Abstract

We investigate the degree of internationalization of Chinese service multinational enterprises (MNEs) and their performance relative to global peers operating in the same industries, using the benchmarking method with the industry financial data. Our theoretical development is based upon Verbeke and Forootan (2012)’s framework, grounded in “new” internalization theory, arguing that an MNE’s financial performance is fundamentally determined by its firm-specific advantages (FSAs). Here FSAs include not only conventional strengths in R&D and brand names, but also the recombination capabilities, which is a higher-order FSA. We theorize that Chinese service MNEs develop FSAs, which are built upon home country-specific advantages (CSAs) and thus their FSAs are home country-bound in nature. They have not yet been able to develop advanced management capabilities through recombination with host CSAs. We empirically examine the largest 500 Chinese service firms. We find that only 23 Chinese service firms are true MNEs, whereas the majority of them are purely domestic firms. The financial performance of Chinese service MNEs is poor relative to global peers. They internationalize mainly through acquisitions of foreign firms, which help them increase their foreign sales, but they are not able to achieve superior performance in overseas operations. We discuss the strategic implications of our findings for managers, public policy makers, and academic research.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Research on the relationship between the degree of internationalization, also known as the degree of multinationality, and performance (M–P) has received significant attention from academic scholars in international management for the past 3 decades. However, despite the substantial body of empirical attempts, statistical findings continue providing inconclusive results. These include positive (Rugman et al. 2008), negative (Denis et al. 2002), and nonsignificant linear effects (Tallman and Li 1996), and wide variations in types of curvilinear, such as U-curve (Xiao et al. 2019), S-curve (Lu and Beamish 2004) and inverted S-curve relationships (Chiang and Yu 2005) (for a comprehensive review, see Nguyen 2017; Nguyen and Kim 2020). Until now, the dominant approaches to explain these divergent results have been either methodological refinement, such as the selection of different multinationality and performance measures, or the incorporation of different sets of moderators that capture firm-, country- and industry-specific characteristics (Geleilate et al. 2016; Kirca et al. 2011, 2016; Shin et al. 2017).

However, Hennart (2007) and Rugman and Verbeke (2008a) among others have criticized the present trend of continuously bringing complex statistical models to the literature. They suggest that the mixed empirical findings are due to the lack of theoretical support for the existence of a universal M–P relationship. Instead, these studies argue that from the perspective of internalization theory, the fundamental reasons for any linkage (might be) observed for the M–P relationship are an MNE’s firm-specific advantages (FSAs) (Hennart 2011; Nguyen 2017; Nguyen and Kim 2020; Rugman and Verbeke 2008a; Verbeke and Brugman 2009). Among them, Verbeke and Forootan (2012) propose one framework arguing that it is FSAs that determine an MNE’s scope of international expansion, as well as its domestic and international performance success. Without the possession of firm resources and capabilities, foreign expansion does not by itself deliver superior financial performance.

“Classic” internalization theory primarily focuses on MNEs’ knowledge-based FSAs typically in the form of asset-type FSAs, such as upstream patented technology and the downstream brand names, and transaction-type FSAs, such as managerial capabilities and coordination skills. An MNE must possess these internationally transferrable or non-location bound (NLB) FSAs over indigenous firms in the host country that outweigh the costs of doing business abroad (Buckley and Casson 1976; Rugman 1981). Meanwhile, “new” internalization theory, proposed by Rugman and Verbeke (1992, 2001, 2003) extend “classic” internalization theory by introducing the concept of location bound (LB) versus NLB FSAs and emphasizing the importance of the resource recombination capabilities that drive MNE success in host countries. An MNE needs to leverage host country-specific advantages (host CSAs) and develop LB FSAs, such as local reputation and network, for national responsiveness. Accordingly, an MNE makes dual use of CSAs from home and host countries, and appropriate recombination of existing NLB FSAs with newly created LB FSAs. Overall, an MNE’s financial performance depends critically on the strengths of its conventional FSAs (asset-type and transaction-type), and its resource recombination capabilities leading to the development of new FSAs to adapt to environmental changes (Verbeke and Brugman 2009; Verbeke and Forootan 2012).

In the light of critiques of the literature on M–P relationship, our purpose is not to test a direct M–P relationship (with or without moderators) statistically as this stream of literature suffers from severe theoretical flaws (Hennart 2011; Verbeke and Brugman 2009; Verbeke and Forootan 2012). Rather, by drawing upon Verbeke and Forootan (2012)’s framework, we analyse the degree of multinationality measured by foreign sales over total sales and the financial performance of Chinese service firms relative to global peers using the benchmarking method with industry financial data. Specifically, we investigate the 500 largest Chinese service firms and identify the number of these service firms to be true MNEs by Rugman (1981)’s definition. According to Rugman (1981), an MNE is a firm headquartered in one country with operations in other countries, having the ratio of foreign sales over total sales (F/Ssales) of minimum 10% and at least three foreign subsidiaries (the threshold of 10% in foreign sales ratio comes from the international financial reporting standard IFRS 8, Operating segment). Our study attempts to address the following research questions:

-

1.

To what extent are the largest 500 Chinese service firms to be true MNEs by a definition of Rugman (1981)?

-

2.

How is the financial performance of Chinese service MNEs relative to their global peers operating in the same industries?

We selected Chinese service sector because service firms’ internationalization is particularly relevant to the on-going debate—whether it is FSAs or multinationality to be the prerequisite for firm performance. This is because Chinese MNEs’ FSAs are built upon home country government support (a type of home CSAs) by providing favourable policies, investment information, and low-cost capital that enables them to embark on internationalization (Ramamurti and Hillemann 2018; Wei and Nguyen 2017). It is particularly true for Chinese service firms, given that Chinese service industries are dominated by state owned enterprises (SOEs) (Breslin 2012; OECD 2015). They use artificially cheap debt capital to finance internationalization which is in line with the “go global” policy and “the Road and Belt Initiative” of the Chinese government (Meyer 2018; Rugman et al. 2014, 2016). As such, Chinese service firms may start international expansion and increase the degree of multinatinality while possessing little or no conventional FSAs in technology and brand reputation. More importantly, we compare the financial performance of Chinese service firms to be true MNEs with more than 10% foreign sales to their global counterparts operating in the same industry. This allows us to investigate to what extent being multinatinality pioneers while lacking valuable firm resources enable firm to perform competitively in the context of Chinese service sector. Overall, these two research questions are inextricably linked to Verbeke and Forootan (2012)’s framework that focuses on the relationship among FSAs, multinatinality and financial performance.

To answer these questions, we elaborate on three important academic streams: the literature on the M–P relationship, on service sector internationalization and on Chinese service MNEs. Our study makes three specific contributions to the literature. First, we contribute to the M–P relationship literature by unbundling the unique sets of FSAs owned by Chinese service firms. On the one hand, most of the extant research on the M–P relationship focusing on advanced economy MNEs have assumed the resource allocation commitments to international expansion. This actually creates endogeneity problem that any effect of an MNE’s multinationality on performance might be explained by its internal strengths and weaknesses given that firms with strong FSAs are more likely to be internationally oriented (Verbeke and Brugman 2009).

On the other hand, Chinese service MNEs shed new lights on the current M–P relationship debate as the type of FSAs which they possess are location-bound and heavily relied on home CSAs of the government support for SOEs and large domestic market size (Rugman et al. 2014, 2016). Their FSAs are stand-alone FSAs through recombination with home CSAs, which are neither exploitable nor sustainable in foreign markets. We demonstrate that overall Chinese service firms have very limited degree of multinationality as the majority of them are purely domestic firms with no foreign sales. Even among a few true Chinese service MNEs, they perform poorly relative to global counterparts operating in the same industries, regardless of their degree of multinationality. As such, we confirm the theoretical validity of Verbeke and Forootan (2012)’s framework that denies any linkage between multinationality and performance without the existence of knowledge-based FSAs constituting a necessary condition for foreign investment.

