Abstract

Purpose

In grid electricity consumption models, the location-based method uses regional average emission factors to account for environmental impacts. The market-based method is based on contractual agreements, verifying the exclusive claim on electricity from specific energy sources. An inconsistent application of these methods in life cycle assessment (LCA) and GHG accounting can lead to double counting. Especially, double counting electricity associated with rather low environmental impacts, such as renewable energy, might lead to impact underestimations. The aim of this paper is to identify, describe and propose solutions to double counting challenges.

Methods

A four-step procedure is carried out. First, the specifications on grid electricity mix selection in frequently applied standards for LCA and GHG accounting are analysed. Besides the ISO norms for LCA (14040/44) and carbon footprinting (14064/67), the GHG Protocol and the Product and Organizational Environmental Footprint (PEF/OEF) are considered. Based on this analysis, challenges of double counting electricity from specific sources are identified. In the third step, potential solutions for avoiding double counting are proposed. The last research step consists of an illustrative case study to demonstrate the calculation of market-based electricity mixes and identify potential adjustments necessities for LCA application.

Results and discussion

A parallel application of the location-based and the market-based method poses the main double-counting challenge. Thus, avoiding double counting demands consistent method application throughout the whole life cycle. Whereas this is relatively straightforward for the location-based method, consistent market-based method application is more challenging. LCAs rely on average life cycle inventory processes, which mostly include location-based electricity mixes. However, for consistent market-based method application throughout the life cycle, electricity-related environmental impacts in the inventory system also need to be market-based. This would demand a partial recalculation of LCI datasets using market-based residual electricity mixes. Besides illustrating the calculation of market-based electricity mixes, the case study is used to identify and propose solutions for two main challenges for residual mix application in LCA: countries without residual mix and electricity under a double marketing ban.

Conclusion

Double counting of electricity from specific energy sources is a challenge, since it can lead to under- or overestimations of environmental impacts. Both the location-based and market-based method can avoid double counting. However, parallel or inconsistent applications of both methods lead to double counting. In order to avoid double counting, there is a need to enable and use consistent electricity accounting rules in LCA and GHG accounting.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Global energy-related greenhouse gas (GHG) emissions added up to circa 33 Gt of CO2-equivalents in 2018, making them the largest contributor to climate change (IEA 2021). With 38%, electricity generation currently accounts for the largest share of energy-related GHG emissions. Consequently, emissions related to electricity consumption constitute a major contribution to most GHG accountings (Ryan et al. 2016; Siddik et al. 2020). The relevance of electricity-related environmental impacts also holds true for LCAs according to the ISO 14040 and 14044 (2006a, b) as well as Product and Organizational Environmental Footprint (PEF/OEF) studies (European Commission 2021). Electricity sources, such as fossil fuel or renewable energy sources (RES), strongly differ in their environmental impacts (Sphera Solution GmBH 2022; Wernet et al. 2016). Thus, the source of consumed electricity can strongly affect the results of GHG accountings and LCAs.

While the calculation of environmental impacts related to on-site electricity generation for own consumption is relatively straightforward, modelling environmental impacts related to grid electricity consumption poses a challenge (Weber et al. 2010). This is due to the interconnectivity of electricity grids. A large number of electricity producers supply electricity to the grid, which then transmits and distributes the mingled electricity to an even larger number of electricity consumers. Physically backtracking ones grid electricity consumption to a single supplier is therefore impossible (Weber et al. 2010).

There is a general distinction between the location-based (regional average) and the market-based (supplier-specific) method for calculating environmental impacts related to grid electricity consumption (ISO 2019b; WRI & WBCSD 2015). The location-based method bases grid electricity emission factors on the physical average consumption mix, of electricity-consuming facilities. The market-based method is based on contractual agreements, intending to guarantee a unique claim for electricity from specific energy sources, such as RES. Nevertheless, as pointed out by Finkbeiner and Bach (2021), the uniqueness of such claims needs to be critically discussed.

A widely used form of contractual agreements that are supposed to guarantee a unique claim for a specific type of energy are energy attribute certificates (EACs) (WRI & WBCSD 2015). In Europe, the most commonly used type of EACs are Guarantees of Origin (GOs) (Gkarakis and Dagoumas 2015). Even though the GO system and other EAC systems are critically discussed (Bjørn et al. 2022; Brander et al. 2018; Hulshof et al. 2019), the market-based purchasing and environmental accounting of electricity from RES is a frequently applied approach to lower ones GHG emissions. The Science Based Targets initiative (SBTi), for instance, recognizes the active sourcing of renewable electricity as a valid pathway to achieve GHG reduction targets (SBTi 2021).

