Abstract

This paper aims to analyze the impact of foreign aid on economic growth in Ethiopia using time series data over the period 1974–2017. Autoregressive distributed lag approach to co-integration and error correction model was applied to investigate the long-run and short-run impact of foreign aid on economic growth. The model results revealed that foreign aid has a negative impact on economic growth in both the long run and short run. The negative and significant error correction term shows that the short-run disequilibrium adjusts to its long-run equilibrium by 84.6% each year. The paper suggested that more effort has to be made to improve the negative impact of foreign aid, mainly because of the existence of poor institutional arrangements that contribute the funds to unproductive sectors. The government has to ensure a close monitoring and consistent management strategies, which are used to avoid misallocation and mismanagement problems and has to ensure that foreign aid is linked to the productive sectors to optimize the benefits.

Similar content being viewed by others

Introduction

In recent times, the global financial crisis of 2007/2008, climate change, the global COVID-19 pandemic, and the current Russo-Ukrainian war have featured prominently in policy circles because these global crises can harm countries that depend on foreign aid from developed countries. Consequently, there have been growing calls for governments in developed countries, international organizations, and non-governmental organizations to not cut back on foreign aid to developing countries (Heinrich et al., 2016; OECD, 2019). This is because a cut in foreign aid could adversely impact the poor and the most vulnerable in developing countries (Boateng et al., 2021). Some recent studies have provided empirical evidence to suggest that aid cuts by donors tend to linger (see Arellano et al., 2009; Frot, 2009; Frot & Perrotta, 2012; Heinrich et al., 2016). However, Heinrich et al. (2016) noted that, although the economic crisis experienced by developed countries tends to cause a reduction in aid flows to developing countries, empirical evidence suggests that foreign donors do increase rather than decrease aid flows to developing countries (see also Perotti, 2005; Auerbach, 2009; Egert, 2015). Despite this, in response to global shocks, some developed country governments have reduced their aid commitments and aid disbursement (OECD, 2019).

Given that many developing countries remain financially constrained (Haile, 2015) and depend on foreign aid (see Sachs, 2005; OECD, 2019), a critical feature of the policy discourse has focused on aid effectiveness (see Bjerg et al., 2011; Civelli et al., 2018; Jena & Sethi, 2020; Ilorah & Ngwakwe, 2021). Despite some existing theoretical and empirical evidence on foreign aid effectiveness in driving economic growth, the empirics are complicated and unresolved. On the one hand, proponents of foreign aid argue that aid stimulates economic growth by relieving developing countries from the problem of capital scarcity by supporting the physical and human capital development necessary to sustain economic growth (Sachs, 2005; Easterly et al., 2004; Clemens et al., 2012; Juselius et al., 2014; Heinrich et al., 2016; Galiani et al., 2017). On the other hand, critics argue that increased aid to developing countries has impeded economic growth by displacing savings, thus creating aid-dependency problems (Rajan & Subramanian, 2011; Liew et al., 2012; Herzer & Morrissey, 2013; Mitra & Hossain, 2013; Adeyemi et al., 2014; Dreher & Langlotz, 2017). Similarly, study by Mallik (2008) found the significant negative effect of foreign aid on economic growth in sub-Saharan countries. He argued that for most sub-Saharan countries the more foreign aid they have received, the more aid dependent they have become.

Several studies have been investigated the impact of foreign aid on economic growth in Ethiopia, but they came up with mixed results. For example, studies by Tadesse (2011), Duresa (2022) and Girma and Tilahun (2022) found the positive relationship between foreign aid and the long-run economic growth, while other studies (e.g., Siraj, 2012; Haile, 2015; Kidanemariam, 2013; Gebru, 2015, and Abera, 2017) found the negative relationships between foreign aid and the long-run economic growth in Ethiopia. These mixed results lead to raise question of why impact of aid on economic growth in Ethiopia continues to be paradoxical in its findings. Moreover, Haile (2015) argued that despite notable donor intervention in the country’s economic activities, the actual role of foreign aid has no significant impact on Ethiopian economic growth. This debate seems to be mainly driven by the results from cross-country regression analyses, while there have been few studies that adopt specific-country approach to investigate the impact of aid on economic growth. Because aid effectiveness is diverse across countries. Although cross-country empirical analyses have progressively developed and enormously contributed to understanding of aid-growth link, there is clear need for country case studies to capture country-specific heterogeneous features. Hence, this study makes a contribution to the less researched country-level literature on the impact of aid on economic growth. This paper aims to analyze the impact of foreign aid on economic growth in Ethiopia using time series data over the period 1974–2017. The significance of this study rests on informing public mandate towards foreign aid impact on economic growth in Ethiopia and gives glimpse of ideas on debates surrounding the mixed results from empirical literature on the contribution of foreign aid towards economic growth in Ethiopia. As commonly known, Ethiopia has been one of the major recipients of international aid; therefore, the expected outcome from this study could help improving policy design, institutional setup, implementation, monitoring and evaluation of foreign aid in Ethiopia.

