Abstract

Previous studies on economic growth have separately examined the role of housing, banking, and credit market conditions, despite their interrelatedness. Therefore, this paper comprehensively investigates the relative importance of four indicators [house prices, residential investment, corporate credit spreads, and aggregate bank liquidity creation (LC)] to forecast U.S. real GDP growth. We do so after accounting for a comprehensive set of other predictors and aim to identify indicators that better forecast economic growth. Our in-and out-of-sample results show that house prices and corporate credit spreads predict real GDP growth better than residential investment and LC. Moreover, shocks to house prices and corporate credit spreads have a greater impact on real GDP growth and other macroeconomic indicators than shocks to LC and residential investment. Furthermore, house prices have the largest positive impact on inflation and the largest negative effect on unemployment. These results may have potential monetary policy implications.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Before the 2007-2009 crisis, macroeconomic research mainly focused on non-financial firm constraints.Footnote 1 However, the Great Recession shifted the focus towards balance sheet constraints faced by households and banks. This led to increased theoretical and empirical research on the financial crisis and its impact on the real economy.

In the empirical literature, investigations into housing, banking, and credit-supply conditions are often conducted in isolation to determine their individual contribution to the real economy. For instance, the credit-cycle literature (e.g, Gilchrist and Zakrajšek 2012) shows that corporate credit spreads, which act as a proxy for firm external finance premium, explain the business cycle fluctuations. Footnote 2 On the other hand, the housing literature (e.g., Miller et al. 2011) finds that house prices can potentially impact economic growth through the wealth effects of housing on the economy.Footnote 3 However, another strand of the housing literature (e.g., Leamer 2007, 2015) argues that residential investment, rather than house prices, determines the business cycle. In contrast, the banking literature (e.g., Berger and Bouwman 2009; Berger and Bouwman 2017) shows that bank economic output, as measured by bank liquidity creation (LC hereafter), determines the business cycle, where banks create more liquidity before crises.

Although housing, banking, and credit-supply conditions may each have their own impact on economic growth, the 2007-2009 housing/credit crisis highlighted the interconnectedness of these three conditions. This relationship persists even in non-crisis periods since firms and households borrowing and spending are linked to banking through their balance sheets. The literature (Mian et al. 2013; Mian and Sufi 2014; Gertler and Gilchrist 2018) finds support of this interconnectedness, especially during the 2007-2009 crisis. For instance, Gertler and Gilchrist (2018) examine the contribution of decline in house prices and banking distress to unemployment during the Great Recession period. They find that both the house price shocks and disruption of banking, as measured by corporate credit spreads shocks, contributed to decline in unemployment.

We build on the above literature by exploring economic growth forecast ability based on housing, banking, and credit-supply conditions. However, we go beyond the Great Recession period, and we assess the relative importance of house prices, residential investment, corporate credit spreads, and LC to forecast U.S. GDP growth. Our primary goal is to take different transmission mechanisms as given and then find their relative importance in forecasting economic growth. Additionally, we examine the impact of shocks to these indicators on inflation and industrial production, in addition to focusing on unemployment. This analysis provides a more comprehensive understanding of the interrelationships among banking, housing, and credit-supply constraints, and their effects on the broader economy.

Our primary findings using the 1984-2016 sample housing are as follows. First, our in-sample results show that both house prices and corporate credit spreads are the leading predictors of real GDP growth, while LC and residential investment are less informative. The results further indicate that house prices are a better predictor of personal consumption expenditures, whereas residential investment are better predictors of business fixed investment. On the other hand and as expected, corporate credit spreads are a stronger predictor of business fixed investment than they are of personal consumption expenditures, while LC contains limited information.

Second, the most important result of our out-of-sample analysis is that the combination of house prices and corporate credit spreads can predict real GDP growth better than other predictors (or their combinations). These results suggest that the combination of house prices and corporate credit spreads is a better predictor of real GDP growth because it captures both personal consumption expenditures and business fixed investment more accurately. Other predictors, such as stock market returns, lack robust in- or out-of-sample performance.

Third, while forecasting of economic growth is important, it is equally crucial to investigate the macroeconomic effects of shocks to housing, banking, and credit supply conditions, as it may have monetary policy implications. Our VAR results are in line with the forecasting results. We find that shocks to house prices and corporate credit spreads have the largest impact on real GDP growth. The VAR results also indicate that house prices have the largest impact on inflation, unemployment, and industrial production, underscoring the significance of housing in the economy. Corporate credit spreads have a notable impact on these macroeconomic indicators, with effects generally lower than those of house prices, but higher than LC and residential investment. Lastly, we find that monetary policy shocks have a greater impact on the housing variables than on bank liquidity creation, with residential investment being more affected than house prices.

Overall, the results indicate that the credit and asset prices channels are among the most significant channels of monetary policy transmissions. Our findings further suggest that the bank lending channel, which is a component of the credit channel, may have a lower impact on the economy. Furthermore, in terms of the asset channel, we observe that housing wealth, as measured by house prices, better forecasts economic growth, than financial wealth, as measured by stock market returns. Therefore, policymakers may monitor both house prices and corporate credit spreads, along with other indicators such as unemployment and inflation, to achieve the objectives of monetary policy, which are to promote price stability and maximum employment.

