long run. Similarly, natural gas had a significant but small impact on economic growth in the short run, which increased significantly in the long run. These results were confirmed using the AMG technique. The Granger causality test result confirms the causal relationship between coal consumption and economic growth, electricity and economic growth, and petroleum and economic growth, supporting the feedback hypotheses, while natural gas consumption and economic growth support the neutral hypothesis. The causality test results demonstrated that any strategy targeting coal, natural gas, petrol, and electricity would significantly enhance economic growth. Thus, energy consumption is a significant driver of suitable economic growth in BRICS economies.

In light of the empirical findings, energy is vital for sustainable economic growth in BRICS economies. In order to improve energy efficiency, policies should focus more on adjusting energy consumption structures and increasing proficient energy utilization technology which is more important in speeding economic development to boost energy efficient usage. Energy authorities should promote the clean and efficient use of disaggregated forms of energy consumption to ensure energy supply and security. The government must mobilize the masses to focus on renewable sources of energy rather than using coal and other traditional sources of energy. The country’s economic growth would not be hampered by environmental measures to cut coal-generated electricity, but they will undoubtedly benefit the environment, as developed countries move toward other forms of energy sources like wind and solar. Therefore, the governments of BRICS countries need to incentivize technological-based solarization in their countries. As energy consumption sources of this study have positive impact on economic growth, there is a dire need to shift and rely more on renewable energy sources than traditional and conventional sources of energy usage. Natural gas is a viable source of energy for BRICS countries, so a future plan should be set for more environmentally friendly usage to keep a check on pollution. This study endorses the idea that policymakers need to devise and implement energy policies that enhance domestic and foreign investments in the energy sector. In addition, the BRICS Development Bank raises money and distributes it among the BRICS nations to adapt innovations and technology in a disaggregated form of energy utilization. A planned activity of capacity building for industrial labor needs to be implemented on a regular basis to make them familiar with updated technologies.

Data Availability

Data used in this study for empirical examination have been obtained from the World Development Indicators (2022), the World Bank publication, and Statistical review of World Energy (2022), https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.

References

Akinlo, A. E. (2021). Petroleum consumption and economic growth nexus in Nigeria: Evidence from nonlinear ARDL and causality approaches. Journal of Quantitative Economics, 19(4), 819–844. https://doi.org/10.1007/s40953-021-00254-y

Ali, A., Radulescu, M., & Balsalobre-Lorente, D. (2023). A dynamic relationship between renewable energy consumption, nonrenewable energy consumption, economic growth, and carbon dioxide emissions: Evidence from Asian emerging economies. Energy & Environment, 34(8), 3391–3416.

Ali, A., Radulescu, M., Lorente, D. B., & Hoang, V. V. (2022). An analysis of the impact of clean and non-clean energy consumption on economic growth and carbon emission: Evidence from PIMC countries. Environmental Science and Pollution Research, 29, 51442–51455.

Anoruo, E. (2017). Coal consumption and economic growth nexus: Evidence from bootstrap panel Granger causality test. Panoeconomicus, 64(3), 255–271.

Apergis, N., & Payne, J. E. (2010). The causal dynamics between coal consumption and growth: Evidence from emerging market economies. Applied Energy, 87(6), 1972–1977.

Aqeel, A., & Butt, M. S. (2001). The relationship between energy consumption and economic growth in Pakistan. Asia-Pacific Development Journal, 8(2), 101–109.

Asghar, Z. (2008). Energy-GDP relationship: A causal analysis for the five countries of South Asia. Applied Econometrics and International Development, 8(1), 167–180.

Aydin, M. (2018). Natural gas consumption and economic growth nexus for top 10 natural gas–consuming countries: A granger causality analysis in the frequency domain. Energy, 165, 179–186.

Aydin, M. (2019). Renewable and non-renewable electricity consumption–economic growth nexus: Evidence from OECD countries. Renewable Energy, 136, 599–606.