Second, our study contributes to “new” internalization theory by contextualizing its application to Chinese service MNEs with a specific focus on FSAs as a key determinant of both internationalization and performance. We draw upon “new” internalization theory as it introduces and highlights the concept of LB FSA referring to the firm strengths deployable and exploitable in a limited geographic area—either home country or host county bound. On the one hand, Rugman et al. (2016) argue that these government-created advantages of Chinese firms, such as state ownership and large domestic market size, are a type of stand-alone FSAs (Verbeke 2013) and are home country-bound. On the other hand, service sector is different from manufacturing sector in numerous features, such as the intangibility of offerings, and the inseparability and perishability of the production and consumption process (Buckley et al. 1992; Meyer et al. 2015). Such features require the FSAs of service MNEs to be host market-specific and locally embedded, or host country-bound that represent disincentives to improve performance (Xiao et al. 2019). In this study, we find that it is often challenging for Chinese service firms to develop new LB FSAs in host countries, which are essential to achieve foreign sales and superior performance in overseas operations. As such, “new” internalization theory is particularly valid in explaining our findings.

Third, we contribute to the literature on the internationalization of Chinese service firms which has been scarcely researched. Bai et al. (2019) and Xiao et al. (2019) are among the first endeavours to study the determinants of Chinese service’s internationalization. However, they did not consider the overall degree of multinationality of Chinese service firms before calling them MNEs, which is a common mistake in the extant literature on Chinese firms’ internationalization (Rugman et al. 2016). One of our striking findings is that most of Chinese service firms including those well-known brands, such as Alibaba and Tencent, generate much of their sales in Mainland China. As such, they are not true MNEs by Rugman (1981)’s definition.

The rest of the paper is organized as follows: section two explicitly explains the “new” internalization theory as the theoretical rationale for this study, and then it introduces Verbeke and Forootan (2012)’s framework by critically reviewing the literature on M–P relationship. Based on “new” internalization theory, section three reviews service MNEs in general and China’s domestic setting in developing service firms, and identifies challenges for Chinese service firms’ international expansion. Section four explains the data source and data collection process for the largest 500 Chinese service firms used in this study. We present our main findings in section five. The final section discusses implications and proposes some suggestions for future research.

2 Theoretical Framework

2.1 “New” Internalization Theory

“Classic” internalization theory explains the reasons of the existence of the MNE when it creates an internal market within its organizational structure to bypass external market imperfections (Buckley and Casson 1976; Rugman 1981). The MNE overcomes the public good externality of knowledge by developing a network of foreign subsidiaries rather than exporting or licensing and transfer tacit knowledge-based FSAs across national borders. The FSAs are benefits or strengths specific to the firm relative to its competitors which can be made by its product and process technology, R&D, brand names, reputation, financial resources and access to finance, marketing and management skills (Rugman 1981; Rugman et al. 2011; Verbeke 2013). Overall, “classic” internalization theory focuses on the efficiency aspects of the MNE, in which the development and utilization of FSAs is central (Rugman 1981; Rugman and Verbeke 2008b).

Rugman and Verbeke (1992, 2001, 2003) make an important extension to classic internalization theory by developing the concepts of non-location bound (NLB) and location bound (LB) FSAs. This is known as “new” internalization theory. NLB FSAs can be internationally transferred within the MNE network with low costs and little adaptation requirements. They can be utilized, deployed and exploited in both home and host countries, and bring the benefits of economies of scale, scope and global integration. LB FSAs are bound to a particular location, a country, or a set of countries, or a region and bring the benefits of local responsiveness. LB FSAs can be both home- and host-country bound. In the former case, MNEs often have privileged access to home country natural resources, capital, government support and network within industries group which will have limited use in host countries (Collinson et al. 2017; Verbeke and Kano 2015). In the latter case, subsidiaries access host CSAs, such as complementary resources of external actors (e.g., suppliers, customers, distributors, research institutes and universities) and host country factors (e.g., national innovation system, labour forces, government policies, industrial clusters, etc.) to develop new knowledge, resources, capabilities and competencies (Birkinshaw 2000; Cantwell and Mudambi 2005).

Verbeke (2013) extends “new” internalization theory by specifying three types of FSAs. These include stand-alone FSAs; routines and codification; and recombination capability leading to tacit knowledge. Stand-alone FSAs are strengths relative to competitors, such as human resources, technological knowledge, marketing skills, reputational resources, and governance-related knowledge, etc. Routines reflect distinct ability to coordinate and efficient use of above FSAs and generate new value whether domestically or internationally. Effective routines can thus support the recombination that requires more than the exploitation of NLB FSAs abroad. Instead, it requires the creation of LB FSAs based on host CSAs that can be transformed to NLB FSAs when being integrated with the existing knowledge base and best practice attributes inside the MNE network. The process of effective and innovative bundling of resources and combining of tacit knowledge resulting in new and/or augmented FSAs leads to the development of recombination capability, which is a higher-order FSA (Rugman et al. 2011; Verbeke 2013).

2.2 Verbeke and Forootan (2012)’s Framework: An MNE’s Performance is Driven by FSAs, Not by Multinationality

Research on the multinationality-performance (M–P) relationship argue that firm performance depends on the trade-off between benefits and costs associated to international expansion (Berry and Kaul 2016; Geleilate et al. 2016). A positive M–P relationship is expected when increased multinationality allows firms to exploit proprietary FSAs and market imperfection, benefit from economies of global scale and scope of production, source lower cost inputs, engage in risk reduction from geographic diversification and access foreign knowledge. A competing argument suggests that there are a set of disadvantages associated with international expansion, such as costs of organization adaptation and duplication, costs of managing complex supply chain, and costs of cultural difference and coordination challenges across multiple markets (see Contractor 2012 for a detailed review).

Some scholars argue that the costs and benefits of multinationality occur in phases (Contractor et al. 2003; Lu and Beamish 2004; Pisani et al. 2020). For example, Contractors et al. (2012) discuss a three-stage S-curve model, in which firms often suffer the negative impact of multinationality in initial foreign growth due to liabilities of newness and foreignness. As MNEs learn how to operate in foreign markets, they progress into the mature stage when positive benefits of internationalization exceed the liabilities. Once they meet the threshold beyond which firms are over-expanded so that foreign operations become too difficult and costly to manage.

One the one hand, the above M–P relationships have been examined by numerous studies identifying wide variations in types of positive, negative, and nonsignificant liner relationship, as well as curvilinear relationships, such as U-curve and S-curve (see Nguyen 2017 and Nguyen and Kim 2020 for a comprehensive review). In light of these contradictory results, previous studies have introduced the moderating roles of firm specific assets, industry type and institutional and cultural discrepancies, etc. in shaping the M–P relationship (Geleilate et al. 2016; Kirca et al. 2011, 2016; Shin et al. 2017). While the above relationships have been confirmed by several meta-analytic studies (e.g., Kirca et al. 2011; Yang and Driffield 2012), Berry and Kaul (2016) and Pisani et al. (2020) failed to find any curvilinear M–P relationship, nor the moderating effect of intangible assets by replicating Lu and Beamish (2004)’s work on the S-curve model. To sum up, empirical findings remain largely inconclusive and confusing.

On the other hand, instead of remediating methodological deficiencies and empirical constructs, some scholars casted doubt on the theory underpinning that can predict a universal M–P relationship. They argue that the performance of an MNE is fundamentally determined by its possession of FSAs, not by the degree of multinationality from the perspective of internalization theory (Lee and Rugman 2012; Nguyen 2017; Verbeke and Brugman 2009; Verbeke and Forootan 2012). First, firm performance is positively related to the degree of multinationality only in the presence of FSAs (Kirca et al. 2011; Verbeke and Forootan 2012). This is because the core benefits of multinationality on firm performance, such as the exploitation of market imperfections and scale economies of global production, depend fully on firms’ underlying proprietary resources (Verbeke and Forootan 2012). For example, the positive M–P relationship is attributed to the competitive advantages of MNEs in the use of their FSAs within the MNE network to overcome the external market imperfections (Kirca et al. 2016). The economies of scale and scope can be achieved by licensing intangible FSAs, mainly in the forms of technology and patents, to foreign manufacturers instead of investing abroad (Hennart 2011). In neither case, it is the multinationality per se that affects performance outcomes upward or downward.