Theories of Economic Growth

The Neo-classical Theory of Growth

The basic framework of neo-classical growth models was first developed by Solow (1956) and Swan (1956), which states that, at any point in time, the total output of the economy depends on the quality and quantity of physical capital employed, the quantity of labor employed, and the average level of skills of the labor force. However, once the economy reaches the full equilibrium level, additional growth in the stock of capital per worker will only take place if productivity increases, either through enhanced capital stock or through improvements in the quality of the labor force.

The basic assumptions of the Solow model include constant returns to scale, diminishing marginal productivity of capital, exogenously determined technical progress, and substitutability between capital and labor. And his basic question was “what are the main determinants of economic growth in the long term?” Based on his growth model, high investment rate (saving rate), high level of technology, skilled human capital, low level of population growth rate, and low rate of capital depreciation are the most determinants of economic growth in long run. According to Solow (1956), simple mathematical model, economic growth can be measured as:

When we divide both sides of [1] by Yt, it becomes that

The above equation decomposes GDP growth into portions that can be attributed to growth in the capital stock, the labor force, and the technology level. Then,

Using the same methodology for labor and technology, reduced form of Eq. (2)in growth form is as follows.

Or

Since Solow’s growth model assumption was constant return to scale and perfect competitive market, the summation of the share of capital and labor is a unity. So if the share of capital is βk, then the share of labor is 1 - βk = βL and the above equation can be rewritten as

where

- gy:

-

= growth rate of real GDP

- gk:

-

= growth rate of physical capital

- gL:

-

= growth rate of human capital

- gA:

-

= growth rate of technology and

βk, βL, and βA are the marginal elasticity of capital, labor force, and technology respectively. So if we have observations on the growth rate of output, the labor force, and the capital stock, we can have an estimate on the growth rate of total factor productivity. Equation (4) defines as the “Solow residual” in its long-run growth model.

According the neo-classical theory of growth, the model makes three important forecasts. First, increasing capital relative to labor creates economic growth, since people can be more productive given more capital. Second, poor countries with less capital per person grow faster because each investment in capital produces a higher return than rich countries with sufficient capital. Third, because of diminishing returns to capital, economies eventually reach a point where any increase in capital no longer creates economic growth and which is called a steady state.

Methodology

Model Specification

As we discussed in the “Theories of Economic Growth” section, the model to examine the relationships between foreign aid and GDP growth in the paper is derived from neo-classical growth model:

where

- Y:

-

denotes a proxy for economic growth

- Gk:

-

denotes physical capital

- Lf:

-

denotes human capital

Following the neo-classical growth model, we specify the economic growth function for Ethiopia as follows: Real GDP is a function of physical capital, foreign aid, external debt, human capital, exports of goods and service, and general inflation rate. The mathematical relationship between real GDP and its components given as:

- Y:

-

denotes a proxy for change in real GDP growth

- GK:

-

denotes gross capital formation

- AID:

-

denotes foreign aid

- EXD:

-

denotes external debt

- EXHE:

-

denotes expenditure for human capital formation/health and education

- EXT:

-

denotes export of total goods and services

- INF:

-

denotes general inflation rate

According to Benoit (2011), the next step is expressing the variables into logarithmical form in a regression model. Thus, the growth function of Eq. (7) written as:

- lnRGD Pt:

-

represents natural logarithm of real GDP;

- lnGKt:

-

represent natural logarithm for physical capital (formally gross investment);

- lnAIDt:

-

represents natural logarithm of foreign aid;

- lnEXDt:

-

represents natural logarithm of external debt;

- lnEXHEt:

-

represents natural logarithm for human capital formation proxies by expenditure to health and education;

- lnEXTt:

-

stands for natural logarithm of total export;

- INFt:

-

stands for general inflation rate;

- ln:

-

denotes natural logarithm

- εt:

-

denotes error term

β0, β1, β2, β3, β4, β5, and β6 are coefficients that measure long-run and short-run relationship of independent variables with real RGDP in this specified model.