Azam, M. (2020). Energy and economic growth in developing Asian economies. Journal of the Asia Pacific Economy, 25(3), 447–471.

Azam, M. (2022). Governance and economic growth: Evidence from 14 Latin America and Caribbean countries. Journal of the Knowledge Economy, 13, 1470–1495. https://doi.org/10.1007/s13132-021-00781-2

Azam, M., & Khan, S. (2022). Threshold effects in the relationship between inflation and economic growth: Further empirical evidence from the developed and developing world. International Journal of Finance and Economics, 27(4), 4224–4243.

Azam, M., & Raza, A. (2022). Does foreign direct investment limit trade-adjusted carbon emissions: Fresh evidence from global data. Environmental Science and Pollution Research, 29(25), 37827–37841.

Bayar, Y., & Özel, H. A. (2014). Electricity consumption and economic growth in emerging economies. Journal of Knowledge Management, Economics and Information Technology, 4(2), 1–18.

Belaid, F., & Abderrahmani, F. (2013). Electricity consumption and economic growth in Algeria: A multivariate causality analysis in the presence of structural change. Energy Policy, 55, 286–295.

Bhattacharya, M., & Bhattacharya, S. N. (2013). Energy consumption and economic growth nexus in the Indian context. Journal of Rural and Industrial Development, 1(2), 6–14.

Bhattacharya, M., & Bhattacharya, S. N. (2014). Economic growth and energy consumption nexus in developing world: The case of China and India. Journal of Applied Economics and Business Research, 4(3), 150–167.

Bildirici, M. E., & Bakirtas, T. (2014). The relationship among oil, natural gas and coal consumption and economic growth in BRICTS (Brazil, Russian, India, China, Turkey and South Africa) countries. Energy, 65, 134–144.

Bp. (2022). Bp Statistical Review of World Energy. British Petrolium. https://www.bp.com/content/dam/bp/businesssites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2022-full-report.pdf

Bulkani, B., Sonedi, S., & Putra, C. A. (2021). The natural gas consumption and economic development nexus: Fresh evidence from Indonesia. International Journal of Energy Economics and Policy, 11(1), 607–614.

Chang, T., Deale, D., Gupta, R., Hefer, R., Inglesi-Lotz, R., & Simo-Kengne, B. (2017). The causal relationship between coal consumption and economic growth in the BRICS countries: Evidence from panel-Granger causality tests. Energy Sources, Part B: Economics, Planning, and Policy, 12(2), 138–146.

Chen, H., Liu, K., Shi, T., & Wang, L. (2022). Coal consumption and economic growth: A Chinese city-level study. Energy Economics, 109(C), 105940.

Chu, H. P. (2012). Oil consumption and output: What causes what? Bootstrap panel causality for 49 countries. Energy Policy, 51, 907–915.

Chu, H. P., & Chang, T. (2012). Nuclear energy consumption, oil consumption and economic growth in G-6 countries: Bootstrap panel causality test. Energy Policy, 48, 762–769.

Chudik, A., & Pesaran, M. H. (2015). Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. Journal of Econometrics, 188, 393–420.

Ciarreta, A., & Zarraga, A. (2010). Economic growth-electricity consumption causality in 12 European countries: A dynamic panel data approach. Energy Policy, 38(7), 3790–3796.

Dantama, Y. U., Abdullahi, Y. Z., & Inuwa, N. (2012). Energy consumption-economic growth nexus in Nigeria: An empirical assessment based on ARDL bound test approach. European Scientific Journal, 8(12), 141–157.

Dumitrescu, E. I., & Hurlin, C. (2012). Testing for Granger non-causality in heterogeneous panels. Economic Modeling, 29(4), 1450–1460.

Ewing, B. T., Sari, R., & Soytas, U. (2007). Disaggregate energy consumption and industrial output in the United States. Energy Policy, 35(2), 1274–1281.