Second, international expansion does not offer a clear link to financial performance compared with domestic operations. Vertically integrated firms decide to perform activities through their subsidiaries if this is more cost efficient and effective than arm’s length transactions, and this argument holds for both domestic and foreign investments (Verbeke and Brugman 2009). In other words, foreign operation is not always the most efficient way to exploit intangible FSAs, and the individual firm only invests abroad when the expected performance is higher than that of domestic investment (Hennart 2011; Kirca et al. 2016; Powell 2014). As such, the degree of multinationality does not guarantee a systematic and universal impact on firm performance. Instead it is a designed variable that one firm needs to constantly evaluate the benefits and costs, along with other related decisions, such as entry mode and locations that best match its FSAs (Verbeke and Brugman 2009).

Third, the concept of a generalizable S-curve M–P relationship is not theoretically convincing (Verbeke and Brugman 2009). Being parallel with increased multinationality, MNEs start to develop international experience and coordination capabilities that enable them to more efficiently transfer and transform existing FSAs (Verbeke and Brugman 2009). They may also develop LB FSAs by accessing and leveraging local complementary resources, and thereby generate the resource recombination capabilities (Kirca et al. 2016; Verbeke and Brugman 2009). Consequently, an MNE not only becomes more efficient but also develops new sets of FSAs allowing them to offset high coordination costs and therefore improve their performance as geographic scope expands. As such, firm performance is fundamentally attributed to the FSAs development in international learning and managerial coordination, and subsequently in local adaptation and resource recombination.

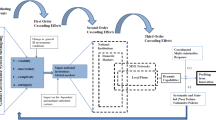

As responses to the criticism on a direct M–P relationship, Verbeke and Forootan (2012) proposes one framework (see Fig. 1) suggesting that knowledge-based FSAs should not be treated as control variables or moderators that impact on the strength of the M–P relationship. Rather, they argue that FSAs not only determine an MNE’s the degree of multinationality (indicated by the solid arrow in Fig. 1) but also the key drivers of MNE success in any host country environment or are the mediators accounting for any M–P relationship (indicated by the dotted arrow in Fig. 1). “Classic” Internalization theory suggests an MNE must possess some competitive advantages—such as technology, brand, marketing etc.—that are superior to those of the local firms in order to survive and thrive in host countries. As such, MNEs can internalize these FSAs inside their firm boundaries in order to effectively compensate for additional costs of doing business abroad arising from the liabilities of foreignness, and FSAs help to translate into enhanced performance in international markets (Rugman 1981; Rugman et al. 2011; Verbeke 2013). Verbeke and Forootan (2012) argue that such FSAs should include not only traditional type of firm resources such as R&D and brand names, but also the recombination capabilities that are embedded in MNEs’ management quality and routines. As such, Verbeke and Forootan (2012)’s framework is grounded in “new” internalization theory which complements “classic” internalization theory by emphasizing resource recombination with host country CSAs and the development of new FSAs. The recombination capabilities benefit the MNE performance as a whole when the newly created FSAs are transferred to NLB ones and disseminated to the headquarters and other subunits.

Source: Adapted from Verbeke and Forootan (2012), pp. 334

Relationship between FSAs, multinationality and performance.

Both “classic” internalization theory and “new” internalization theory capture the essence of the resource-based view suggesting that firm resources, especially those are valuable, rare, imitable and organized, are leveraged to create competitive advantages and in turn confer performance advantages (Barney 1991). Crook et al. (2008), using a meta-analytic regression, confirmed the positive impact of strategic resources on firm performance. Lee and Rugman (2012) find a U-shape relationship between FSAs of R&D intensity and marketing capabilities and firm performance. It is because low level of resources is not sufficient to be exploited in a profitable fashion. The negative effects are supressed by positive effects only at high level of resource commitment due to economies of scales and learning-by-investing allow firms to benefit efficiency advantages. Overall, both internalization theory of MNEs and the resource-based view of the firm have consistently suggest that firm performance is essentially determined by hard-to-replicate FSAs.

3 Literature Review

3.1 “New” Internalization Theory in Explaining Service Firms’ Internationalization: The Need to Develop LB FSAs Based on Host CSAs

“New” internalization theory that differentiates between NLB and LB FSAs is critical in advancing our understanding of the challenges of delivering services internationally. This is because services are intangible in nature, requiring simultaneous production, consumption and direct interaction between producers and consumers. The unique features of services must be considered when analysing internationalization of service firms (Brouthers and Brouthers 2003; Pla-Barber and Ghauri 2012). First, because services are intangible and inseparable with consumer involvement in their production, centralized mass production to gain economies of scale and scope is very difficult to achieve (Buckley et al. 1992; Xue et al. 2013). For example, Katrishen and Scordis (1998) find that international service providers in some industries may not even profit from economies of scale which are believed to benefit traditional manufacturers. Campbell and Verbeke (1994) argue that economies of scale in services occur only in marketing and brand building.

Second, most services require simultaneity of production and consumption. They are location-bound, meaning that their outputs must be consumed at the same time and at the location where they are produced (Bouquet et al. 2004; Erramilli and Rao 1993). The location-bound nature of services implies the need for local responsiveness or adaptation in foreign markets (Ball et al. 2008; Rugman and Verbeke 2008b). Given the intensive buyer–seller interactions, there are more opportunities for service MNEs to customize services as a response to linguistic and cultural differences and local market preferences and customer needs (Boehe 2016; Campbell and Verbeke 1994; Dunning 1989).

Due to the unique characteristics of service offerings, competitive advantages of service MNEs largely depend on their capabilities to understand and respond to local customer demands and government regulations (Meyer et al. 2015; Rugman and Verbeke 2008b). “New” internalization theory argues that the extent of local responsiveness depends on the degree to which LB FSAs are developed by MNEs and subsidiaries (Rugman and Verbeke 1992, 2001). As the provision of services tends to be people-intensive, these LB FSAs specific for service MNEs are mainly tacit knowledge and intangible assets, including local brand reputation, the capability to produce, store, interpret and analyse information and make them available for local customers, local knowledge about customer demands and institutional settings, and human capital and relational capital embedded in local personnel with training, learning and experience (Ando and Endo 2013; Buckley et al. 1992; Dunning 1989). Moreover, the creation of new LB FSAs is largely determined by MNEs’ capabilities to bundle or recombine existing FSAs with complementary host CSAs—the higher-order recombination capability as “new” internalization theory suggests (Hennart 2012; Verbeke 2013). These LB FSAs can even become NLB FSAs when they are transferred to geographically dispersed subsidiaries as best practices (Rugman et al. 2011). For service MNEs, knowledge and professional skills are transferred via flows of personnel within the MNE networks (Bouquet et al. 2004; Buckley et al. 1992; Dunning 1989).

3.2 The Internationalization of Chinese Service Firms

3.2.1 Services in China—the Dominant Role of State Ownership

Unlike Western MNEs’ FSAs, such as technology, global brand, and managerial capabilities, that are internationally transferrable across border, Chinese firms’ FSAs are based upon home CSAs and home country-bound in nature (Bai et al. 2019; Rugman and Li 2007; Rugman et al. 2016). It is particularly true for Chinese service firms as economies of scales are difficult to achieve due to the heterogeneous nature of many services which requires customization to local preferences (Buckley et al. 1992; Xue et al. 2013). Meanwhile, the abundant low-wage labour resources in China are irrelevant for services when venturing abroad due to the inseparability of service provision and consumption (Boehe 2016).

The first type of home country-bound FSA particular to Chinese service firms is referred to as government-created advantages (Ramamurti and Hillemann 2018) given that the majority are SOEs. Table 1 reports different ownership forms in key service industries in China based on annual assets. SOEs account for, on average, 41.52% of total assets in service industries while private-owned enterprise (POEs) account for only 21.95%. Meanwhile, those services with state as the largest ownership account for 31.00% of China’s GDP, while services dominated by private enterprises represent only 12.30% of GDP (China Statistical Yearbook of the Tertiary Industry 2018). Though data is not available for the financial sector, it is estimated that the largest proportion of Chinese SOEs is in the financial sector, accounting for 60% of all SOEs by assets (OECD 2017). Chinese SOEs have long been dominant in the service industries because most service sectors have not been open to POEs until 2005 when the State Council issued “36 guidelines” encouraging the development of non-state-owned economy (Breslin 2012).