Our findings contribute to the literature by shedding light on the relative importance of different channels of monetary policy transmission. Additionally, we contribute to the housing literature (e.g., Leamer 2007, 2015; Ghent and Owyang 2010) that argues that residential investment determines the business cycle by showing that residential investment has limited predictive power for personal consumption expenditures when other preditors are considered. As a direct consequence, although residential investment is most impacted by monetary policy shocks, it provides limited leading information about economic growth. In contrast, we find support for the literature (e.g., Campbell and Cocco 2007) that argues house prices are highly correlated with consumption, and hence better forecast economic growth.

Finally, we contribute to the banking literature on the role of banks for economic development (e.g., e.g., Bencivenga and Smith 1991, Levine and Zarvos 1998, Kashyap, et al. 2002). However, unlike the existing literature (Berger and Sedunov 2017; Chatterjee 2018), our findings indicate that LC does not provide leading information about future economic growth after accounting for other indicators. Thus, our results are consistent with the findings in the literature (e.g., Bernake and Lown 1991; Kashyap and Stein 1994) on the relationship between bank lending and economic activites.

The paper is organized as follows: Section 2 describes the data sources and characteristics; Section 3 presents in- and out-of-sample real GDP growth prediction results; Section 4 investigates macroeconomic consequences and policy implications, while Section 5 concludes.

2 Data Sources and Characteristics

We analyze a sample from the first quarter of 1984 to the second quarter of 2016. We select the sample period based on the availability of LC data, which is available from 1984 onwards. We obtain LC data for all U.S. commercial banks from Christa Bouwman’s website.Footnote 4 We use ΔLC, ΔLCON, and ΔLCOFF, the log differences of bank aggregate, on-, and off-balance sheet liquidity creation, respectively. We use ΔLC in most of our analysis since the literature (e.g., Berger and Sedunov 2017) shows that it explains economic growth. However, we use ΔLCON and ΔLCOFF to ensure robustness.

We use two corporate bond credit spreads measures proposed in Gilchrist and Zakrajšek (2012) that are computed from unsecured nonfinancial corporate bonds’ trading data: excess bond premium (EBP hereafter) and GZ spreads (GZS hereafter).Footnote 5 EBP is computed from GZS by removing the corporate default risk and EBP is shown to be a superior predictor of economic outcomes. Thus, we primarily use EBP in most of our analysis. For robustness tests, we further use the traditional measure of corporate credit spreads (CS), which is computed as the difference between the yields of Moody’s corporate AAA and BAA rated bond indices.

We use two house price indices and residential investment (RINV hereafter) as housing indicators following the literature (e.g., Leamer 2015; Miller et al. 2011). The Real Residential Property Price index (RRPP hereafter) data are from the Bank of International Settlements (BIS) that includes all types of dwellings in the U.S. in both existing and new houses.Footnote 6 We obtain all-transaction house price index (HPI hereafter) from the U.S. Federal Housing Finance Agency; HPI is a weighted, repeat-sales index. We use the log differences of RRPP, HPI and RINV represented as ΔRRPP, ΔHPI and ΔRINV, respectively. To ensure robustness, we use ΔRRPP and ΔHPI interchangeably. To ensure further robustness, and to test the effect of the household balance-sheet effects, we investigate ΔMIR, the changes in mortgage debt service payment to disposable income ratio following the literature (e.g.Gertler and Gilchrist 2018).

2.1 Other Predictor Variables

For the asset channel of monetary policy transmission to function, asset prices should be reasonable predictors of economic growth. While we have included house prices, households’ portfolios also include financial assets in addition to houses. Thus, we use stock market excess returns (MKT) as another predictor, and this selection is also consistent with the economic growth literature (e.g., Levine and Zarvos 1998). We also use the changes in the Federal funds rate (ΔFED) as a proxy for monetary policy and this is common in the literature (e.g., Estrella and Hardouvelis 1991; Næs et al. 2011). Following the literature (e.g., Estrella and Mishkin 1998; Harvey 1988, 1989) we also use the Treasury term spread (TS) since TS is found to be an important predictor of economic growth and recessions. TS is computed as the difference in the yields on the 3-month Treasury-bill and the 10-year Treasury bond index as per Estrella and Hardouvelis (1991).

We further include stock market illiquidity (ILR) as per the literature (e.g., Amihud 2002). While there are other measures of stock market illiquidity, ILR is found to be among the best predictor of real GDP (e.g., Næs et al. 2011). The illiquidity ratio of a stock is computed as:\({ILR}_{i,t}=\frac{1}{D_{i,t}}\sum_{d=1}^{D_{i,t}}\mid {R}_{i,d,t}\mid /{VOL}_{i,d,t}\), where |Ri, d, t| and VOLi, d, t are absolute returns, the dollar volume of security i on date d, respectively; Di, t is the number of days over which ILR is computed. This measure is a proxy for stock illiquidity. Stocks must have share prices of more than $5 and less than $1000 and be traded for 20 days in a month to be included in the sample. An equally weighted quarterly average illiquidity of all stocks is stock market illiquidity and it is denoted as ILR.

We further collect macroeconomic data such as real GDP, personal consumption expenditure, unemployment, etc., from the U.S. Bureau of Economic Analysis and the Federal Reserve Bank’s ALFRED database. As for stock market data, we use the Center for Research in Security Prices (CRSP) common stocks data. For monthly data, we compute quarterly variables by averaging monthly data over a three-month period starting from January of each year. Our data consist of different vintages.

First, we conduct both ADF (Dickey and Fuller 1979) unit-root and KPPS (Kwiatkowski et al. 1992) stationarity tests, and transform variables as needed to attain stationarity. The transformed variables are indicated by the prefix ‘Δ’. For instance, real GDP growth is shown as ΔGDP. We show the data characteristics in Table 1.