Farhani, S., & Rahman, M. M. (2020). Natural gas consumption and economic growth nexus: An investigation for France. International Journal of Energy Sector Management, 14(2), 261–284.

Fatai, K., Oxley, L., & Scrimgeour, F. G. (2004). Modelling the causal relationship between energy consumption and GDP in New Zealand, Australia, India, Indonesia, the Philippines and Thailand. Mathematics and Computers in Simulation, 64(3–4), 431–445.

Fuinhas, J. A., & Marques, A. C. (2012). An ARDL approach to the oil and growth nexus: Portuguese evidence. Energy Sources, Part B: Economics, Planning, and Policy, 7(3), 282–291.

Güler, H., Haykır, Ö., & Öz, S. (2022). Does the electricity consumption and economic growth nexus alter during COVID-19 pandemic? Evidence from European countries. The Electricity Journal, 35(6), 107144.

Hasan, M. M., & Raza, M. Y. (2022). Nexus of natural gas consumption and economic growth: Does the 2041 Bangladesh development goal realistic within its limited resource. Energy Strategy Reviews, 41, 100863.

Jinke, L., & Zhongxue, L. (2011). A causality analysis of coal consumption and economic growth for China and India. Natural Resources, 2(1), 54–60.

Kao, C., & Chiang, M.-H. (1999). On the estimation and inference of a cointegrated regression in panel data. Available at SSRN: https://ssrn.com/abstract=1807931 or https://doi.org/10.2139/ssrn.1807931. Accessed on Jan 17, 2024.

Kapetanios, G., Pesaran, M. H., & Yamagata, T. (2011). Panels with non-stationary multifactor error structures. Journal of Econometrics, 160(2), 326–348.

Kartal, M. T., Ertuğrul, H. M., Taşkın, D., & Ayhan, F. (2023). Asymmetric nexus of coal consumption with environmental quality and economic growth: Evidence from BRICS, E7, and fragile five countries by novel quantile approaches. Energy & Environment, 0958305X231151675. https://journals.sagepub.com/doi/full/10.1177/0958305X231151675?casa_token=Kf0MVzohZj4AAAAA%3AUyPMf3IXDO_H-uzJ6vsrQ1-MvalxbL7Ha57W7J4VhOIyiDBbFGa9oPGDmqUxYPPDYfqHAEYgkJ5Ipg

Khan, A. M., & Osińska, M. (2021). How to predict energy consumption in BRICS countries. Energies, 14(10), 2749.

Khan, Z., Ali, S., Umar, M., Kirikkaleli, D., & Jiao, Z. (2020). Consumption-based carbon emissions and international trade in G7 countries: The role of environmental innovation and renewable energy. Science of the Total Environment, 730, 138945.

Kocaslan, G., & Yilanci, V. (2010). Oil consumption and economic growth: Evidence from Turkey. Energy Studies Review, 17(1), 26–32.

Kraft, J., & Kraft, A. (1978). On the relationship between energy and GNP. Journal of Energy and Development, 3, 401–403.

Kum, H., Ocal, O., & Aslan, A. (2012). The relationship among natural gas energy consumption, capital and economic growth: Bootstrap-corrected causality tests from G-7 countries. Renewable and Sustainable Energy Reviews, 16(5), 2361–2365.

Le, H. P., & Sarkodie, S. A. (2020). Dynamic linkage between renewable and conventional energy use, environmental quality and economic growth: Evidence from emerging market and developing economies. Energy Reports, 6, 965–973.

Lean, H. H., & Smyth, R. (2010). CO2 emissions, electricity consumption and output in ASEAN. Applied Energy, 87(6), 1858–1864.

Lee, C. C., & Chang, C. P. (2005). Structural breaks, energy consumption, and economic growth revisited: Evidence from Taiwan. Energy Economics, 27(6), 857–872.

Lim, K. M., Lim, S. Y., & Yoo, S. H. (2014). Oil consumption, CO2 emission, and economic growth: Evidence from the Philippines. Sustainability, 6, 967–979.