According to the ISO 14067 (2019b), all electricity attributes that have been claimed via certificates, and other contractual agreements shall be removed from the consumption electricity grid mix. The removal of these exclusively claimed electricity attributes from the electricity consumption mix results in a residual electricity mix, which also plays a major role in the market-based method of the GHG Protocol (WRI & WBCSD 2015).

It is not uniformly defined in the standards for LCA and GHG accounting which electricity accounting method shall be used as the basis for calculating environmental impacts (European Commission 2021; ISO 2006a, b, 2019a, b; WRI & WBCSD 2015). Contractual agreements and residual electricity mixes are only used in the market-based method. The location-based method uses average grid emission factors for all grid electricity consumers in a specific region, regardless of the trade with market-based contractual agreements. Thus, the allowance of both market- and location-based method may lead to double counting, as also discussed by Bjørn et al. (2022) regarding the allowance of both scope 2 accounting methods by the SBTi (SBTi 2021). In the context of this paper, double counting can be seen as a double claiming of electricity from specific energy sources, such as RES, since this electricity is claimed both by individual EAC purchasing consumers (market-based) and by average grid electricity mix consumers (location-based) (Schneider et al. 2015). Especially a double counting of electricity from energy sources with relatively low environmental impacts, such as RES, might lead to impact underestimations. For example, the direct CO2 emissions related to the Norwegian residual mix (405 gCO2/kWh) are roughly 100 times higher than those of the Norwegian production mix (4 gCO2/kWh) (AIB 2022).

Double counting in the context of electricity accounting has already been addressed by some studies. Lenzen (2008) discusses the matter that environmental impacts related to electricity generation can be double counted if an electricity consumer is part of the supply chain of an electricity producer. Agez et al. (2020) analyse different methods to correct double counting in hybrid LCAs of LCA and environmentally extended input–output analyses (EEIOA). Betten et al. (2020) analyse different methods for avoiding double counting when integrating LCA into energy systems analysis. They find a difference of 19% global warming potential between direct and LCA emissions and highlight the importance of LCA in decision making for energy systems. In their report, Krebs and Frischknecht (2021) compare location-based European electricity mixes with market-based total supplier mixes, which include GO trade and thus substantially differ from location-based mixes. They state that preventing double counting can be achieved by 2 options: (1) limiting GO accounting to situations where double counting can be excluded and modelling all European electricity mixes based on production and trade data. (2) A mandatory full-disclosure system and the application of total supplier mixes in life cycle inventories (LCIs). However, unlike residual electricity mixes, total supplier mixes still include exclusively claimed GOs. Thus, the second approach proposed by Krebs and Frischknecht (2021) works well on a country level, but may still incorporate double counting on a product or company level. Also, a mandatory full electricity disclosure system is not alone for the LCA community to decide.

With regards to electricity disclosure to individual consumers, Klimscheffskij et al. (2015) address the importance of the accurate calculation and application of residual electricity mixes, which exclude all exclusively claimed electricity. Literature on residual electricity mixes in LCA is scarce, but the discussion on the topic is rather controversial. Olindo et al. (2021) argue against the application of residual mixes, due to inaccuracies in the calculation processes. Whereas Lewandowska et al. (2021) emphasize the importance of residual mixes in their LCA of refrigerating devices. Furthermore, both Sphera and ecoinvent have recently included residual electricity mixes in their LCI databases (Sphera Solution GmBH 2022; Wernet et al. 2016). However, residual mixes are not included as input for other processes of the database.

Even though the topic of double counting is discussed in scientific literature, there are no uniform accounting rules for electricity-related environmental impacts. Especially challenges of double counting regarding the use of LCI datasets and the suitability of residual mixes for LCA still need further discussion. Thus, the aims of this paper are to (i) identify methodological challenges of double counting electricity from specific electricity sources within and across frequently applied standards for LCA and GHG accounting; (ii) provide possible solutions for a consistent and double counting free accounting of electricity-related environmental impacts, with a focus on LCI datasets; (iii) analyse available European market-based residual electricity mixes and identify challenges for their application in LCA and GHG accounting, as well as to provide possible solutions for these challenges. This paper focusses on the European GO system. Nevertheless, it is also relevant for other EAC systems and other forms of contractual agreements.