Table 1 Panel A displays correlations between select variables. The correlation analysis shows that ΔRRPP, ΔRINV, and LC are positively correlated with ΔGDP, while EBP is negatively correlated with ΔGDP. Rising house prices, residential investment, and banks liquidity creation are associated with economic expansion, while increase in credits spreads signals a contraction of growth.

Table 1 Panels B and C present pairwise Granger causality test results for selected variablesFootnote 7, with an optimal lag length of one quarter is chosen in a vector autoregression (VAR) framework incorporating both SIC and AIC information criteria. The Granger causality results show that house prices, residential investment, corporate credit spreads, and LC Granger cause real GDP growth, while no reverse Granger causalities exist. The Granger causality results further show that house prices Granger cause residential investment, corporate credit spreads, and LC, while there is no reverse Granger casuility. Although Granger causality does not imply causation, these results demonstrate that house prices contain leading information, not only about real GDP growth, but also about the other predictors that we focus on. We next formally investigate the predictive relationship in a multivariate setup.

3 Predicting Real GDP, Consumption, and Investment

In this section, we conduct in- and pseudo-out-of-sample prediction of real GDP growth by house prices, residential investment, LC, and EBP. The forecasting literature (e.g., Inoue and Kilian 2004, among others) suggests that in-sample predictions must precede out-of-sample predictions. For the in-sample predictions, we use a predictive model as in Eq. (1) where ΔGDP (or other macroeconomic indicators) is the dependent variable, “V” is a vector of explanatory variables that include ΔRRPP (or ΔHPI), ΔRINV, ΔLC, EBP, and other control variables.

The corresponding results are presented in Table 2, where we do not show the results for some predictors since their coefficients are not statistically significant. Furthermore, the out-of-sample tests that we conduct next indeed show that these variables have limited predictive power for real GDP growth.

In table 2 panel A, Model 1 shows that ΔLC is positively and significantly related to ΔGDP. Model 2 shows that the predictability ΔLC for ΔGDP remains intact in the presence of ΔRRPP. We further find that ΔRRPP is also positively and significantly related to ΔGDP. The positive sign of the coefficient of ΔRRPP is also consistent with the housing literature (e.g., Miller et al. 2011) that higher house prices leads to higher economic growth. The results are also consistent with the banking literature (e.g., Berger and Sedunov 2017) that LC is positively related to economic growth.

In Model 3, we include an interaction term between ΔRRPP and ΔLC. We find that there is a positive interactive effect of house prices and LC on ΔGDP. However, since the coefficient of ΔLC of the corresponding model is not statistically significant, we cannot make any conclusive argument about the interaction term. The interactive effect is valid only if there are independent effects. Model 4 shows that when we replace ΔRRPP with ΔRINV, the coefficient of ΔLC is statistically insignificant, while ΔRINV predicts ΔGDP, which is consistent with the results in Leamer (2007, 2015). Overall, these results show that ΔLC may not be a good predictor of ΔGDP.

In Model 5, we include ΔRRPP, ΔRINV, ΔLC, and EBP -- the four variables of interest to predict ΔGDP. We further include MKT as another predictor in Model 5. The corresponding results show that the coefficients of ΔRRPP and EBP are statistically significant, while those for ΔRINV and ΔLC are not. The negative sign of the coefficient of EBP is consistent with the findings in Gilchrist and Zakrajšek (2012). Additionally, in line with previous literature (e.g., Levine and Zarvos 1998), we find that MKT predicts ΔGDP.

In Model 6, we include the interaction terms between ΔLC and ΔRRPP, ΔLC and ΔRINV, and ΔLC and EBP, respectively, to investigate whether the Model 5 results hold after accounting for these interaction terms. Looking at the Model 6 results, we find that ΔRRPP and EBP are the only two robust predictors of ΔGDP. The results further underscore the importance of housing wealth, as captured in ΔRRPP, which is more important than financial wealth, as captured in MKT, in predicting economic growth.

Model 7 omits ΔLC and its interaction terms, but include ΔRRPP and ΔRINV, EBP and ΔRINV, and EBP and ΔRRPP interaction terms. We further include ΔFED and TS as predictors. The results reveals that ΔRRPP and EBP are still robust predictors of ΔGDP. This model has the highest adjusted R-Squared value of 0.41 among all the presented models in this table.

Models 8 and 9 show that replacing ΔRRPP with ΔHPI, the alternative house prices indicator, or replacing EBP with CS, the traditional measure of corporate credit spreads, do not change our main conclusion. Overall, our in-sample results indicate that house prices and corporate credit spreads are robust predictors of ΔGDP, while LC and residential investment may not be as robust. Furthermore, TS, ΔFED, and MKT contain limited information about ΔGDP, which aligns with the findings in Stock and Watson (2003) that asset prices may not be stable predictors of macroeconomic outcomes.