Lin, F. L., Inglesi-Lotz, R., & Chang, T. (2018). Revisit coal consumption, CO2 emissions and economic growth nexus in China and India using a newly developed bootstrap ARDL bound test. Energy Exploration & Exploitation, 36(3), 450–463.

Lindenberger, D., & Kummel, R. (2002). Energy-dependent production functions and the optimization model “PRISE” of price-induced sectoral evolution. International Journal of Applied Thermodynamics, 5(3), 101–107.

Mahmoudinia, D., Amroabadi, B. S., Pourshahabi, F., & Jafari, S. (2013). Oil products consumption, electricity consumption-economic growth nexus in the economy of Iran: A bound testing cointegration approach. International Journal of Academic Research in Business and Social Sciences, 3(1), 3535–4367.

Mankiw, N. G., Romer, D., & Weil, D. N. (1992). A contribution to the empirics of economic growth. The Quarterly Journal of Economics, 107(2), 407–437.

Mighri, Z., & Ragoubi, H. (2020). Electricity consumption–economic growth nexus: Evidence from ARDL bound testing approach in the Tunisian context. Global Business Review. https://doi.org/10.1177/0972150920925431

Narayan, P. K., & Prasad, A. (2008). Electricity consumption-real GDP causality nexus: Evidence from a bootstrapped causality test for 30 OECD countries. Energy Policy, 36(2), 910–918.

Nasiru, I., Usman, H. M., & Saidu, A. M. (2014). Oil consumption and economic growth: Evidence from Nigeria. Bulletin of Energy Economics, 2(4), 106–112.

Neter, J., Wasserman, W., & Kutner, M. H. (1985). Applied linear statistical models: Regression. Analysis of variance, and experimental designs (2nd ed.), Richard D.

Ocal, O., Ozturk, I., & Aslan, A. (2013). Coal consumption and economic growth in Turkey. International Journal of Energy Economics and Policy, 3(2), 193–198.

Odhiambo, N. M. (2009a). Electricity consumption and economic growth in South Africa: A trivariate causality test. Energy Economics, 31(5), 635–640.

Odhiambo, N. M. (2009b). Energy consumption and economic growth nexus in Tanzania: An ARDL bounds testing approach. Energy Policy, 37(2), 617–622.

Odhiambo, N. M. (2010). Finance-investment-growth nexus in South Africa: An ARDL-bounds testing procedure. Economic Change and Restructuring, 43(3), 205–219.

Park, S. Y., & Yoo, S. H. (2014). The dynamics of oil consumption and economic growth in Malaysia. Energy Policy, 66, 218–223.

Pedroni, P. (2000). Fully modified OLS for heterogeneous cointegrated panels. Advances in Econometrics, 15, 93–130.

Pesaran, M. H. (2007). A simple panel unit root test in the presence of cross-section dependence. Journal of Applied Econometrics, 22(2), 265–312.

Pesaran, M. H., & Yamagata, T. (2008). Testing slope homogeneity in large panels. Journal of Econometrics, 142(1), 50–93.

Pokharel, S. (2007). An econometric analysis of energy consumption in Nepal. Energy Policy, 35(1), 350–361.

Rahman, M. M. (2021). The dynamic nexus of energy consumption, international trade and economic growth in BRICS and ASEAN countries: A panel causality test. Energy, 229, 120679. https://doi.org/10.1016/j.energy.2021.120679

Reynolds, D. B., & Kolodziej, M. (2008). Former Soviet Union oil production and GDP decline: Granger causality and the multi-cycle Hubbert curve. Energy Economics, 30(2), 271–289.

Saidi, K., & Hammami, S. (2015). The impact of energy consumption and CO2 emissions on economic growth: Fresh evidence from dynamic simultaneous-equations models. Sustainable Cities and Society, 14, 178–186.

Salmerón-Gómez, R., García-Pérez, J., López-Martín, M. D. M., & García, C. G. (2016). Collinearity diagnostic applied in ridge estimation through the variance inflation factor. Journal of Applied Statistics, 43(10), 1831–1849.