2 Method

To reach the goals of the paper, the following four-step iterative procedure is defined:

-

1.

Analysis of electricity accounting methods in existing standards

-

2.

Identification of double counting challenges

-

3.

Determination of potential solutions to avoid double counting

-

4.

Illustrative case study of residual mix calculations and potential adjustments for LCA application

The first step—Analysis of electricity accounting methods in existing standards—consists of desk research. The ISO standards 14040, 14044, 14064 and 14067 as well as the Product Environmental Footprint (PEF), the Organizational Environmental Footprint (OEF) and the GHG Protocol (corporate and product) are analysed regarding their specifications on environmental accounting related to electricity consumption.

Each document is analysed regarding its requirements and recommendations on using location-based or market-based electricity mixes. Furthermore, the analysis includes specifications on which electricity-related emissions shall be accounted for. This includes the differentiation of direct electricity-related emissions and up-stream emissions, such as own consumption of power plants and electricity losses.

In the second step—Identification of double counting challenges—challenges of double counting regarding electricity from specific sources are identified. The identification process is structured into two parts.

First, general challenges of double counting electricity from specific sources are identified by analysing both the location-based and the market-based method separately. Next, the situation that both accounting methods are applied in parallel by different entities is investigated regarding double counting challenges. This part refers to the situation that the electricity consuming processes, and hence the electricity inputs, are either directly controlled by the reporting entity or that primary data is available for the supply chain processes.

Based on the findings of the first part, the second part identifies challenges of double counting within a single LCA or GHG accounting, which includes supply chain processes, for which no primary data is available. Special focus is given to the use of average LCI datasets. It is investigated which accounting method is usually used for calculating electricity-related environmental impacts in LCI datasets and if it is consistent with the method used in processes controlled by the reporting entity or with primary data.

The third step derives potential solutions for avoiding double counting. Based on the identified challenges, different regulatory requirements are proposed, which could preclude double-counting electricity from specific energy sources. The derived potential solutions address both the utilization of location-based and market-based electricity mixes. In accordance with step two, this step is split into one part addressing processes controlled by the reporting entity as well as primary data and one part addressing processes unknown to the reporting entity, for which average LCI datasets are used.

Due to their importance in avoiding double counting with the market-based method, the last research step—Illustrative case study of residual mix calculations and potential adjustments for LCA application—focuses on residual electricity mixes. In order to illustrate the currently applied issuance-based calculation method for European residual mix calculation, a simplified model residual mix area based on five theoretical countries is developed. These theoretical countries are modelled in a way that aims to illustrate real countries with strong effects on the residual mix calculation and countries which pose challenges for residual mix application in LCA.

Next, challenges when using state-of-the-art residual mixes in LCA are identified by examining the availability and applicability of residual electricity mixes for LCA and GHG accounting. It is analysed whether residual mixes are required and available for double counting free market-based environmental accounting. Furthermore, adoptions to residual mix calculations for LCA application are proposed.

3 Results

The first section of this chapter analyses specifications on electricity mix selection in frequently applied standards for LCA and GHG accounting (3.1). Based on this analysis, Sect. 3.2 describes potential challenges of double counting electricity from specific sources. Section 3.3 provides potential solutions for the avoidance of double counting. In the last section of this chapter, the currently applied issuance-based methodology for calculating European residual mixes is illustrated and potential adoptions for LCA application are proposed (3.4).

3.1 Analysis of electricity accounting methods in frequently applied standards

3.1.1 GHG protocol

The GHG Protocol Corporate Accounting and Reporting Standard divides emissions into three scopes (WRI & WBCSD 2004). Reporting of scopes 1 and 2 is mandatory and scope 3 reporting is optional. Electricity-related emissions are divided among these different scopes (WRI & WBCSD 2004, 2015). Direct emissions associated with on-site electricity generation for own use are reported in scope 1. Direct emissions associated with the consumption of purchased electricity, as well as T&D losses in self-owned electricity grids, are reported in scope 2. All other electricity-related emissions, such as emissions related to resource extraction and plant construction as well as T&D losses of non-self-owned power grids and losses due to electricity storage, such as hydro pump stations, are reported in scope 3 (WRI & WBCSD 2004, 2015). Electricity consumption occurring not at the reporting entity’s facilities, but at a different point of the entity’s value chain, is also reported under scope 3.

