Abstract

Using an agent-based model of the limit order book, we explore how the levels of information available to participants, exchanges, and regulators can be used to improve our understanding of the stability and resiliency of a market. Ultimately, we want to know if electronic market data contains previously undetected information that could allow us to better assess market stability. Using data produced in the controlled environment of an agent-based model’s limit order book, we examine various resiliency indicators to determine their predictive capabilities. Most of the types of data created have traditionally been available either publicly or on a restricted basis to regulators and exchanges, but other types have never been collected. We confirmed our findings using actual order flow data with user identifications included from the CME (Chicago Mercantile Exchange) and New York Mercantile Exchange. Our findings strongly suggest that high-fidelity microstructure data in combination with price data can be used to define stability indicators capable of reliably signaling a high likelihood for an imminent flash crash event about one minute before it occurs.

Similar content being viewed by others

Notes

The data and the agent distributions used in the construction of the limit order book ABM cannot be made public out of concerns of providing detailed trading strategy secrets on order size and placement.

Agents only manage a single order at a time. If an agent has an old order that is still in the order book at the time it is scheduled to place a new order, it cancels the old order before adding the new order to the market.

See Appendix A for exact numbers\(_{.}\)

The code for the ABM will be made available upon request by emailing ...

The simulation is initialized to begin running at the same price as the market started trading at on 1270. The model is run at 1 of 1/24 scale as the original number of market participants so as to decrease model run time. As a result the trading volume and resting order totals are multiplied by the 24.

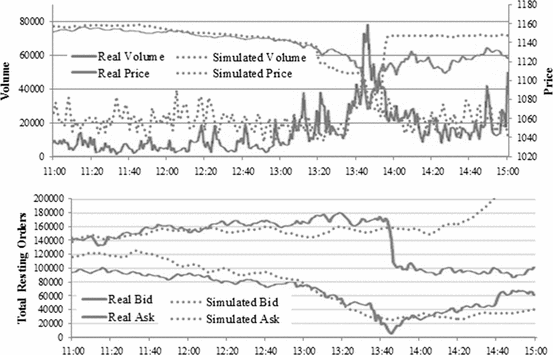

Fig. 4

Real versus simulated E-Mini: volume, moving average price, and order book depth

It is important to note that some of these metrics contain parameters that require tuning. In our work, we will select similar time scales for all the parameters so they produce new measurements every 30 s on average. We do not spend time calibrating these parameters to better fit the data, which has been an area of concern in previous research (Andersen and Bondarenko 2014).

Fig. 5

Market state diagram

The parameters were selected based on the average volume bucket, V, would be equal to 30 s during a normal period so the model would produce new values every 30 s. The number of buckets was selected during based on the (Easley et al. 2010) value.

We will simply refer to this as the price impact measure for simplicity throughout the rest of the paper.

The selling algorithm was believed to have been set at a PTV value of 9 % on May 6th 2010 accord the CTFC and SEC Report (2010).

References

Anderson P, Arrow K, Pines D (1988) The economy as an evolving complex system. Redwood City, Addison-Wesley Co

Andersen T, Bollerslev T, Diebold F, Vega C (2007) Real-time price discovery in global stock, bond and foreign exchange markets. J Int Econ 73(2):251–277

Andersen T, Bondarenko O (2014) VPIN and the flash crash. J Financ Mark 17:1–46

Benic V, Franic I (2008) Stock market liquidity: comparative analysis of Croatian and regional markets. Financ Theory Pract 32(4):477–498

Berger D, Chaboud A, Chernenko S, Howorka E, Wright J (2008) Order flow and exchange rate dynamics in electronic brokerage system data. J Int Econ 75:93–109

Berger D, Chaboud A, Chernenko S, Howorka E, Wright J (2008) Order flow and exchange rate dynamics in electronic brokerage system data. J Int Econ 75:93–109

Bethel E, Leinweber D, Rübel O, Wu K (2011) Federal market information technology in the post flash crash era: roles for supercomputing. In: Proceedings of the fourth workshop on High performance computational finance. ACM, pp 23–30

Brandt M, Kavajecz K (2004) Price discovery in the U.S. Treasury market: the impact of order flow and liquidity on the yield curve. J Finance 59:2623–2654