Meanwhile, foreign investment remains trivial in China’s services. As shown in Table 1, service FDI from Hong Kong, Macao and Taiwan accounts for only 4.66% of total assets, and other foreign investments account for only 4.88%. The Service Trade Restrictiveness Index, based on the restrictions to foreign investment into 22 services, shows that China is in the top 4 out of 44 countries after India, Indonesia and Russia. Despite major reforms and liberalization in recent years, foreign investors still face numerous barriers to compete with domestic Chinese companies particularly in services (OECD 2015; Rutkowski 2015).

In addition to state ownership, other government-created advantages for Chinese service firms are the large domestic market size and the growth rate of China’s economy (Li and Oh 2016; Ramamurti 2009; Ramamurti and Hillemann 2018). Unlike manufacturing outputs which can be easily transferred and exported overseas, services account for only 8.9% of China’s total export in 2017 due to the intangible, inseparable and untradeable nature of many services (China Statistic Yearbook of the Tertiary Industry 2018). As such, the increasing domestic demand and consumptions are essential home CSAs for the development of Chinese service firms. Several Chinese service giants, such as Alibaba, Alipay, Tencent, WeChat Pay have substantially benefited from serving large domestic market due to Chinese customers’ willingness to use digital platform, as well as government regulations in supporting sunrise industries (Ramamurti and Hillemann 2018).

3.2.2 Challenges of Internationalization for Chinese Service Firms

As discussed above, home CSAs of state ownership and accumulated experience and knowledge in large domestic market are underlying key success factors for Chinese service firms so far. However, as discussed previously, the success of service’s internationalization requires different sets of FSAs—the LB FSAs based on host CSAs. Hennart (2009, 2012) argue that complementary resources in host countries are monopolized by local firms and are not freely accessible to all parties, especially foreign investors. Consequently, it is very difficult to achieve recombination of FSAs and host CSAs, which in turn constrain and inhibit the international market entry and expansion of firms (Hennart 2009). In this study, we argue that the home country-bound FSAs of Chinese service firms are hardly sustainable advantages to be utilized, deployed and exploited abroad in bundling with host country local resources for the development of LB FSAs (Bai et al. 2019; Du and Luo 2016) for several reasons.

First, due to the monopolistic protection from the government in their domestic operation, Chinese service SOEs are generally viewed as heavily cumbersome, inefficient and bureaucratic entities. Moreover, the close connection with the Chinese government can provoke sensitivity and negative reactions from host country governments and publics on the grounds of national security concerns and resource protection. The negative corporate images thus impede their access to host country resources, such as customer information, government support and skilled labour which are critical for service provision (Meyer et al. 2014; Rugman et al. 2014; Zhang et al. 2011). In other words, local adaptation of service offering is more challenging for Chinese service SOEs.

Second, the very limited participation of foreign investors in services in China may impede Chinese service firms to enhance their FSAs from cooperating with foreign MNEs. Therefore, Chinese government’s discriminatory policies toward inward FDI in services have restricted Chinese service firms’ opportunities to learn and benefit from knowledge dissemination from their Western counterparts.

Third, services are people-intensive requiring extensive investment in human resources rather than large-scale investment in physical assets (Ando and Endo 2013; Brouthers and Brouthers 2003). However, Chinese firms are at early stage of outward FDI, thus in general have limited pools of managers with international managerial capabilities in interacting with local managers, employees, and politicians in host countries (Estrin et al. 2018; Peng 2012; Rugman et al. 2016). Given the short history of outward FDI and limited export experience of Chinese services, it is difficult for Chinese service firms to develop managerial competence allowing the recombination process in developing new LB FSAs in host countries and integrate them with the rest of MNE network.

Lastly, Chinese service firms’ FSAs based on their access to large domestic market is only applicable in other developing countries, in which customer demands focus more on cost advantages than cutting-edge services (Cuervo-Cazurra and Genc 2008; Cui and Jiang 2009). For example, Chinese internet service providers, such as Alibaba, Tencent and Baidu have successfully applied their business models in other developing countries (Meyer 2018). However, the marketing and distribution capabilities developed in China are less exploitable in developed countries with more sophisticated customer demands and stricter regulatory institutions (Held et al. 2014; Verbeke and Kano 2016).

In summary, we argue that these home country-bound and stand-alone FSAs of Chinese service firms are of little relevance in international markets, and they even deter Chinese firms to invest necessary resources and efforts in developing host country-bound FSAs and providing local responsive services. As such, this study needs to go beyond “classic” internalization theory that mainly focuses on the exploitation of NLB FSAs within firms to limit transaction costs and maximize returns. In order to investigate the degree of multinationlaity and financial performance of Chinese service firms, we rely on Verbeke and Forootan (2012)’s framework (see Fig. 1) embedded in “new” internalization theory. As discussed previously, the framework argues that an MNE’s multinationality scope and performance are essentially underpinned by its FSAs. Due to their lack of recombination capabilities in developing host country-bound FSAs, this study enables us to assess the validity of Verbeke and Forootan (2012)’s framework in explaining Chinese service firms’ internationalization. In the next section, we use a dataset of the largest 500 Chinese service firms to identify the number of firms to be true MNEs by Rugman (1981) definition and their financial performance against global peers operating in the same sectors.

4 Methodology

4.1 Data Sources and Sample

We follow the approach in the study of Rugman et al. (2016) which explored foreign sales and performance of the largest Chinese manufacturing firms. Our study used a new dataset of Chinese service firms, which are legally registered and headquartered in Mainland China. We excluded those firms from Taiwan, Hong Kong, and Macao. We manually constructed our sample from the list of the 500 largest Chinese service companies ranked by revenues, which was published by the China Enterprise Confederation and China Enterprise Directors Association in 2018. We examined these firms’ annual reports together with other stock market documents (e.g., prospectuses and various announcements) to obtain data on their outward FDI, sales and geographic segments. Data were available for only 196 Chinese service firms due to either the unavailability of annual reports for the rest firms or their annual reports do not disclose information on geographic segments of foreign sales.

4.1.1 Financial Benchmarking

Rugman and Nguyen (2014) argue that the performance of Chinese firms should be compared to global peers rather than being left in the limbo of emerging market MNEs literature given that they internationalize aggressively. Financial benchmarking refers to the process of comparing the performance standards of a firm to that of other firms within the same industry. It uses financial information, most often in the form of ratios and metrics to perform these comparisons. In business practices, financial benchmarking has been widely used by MNEs and their subsidiaries. In academic literature, financial benchmarking is mainly studied in the fields of management accounting and financial management. It has received little or no attention in the international business literature. The studies by Rugman and Nguyen (2014) and Rugman et al. (2016) are exceptions.

Peer group analysis is one of the most frequently used methods for financial benchmarking. North American Industry Classification System (NAICS) codes are used to identify potential peers operating in the same industry for comparison purposes, i.e., finding firms with the same NAICS codes. The financial ratios and metrics from a group of peers in the same industry are calculated and analysed, which are called the industry financial data. Once the financial ratio benchmark is established, the financial ratios and metrics of a particular company relative to the industry financial data or two firms operating in the same industry are compared (Drury 2009; Sea et al. 2011).

4.1.2 Data Source for Industry Financial Data

We use Dun & Bradstreet (D&B) Global Business Browser database to collect financial data, including multiple financial ratios and metrics of Chinese service firms identified as true MNEs in accordance with Rugman (1981)’s definition, and the industry financial data (it is noted that D&B acquired OneSource Global Business Browser from Avention, the maker of OnceSource in 2017). Data is organized into industry in accordance with the NAICS. A NAICS code may correspond to more than one Standard Industrial Classification (SIC), so there may be several SICs listed. If a NAICS code maps to more than three SIC codes, only the first three SICs will be listed at the top of the page, with all corresponding SIC codes found in the NAICS description index (D&B Global Business Browser 2019). When there are fewer than 10 financial statements in a particular asset or sales size category, the composite data is not displayed because a sample of this small is not considered representative and could be misleading (D&B Global Business Browser 2019).

4.2 Definitions

Multinational Enterprises (MNEs)

A classic definition of an MNE is a firm headquartered in one country and having operations in other countries. Moreover, an MNE must have at least 10% of annual sales in foreign markets and at least three foreign subsidiaries (Rugman 1981; Rugman and Nguyen 2014; Rugman et al. 2016). The threshold of 10% (based on either sales, assets or profits) comes from international accounting standards, such as International Financial Reporting Standard IFRS8-Operating Segments (for firms’ reporting in compliance with IFRS), and SFAS No. 131, FASB Disclosures about Segments of an Enterprise and Related Information (for firms’ reporting in compliance with US GAAP).