An ARDL representation of Eq. (6) will be:

where ∆ denotes for first difference operation, Yt is for a vector of dependent variables, Xt is a vector of p determinants of Yt regressors, Ut is the residual term which is assumed to be white noise.

Basically, the ARDL approach to co-integration (Pesaran et al. 2001) involves estimating of the error correction model (ECM) version of ARDL model for the determinants of economic growth:

where RGDP is the real GDP in Million Birr at a time t, GK is capital formation (proxied by gross investment), AID is foreign Aid, EXD is total external debt, EXHE is expenditure of health and education (both recurrent and capital), which is proxy of human capital, EXT is total export of goods and service, and INF is the general inflation rate, u is the residual term, which is assumed to be white noise, p is the optimal lag length, and ln is natural logarithm. Except inflation, all the variables entered in the model is measured in millions of Birr.

The bounds test is mainly based on the joint Wald test or F-test which its asymptotic distribution is non-standard under the null hypothesis of no co-integration. The hypotheses to determine a long-run relationship between the variables in Eq. (10) are:

Null: - H0: Ө0 = Ө1 = Ө2 = Ө3 = Ө4 = Ө5 = Ө6 =0 (no long-run relationship)

Alternative: - H1: Ө0 ≠ Ө1 ≠ Ө2 ≠ Ө3 ≠ Ө4 ≠ Ө5 ≠ Ө6 ≠ 0 (there is a long-run relationship)

If there is an evidence of long-run relationship (co-integration) of the variables, the following long-run ARDL (P1, P2, P3, P4, P5, P6, P7) models will be estimated.

Data Sources

The necessary data for the paper is collected from various sources such as Ethiopian Economic Association (EEA) database CD Rom, Ministry of Finance and Economic Development (MOFED), National Bank of Ethiopia (NBE), Ethiopian Central Statistical Authority (CSA), National Metrology Agency, International Monetary Fund (IMF) database, Penn World Table, and World Bank online databases. The method employed in the study is based on recent advancements in the theoretical and empirical aid–growth relationships. As the data used is time series (annual time series data over the period 1974 to 2017), various tests such as testing for stationary (unit root test) and co-integration test are performed. The rank of co-integration is determined by using ARDL. The model is estimated by using ordinary least Square (OLS).

Results and Discussion

Econometric Model Testing

The Unit Root Test Analysis

Before conducting ARDL co-integration test, first it is recommended to conduct test for the stationarity status of the given time series data to determine their order of integration. A unit root test is carried out using Augmented Dickey-Fuller (ADF) test for each variable in the model. The unit root test could convenience us whether or not the ARDL model should be used and to avoid spurious results, all the variables used in the regression model should not be stationary at an integrated of order two (I(2), because the computed F-statistics provided by Pesaran et al. (2001) are valid only when the variables are I(0) or I(1). Therefore, Augmented Dickey-Fuller (ADF) test was conduct and its result shown in Table 1.

The unit root test results clearly show all explanatory variables which are non-stationary [i.e., I(0)] at levels and stationary [i.e., I(1)] at their first difference and but not on I(2). This gives a clue to meet the basic requirements in applying ARDL model due to fact that the order of integration of the time series is not I(2). That is, the variables included in this model are integrated of order zeros [i.e., I(0)] and order one [i.e., I(1)], but not any order two [i.e., I(2)] which is not desirable in this model.

Diagnostic Test and Model Stability

After checking the stationarity of the variables, standard property of the model is tested through diagnostic and model stability test. Model stability and diagnostic checking to detect serial correlation (Brush and God fray LM test), functional form (Ramsey’s RESET), conflict to normality (Jaque-Bera test), and heteroscedasticity (Breusch-Pagan-Godfrey test) were performed. In order to reject or accept the null hypothesis, we can decide by looking the p-values associated with the test statistics. That is, the null hypothesis is rejected when the p-value are smaller than the standard significance level (i.e., 5%). The p-value associated with both LM version and F version of the diagnostic test statistics is above the standard critical value (its above 5%). Therefore, it is possible to conclude that the ARDL co-integration model of the study passes all the diagnostic tests (which include serial correlation, functional form, normality, and heteroscedasticity) (Table 2). Therefore, based on the result of the test, both LM and F versions of the statistic indicate that there is no serial correlation problem; the model is correctly specified; the errors are normally distributed and there is no heteroskedasticity problem in the model.