Brewer PJ, Huang M, Nelson B, Plott CR (2002) On the behavioral foundations of the law of supply and demand: human convergence and robot randomness. Exp Econ 5(3):179–208

CFTC & SEC (2010) Findings regarding the market events of May 6, 2010. September 30, 2010

Challet D, Stinchombe R (2001) Analyzing and modeling 1 + 1d. Phys A 300:285–599

Chiarella C, Iori G (2002) A simulation analysis of the microstructure of double auction markets*. Quant Finance 2(5):346–353

Clark-Joseph AD (2013) Exploratory trading. Unpublished job market paper,Harvard University, Cambridge, MA

CME Group (2013) CME MDP Message Statistics. Web. http://beta.cmegroup.com/market-data/distributor/market-data-platform.html

Cohen S, Kamarck T, Mermelstein R (1983) A global measure of perceived stress. J Health Soc Behav 24(4):385–396

Cont R, Kukanov A, Stoikov S (2013) The price impact of order book events. J Financ Econom 12(1):47–88

Darley V, Outkin AV (2007) NASDAQ market simulation: insights on a major market from the science of complex adaptive systems. World Scientific Publishing Co. Inc, River Edge

Duong H N, Kalev P S (2014) Anonymity and the information content of the limit order book. J Int Financ Mark. Institutions and Money

Easley D, López de Prado M, O’Hara M (2010) The microstructure of the ‘flash crash’: flow toxicity, liquidity crashes and the probability of informed trading. Working Paper

Easley D, López de Prado M, O’Hara M (2011) The microstructure of the flash crash: flow toxicity, liquidity crashes and the probability of informed trading. J Portf Manag 37(2):118–128

Easley D, López de Prado M, O’Hara M (2012) Flow toxicity and liquidity in a high-frequency world. Rev Financ Stud 25:1457–1493

Evans M, Lyons R (2002) Order flow and exchange rate dynamics. J Polit Econ 110:170–180

Farmer JD, Patelli P, Zovko I (2005) The predictive power of zero intelligence in financial markets. Proc Natl Acad Sci USA 102(6):2254–2259

Farmer JD, Foley D (2009) The economy needs agent-based modelling. Nature 460(7256):685–686

Friedman D, Rust J (1993) The double auction market: institutions, theories, and evidence. Addison-Wesley Co, Redwood City

Frey S, Grammig J (2006) Liquidity supply and adverse selection in a pure limit order book market. Empir Econ 30:1007–1033

Gode DK, Sunder S (1993) Allocative efficiency of markets with zero-intelligence traders: market as a partial substitute for individual rationality. J Polit Econ 101(1):119–137

Glosten L (1987) Components of the bid ask spread and the statistical properties of transaction prices. J Finance 42:1293–1307

Glosten L (1994) Is the electronic open limit order book inevitable? J Finance 49:1127–1162

Golub A, Keane J, Poon S H (2012) High frequency trading and mini flash crashes. arXiv preprint arXiv:1211.6667

Harris L (2003) Trading and exchanges: market microstructure for practitioners. Oxford University Press, New York

Hasbrouck J (1991) Measuring the information content of stock trades. J Finance 46:179–207

Hasbrouck J (1995) One security, many markets determining the contributions to price discovery. J Finance 50:1175–1199

Hasbrouck J, Saar G (2013) Low-latency trading. J Financ Mark 16(4):646–679

Hayes R, Todd A, Chaidarun N, Tepsuporn S, Beling P, Scherer W (2014) An agent-based financial simulation for use by researchers. Available at SSRN

Hendershott T, Jones CM, Menkveld AJ (2011) Does algorithmic trading improve liquidity? J Finance 66:1–33

Johnson N, Zhao G, Hunsader E, Meng J, Ravindar A, Carran S, Tivnan B (2012) Financial black swans driven by ultrafast machine ecology. Available at SSRN

Kaldor N (1961) Economic growth and capital accumulation. The Theory of Capital, Macmillan, London

Kim Y, Yang J (2004) What makes circuit breakers attractive to financial markets? A survey. Financ Mark Inst Instrum 13:109–146