Service sectors

National Bureau of Statistics of China defines services as the industries except for the primary and the manufacturing industries, including tourism; wholesale and retail trades; traffic, transport, storage and post; hotels and catering services; information transmission, computer services and software; finance; real estate; leasing and business services; scientific research and technical service; management of water conservancy, environment and public facilities; household service; education; health and social work; culture, sports and entertainment; and public administration and defence, compulsory social security. These classifications are consistent with the service categories defined by the International Standard Industrial Classification (China Statistic Yearbook of the Tertiary Industry 2018).

4.3 Measurements

Degree of multinationlaity

Foreign sales ratio (F/Tsales) is measured by foreign sales over total sales, which is frequently used to measure the degree of multinationlaity (Gomes and Ramaswam 1999; Hennart 2011; Rugman and Verbeke 2008b; Rugman et al. 2016). We carefully consult the accounting policies and disclosure notes of Chinese firms’ annual reports, which define foreign sales as sales outside Mainland China. Hong Kong and Macau are considered to be foreign sales according to the financial accounting and reporting by these firms. Meanwhile, we use data of foreign sales as they are reported by these Chinese service firms, in which foreign sales include both export sales by parent firms from China and sales generated by their foreign subsidiaries through FDI in host countries. We calculate the F/Tsales data for the five consecutive years ranging from 2014 to 2018.

Financial performance

We use multi-dimensional performance indicators, which measure growth (average 5-year sales growth), profitability (average 5-year net profit margin), financial stability (debt-to-equity, current ratio and quick ratio), and management effectiveness in resource utilization (return on assets ROA, and return on equity ROE) (Collinson et al. 2017; Rugman and Nguyen 2014; Rugman et al. 2016). D&B Global Business Browser provides financial performance data of Chinese service firms relative to the industry financial data. The average of 5-year data neutralizes variance over time (D&B Global Business Browser 2019).

5 Findings

5.1 The Majority of the Largest 500 Chinese Service Firms are Not MNEs: They are Actually Domestic Firms

We find that among the 196 largest Chinese service firms with the availability of financial data, 110 firms (56%) are purely domestic firms without any foreign sales. There are only 26 firms which have more than 10% of F/Tsales in at least 1 year between 2014 and 2018. However, there are three companies among them having less than three foreign subsidiaries, thus are not qualified for being an MNE, including China Eastern Airlines Corporation, China Southern Airlines Company, and Anhui Huilong Agricultural Means of Production. Overall, there are only 23 Chinese service firms, which are true MNEs according to Rugman (1981)’s definition. As such, the results show that the largest Chinese service firms have a very low degree of internationalization as measured by their F/Tsales. Our new finding is consistent with Rugman et al. (2016), which reports that there are only 49 true MNEs out of the 500 largest manufacturing firms. Table 2 ranks these 23 firms by their F/Tsales in 2018 and presents other information including service sectors, foreign assets over total assets—F/Tassets (if data is available in 2018), and ownership type (state ownership versus private ownership).

A closer assessment of these true Chinese service MNEs indicates that their internationalization engagement is even lower than the F/Tsales data suggests. For example, Fig. 2 explains the geographical location of foreign subsidiaries of these 23 Chinese service MNEs. There are 39% of subsidiaries located in Hong Kong and Macau, and 13% of them are located in British Virgin Islands and Cayman Islands. These locations are regarded as tax havens (for the list of tax havens, see Dharmapala and Hines 2009), in which internationalization activities are mainly for “round tripping” for “going out” to invest in third countries and investments back into China (Lu et al. 2014; Meyer et al. 2014). Such flows are more akin to domestic investments and therefore are not really indicators of outward FDI.

The geographical distribution (number) of foreign subsidiaries of 23 Chinese service MNEs. Sources: Authors’ compilation and calculation. Data are manually extracted from company annual reports

Furthermore, we find that Chinese service MNEs have frequently used foreign acquisitions to increase their F/Tsales. Based on annual reports, we find that there are 15 firms, out of the 23 true service MNEs, have acquired foreign assets by the end of 2018. There are only two service MNEs having no foreign acquisitions. The annual reports do not disclose information on the establishment mode of foreign subsidiaries for the rest five MNEs. Table 3 illustrates the foreign acquisitions undertaken by these 15 Chinese service MNEs. It includes F/Tsales comparison for the year before and right after each acquisition at which the foreign sales of the acquired company are included in consolidated financial statements. As shown in Table 3, the F/Tsales for most of these Chinese service MNEs increased either incrementally or substantially after each acquisition, especially for Shenzhen Huaqiang Industry and Nanjing Xinjiekou Department Store which had no foreign sales before their first acquisition abroad. Although the F/Tsales have reduced slightly for Jiangsu Holly Corporation and Neusoft Corporation, the absolute value for foreign sales have actually increased compared to the year before each acquisition. For example, Jiangsu Holly’s sales in the European market increased by 14.4% in 2017 after acquisitions compared to the previous year (Jiangsu Holly Corporation, Annual report 2018).

In summary, the very limited foreign sales of Chinese service firms delineate straightforward support to Fig. 1 (indicated by the solid arrow) showing that FSAs are the key determinants for an MNE’s multinationality level. On the one hand, home country-embedded CSAs, such as government support and monopolistic protection that restrict on foreign ownership, enable Chinese service firms to easily serve large domestic market without the need to develop competitive and sustainable FSAs. On the other hand, this type of stand-alone FSAs is not exploitable in making Chinese services competitive in foreign markets and generating enough foreign sales accordingly.

Furthermore, the frequent usage of foreign acquisition for international expansion is in line with the above arguments. It enables Chinse service firms not only take over foreign assets and thus foreign customers subsequently, but also to obtain strategic assets, especially those LB FSAs owned by local firms and adaptive to local service offerings. The improved FSAs can further generate more foreign sales and thus escalate multinationality level of Chinese service firms as suggested by Fig. 1. Furthermore, given the unanimous improvement of F/Tsales for the largest Chinese service firms after acquisitions, we fail to find any evidence to support the current literature arguing that Chinese firms in general often go abroad to acquire technologies and brands that can be brought back to their home countries for exploitation as a response to increasing domestic competition (Cui et al. 2014; Meyer 2015; Ramamurti 2012). Indeed, there is a paucity of empirical evidence showing to what extent foreign acquisitions of Chinese firms facilitate domestic sales versus foreign sales, reflecting a notable research gap.

It is also worth mentioning that many internationally well-known Chinese service brands in the sample are not true MNEs because they have less than 10% F/Tsales. Table 4 illustrates F/Tsales (2014–2018) for service firms in the top 20 most valuable Chinese brands ranking (Kantar Millward Brown 2018). It shows that there are overall 14 service brands but only Bank of China is true MNE. In other words, these service firms have developed their brand reputation and value by mainly servicing domestic Chinese market.

For example, Alibaba Group is an e-commerce company, which provides fundamental technology infrastructure for merchants, businesses and brands to market, sell and operate using internet. In 2016, Alibaba acquired a controlling stake in Lazada, which operates e-commerce platforms in Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam (Alibaba 2017). However, even with foreign acquisitions, its F/Tsales is only 8.33% in 2018. As stated in its annual report (2018), “we may face challenges in expanding our international and cross-border businesses and operations (p. 15)” due to the lack of acceptance of products and service offerings, inability to recruit international and local talents, and trade barrier, etc. (for full descriptions, see Alibaba 2018, Annual report p. 15). Similarly, although data is unavailable for the search-engine company Baidu—China's equivalent of Google, its annual report (2018) states that “our overseas operations may not be successful (Baidu 2018, p. 20)”, given the language and cultural difference, and diverse range of local preferences and demands etc. (for full descriptions, see Baidu 2018, Annual report p. 20).

5.2 Financial Benchmarking of Large Chinese Service MNEs Relative to Global Peers Using the Industry Financial Data

We use the industry financial data from D&B Global Business Browser to compare the financial performance of large Chinese service MNEs with global peers operating in the same industries for the 5-year period 2014–2018 (Table 5).