Shaari, M. S., Hussain, N. E., & Ismail, M. S. (2013). Relationship between energy consumption and economic growth: Empirical evidence for Malaysia. Business Systems Review, 2(1), 17–28.

Shahbaz, M., Farhani, S., & Rahman, M. M. (2014). Natural gas consumption and economic growth nexus: The role of exports, capital and labor in France, Working Paper 2014–583. IPAG Business School, Paris-France.

Shahbaz, M., & Lean, H. H. (2012). The dynamics of electricity consumption and economic growth: A revisit study of their causality in Pakistan. Energy, 39(1), 146–153.

Solow, R. M. (1956). A contribution to the theory of economic growth. The Quarterly Journal of Economics, 70(1), 65–94.

Stern, D. I., & Cleveland, J. C. (2004). Energy and economic growth. Rensselaer Working Papers in Economics No. 0410.

Stern, D. I. (2000). A multivariate cointegration analysis of the role of energy in the US macroeconomy. Energy Economics, 22(2), 267–283.

Stern, D. I. (2011). The role of energy in economic growth. Annals of the New York Academy of Sciences, 1219(1), 26–51.

Teal, F., & Eberhardt, M. (2010). Productivity analysis in global manufacturing production. Economics Series Working Papers 515, University of Oxford, Department of Economics. Retrieved from https://ora.ox.ac.uk/objects/uuid:f9d91b40-d8b7-402d-95eb-75a9cbdcd000. Accessed on Dec 14, 2023.

Wang, L., Ali, A., Ji, H., Chen, J., & Ni, G. (2023a). Links between renewable and non-renewable energy consumption, economic growth, and climate change, evidence from five emerging Asian countries. Environmental Science and Pollution Research, 30, 83687–83701.

Wang, Q., Ali, A., Chen, Y., & Xi, X. (2023b). An empirical analysis of the impact of renewable and non-renewable energy consumption on economic growth and carbon dioxide emissions: Evidence from seven Northeast Asian countries. Environmental Science and Pollution Research, 30, 75041–75057.

Warsame, A. A., Alasow, A. A., & Salad, M. A. (2024). Energy consumption and economic growth nexus in Somalia: An empirical evidence from nonlinear ARDL technique. International Journal of Sustainable Energy, 43(1), 2287780. https://doi.org/10.1080/14786451.2023.2287780

Westerlund, J. (2007). Testing for error correction in panel data. Oxford Bulletin of Economics and Statistics, 69(6), 709–748.

Wolde-Rafael, Y. (2004). Disaggregated industrial energy consumption and GDP: The case of Shanghai 1952–1999. Energy Economics, 26(1), 69–75.

Wolde-Rufael, Y. (2006). Electricity consumption and economic growth: A time series experience for 17 African countries. Energy Policy, 34(10), 1106–1114.

World Development Indicators. (2022). The World Bank Publication

Yang, H. Y. (2000). A note on the causal relationship between energy and GDP in Taiwan. Energy Economics, 22, 309–317. https://doi.org/10.1016/S0140-9883(99)00044-4

Yazdi, S. K., & Mastorakis, N. (2014). Natural gas consumption and economic growth in Iran. Advances in environmental technology and biotechnology, 165–172. Retrieved from http://www.wseas.us/e-library/conferences/2014/Brasov/BIOLET/BIOLET-25.pdf. Accessed on Feb 4, 2024.

Zamani, M. (2007). Energy consumption and economic activities in Iran. Energy Economics, 29(1), 1135–1140.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of Interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Raza, A., Khan, M.A. & Bakhtyar, B. Exploring the Linkage Between Energy Consumption and Economic Growth in BRICS Countries Through Disaggregated Analysis. J Knowl Econ (2024). https://doi.org/10.1007/s13132-024-02045-1

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s13132-024-02045-1