Kirilenko A, Kyle A, Samadi M, Tuzun T (2011) The flash crash: the impact of high frequency trading on an electronic market. Available at SSRN: http://ssrn.com/abstract=1686004

Kirman A, Teyssiere G (2002) Microeconomic models for long memory in the volatility of financial time series. Stud Nonlinear Dyn Econom 5(4):1–23

Krantz M (2011) Mini flash crashes worry traders. USA Today. 16 May 2011. Web. http://www.usatoday.com/money/markets/2011-05-16-mini-flash-crashes-market-worry_n.htm

Kullmann L, Töyli J, Kertesz J, Kanto A, Kaski K (1999) Characteristic times in stock market indices. Phys A 269(1):98–110

LeBaron B (2001) A builders guide to agent-based financial markets. Quant Finance 1:254–261

Love R, Payne R (2008) Macroeconomic news, order flows, and exchange rates. J Financ Quant Anal 43:467–488

Macal CM, North MJ (2010) Tutorial on agent-based modelling and simulation. J Simul 4(3):151–162

Maslov S (2000) Simple model of a limit order-driven market. Phys A 278:571–578

Mandelbrot B (1963) The variation of certain speculative prices. J Bus 36:394

Menkveld AJ (2010) High frequency trading and the new market maker. Working Paper

Nanex (2011) Flash crash analysis continuing developments: flash equity failure for 2006, 2007, 2008, 2009, 2010, and 2011. http://www.nanex.net/FlashCrashEquities/FlashCrashAnalysis_Equities.html

O’Hara M (1995) Market microstructure theory, vol 108. Blackwell, Cambridge, MA

O’Hara M (2014) High frequency market microstructure. Working Paper. Cornell University

Paddrik M, Hayes R, Todd A, Yang S, Beling P, Scherer W (2012) An agent based model of the E-Mini S&P 500 applied to flash crash analysis. In: IEEE conference on computational intelligence for financial engineering & economics (CIFEr), pp 1–28

Preis T, Golke S, Paul W, Schneider JJ (2006) Multi-agent based order book model of financial markets. Europhys Lett 75(3):510516

SEC (2010) Concept release on equity market structure. Release No. 34-61358; File No. S7-02-10

SEC (2012) Investor bulletin: new measures to address market volatility. Release 23 July 2012. Web http://www.sec.gov/investor/alerts/circuitbreakersbulletin.htm

Subrahmanyam A (1994) Circuit breakers and market volatility: a theoretical perspective. J Finance 49:237–254

Svenson O, Maule AJ (eds) (1993) Time pressure and stress in human judgment and decision making New York. Plenum Press, New York

Wah E, Wellman M P (2013) Latency arbitrage, market fragmentation, and efficiency: a two-market model. In: Proceedings of the fourteenth ACM conference on Electronic commerce, 855-872

Zhang F (2010) High-frequency trading, stock volatility, and price discovery. Working Paper

Acknowledgments

The authors are very grateful to Philip Maymin, Michael Wellman, Nathan Palmar, Greg Feldberg and Wendy Wagner-Smith for their help and guidance with this paper. Special acknowledgement is due Andrew Todd for his help in the development of the agent-based simulation used in this paper. The research presented in this paper was authored by Mark Paddrik, Roy Hayes, William Scherer, Peter Beling, former contractors for the Commodity Futures Trading Commission (CFTC) who worked under CFTC OCE contract. The Office of the Chief Economist and CFTC economists produce original research on a broad range of topics relevant to the CFTC’s mandate to regulate commodity futures markets, commodity options markets, and the expanded mandate to regulate the swaps markets under the Dodd-Frank Wall Street Reform and Consumer Protection Act. These papers are often presented at conferences and many of these papers are later published by peer-review and other scholarly outlets. The analyses and conclusions expressed in this paper are those of the authors and do not reflect the views of other members of the Office of the Chief Economist, other Commission staff, or the Commission itself.

Author information

Authors and Affiliations

Corresponding author

Appendix

Rights and permissions

About this article

Cite this article

Paddrik, M., Hayes, R., Scherer, W. et al. Effects of limit order book information level on market stability metrics. J Econ Interact Coord 12, 221–247 (2017). https://doi.org/10.1007/s11403-015-0164-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11403-015-0164-6