Firstly, we find that Chinese service MNEs pursue a high sales growth strategy by making aggressive foreign acquisitions (top line growth), but pay little attention to profit margins (bottom line) and the efficiency and effectiveness in utilizing resources in the balance sheet to deliver performance results in the income statement. Specifically, compared to the industry financial data, Chinese service MNEs have lower financial performance. Among the 23 Chinese service MNEs, there are only four of them with a solid financial performance (ROA and ROE), including COSCO Shipping Holdings (a SOE), Anhui Guozhen Environment Protection Technology Joint Stock (GZEP) (a POE), Bank of China (a SOE), and Industrial and Commercial Bank of China (a SOE). Furthermore, both COSCO Shipping Holdings and GZEP rely heavily on debt finance to fund their operations with the debt-to-equity ratio of 5.34 and 2.15 relative to that of the industry ratio of 1.27 and 0.58 respectively, implying high risk profiles in terms of financial stability.

Second, we compare Chinese service SOEs against global peers using the industry financial data. We discard all banks because their balance sheets are specific in these cases and potentially incomparable to other types of service firms. This approach has been used in in previous studies in the finance and international business literature (Banalieva and Dhanaraj 2013; Foley et al. 2007). We remove those firms which do not have the industry financial data for comparison purposes. After conducting this procedure, there are 12 SOEs left in the dataset. We run paired samples two-tailed t test. We report descriptive statistics of means, standard deviation, standard error and paired samples two-tailed t test and the significant level (Tables 6, 7).

In the same vein, we compare Chinese service POEs (six firms with the availability of industry financial data) against global peers using the industry financial data (Tables 8, 9).

The results in Tables 6 and 7 (Chinese service SOEs) and Tables 8 and 9 (Chinese service POEs) show that the financial performance (ROA and ROE) of both service SOEs and POEs are much lower than those of the industry financial data. Specifically, the ROA mean of Chinese service SOE is 2.14, whereas ROA mean of the industry financial data is 4.31. The paired samples t test for ROA using the financial benchmarking is significant at 0.01. Similarly, ROE mean of Chinese service SOE is 8.66 whereas ROE mean of the industry financial data is 15.77. The paired samples t test for ROE is significant at 0.05. In the same vein, ROA mean of Chinese service POEs is 1.47 whereas ROA mean of the industry financial data is 5.53. The paired samples t test for ROA is significant at 0.00. Furthermore, ROE mean of Chinese service POEs is 4.80 whereas ROE mean of the industry financial data is 14.62. The paired samples t test for ROE is significant at 0.05.

Overall, our empirical findings show that Chinese service MNEs perform poorly compared to their global counterparts in the same industry. While we have observed that the majority of Chinese service firms focus on domestic market, these 23 firms are true MNEs with various degree of internationalization (see Table 2). As such, their overall poor financial performance is not because of their limited scope of international expansion, but due to their lack of firm resources. As observed before, these Chinese service MNEs have either initiated or enhanced their multinationality by aggressively taking over foreign assets. However, foreign acquisition cannot guarantee the performance improvement for neither acquired local firms nor Chinese parent firms. Post-acquisition integration often involves extra costs, especially in culturally and institutionally distant countries (Shimizu et al. 2004). An effective and efficient integration with acquired firms is challenging for Chinese MNEs as they are lacking FSAs especially in international experience, management quality and ability to manage a multinational network (Peng 2012; Rugman et al. 2016).

For example, after having been acquired by Nanjing Xinjiekou Department Store in 2014 (see Table 3), House of Fraser in the UK has entered into administration in 2018 and was eventually sold to Sports Direct. The net profits of House of Fraser dropped from 319.56 million (RMB) in 2014 to a loss of 319.45 million (RMB) in 2017 (Nanjing Xinjiekou 2017, Annual report). On the one hand, it was due to the emergence of e-commerce, and the increasing property rents and labour costs in recent years which have challenged the traditional mode of physical retail stores. On the other hand, Nanjing Xinjiekou evidently suffers from the liabilities of foreignness and lacks international knowledge and managerial capabilities in tackling these uncertainties in foreign market as this acquisition was its first foreign investment. Meanwhile, the acquisitions made by Nanjing Xinjiekou were financed by debts. Like many other large Chinese conglomerates, such as Hainan Airlines Group, Dalian Wanda and Anbang Insurance, many assets of Nanjing Xinjiekou have been pledged by its parent firm Sanpower against debts (Financial Times 2018); however, using debts to finance foreign acquisitions is highly risky (Rugman and Nguyen 2014).

6 Discussions

6.1 Implications for Theoretical and Empirical Literature

This study responds to the current call for a more careful assessment of theoretical rationale to anticipate general M–P relationships given that extant empirical findings are mixed and inconclusive (Hennart 2007, 2012; Rugman and Verbeke 2008a; Verbeke and Brugman 2009; Verbeke and Forootan 2012). Instead of testing the M–P relationship with complex statistical models, we take a different approach by investigating basic but essential issues—the nature of FSAs, the multinationality scope, and financial performance of the Chinese service firms relative to global counterparts. Our findings firstly support Verbeke and Forootan (2012)’s framework arguing that international expansion per se is not the solution for performance upward, but knowledge-based FSAs are. Specifically, without the requisite FSAs for geographic expansion, Chinese service firms find it very challenging to achieve foreign sales and sustainable financial performance. Even for those true MNEs with a certain degree of internationalization—more than 10%, they have failed to transfer their foreign sales to superior performance as their ROA and ROE are poor relative to global peers using the benchmarking method with the industry financial data. Their international expansion is largely stimulated by home country government and their financial performance will only be improved if firms start developing FSAs.

Second, our findings can be well explained by “new” internalization theory (Rugman and Verbeke 1992, 2001; Verbeke 2013) as it is important to distinguish between NLB FSAs and LB FSAs, and between stand-alone FSAs and recombination capabilities in understanding Chinese service MNEs’ internationalization. Our core theoretical proposition is that Chinese service firms’ FSAs are mainly stand-alone in nature and home country-bound, which are deeply embedded in home CSAs (Rugman and Li 2007; Rugman and Nguyen 2014; Rugman et al. 2014). However, this type of the FSAs can only guarantee domestic success and are not transferrable in foreign markets (Rugman et al. 2016). It is particularly true for the internationalization of service MNEs given the high demand of host country-bound FSAs and the customization and localization of many service offerings (Bai et al. 2019). As such, Chinese service MNEs’ financial performance is poor because they have not yet developed advanced management capabilities in recombination with host CSAs.

Third, our findings provide new insights into the M–P literature when a firm quickly enhances its degree of internationalization through foreign acquisitions. Whether foreign acquisitions positively or negatively influence performance is fundamentally subject to an MNE’s FSAs in absorbing knowledge, learning from prior acquisition experience and its existing knowledge base, etc. (Cai et al. 2014; Shimizu et al. 2004). However, the majority of Chinese service firms are SOEs, which have long benefited from the Chinese government’s protection policies. Consequently, the lack of competition in domestic market and inertia have placed a limit on the organizational learning of these firms when encountering different business circumstances in international markets. We support this argument by finding that Chinese service MNEs, although have engaged in aggressive international acquisitions in taking over foreign assets and sales, their integration of foreign acquisitions may be constrained due to numerous reasons. As suggested by Verbeke and Forootan (2012)’s framework, it is ultimately the resource deficiency that have hampered Chinese service MNEs to deploy and exploit new assets through acquisitions and deliver desirable firm performance compared to their Western counterparts.

Lastly, our findings show that there is a fundamental error in the current literature, in which when a firm from an emerging country, especially from China, enters the Fortune Global 500, it is automatically referred to as an MNE. This is basically incorrect (Rugman et al. 2016). While it is true that more and more firms from China have entered the Fortune Global 500 over the years, the majority of them are, however, domestic firms, not MNEs by a classic definition (Rugman and Nguyen 2014). Thus, we suggest that going forward, the literature needs to exercise more prudence and use more precise terminology by distinguishing clearly “domestic firms” versus “MNEs”. It is important to refer to the definition of an MNE by Rugman (1981), identify whether firms are domestic firms or MNEs before discussing the need to develop new theories to explain the internationalization of emerging market MNEs.