Next, we investigate whether ΔRRPP, ΔRINV, EBP, and ΔLC predict two important components of GDP: personal consumption expenditures growth (ΔCONS) and business fixed investment growth (ΔBINV). Table 2 Panel B indicates that housing variables and corporate credit spreads predict ΔCONS and ΔBINV, while LC may not provide leading information. Notably, we find that ΔRRPP contain leading information about ΔCONS, supporting existing literature that shows that the impact of housing on economic growth is through consumption (e.g., e.g., Lettau and Ludvigson, 2004). Conversely, the results suggest that ΔRINV contain leading information about ΔBINV, consistent with the literature that housing may affect economic growth through residential investment (e.g., Leamer 2007, 2015). However, as consumption is the most important component of GDP, ΔRRPP rather than ΔRINV better predicts ΔGDP as shown in Table 2 Panel A. Table 2 Panel B results further indicate that EBP predicts both ΔBINV and ΔCONS, underscoring the significance of credit constraints in the economy. These results are also consistent with the literature (e.g., Gilchrist and Zakrajšek 2012). However, upon examining the coefficients of EBP, we observe that EBP is a better predictor of ΔBINV than it is of ΔCONS. Overall, the in-sample results indicate that house prices and corporate credit spreads are better predictor of economic growth. We next, investigate whether the in-sample results hold out-of-sample.

3.1 Out-of-sample Forecasts

In this section, we perform pseudo-out-of-sample forecasts of ΔGDP. In addtion to the predictors used in the in-sample investigation, we use the following additional variables: ΔLCON and ΔLCOFF, bank on- and off-balance sheet liquidity creation variables, respectively, and ΔILR, stock market illiquidity. We briefly describe the methodology and present the out-of-sample results.

We adopt a τ-step-ahead out-of-sample rolling window forecast methodology, setting τ =1, 2, 3, and 4 quarters. For model estimation, we consider the first quarter of 1984 through the fourth quarter of 2004. Next, we forecast for the dependent variable from the first quarter of 2005 through the second quarter of 2016. Our baseline model is an AR(1) model, where one quarter lag of ΔGDP is the predictor of ΔGDP. We then augment the AR(1) model with additional predictors to evaluate thier forecast performance. We measure the performance of the test models relative to the baseline model using out-of-sample root mean squared error (RMSE) ratios. However, since RMSE ratios may be biased, we also evaluate the forecast performance based on the test-statistics, as described below.

If the parsimonious model has the same predictor variables of a larger encompassing model, then the models are nested. In our case, the models we are interested in are nested.Footnote 8 For the nested-models, we evaluate model accuracy by the MPSE-adjusted-statistics proposed in Clark and West (2007), and we present the methodology briefly.Footnote 9 Suppose there are a candidate predictor variable 1 and a competing predictor variable 2. The forecaster is interested in τ-step-ahead forecasts of the dependent variable “y”. Let us denote the period “t” forecasts of yt + τ from the two models as \({\hat{y}}_{1t+\tau }\) and \({\hat{y}}_{2t+\tau }\), respectively. We test the null that both models have equal predictive accuracy. We define a variable \({\hat{f}}_{t+\tau }\) as per Eq. (2) and test for equal RMSE by regressing it on a constant. Then, we use the resulting t-statistics for a zero coefficient, and reject the null at 5% level if | MPSE-adjusted | > 1.65.

Table 3 presents the out-of-sample test results. We investigate a number of models that nest the AR(1) model. For brevity, we do not show other possible combinations because all of these models have higher RMSE ratios than what we show in Table 3, but these results are available on request. For parsimony and visual clarity, we further show the statistical significance of the model that has the lowest RMSE ratio relative to the competing models.

Looking from the left and top in Table 3 for a one-quarter ahead forecasts of ΔGDP, first we present the baseline AR(1) model. Next, we add one of the predictors to the baseline model, and then, we add two predictors, and so on.

By comparing the two-variable forecast models and the baseline model, we find that the model that contains AR(1) and ΔRRPP terms has the lowest RMSE ratio of 0.94. The next best two-variable model contains AR(1) and EBP terms, and it has an RMSE ratio of 0.96. If we augment the baseline AR(1) model with ΔRINV, ΔLC, ΔLCON, and ΔLCOFF, etc., we find that the corresponding RMSE ratios are higher than those for the other two augmented models, and often an AR(1) model does better in terms of model accuracy. Overall, we find that ΔRRPP and EBP as forecasting variables of ΔGDP perform better than others.

Looking next at the three-variable forecast models and the baseline model, we observe that an RMSE ratio of 0.92 is the lowest among all the models in Table 3, and this model contains three predictors: AR(1)+EBP+ΔRRPP. Based on the MPSE-adjusted-statistics, this model is more accurate than the competing three models: 1) AR(1); 2) AR(1)+EBP; 3) AR(1)+ΔRRPP. That is, EBP considerably improves the forecast accuracy of the parsimonious model that contain AR(1) and ΔRRPP. Looking next at the model with three predictors: AR(1)+EBP+ΔRINV, we find that the RMSE ratio of the corresponding model is 0.96, and this model is inferior to the parsimounius AR(1)+ΔRRPP model. We further find that the AR(1)+ΔRRPP+ΔRINV model is inferior to the model AR(1)+ΔRRPP+ΔRINV model. Therefore, among the housing variables, ΔRRPP seems to be a better predictor of ΔGDP than ΔRINV.

Finally, looking at the last two rows, we find that adding more indicators to the three factor AR(1)+EBP+ΔRRPP model does not improve the RMSE ratios of the corresponding larger models. For the two- to four-quarter-ahead forecasts, we find that the results are qualitatively similar to those for the one-quarter-ahead forecasts. Therefore, our out-of-sample results generally conform to the in-sample results. Importantly, out-of-sample results show that the combination of ΔRRPP and EBP can predict ΔGDP better than other predictors and their combinations. This result can be explained from the findings in Table 2 Panel B, where we show that ΔRRPP is a good predictor of personal consumption expenditures and EBP is a good predictor of business fixed investment. Therefore, a combination of ΔRRPP and EBP captures both personal consumption and business investment, and hence better predicts ΔGDP.