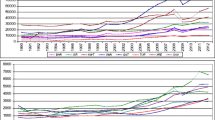

In addition to the above diagnostic tests, the overall stability of short-run and long-run coefficients is also tested by cumulative sum of recursive residuals (CUSUM) and the cumulative sum of squares of recursive residuals (CUSUMSQ) tests (Figs. 1 and 2), which are recommended by Pesaran and Shin (1999).

Plot of cumulative sum of recursive residuals

Plot of cumulative sum of squares of recursive residuals

As shown in the above figures, the plot of CUSUM stays within the critical 5% bound for all equations (Fig. 1), and CUSUMSQ statistics does not exceed the critical boundaries (Fig. 2), that confirms the long-run relationships between the economic growth and the explanatory variables; thus, we can be able to conclude that the parameters of the model do not suffer from any structural instability over the study period. Thus, the model appears to be stable in estimating long-run and short-run relationship between variables. In addition to the model stability, 99.8% of the model has been explained by the regressors; hence, the results of the estimated model are reliable and efficient.

Long-Run ARDL Bounds Tests for Co-integration

The bounds test approach of co-integration is estimating the ARDL model specified in Eq. (4) using the appropriate lag-length selection criterion. It is run to check the joint significant of the coefficients in the specified conditional ARDL model.

The Wald test is conducted by imposing restrictions on the estimated long-run coefficients of all lagged level variables (real GDP, gross capital formation, foreign aid, external debt, expenditure for education and health, total export, and general inflation) in Eq. (5) The computed F-statistic value is compared with the lower and upper bound critical values provided by Pesaran et al. (2001) and Narayan (2004). It should exceed the cross-validation (CV) to establish the long-run relationship of the series. As it is depicted below in the table, with an intercept and trend, the calculated F-statistics is 9.388 Table 3.

The computed F-statistic value is compared with the lower bound and upper bound critical values tabulated in Table 4 CI (III) case IV of Pesaran et al. (2001) and Narayan (2004).

As it is depicted in the above table, the value of significance level at 1%, 5%, and 10% are tabulated, based on Pesaran et al. (2001) and Narayan (2004) lower and upper bound critical values. The critical values reported for Pesaran et al. (2001) are the case with unrestricted intercept and no trend (case III). However, in this study, we have used Narayan (2004) which is developed based on 30 to 80 observations as we discussed earlier in the third part of this study.

Accordingly, the value of the calculated F-statistics 9.388 is higher than Pesaran et al. (2001) and Narayan (2004) lower and upper bound critical values. This implies that the null hypothesis of no long-run relationship is rejected, rather accept the alternative hypothesis (there is long-run relationship) based on the Pesaran et al. (2001) and Narayan (2004) upper bound critical values at 1% level of significance. Therefore, there is an evidence for a long-run relationship among economic growth and variables in the model.

Long-Run ARDL Model Estimation

The bound test for co-integration test, model stability, and diagnostic test results indicates us the existence of a long-run relationship between real GDP and independent variables. Once we are checking long-run co-integration among the variables, and then it is good to estimate the ARDL model to find out the long-run coefficients. The estimated coefficients are reported in Table 5. In doing so, the Akaike information criterion (AIC) is chosen with two maximum lag order and found the ARDL (1, 0, 0, 2, 2, 0, 0) equation. The F-statistic indicates that the model is statistically significant as a whole and the R-squared value of the estimated model reveals that 99.8% of the variation in real GDP is substantially explained by the variables included in the model. Because of the Durbin Watson statistic value is two and greater than the upper critical value of DW test, there is no spurious relationship between the variables (there is no serial autocorrelation).

Table 5 presents the summary of estimated results of the long-run growth model in the regression with respect to their significant levels. It shows that, the estimated coefficients of the variables entered in the regression; gross capital formation, human capital formation, and inflation have positive signs and statistically significant at 1% significant level. Meanwhile, external debt and exports of goods and service have negative sign and statistically significant at 1% significant level.

Foreign aid is the central variable in this study, as shown in the table above; it has negative significant impact on Ethiopian economic growth. The negative coefficient of the results of foreign aid is consistent with the studies by Siraj (2012), Haile (2015), Kidanemariam (2013), Gebru (2015), and Abera (2017) which found the negative impacts of foreign aid on long-run economic growth in Ethiopia. In contrary, Tadesse (2011), Duresa (2022), and Girma and Tilahun (2022) found the positive impacts of foreign aid on long-run economic growth in Ethiopia.