6.2 Implications for Practice

The findings of our study provide important implications for managers and public policy makers. It is critically important for managers of Chinese service MNEs to benchmark, compare, and contrast their financial performance ratios and metrics against those of global peers using the industry financial data once they venture internationally. Although there are arguments in the literature that Chinese service firms have other non-financial objectives, such as promoting Chinese government’s interests and powers in international arenas, a lack of managerial effectiveness in using firm resources is not sustainable for firms’ survival in the short term and in the long term.

Chinese government needs not only to support service firms’ internationalization, but also to implement policies in strengthening their FSAs. One public policy option is to liberalize and open more the domestic service market to foreign investors and encourage Chinese service firms to learn and collaborate with those foreign investors operating in China. In this way, Chinese service firms could develop more sustainable FSAs which are deployable in foreign markets when they expand internationally.

As the business reality shows that more firms have encountered serious problems in aggressive buying of overseas assets using debt finance and subsequently got into financial troubles, such as Nanjing Xinjiekou (discussed above), Anbang Insurance (Reuters 2018), Hainan Airlines (Bloomberg 2019), Dalian Wanda Group, Sunac and LeEco (CNBC 2017; Financial Times 2018), etc. Chinese policy makers are recommended to tighten the evaluation and granting of credit finance and implement stricter and more effective measures in controlling and monitoring these financing sources, otherwise these valuable resources may end up in wasteful foreign investments and potential corruptions.

6.3 Limitations and Future Research Implications

Our study is subject to several limitations, which we suggest future research to tackle. First, while we have applied “new” internalization theory to explain the limited foreign sales of Chinese service firms and the poor performance of those true MNEs, we did not statistically test the impacts of FSAs, especially locally developed knowledge, resources and capabilities or LB FSAs required by service offerings on the degree of internationalization and performance. We suggest that future research can extend our study by collecting data and further identifying different types of LB FSAs that facilitate services’ internationalization. Similarly, by following our argument that FSAs of Chinese service firms are home country-bound and thus are not internationally transferrable, future study is suggested to examine the impacts of state ownership and home country government support on the performance of Chinese service firms.

Second, our findings on Chinese service firms’ aggressive international M&As in boosting foreign sales but failing in financial performance offer opportunities to investigate the role played by foreign acquisitions in influencing Chinese firms’ FSAs, the degree of multinatioanlity and performance. For example, future research is suggested to extend our study by statistically test to what extent acquired FSAs enable Chinese firms to increase domestic sales driven by strategic assets seeking verse foreign sales driven by foreign market seeking, and to further explore through what mechanisms that firm performance is affected upward or downward.

Data Availability

All the data used in this paper is available upon request.

References

Alibaba. (2017). Alibaba Group Holding Limited Annual Report 2017.

Alibaba. (2018). Alibaba Group Holding Limited Annual Report 2018.

Ando, N., & Endo, N. (2013). Determinants of foreign subsidiary staffing by service firms. Management Research Review, 36(6), 548–561.

Bai, T., Chen, S., & He, X. (2019). How home-country political connections influence the internationalization of service firms. Management International Review, 59(4), 541–560.

Baidu (2018). Baidu Inc. Annual report 2018.

Ball, D. A., Lindsay, V. J., & Rose, E. L. (2008). Rethinking the paradigm of service internationalisation: Less resource-intensive market entry modes for information-intensive soft services. Management International Review, 48(4), 413–431.

Banalieva, E. R., & Dhanaraj, C. (2013). Home regional orientation in international expansion strategies. Journal of International Business Studies, 44(2), 89–116.

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120.

Berry, H., & Kaul, A. (2016). Replicating the multinationality-performance relationship: Is there an S-curve? Strategic Management Journal, 37(11), 2275–2290.

Birkinshaw, J. (2000). Entrepreneurship in the global firm. London: Sage Publications.

Bloomberg (2019). HNA's $25 billion fire sale not enough to emerge from crisis. https://www.bloomberg.com/news/articles/2019-04-28/hna-s-25-billion-fire-sale-not-enough-to-bring-it-out-of-crisis. Accessed 18 Aug 2020.

Boehe, D. M. (2016). The internationalization of service firms from emerging economies: An internalization perspective. Long Range Planning, 49(5), 559–569.

Bouquet, C., Hébert, L., & Delios, A. (2004). Foreign expansion in service industries: Separability and human capital intensity. Journal of Business Research, 57(1), 35–46.

Breslin, S. (2012). Government-industry relations in China: A review of the art of the state. In A. Walter & X. Zhang (Eds.), East Asian capitalism: Diversity, change, and continuity. Oxford: Oxford University Press.

Brouthers, K. D., & Brouthers, L. E. (2003). Why service and manufacturing entry mode choices differ: The influence of transaction cost factors, risk and trust. Journal of Management Studies, 40(5), 1179–1204.

Buckley, P., & Casson, M. (1976). The future of the multinational enterprise. Basingstoke: Macmillan.

Buckley, P. J., Pass, C. L., & Prescott, K. (1992). The internationalization of service firms: A comparison with the manufacturing sector. Scandinavian International Business Review, 1(1), 39–56.

Cai, L., Hughes, M., & Yin, M. (2014). The relationship between resource acquisition methods and firm performance in Chinese new ventures: The intermediate effect of learning capability. Journal of Small Business Management, 52(3), 365–389.

Campbell, A. J., & Verbeke, A. (1994). The globalization of service multinationals. Long Range Planning, 27(2), 95–102.

Cantwell, J. A., & Mudambi, R. (2005). MNE competence-creating subsidiary mandates. Strategic Management Journal, 26(12), 1109–1128.

Chiang, Y. C., & Yu, T. H. (2005). The relationship between multinationality and the performance of Taiwan firms. Journal of American Academy of Business, 6(1), 130–134.

China Statistical Yearbook of the Tertiary Industry (2018). National bureau of statistics.

CNBC (2017). Debt problems are sinking three major Chinese companies. https://www.cnbc.com/2017/07/18/debt-problems-are-sinking-three-major-chinese-companies.html. Accessed 18 Aug 2020.

Collinson, S., Narula, R., & Rugman, A. M. (2017). International business (7th ed.). Haslow: Pearson.

Contractor, F. J. (2012). Why do multinational firms exist? A theory note about the effect of multinational expansion on performance and recent methodological critiques. Global Strategy Journal, 2(4), 318–331.

Contractor, F., Kundu, S., & Hsu, C. (2003). A three-stage theory of international expansion: The link between multinationality and performance in the service sector. Journal of International Business Studies, 34(1), 5–18.

Crook, T. R., Ketchen, D. J., Jr., Combs, J. G., & Todd, S. Y. (2008). Strategic resources and performance: A meta-analysis. Strategic Management Journal, 29(11), 1141–1154.

Cuervo-Cazurra, A., & Genc, M. (2008). Transforming disadvantages into advantages: Developing country MNEs in the least developed countries. Journal of International Business Studies, 39(6), 957–979.

Cui, L., & Jiang, F. (2009). FDI entry mode choice of Chinese firms: A strategic behaviour perspective. Journal of World Business, 44(4), 434–444.

Cui, L., Meyer, K. E., & Hu, H. W. (2014). What drives firms’ intent to seek strategic assets by foreign direct investment? A study of emerging economy firms. Journal of World Business, 49(4), 488–501.

Denis, D. J., Denis, D. K., & Yost, K. (2002). Global diversification industrial diversification and firm. Journal of Finance, 57(5), 1951–1979.

Dharmapala, D., & Hines, J. R. (2009). Which countries become tax havens? Journal of Public Economics, 93(9), 1058–1068.

Drury, C. (2009). Management accounting for business (4th ed.). Australia: Cengage Learning.

Du, X., & Luo, J.-h. (2016). Political connections, home formal institutions and internationalization: Evidence from China. Management and Organization Review, 12(1), 103–133.

Dunning, J. H. (1989). Multinational enterprises and the growth of services: Some conceptual and theoretical issues. The Service Industries Journal, 9(1), 5–39.

Erramilli, M. K., & Rao, C. P. (1993). Service firms’ international entry-mode choice: A modified transaction-cost analysis approach. Journal of Marketing, 57(3), 19–38.