The takeways from the above in- and out-of-sample results are as follows. First, we find that the inclusion of both corporate credit spreads and house prices is needed to improve the forecast accuracy of the baseline AR(1) model. Second, we further find that the inclusion of LC does not improve the forecast accuracy once we have included those two indicators.

4 Macroeconomic and Monetary Policy Implications

While forecasting real GDP is important, policymakers may also be interested in understanding how important macroeconomic indicators, such as unemployment and inflation, respond to shocks from different leading indicators, as well as examining the response of economic indicators to monetary policy changes. Additionally, it is crucial to account for the inherent endogeneity that exists among housing, banking, credit conditions, and the macroeconomy. Therefore, an analysis that takes these factors into consideration is imperative.

We use a standard vector auto-regression (VAR) method, which is similar to the VAR specification used in Gilchrist and Zakrajšek (2012) to investigate the macroeconomic effects of EBP. However, in our study, we include ΔRRPP, ΔRINV, and ΔLC in the VAR model. To ensure robustness, we also include ΔLCON and ΔLCOFF, the components of ΔLC.

We further include the following variables in the endogenous VAR model: real consumption (ΔCONS) and business fixed investment (ΔBINV) growths; quarterly percentage change in industrial production (ΔIP); unemployment (UNEMP) and inflation (Π) rates. The ordering of the endogenous VAR variables is important, and we follow the literature (Christiano et al. 1994, 1999, 2001), where the monetary policy variables is ordered first, followed by macro and micro variables.

Thus, the VAR specification includes the endogenous variables that are ordered as follows: ΔFED, ΔGDP, ΔCONS, ΔBINV, ΔIP, UNEMP, Π, ΔRRPP, ΔRINV, ΔLC, ΔLCON, ΔLCOFF, TS, EBP, MKT, and ΔILR. Based on information criteria such as Akike information criterion (AIC) we find that VAR(1) describes the dynamics. We evaluate the VAR(1) results by examining both the forecast error variance decomposition (FEVD) and the accumulated impulse response functions (IRFs) of the variables of interest over a period of ten quarters.

Table 4 presents the FEVD of ΔGDP, our primary variable of interest. The results are rounded to one decimal place for improved readability, and we do not show the FEVDs for other variables to conserve space. The first column of Table 4 displays the forecast horizon, while the second column, labeled "S.E.", presents the forecast error of ΔGDP at the specified forecast horizon. The remaining columns provide the percentage of the forecast variance attributable to each innovation, with each row summing up to 100%.

The FEVD of ΔGDP in Table 4 indicates that at a one-quarter forecast horizon, the forecast variance is solely attributable to ΔFED (3.9%) and ΔGDP (96.1%). However, after ten quarters, ΔGDP accounts for approximately 50% of the forecast variance, while ΔRRPP and EBP contribute around 11% and 8.4% respectively. Conversely, the contribution of other variables, such as ΔLC, ΔLCON, and ΔLCOFF, is lower compared to ΔRRPP and EBP after ten quarters. Alternative ordering of the VAR variables, with bank variables placed before the housing variables, does not qualitatively change the above results, and these results are available upon request. The above findings align with both the in-sample and out-of-sample results that house prices and corporate credit spreads are robust leading indicators of ΔGDP. Next, to complement the FEVD findings, we investigate the IRFs of ΔGDP to various shocks.

Figure 1 shows the IRFs of ΔGDP for one standard deviation positive Cholesky shocks to ΔRRPP, ΔRINV, ΔLC and EBP. For brevity and to save space, we do not present the IRFs of ΔGDP to other shocks since these responses are smaller than the ones we show. We find that the IRFs of ΔGDP to ΔRRPP, ΔRINV, ΔLC and EBP positive shocks are approximately 0.82, 0.20, -0.09, and -0.43 percentage points, respectively. In our sample, the mean quarterly ΔGDP is 0.68 percent, and hence those impacts are economically significant. The IRFs indicate that housing plays an important role in driving economic growth, whether we consider house prices or residential investment. Additionally, the IRF of ΔGDP for shocks to EBP aligns with the findings of Gilchrist and Zakrajšek (2012) that a contraction in EBP leads to economic growth. In contrast, the impact of ΔLC on ΔGDP is found to be limited and negative. We next investigate the robustness of our VAR results.

Accumulated Impulse Responses of GDP growth to Cholesky Shocks. This figure shows accumulated impulse responses of different variables to positive one standard deviation Cholesky shocks for the VAR(1) model with the following endogenous variables: ΔFED, ΔGDP, ΔCONS, ΔBINV, ΔIP, UNEMP, Π, ΔRRPP, ΔRINV, ΔLC, ΔLCON, ΔLCOFF, TS, EBP, MKT, and ΔILR. Response functions are plotted for 10 quarters in % points. Other response functions are not shown for parsimony. Quarterly sample 1984:Q1-2016:Q2

There is no established economic theory that prescribes a specific ordering for banking, housing, and credit spreads variables. To address this issue, we follow the VAR literature (e.g., Koop et al. 1996, Pesaran and Shin 1998) and investigate generalized shocks where the ordering of the endogenous VAR variables is unimportant. The VAR specification remains unchanged and includes the same endogenous variables as before: ΔFED, ΔGDP, ΔCONS, ΔBINV, ΔIP, UNEMP, Π, ΔRRPP, ΔRINV, ΔLC, ΔLCON, ΔLCOFF, TS, EBP, MKT, and ΔILR. We present the generalized accumulated IRFs over ten quarters in Fig. 2.