There might be two possible reasons behind the negative impact result of foreign aid on long-run economic growth in Ethiopia.

-

I)

In the first case, this may be that the inflow of foreign aid received in the form of grants and loan spent to use for daily expense on consumption of goods and services and help the society in reducing poverty rather than building a fixed investment, which is used to accelerating economic growth. If so, it does not have any impact on Ethiopian economic growth due to no value added to macroeconomic growth.

-

II)

The second reason behind the negative impact result of foreign aid may be associated with the data inconsistency, which we took from two organizations (NBE and MoFED annual time series data ranging from 1974 to 2017).

The other variable is the debt burden, which is measured by total external debt. It has a significant negative relationship with real GDP at 1% significant level. The estimated coefficient of the long-run relationship shows that a 1% increase in the external debt holding other things constant leads to approximately 0.0895% decrease in real GDP in the long-run during the study period. This result indicates that the existence of debt overhang problem in the country during the study periods.

The negative impact of external debt on economic growth might be linked with the low domestic saving rate in the country. As a result, to finance the government investment especially for the mega project, the Ethiopian government borrows from different external financial institutions and governments; this implies the government with heavy debt burden.

The long-run coefficient of human capital formation/expenditures for education and health revealed that has an expected long-run positive impact on the Ethiopian economy growth and statistically significant at 1% significant level. A 1% increase in human capital formation which is proxied by expenditures to education and health in the long run, holding other things constant, has resulted in 0.3977% change in real GDP during the study period. This result is similar with the results found by Demissie (2011) and Gebru (2015) in Ethiopia. The result of this study revealed that total exports of goods and service has a significant negative impact on Ethiopian economic growth. This negative coefficient might be associated with more than 68% of export level in the country that comes from agricultural primary product, which suffered from international price shock.

General inflation rate in Table 5 shows the unexpected positive impact on Ethiopian economic growth. However, it is not statistically significant at 1% significant level. From the results, we can understand that inflation does not harm the economic growth significantly during the study period. Finally, the long-run estimated model presented approximately as follow with figures in the parenthesis indicates calculated t-value.

Short-Run Error Correction Estimates

The short-run dynamic coefficient estimation was obtained from estimation of the error correction model (ECM). The error correction term (ECM) indicates the speed of adjustment to restore equilibrium in the dynamic model. It is a one lagged period residual obtained from the estimated dynamic long-run model. The coefficient of the error correction term indicates how quickly variables converge to equilibrium and it should have a negative sign and statistically significant (i.e., p-value should be less than 0.05). The coefficient of determination (R-squared) explains that about 72.5% of variation in GDP is attributed to variations in the explanatory variables in the short-run model. In addition, the DW statistic does not suggest autocorrelation and the F-statistic is quite robust.

As presented in the error correction model Table 6, the error correction term is strongly significant and its coefficient (ECM-1) is −.0.8465, which implies that the deviation from the long term in economic growth is corrected by 85% in the next year. The coefficient of the lagged error correction coefficient, estimated at −0.8465, is highly significant, has the correct negative sign, and implies a very high speed of adjustment to equilibrium. Gebru (2015) and Girma and Tilahun (2022) stated that a highly significant error correction term was a further evidence of the existence of a stable long-run relationship. Moreover, the coefficient of the error term (ECM-1) implies that the deviation from long-run equilibrium level of real GDP in the current period is corrected by 84.65% in the next period to bring back equilibrium when there is a shock to a steady-state relationship among the variables.

Most of the results are similar in both long run and short run. Capital formation/gross investment has a significant positive impact on economic growth with expected coefficient sign in the short run at 1% significance level in the short term. This shows that holding other things remain constant a 1% increase in capital formation will result approximately in 21% increase in real GDP in the short run during the study period.

Foreign aid is similar to the long-run model that has significant negative impact on Ethiopian economic growth with unexpected coefficient sign and statistically significant at 1% significance level, in the short term. As a result, holding other things constant, a 1% increase in foreign aid will result in approximately 10% decrease in real GDP in the short run.