Estrin, S., Meyer, K. E., & Pelletier, A. (2018). Emerging economy MNEs: How does home country munificence matter? Journal of World Business, 53(4), 514–528.

Foley, C. F., Hartzell, J. C., Titman, S., & Twite, G. (2007). Why do firms hold so much cash? A tax-based explanation. Journal of Financial Economics, 86(3), 579–607.

Geleilate, J. M. G., Magnusson, P., Parente, R. C., & Alvarado-Vargas, M. J. (2016). Home country institutional effects on the multinationality–performance relationship: A comparison between emerging and developed market multinationals. Journal of Business Research, 69(6), 1980–1992.

Gomes, L., & Ramaswamy, K. (1999). An empirical examination of the form of the relationship between multinationality and performance. Journal of International Business Studies, 30(1), 173–188.

Held, K., & Berg, N., et al. (2014). Facing discrimination by host country nationals emerging market multinational enterprises in developed markets. In A. Verbeke (Ed.), Multinational enterprises, markets and institutional diversity: Progress in international business research (9th edn.) (pp. 417–441). Emerald Group Publishing Limited: Bingley.

Hennart, J. F. (2007). The theoretical rationale for a multinationality-performance relationship. Management International Review, 47(3), 423–452.

Hennart, J. F. (2009). Down with MNE centric theories! Market entry and expansion as the bundling of MNE and local assets. Journal of International Business Studies, 40(9), 1432–1454.

Hennart, J. F. (2011). A theoretical assessment of the empirical literature on the impact of multinationality on performance. Global Strategy Journal, 1(1–2), 135–151.

Hennart, J. F. (2012). Emerging market multinationals and the theory of the multinational enterprise. Global Strategy Journal, 2(3), 168–187.

Jiangsu Holly Corporation. (2018). Jiangsu holly corporation annual report annual report 2018 (in Chinese).

Kantar Millward Brown. (2018). Top 100 most valuable global brands. http://online.pubhtml5.com/bydd/rxhd/. Accessed 9 Sep 2020.

Katrishen, F. A., & Scordis, N. A. (1998). Economies of scale in services: A study of multinational insurers. Journal of International Business Studies, 29(2), 305–323.

Kirca, A. H., Fernandez, W. D., & Kundu, S. K. (2016). An empirical analysis and extension of internalization theory in emerging markets: The role of firm-specific assets and asset dispersion in the multinationality-performance relationship. Journal of World Business, 51(4), 628–640.

Kirca, A. H., Hult, G. T. M., Roth, K., Cavusgil, S. T., Perry, M. Z., Akdeniz, M. B., et al. (2011). Firm-specific assets, multinationality, and firm performance: A meta-analytic review and theoretical integration. Academy of Management Journal, 54(1), 47–72.

Lee, I. H., & Rugman, A. (2012). Firm-specific advantages, inward FDI origins, and performance of multinational enterprises. Journal of International Management, 18(2), 132–146.

Li, J., & Oh, C. H. (2016). Research on emerging market multinational enterprise: Extending Alan Rugman’s critical contribution. International Business Review, 25(3), 776–784.

Lu, J. W., & Beamish, P. (2004). International diversification and firm performance: The S-curve hypothesis. Academy of Management Journal, 47(4), 598–609.

Lu, J., Liu, X., Wright, M., & Filatotchev, I. (2014). The impact of domestic diversification and top management teams on international diversification of Chinese firms. International Business Review, 23(2), 455–467.

Meyer, C. R., Skaggs, B. C., Nair, S., & Cohen, D. G. (2015). Customer interaction uncertainty, knowledge, and service firm internationalization. Journal of International Management, 21(3), 249–259.

Meyer, K. E. (2018). Catch-up and leapfrogging: Emerging economy multinational enterprises on the global stage. International Journal of the Economics of Business, 25(1), 19–30.

Meyer, K. E., Ding, Y., Li, J., & Zhang, H. (2014). Overcoming distrust: How state-owned enterprises adapt their foreign entries to institutional pressures abroad. Journal of International Business Studies, 45(8), 1–24.

Nanjing Xinjiekou (2017). Nanjing Xinjiekou Department Store Co., Ltd Annual Report 2017 (in Chinese).

Nguyen, Q. T. K. (2017). Multinationality and performance literature: A critical review and future research agenda. Management International Review, 57(3), 311–347.

Nguyen, Q. T. K., & Kim, S. (2020). The multinationality and performance relationship: Revisiting the literature and exploring the implications. International Business Review, 29(2).

Organisation for Economic Co-operation and Development (OECD) (2015). China in a changing global environment.

Organisation for Economic Co-operation and Development (OECD) (2017). OECD economic surveys China: Overview.

Peng, M. W. (2012). The global strategy of emerging multinationals from China. Global Strategy Journal, 2(2), 97–107.

Pisani, N., Garcia-Bernardo, J., & Heemskerk, E. (2020). Does it pay to be a multinational? A large-sample, cross-national replication assessing the multinationality-performance relationship. Strategic Management Journal, 41(1), 152–172.

Pla-Barber, J., & Ghauri, P. N. (2012). Internationalization of service industry firms: Understanding distinctive characteristics. The Service Industries Journal, 32(7), 1007–1010.

Powell, K. S. (2014). From M–P to MA-P: Multinationality alignment and performance. Journal of International Business Studies, 45(2), 211–226.

Ramamurti, R. (2009). What have we learned about emerging-market MNEs? In R. Ramamurti, & J. V. Singh (Eds.), Emerging multinationals in emerging markets (pp. 399–426). Cambridge: Cambridge University Press.

Ramamurti, R. (2012). What is really different about emerging market multinationals? Global Strategy Journal, 2(1), 41–47.

Ramamurti, R., & Hillemann, J. (2018). What is “Chinese” about Chinese multinationals? Journal of International Business Studies, 49(1), 34–48.

Reuters (2018). Exclusive: China's Anbang prepares to sell overseas properties worth $10 billion. https://www.reuters.com/article/us-anbang-group-divestment-property-excl/exclusive-chinas-anbang-prepares-to-sell-overseas-properties-worth-10-billion-sources-idUSKBN1K917X. Accessed 18 Aug 2020.

Rugman, A. M. (1981). Inside the multinationals: The economics of internal markets. New York: Columbia Press. (Reissued by Palgrave Macmillan in 2006 as Inside the Multinationals, (25th Anniversary Edition), Basingstoke and New York: Palgrave Macmillan).

Rugman, A. M., & Li, J. (2007). Will China’s multinationals succeed globally or regionally? European Management Journal, 25(5), 333–343.

Rugman, A. M., & Nguyen, Q. T. K. (2014). Modern international business theory and emerging economy multinational companies. In A. Cuervo-Cazurra & R. Ramamurti (Eds.), Understanding multinationals from emerging markets (pp. 53–80). Cambridge: Cambridge University Press.

Rugman, A. M., Nguyen, Q. T. K., & Wei, Z. Y. (2014). Chinese multinationals and public policy. International Journal of Emerging Markets, 9(2), 205–215.

Rugman, A. M., Nguyen, Q. T. K., & Wei, Z. Y. (2016). Rethinking the literature on the performance of Chinese multinational enterprises. Management and Organization Review, 12(2), 269–302.

Rugman, A. M., & Verbeke, A. (1992). A note on the transnational solution and the transaction cost theory of multinational strategic management. Journal of International Business Studies, 23(4), 761–771.

Rugman, A. M., & Verbeke, A. (2001). Subsidiary-specific advantages in multinational enterprises. Strategic Management Journal, 22(3), 237–250.

Rugman, A. M., & Verbeke, A. (2003). Extending the theory of the multinational enterprise: Internalization and strategic management perspectives. Journal of International Business Studies, 34(2), 125–137.

Rugman, A. M., & Verbeke, A. (2008a). Internalization theory and its impact on the field of international business. In J. J. Boddewyn (Ed.), Research on global strategic management. International business scholarship: AIB fellows on the first 50 years and beyond (14th ed.) (pp. 155–174). Emerald Group: Bradford.

Rugman, A. M., & Verbeke, A. (2008b). A new perspective on the regional and global strategies of multinational service firms. Management International Review, 48(4), 397–411.