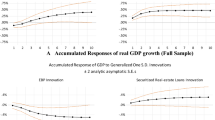

Robustness: Impulse Responses of GDP Growth to Generalized Shocks. This figure shows accumulated impulse responses of different variables to positive one standard deviation Generalized shocks for the VAR(1) model shown in Figure 1. Response functions are plotted for 10 quarters in % points. Quarterly sample 1984:Q1-2016:Q2

We observe that the IRFs of ΔGDP to ΔRRPP, ΔRINV, ΔLC and EBP positive shocks are approximately 0.64, 0.41, 0.13, and -0.51 percentage points, respectively. Overall, these generalized responses of ΔGDP for shocks to ΔRRPP, ΔRINV, and EBP are qualitatively similar to those under the Cholesky shocks. While small, the impact of ΔLC on ΔGDP is positive and is consistent with the literature (e.g., Berger and Sedunov 2017) that LC fosters economic growth. Since the generalized IRFs are consistent with the banking literature, we will use these response functions throughout the rest of the paper. We next investigate the IRFs of other macroeconomic variables, such as personal consumption expenditures growth, to different shocks.

In Fig. 3, we show the IRFs of each variable in one plot to save space. For visual clarity, we do not show the standard error (S.E.) bands of the IRFs. Figure 3A displays the accumulated IRFs of ΔCONS and ΔBINV for generalized one standard deviation positive shocks to EBP, ΔRRPP, ΔRINV, and ΔLC. We observe that shocks to ΔRRPP and EBP have impacts on ΔCONS of approximately 0.25 and -0.15 percentage points, respectively. In contrast, ΔRINV and ΔLC have lower impacts. Additionally, we find that positive shocks to ΔRINV, ΔRRPP, and EBP have impacts of approximately 0.10, 0.08, and -0.10 percentage points, respectively, on ΔBINV. Once again, we find ΔLC has a very limited impact on ΔBINV. Therefore, the VAR results are consistent with our in-sample findings for personal consumption expenditures and business fixed investment.

Accumulated Impulse Responses of Other Macroeconomic Indicators. This figure shows accumulated impulse responses of macroeconomic indicators to positive one standard deviation Generalized shocks for the VAR(1) model described in Figure 1. Response functions are plotted for 10 quarters in % points. Quarterly sample 1984:Q1-2016:Q2. A: Responses of Personal Consumption Expenditures and Business Fixed Investment. B: Responses of Industrial Production, Unemployment, and Inflation

In Figure 3B, we investigate the IRFs of industrial production (ΔIP), unemployment (UNEMP), and inflation (Π) for positive generalized shocks to ΔRINV, ΔRRPP, ΔLC, and EBP. We do not report the IRFs to other shocks since the impacts are lower. We find that shocks to ΔRRPP have the most significant impact on ΔIP, UNEMP, and Π, while EBP has a considerable impact on ΔIP and UNEMP. In contrast, shocks to ΔLC and ΔRINV have lower impacts. Overall, the VAR results supports in- and out-of-sample results that house prices and corporate credit spreads are important indicators of real GDP with significant impact on other macroeconomic indicators. Next, we investigate the effect of monetary policy on different indicators.

In Fig. 4, we show the IRFs of different indicators to ΔFED shocks, using FED as a proxy for monetary policy stance. Figure 4A shows the IRFs of unemployment and inflation to monetary policy shocks. For a comparison, we also show the impact of ΔRRPP and EBP shocks. We find that ΔRRPP have a greater impact than ΔFED on unemployment and inflation. These results suggest that monetary policy may work through the housing market to influence unemployment and inflation. To better understand the dynamics, we next investigate the impact of ΔFED shocks on ΔRINV, ΔRRPP, ΔLC, and EBP.

Accumulated Impulse Responses to Fed Funds Rate Shocks. This figure shows accumulated impulse responses of macroeconomic indicators to generalized positive one standard deviation shocks for the VAR(1) model described in Figure 1. Response functions are plotted for 10 quarters in % points. Quarterly sample 1984:Q1-2016:Q2. A: Responses of Inflation and Unemployment Rates to Federal Funds Rate shocks. B: Responses of Housing, Banking and Credit Spreads to Federal Funds Rate shocks

Figure 4B shows that higher monetary policy leads to lower house prices, decreased residential investment, and increased bank liquidity creation. We observe that the highest impact of ΔFED shocks is on ΔRINV, while the impact on EBP is not as pronounced. While the results for housing variables are as expected, the positive relationship between LC is consistent with the findings of Berger and Bouwman (2009) that banks create more liquidity when the Federal funds rates are higher. The result is also consistent with the argument in the literature (e.g., Thakor 2005, among others) that commercial banks act as a buffer for long-standing customers through off-balance sheet bank activities such as lines of credit, thereby mitigating the effect of monetary policy. Overall, we find some evidence that monetary policy seems to be working through the housing market to influence the economy. Therefore, policymakers may focus on monitoring fluctuations in the housing and credit markets since they are not only important indictors of economic growth but also of unemployment and inflation. This is particularly relevant as policymakers work towards achieving their primary goals of promoting price stability and maximum employment.