The estimated external debt variable in the short run is found similar to the long-run effect, to have an expected negative relationship with real GDP and statistically significant at 5% significance level. As a result holding other things constant, a 1% increase in external debt will result in approximately a 1% decline in the real GDP in the short run. However, the 1-year lag result value indicates unexpected positive impact on real GDP, but it is not significant. The short-run external debt effect indicates that, in Ethiopia under the study periods, it is permanent as well as transitory and overhang occurs both in short and long run. This result is consistent with the results of long-run model and the study by Wessene (2014) and Gebru (2015) in Ethiopia. According to Wessene (2014) and Gebru (2015), the reason behind the negative impact on economic growth in the short run might be the improper management of external debt which might also be the case in this study.

Human capital formation/expenditures to health and education showed similar result with the long run, have significant positive impact on Ethiopian economic growth and statistically significant at 1% significance level, in the short term. As a result, holding other things constant, a 1% increase in human capital expenditure will result in approximately 29% increase in real GDP in the short run.

Total exports of goods and service has still unexpected negative impact on Ethiopian economic growth both in the long-run and short-run model. However, unlike the long run in the short term, it is not statistically significant at 5% significance level. This indicates that there is a negative relationship between export and Ethiopian economic growth, both in the long run and short run during the study period.

The general inflation rate has unexpected positive impact on Ethiopian economic growth and statistically significant at 1% significance level, unlike positive insignificant impact in the long run. We can conclude from this result, whether in the long run or in the short run, general inflation rate does not have significant (both negative and positive) impact on the Ethiopian economic growth under the study period.

Conclusion

Similar to other developing countries, physical domestic capital accumulation has a pivotal role to lifting up economic growth in Ethiopia. Due to domestic resources gap, the country obliged to look for external source of capital in terms foreign aid to enhance economic growth. There are several empirical studies that are undertaken to analyze the nexus between foreign aid and economic growth in Ethiopia; but they came up with mixed results. Some of the studies concluded that foreign aid has a positive and significant effect on economic growth, while the others showed that foreign aid has a negative impact on economic growth. This enables to raise question of why impact of aid on economic growth in Ethiopia continues to come up with paradoxical findings.

To investigate and examine the inconsistency in findings of foreign aid and economic growth in Ethiopia, this study aims at exploring this question by analyzing the impact of foreign aid on economic growth and the study also examined the contribution of foreign aid and the macroeconomic policy environment to economic growth in the country.

In order to examine the long-run and short-run economic growth model, the study applied an autoregressive distributed lag (ARDL) approach over the period 1974 to 2017. This is because ARDL gives reliable estimates even if in the presence of endogenous variables; it is possible to apply whether the regressors are I(0), I(1), or mixed; it is relatively more reliable and efficient for small size sample, which is the case for this study.

The empirical finding of the study revealed that foreign aid flow has a negative sign in the long run and short run. The study also found out that external debt and export of goods and services have unexpected significant impact on economic growth of Ethiopia with negative sign in the long run and short run. The result of external debt indicates the existence of debt overhang problem in the country during the study periods. On the other hand, export of goods and services in the long run and short run showed unexpected significant impact on economic growth of Ethiopia with negative sign. From this, one can understand that, holding other things constant, export of goods and services has no brought significant impact in real GDP growth and so far economic growth does not achieved by export of goods and services during the study period.

The long-run and short-run ECM model results showed that a 1% increase in foreign aid, holding other things constant, has resulted in 0.0587 and 0.101% decrease in real GDP during the study period respectively. Hence, it is concluded that there might be a possible reason behind the negative impact result of foreign aid on Ethiopian economic growth. This might be the inflow of foreign aid received in the form of grants and loan spent to use for daily expense on consumption of goods and services and help the society in reducing poverty rather than building a fixed investment, which is used to accelerating economic growth. .

Policy Recommendation

The country’s economic strategy should be more on structural transformation/industrialization than heavy dependence on agriculture. The dependence on agriculture in turn diverts the original purpose of foreign aid to individual consumptions when drought occurred. The government should work more effort to improve the negative impact of foreign aid on real GDP growth of Ethiopia. Thus, the study recommends that Ethiopia’s government has to ensure that foreign aid is linked to productive sectors and has to pursue policies device to reduce its over-reliance on foreign aid. The government should work to bridge gaps of the financial source by setting policies to increase domestic saving which is believed as a back bone of growth. This includes increase saving mobilization like selling of government bonds, expanding financial institutions, and strengthening existing saving tools, such as strengthening both private and government workers social security scheme and strengthening saving for housing program and for investment equipment scheme.

Data Availability

The datasets used and analyzed during the current study are available from the corresponding author on reasonable request.