With regard to the applicable electricity mix, the GHG Protocol differentiates between the market-based and the location-based electricity method in its scope 2 amendment (WRI & WBCSD 2004, 2015). In location-based scope 2 accounting, an average regional grid emission factor is used to calculate emissions associated with grid electricity consumption. The emission factor is based on the average physical electricity consumption in a defined geographic boundary and defined time period. The location-based method omits the accounting for contractual agreements for claiming the attributes of specific electricity sources. The market-based method on the other hand bases the calculation of electricity-related emissions on contractual instruments, such as EACs. If the reporting entity has acquired contractual instruments that provide supplier-specific data and meet the scope 2 quality criteria, market-based emission factors shall be calculated according to these contractual instruments. If no such contractual instruments are acquired, market-based emissions shall be calculated using a residual electricity mix, which excludes any previously claimed electricity. If a residual electricity mix is not available, location-based emission factors may be used, which render the same market-based and location-based scope 2 total.

If supplier-specific data is generally available in the area of the electricity consuming facility, both market-based and location-based scope 2 emissions shall be reported (WRI & WBCSD 2015). “For companies adding together scope 1 and scope 2 for a final inventory total, companies may either report two corporate inventory totals (one reflecting each scope 2 method), or may report a single corporate inventory total reflecting one of the scope 2 methods” (WRI & WBCSD 2015). If a company reports a single inventory total, the same method shall be used for reporting and goal setting. The method choice shall be disclosed.

In its Technical Guidance for Calculating Scope 3 Emissions (WRI & WBCSD 2011b), the GHG Protocol specifies the accounting of up- and downstream emissions related to the reporting entity. For the calculation of emissions related to purchased goods and services the scope 3 standard specifies four calculation methods: (i) supplier-specific; (ii) hybrid; (iii) average-data and (vi) spend-based. In the supplier-specific method cradle-to-gate emission factors, specific to the individual suppliers, are used. However, the standard does not specify which emission factor shall be used for electricity consumption within the production processes of the purchased good. With the average-data method, emissions are calculated by multiplying the mass or another relevant unit of the purchased good or service by relevant cradle-to-gate secondary emission factors, which can be obtained from life cycle inventory (LCI) databases. These LCI databases usually calculate electricity-related emissions based on average location-based emission factors (Sphera Solution GmBH 2022; Wernet et al. 2016). With the hybrid method, supplier-specific data is used when available, and data gaps are filled with secondary data. If the first three methods are not feasible, the reporting entity should apply the spend-based method. With this method, companies collect data on the economic value of the purchased goods and services and multiply them by the relevant environmentally extended input–output emission factors.

Emissions related to the use of sold products are divided into two types: direct and indirect use phase emissions (WRI & WBCSD 2011b). Regarding the applicable emission factor for calculating electricity-related emissions, the scope 3 standard advises the use of regional or national grid emission factors and also allows the use of global average emission factors. These emission factors are consistent with location-based scope 2 accounting.

The standards described above specify GHG reporting on a corporate level and differentiate between three different scopes. The Product Life Cycle Accounting and Reporting Standard (WRI & WBCSD 2011a) specifies GHG accounting on a product level and aims to account for all life cycle emissions. Thus, both direct and indirect emissions related to electricity consumption shall be accounted for. With regards to emission factor selection for grid electricity consumption, the Product Standard states: “When an electricity supplier can deliver a supplier-specific emission factor and these emissions are excluded from the regional emission factor, the supplier’s electricity data should be used. Otherwise, companies should use a regional average emission factor for electricity to avoid double counting.” (WRI & WBCSD 2011a). Even though not as detailed, these specifications on electricity emission factor selection are in line with the market based-method.