We conduct several robustness tests using alternative measures of house prices, corporate credit spreads, and bank liquidity creation. We further consider mortgage debt service payment to disposable income ratio as household credit constraints as in Gertler and Gilchrist (2018). To save space, these results are not reported, but available upon request. These robustness tests confirm our main conclusions that both the housing and credit market conditions are the most important indicators of economic growth and other macroeconomic indicators.

5 Summary and Conclusions

The existing literature on economic growth examines housing (e.g., Miller et al. 2011), banking (e.g., Bencivenga and Smith 1991), and credit market conditions (e.g., Gilchrist and Zakrajšek 2012) independently. However, since housing, banking, and credit constraints are interrelated, this paper aims to examine the real GDP growth forecasting ability of house prices, residential investment, corporate credit spreads (EBP), and bank aggregate liquidity creation (LC) concurrently.

Our findings indicate that house prices and EBP have a strong forecasting power for real GDP growth, while the forecasting power of LC and residential investment is not as robust. The results from our vector-autoregression analysis show that orthogonalized shocks to house prices and EBP have an economically significant impact on economic growth, while the impact of similar shocks to LC and residential investment is lower.

While the impact of LC on macroeconomic indicators, including real GDP growth, may be relatively small, this does not diminish the significance of banking. Real-estate loans are one of the crucial components of LC, but it also includes other important on- and off-balance items, such as commercial and industrial loans and letter of credits, which are essential for economic activities. Our results suggest that, once we consider credit constraints as captured in corporate credit spreads, the impact of LC, as measured, is somewhat lower on macroeconomic outcomes.

There are several ways our findings could be further explored. It would be worthwhile to investigate whether other bank on- or off-balance sheet variables, such as home equity line of credit (HELOC), have stronger ability to predict macroeconomic indicators than aggregate LC. Additionally, it would be interesting to examine whether our results hold in non-U.S. economies.

Data Avaliabilty

The authors declare that the data supporting the findings of this study are available from the corresponding author upon reasonable request. The reason is that the Center for Research in Security Prices (CRSP) common stocks data that is used in the study is subscription-based.

Notes

For instance, the financial accelerator/credit cycle theories (e.g. Bernanke and Gertler 1989; Kiyotaki and Moore 1997; Bernanke, et al. 1999) highlight how the quality of borrowers' balance sheets affects their access to external finance: a weak balance sheet results in less borrowing, spending, and economic activity, and vice versa.

An incomplete list of the literature that investigates whether fluctuations in credit supply, often measured by spreads between yields of different types of bonds, contain leading information about economic indicators are Estrella and Hardouvelis 1991; Estrella and Mishkin 1998; Mody and Taylor (2004); Gertler and Lown 1999; Gilchrist et al. (2009); Favara et al. (2016). etc.

A short list in the housing literature includes Bostic et al. 2009; Kartashova and Tomlin 2017; Bluedorn et al. (2016); Christensen et al. (2019); among others, investigate house prices. A large body of literature (e.g., Lettau and Ludvigson, 2004; Benjamin et al., 2004; Case et al., 2005; Kartashova and Tomlin, 2017; Adam et al. 2021) investigate housing wealth and the real economy. Literature further shows that a financial accelearor mechanism exists in the housing market (Bernanke 2007).

We thank Christa Bouwman for providing liquidity creation data.

We thank Simon Gilchrist for proving the data.

Source: BIS Residential Property Price database (http://www.bis.org/statistics/pp.htm)

Complete Granger causality results are available upon request.

Since the non-nested models have higher RMSE ratios relative to the nested models in Table 3, those are not reported for parsimony, but are available on request. Thus, we do not decribe the test-statistcs computation for non-nested models to save space.

Please see the detailed methodology described in Clark and West’s (2007) and we keep the original description of the test-statistics of their paper.

References

Amihud Y (2002) Illiquidity and stock returns: cross-section and time-series effects. J Financ Mark 5:31–56

Bencivenga VR, Smith BD (1991) Financial intermediation and endogenous growth. Rev Econ Stud 58:195–209

Benjamin JD, Chinloy P, Jud GD (2004) Real estate versus financial wealth in consumption. J Real Estate Financ Econ 29:341–354

Berger AN, Bouwman CHS (2009) Bank liquidity creation. Rev Financ Stud 22:3779–3837

Berger AN, Bouwman CHS (2017) Bank liquidity creation, monetary policy, and financial crises. J Financ Stab 30:139–155

Berger AN, Sedunov J (2017) Bank liquidity creation and real economic output. J Bank Financ 81:1–19

Bernanke B, Gertler M (1989) Agency Costs, Net Worth, and Business Fluctuations. Am Econ Rev 79(1):14–31

Bernanke BS, Lown CS (1991) The Credit Crunch. Brook Pap Econ Act 1991(2):205–239

Bernanke B, Gertler M, Gilchrist S (1999) The Financial Accelerator in a Quantitative Business Cycle Framework. In: Taylor JB, Woodford M (eds) Handbook of Macroeconomics, vol 1C. Elsevier Science, North-Holland, Amsterdam, pp 1341–1393

Bernanke, Ben 2007. The financial accelrator and credit channel. The credit channel of monetary policy in the Twenty-first Century Conferenece, Federal Reserve Bank Atlanta, Atlanta, Georgia. The Financial Accelerator and the Credit Channel - Federal Reserve Board; pages 1-15.