Abbreviations

- ARDL:

-

autoregressive distributed lag

- GDP:

-

gross domestic product

- ADF:

-

augmented Dickey-Fuller (ADF) test

- PP:

-

Philip-Perron test

- NBE:

-

National Bank of Ethiopia

- MoFED:

-

Ministry of Finance and Economic Development

- CSA:

-

Central Statistical Agency

- IMF:

-

International Monetary Fund

- AIC:

-

Akaike information criterion

- CS:

-

cumulative sum

- CSS:

-

cumulative sum of squares

- CV:

-

cross-validation

References

Abera, A. (2017). The nexus of foreign capital inflows and economic growth in Ethiopia Diploma Thesis (p. 2017). Mendel University.

Adeyemi, A. O., Ojeaga, P., & Ogundipe, O. M. (2014). Is aid really dead? Evidence from Sub-Saharan Africa. International Journal of Humanities and Social Science, 4(10).

Arellano, C., Bulír, A., Lane, T., & Lipschitz, L. (2009). The dynamic implications of foreign aid and its variability. Journal of Development Economics, 88(1), 87–102.

Auerbach, A. J. (2009). Implementing the new fiscal policy activism. American Economic Review, 99(2), 543–549.

Benoit, K. (2011). Linear regression models with logarithmic transformations. Methodology Institute.

Bjerg, C., Bjørnskov, C., & Holm, A. (2011). Growth, debt burdens, and alleviating effects of foreign aid in the least developed countries. European Journal of Political Economy, 27(1), 143–153. https://doi.org/10.1016/j.ejpoleco.2010.08.003

Boateng, E., Agbola, W. F., & Mahmood, A. (2021). Foreign aid volatility and economic growth in Sub-Saharan Africa: Does institutional quality matter. Economic Modeling, 96, 111–127.

Civelli, A., Horowitz, A., & Teixeira, A. (2018). Foreign aid and growth: A Sp P-VAR analysis using sub-national satellite data for Uganda. Journal of Development Economics, 134, 50–67. https://doi.org/10.1016/j.jdeveco.2018.05.001

Clemens, M. A., Radelet, S., Bhavnani, R. R., & Bazzi, S. (2012). Counting chickens when they hatch: Timing and the effects of aid on growth. Economic Journal, 122(561), 590–617. https://doi.org/10.1111/j.1468-0297.2011.02482.x

Demissie, T. (2011). Sources of economic growth in Ethiopia: A time series empirical analysis. University of Oslo.

Dreher, A., & Langlotz, S. (2017). Aid and growth: New evidence using an excludable instrument. Center for Economic Studies & Ifo Institute Working Paper, 5515.

Duresa, K. M. (2022). Effect of foreign aid on economic growth and investment in Ethiopia. International Journal of Economics, Finance and Management Sciences, 10(1), 12–27. https://doi.org/10.11648/j.ijefm.20221001.12

Easterly, W., Levine, R., & Roodman, D. (2004). Aid, policies, and growth: Comment. American Economic Review, 94(3), 774–780. https://doi.org/10.1257/0002828041464560

Egert, B. (2015). Public debt, economic growth and nonlinear effects: Myth or reality? Journal of Macroeconomics, 43(1), 226–238. https://doi.org/10.1016/j.jmacro.2014.11.006

Frot, E., 2009. Aid and the financial crisis: Shall we expect development aid to fall?. Available at: SSRN 1402788

Frot, E., & Perrotta, M. (2012). Aid effectiveness: New instrument, new results. Mimeo Stockholm Institute of Transition Economics www.hhs.se/SITE/Sta ff/Documents/MPdraft_2012.pdf

Galiani, S., Knack, S., Xu, L. C., & Zou, B. (2017). The effect of aid on growth: Evidence from a Quasi- experiment. Journal of Economic Growth, 22(1), 1–33.

Gebru, T. (2015). The determinants of economic growth in Ethiopia: A time series analysis. A thesis submitted to the Department of Economics in Partial fulfillment of the requirements for the Degree of Master Science in Economics (Economic Policy Analysis) (p. 2015). Addis Ababa University.

Girma, T., & Tilahun, S. (2022). Predictability of foreign aid and economic growth in Ethiopia. Cogent Economics and Finance, 10(1), 2098606. https://doi.org/10.1080/23322039.2022.2098606

Haile, H. (2015). The impact of foreign aid on economic growth: Empirical evidence from Ethiopia, Using ARDL approach. Aksum University.