3.1.2 ISO 14040, 14044, 14067 and 14064

The ISO standards on LCA (ISO 14040 and ISO 14044) and product carbon footprinting (ISO 14067) agree that direct emissions as well as all indirect emissions related to electricity production and consumption shall be accounted for (ISO 2006a, b, 2019b). This includes environmental accounting power plants’ own electricity consumption, as well as T&D losses and losses due to electricity storage. The ISO standard on GHG accounting on an organizational level (ISO 14064) is less binding regarding the inclusion of indirect electricity-related emissions and states that the emission factors “may” include these indirect emissions (ISO 2019a).

Regarding the use of the location-based or the market-based method, the ISO standards 14040 and 14044 do not provide specific information (ISO 2006a, b).

According to Annex E of the ISO 14064 “emissions from imported electricity consumed by the organization shall be quantified by the organization using the location-based approach by applying the emission factor that best characterizes the pertinent grid, i.e. dedicated transmission line, local, regional or national grid average emission factor” (ISO 2019a). These grid average emission factors shall be based on the average consumption mix of the relevant grid and the most recent available year. Besides this mandate on using the location-based method to account for emissions related to purchased electricity, the ISO 14064 states in Annex E.2.2 that an organization may report market-based information on electricity-related emission as additional information.

The ISO 14067 (2019b) on the other hand states that a supplier-specific electricity product shall be used if the supplier can provide contractual instruments that meet the quality criteria. If no supplier-specific information is available, emissions associated with the relevant electricity grid mix shall be used. “The relevant grid shall reflect the electricity consumption of the related region, excluding any previously claimed attributed electricity” (ISO 2019b). These requirements for the accounting of electricity-related GHG emissions are consistent with the market-based method (ISO 2019b; WRI & WBCSD 2015). If no electricity tracking system is in place, the grid mix shall reflect the regional average consumption.

3.1.3 Organizational and product environmental footprint

The European Commission specifies environmental accounting of electricity-related emissions in annex I and II for the PEF and annex III and IV for the OEF of its recommendation on the use of Environmental Footprint methods (European Commission 2021). By default, the PEF includes all life cycle stages. Thus, indirect emissions of electricity consumption shall be included in PEF studies. The OEF generally differentiates between direct and indirect emissions. Emissions related to electricity consumption are accounted for as indirect emissions. However, electricity-related emissions shall also include indirect as well as direct emissions.

In both PEF and OEF studies, the following electricity mixes shall be used in hierarchical order: (i) a supplier-specific electricity product, (ii) a supplier-specific total electricity mix and (iii) the country-specific residual consumption grid mix (European Commission 2021). Supplier-specific electricity products and supplier-specific total electricity mix must fulfil a minimum set of quality criteria. The hierarchical order and quality criteria are consistent with the market-based method, defined by the GHG Protocol (European Commission 2021; WRI & WBCSD 2015).

The specifications above are valid for processes run by the company applying the PEF study and for processes not run by the company but with access to supplier-specific information (European Commission 2021). Processes unknown to the company shall be modelled according to the PEF-specific LCI datasets. In accordance with internal emission factor rules, database providers usually model electricity input based on location-based average consumption electricity mixes (Sphera Solution GmBH 2022; Wernet et al. 2016).

Emissions related to electricity consumption in a product’s use phase shall be modelled based on average electricity consumption mixes. “The electricity mix shall reflect the ratios of sales between EU countries/regions” (European Commission 2021). The average EU consumption mix shall be used, if data on product sales is insufficient (European Commission 2021). The Environmental Footprint specifications for use-phase electricity consumption are consistent with the GHG Protocol’s location-based method (European Commission 2021; WRI & WBCSD 2015).

3.1.4 Summary of electricity accounting methods in frequently applied standards

The ISO standards 14040/14044 as well as OEF and PEF analyse all life cycle emissions (European Commission 2021; ISO 2006a, b). Thus, all emissions related to electricity consumption, including indirect emissions, need to be accounted for. Of the standards on GHG accounting, ISO 14064/67 and GHG Protocol, only the product standards mandate the inclusion of indirect electricity-related emissions (ISO 2019b; WRI & WBCSD 2011a). Under the GHG accounting standards for organizations, GHG Protocol corporate standard and ISO 14064, reporting indirect emissions related to electricity consumption is optional (ISO 2019a; WRI & WBCSD 2004, 2015).