Bluedorn JC, Decressin J, Terrones ME (2016) Do asset price drops foreshadow recessions? Int J Forecast 32:518–526

Bostic R, Gabriel S, Painter G (2009) Housing wealth, financial wealth, and consumption: New evidence from micro data. Reg Sci Urban Econ 39:79–89

Campbell JY, Cocco JF (2007) How do house prices affect consumption? Evidence from micro data. J Monet Econ 54:591–621

Case, KE, JM Quigley, and RJ Shiller 2005. Comparing wealth effects: the stock market versus the housing market. Adv Macroecon 5

Chatterjee UK (2018) Bank liquidity creation and recessions. J Bank Financ 90:64–75

Christiano LJ, Eichenbaum M, Evans C (1994) The effects of monetary policy shocks: some evidence from the flow of funds. National Bureau of Economic Research

Christiano LJ, Eichenbaum M, Evans C (1999) Monetary policy shocks: What have we learned and to what end? Handb Macroecon 1:65–148

Christiano LJ, Eichenbaum M, Evans C (2001) Nominal rigidities and the dynamic effects of a shock to monetary policy. National Bureau of Economic Research

Christensen C, Eriksen JN, Møller SV (2019) Negative House Price Co-Movements and US Recessions. Reg Sci Urban Econ 77:284–228. https://doi.org/10.1016/j.regsciurbeco.2019.06.007

Clark T, West K (2007) Approximately normal tests for equal predictive accuracy in nested models. J Econ 138:291–311

Dickey DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74:427–431

Estrella A, Hardouvelis GA (1991) The term structure as a predictor of real economic activity. J Financ 46:555–576

Estrella A, Mishkin FS (1998) Predicting US recessions: Financial variables as leading indicators. Rev Econ Stat 80:45–61

Favara G, Gilchrist S, Lewis KF, Zakrajsek E (2016) Recession risk and the excess bond premium. Board of Governors of the Federal Reserve System (US)

Ghent AC, Owyang MT (2010) Is housing the business cycle? Evidence from US cities. J Urban Econ 67:336–351

Gertler M, Lown C (1999) The Information Content of the High Yield Bond Spread for the Business Cycle. Oxf Rev Econ Policy 15:132–150

Gertler M, Gilchrist S (2018) What happened: Financial factors in the Great Recession (No. w24746). J Econ Perspect 32:3–30

Gilchrist S, Yankov V, Zakrajsek E (2009) Credit market shocks and economic fluctuations: Evidence from corporate bond and stock markets. J Monet Econ 56(4):471–493

Gilchrist S, Zakrajšek E (2012) Credit spreads and business cycle fluctuations. Am Econ Rev 102:1692–1720

Harvey CR (1988) The real term structure and consumption growth. J Financ Econ 22:305–333

Harvey CR (1989) Forecasts of economic growth from the bond and stock markets. Financ Anal J 45:38–45

Inoue A, Kilian L (2004) Bagging time series models, https://papers.ssrn.com/sol3/papers.cfm?abstract_id=540262

Kartashova K, Tomlin B (2017) House prices, consumption and the role of non-Mortgage debt. J Bank Financ 83:121–134

Kashyap A, Stein J (1994) Monetary Policy and Bank Lending, p. 221-261 in, Monetary Policy, National Bureau of Economic Research, Inc. https://EconPapers.repec.org/RePEc:nbr:nberch:8334

Kashyap AK, Rajan R, Stein JC (2002) Banks as liquidity providers: An explanation for the coexistence of lending and deposit-taking. J Financ 57:33–73

Kiyotaki N, Moore J (1997) Credit Cycles. J Polit Econ 105(2):211–248

Koop G, Pesaran MH, Potter SM (1996) Impulse response analysis in nonlinear multivariate models. J Econ 74:119–147. https://doi.org/10.1016/0304-4076(95)01753-4

Kwiatkowski D, Phillips PCB, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? J Econ 54:159–178

Lettau M, Ludvigson SC (2004) Understanding trend and cycle in asset values: Reevaluating the wealth effect on consumption. Am Econ Rev 94:276–299

Levine, Zarvos (1998) Stock markets, banks and economic growth. Am Econ Rev 88(3):537–558

Mian A, Rao K, Sufi A (2013) Household Balance Sheets, Consumption and the Economic Slump, Quart J Econ

Mian A, Sufi A (2014) What Explains the 2007-2009 Drop in Employment. Econometrica 82:2197–2223

Miller N, Peng L, Sklarz M (2011) House prices and economic growth. J Real Estate Financ Econ 42:522–541

Mody A, Taylor MP (2004) Financial Predictors of Real Activity and the Financial Accelerator. Econ Lett 82:167–172

Næs R, Skjeltorp JA, Ødegaard BA (2011) Stock market liquidity and the business cycle. J Financ 66:139–176

Pesaran HH, Shin Y (1998) Generalized impulse response analysis in linear multivariate models. Econ Lett 58:17–29

Stock J, Watson M (2003) Forecasting Output and Inflation: The Role of Asset Prices. J Econ Lit 41:788–829. https://doi.org/10.1257/002205103322436197

Thakor AV (2005) Do loan commitments cause overlending? J Money, Credit, Bank 37:1067–1099

Funding

Open access funding provided by Università degli Studi di Trento within the CRUI-CARE Agreement.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of Interest

The authors declare that there is no conflict of interest.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Chatterjee, U. Forecasting Economic Growth: Evidence from housing, banking, and credit conditions. J Econ Finan 47, 936–958 (2023). https://doi.org/10.1007/s12197-023-09637-8

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12197-023-09637-8

Keywords

- House Prices

- Residential Investment

- Credit Supply

- Bank Liquidity Creation

- Economic Growth

- Inflation

- Monetary Policy