Heinrich, T., Kobayashi, Y., & Bryant, K. A. (2016). Public opinion and foreign aid cuts in economic crises. World Development, 77, 66–79. https://doi.org/10.1016/j.worlddev.2015.08.005

Herzer, D., & Morrissey, O. (2013). Foreign aid and domestic output in the long run. Review of World Economics, 149(4), 723–748. https://doi.org/10.1007/s10290-013-0169-y

Ilorah, R., & Ngwakwe, C. C. (2021). Foreign aid and economic development in sub-Saharan Africa: The mediating role of governance effectiveness. Managing Global Transitions, 19(4), 307–326.

Jena, N. R., & Sethi, N. (2020). Foreign aid and economic growth in sub-Saharan Africa. African Journal of Economic and Management Studies, 11(1), 147–168. https://doi.org/10.1108/AJEMS-08-2019-0305

Juselius, K., Møller, N. F., & Tarp, F. (2014). The long-run impact of foreign aid in 36 African countries: Insights from multivariate time series analysis. Oxford Bulletin of Economics and Statistics, 76(2), 154–184. https://doi.org/10.1111/obes.12012

Kidanemariam, G. (2013). The impact of human capital development on economic growth in Ethiopia: Evidence from ARDL approach to co-integration. A Peer-Reviewed Indexed International Journal of Humanities & Social Science, II(IV) April- 2014.

Liew, C., Masoud, R. M., & Said, S. M. (2012). The impact of foreign aid on economic growth of east African countries. Journal of Economics and Sustainable Development, 3(12), 129–138.

MacKinnon, G. J. (1996). Numerical Distribution Functions for Unit Root and Cointegration Tests. Journal of Applied Econometrics, 11(6), 601–618.

Mallik, G. (2008). Foreign aid and economic growth: A co-integration analysis of the six poorest African countries. Economic Analysis and Policy, 38(2), 251–260.

Mitra, R., & Hossain, S. (2013). Foreign aid and economic growth in the Philippines. Economics Bulletin, AccessEcon, 33(3), 1706–1714.

Narayan, K. (2004). Reformulating critical values for the bounds F-statistics approach to cointegration: An application to the tourism demand model for Fiji. Discussion Papers No 02. Monash University, Victoria.

OECD, 2019. OECD statistics. https://stats.oecd.org/Index.aspx?DataSetCode=TABLE3A

Perotti, R., 2005. Estimating the effects of fiscal policy in OECD countries’. CEPR Discussion Paper No. 4842.

Pesaran, M. H., & Shin, Y. (1999). Econometrics and Economic Theory in the 20th Century The Ragnar Frisch Centennial Symposium, An Autoregressive Distributed-Lag Modelling Approach to Cointegration Analysis, Cambridge University Press Cambridge, 371–413.

Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bound testing approach to the analysis of level relationships. Journal of Applied Econometrics, 16, 289–326.

Rajan, R. G., & Subramanian, A. (2011). Aid, Dutch disease, and manufacturing growth. Journal of Development Economics, 94(1), 106–118. https://doi.org/10.1016/j.jdeveco.2009.12.004

Sachs, J. D. (2005). The end of poverty: Economic possibilities for our time. The Penguin Press.

Siraj, T. (2012). Official development assistance (ODA), public spending and economic growth in Ethiopia. Journal of Economics and International Finance, 4(8), 173–191.

Solow, R. M. (1956). A contribution to the theory of economic growth. The Quarterly Journal of Economics, 70(1), 65–94 (Feb., 1956) The MIT Press.

Swan, W. T. (1956). Economic growth and capital accumulation. Economic Record, 32(2), 334–361. https://doi.org/10.1111/j.1475-4932.1956.tb00434.x

Tadesse, T. (2011). Foreign aid and economic growth in Ethiopia: A co integration analysis. The Economic Research Guardian, 1(2), 88–108.

Wessene, K. (2014). Does external debt cause economic growth? The case of Ethiopia.

Author information

Authors and Affiliations

Contributions

The first author visualized the concept of this paper, collected data, analyzed the data, and drafted the paper. The second author clearly designed this article and approved the final version of the manuscript.

Corresponding author

Ethics declarations

Conflict of Interest

The authors declare no competing interests.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Gebresilassie, B.A., Legesse, T. & Gebre, G.G. Impact of Foreign Aid on Economic Growth in Ethiopia. J Knowl Econ (2023). https://doi.org/10.1007/s13132-023-01303-y

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s13132-023-01303-y