In its scope 2 amendment, the GHG Protocol differentiates between the location-based and the market-based method for selecting the applicable electricity mix to account for emissions related to purchased electricity (WRI & WBCSD 2015). The location-based method is based on the physical average regional electricity consumption and the market-based method is based on contractual agreements, aiming to provide a unique claim for electricity from specific sources. With the exception of the ISO standards 14040/44, the specifications on electricity accounting in the analysed standards can be related to these two methods. The GHG Protocol Corporate Standard and it’s scope 2 amendment demand the reporting of electricity-related emissions in accordance with both methods in scope 2 (WRI & WBCSD 2004, 2015). However, it allows the selection of one single method for companies that report total GHG emissions by adding up the different scopes. Also, it mandates goal setting for GHG reduction targets and emission reporting according to one single method, which can be chosen by the reporting entity. The other analysed standards are more explicit with their specifications on electricity mix selection. These specifications, as well as the specifications on the inclusion of indirect electricity-related emissions, are summarized in Table 1.

3.2 Challenges of double counting electricity from specific energy sources

Section 3.2.1 presents the general challenges of double counting electricity from specific energy sources related to the location-based and market-based method. Section 3.2.2 addresses the challenges of double counting when using average LCI datasets in LCA and GHG accounting.

3.2.1 General challenges of double counting in location- and market-based electricity accounting

For the location-based method, the main challenge of double counting results from different spatial and temporal resolutions of the applied emission factors. Due to regional differences, database providers often provide individual LCI datasets for electricity consumption in different regions of larger countries, like China or the USA (Sphera Solution GmBH 2022; Wernet et al. 2016). Furthermore, the interest in emission factors with high temporal resolution (typically hourly) is rising, especially on a research level but also in the industrial application (Baumgärtner et al. 2019; Jaeger et al. 2022). Whereas this offers potentials, such as incentives for shifting electricity use to times and space of high RES shares and thus low emission factors via demand side management, it could also lead to under- or overestimations of total electricity-related environmental impacts. The reason for this is the application of different temporal and spatial emission factor resolutions within one electricity system.

The annual country-specific electricity consumption emission factor per kilowatt-hour is equal to the average emission factor of all kilowatt-hours that have been consumed during all hours of the year throughout the whole country. If specific kilowatt-hours, consumed at a certain time and space, are accounted for on an individual level and are also part of the average mix, these kilowatt-hours are double counted. This can lead to under- or overestimations of total electricity-related emissions.

For example, if both average annual and hourly-resolved emission factors were applicable, entities with higher electricity demands in times with lower emission factors or possibilities for load shifting might account their environmental impacts according to hourly-resolved emission factors. However, other entities could still use the annual average emission factors, which also include kilowatt-hours of electricity which were accounted for on an individual level using hourly-resolved emission factors. Figure 1 illustrates this issue with regard to different emission factors during a hypothetical day.

Differences in GHG emission levels over a hypothetical day

For the market-based method challenges mainly lie in double counting contractual agreements for the usage of electricity from specific sources. For instance, this may be the case for the specification on market-based electricity mix selection in the PEF guidance. If the supplier-specific total electricity mix, which should be used if no supplier-specific electricity product is available, is calculated according to the same method as the country-specific total supplier mix (outlined in Sect. 2 of the supporting information), it would also include exclusively claimed electricity products, which would hence be double counted.

Nevertheless, if applied consistently both the location-based and market-based method can avoid double counting of electricity from specific energy sources, such as RES. However, the probability of double counting is given, if location-based and market-based method are applied in parallel. The following simplified example illustrates this fact.

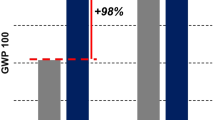

In a hypothetical region electricity generated from RES sums up to 25%, whereas the remaining electricity is generated from other energy sources, such as fossil fuel or nuclear (also referred to as grey electricity). In the location-based approach, every grid electricity consumer accounts for electricity-related environmental impacts according to the same electricity mix, containing 25% electricity from RES. If, in the market-based method, an electricity consumer group A acquires contractual agreements to claim all the generated electricity from RES, all other electricity consumers have to calculate their electricity-related environmental impacts according to the regional residual electricity mix, which consists of 100% grey electricity. Thus, the overall regional share of electricity from RES would still be 25%.

However, if consumer group A accounts for electricity-related environmental impacts according to the market-based approach and all other electricity consumers use the location-based approach, 75% of the electricity from RES would be double counted. The accounted share of electricity from RES would hence rise by 18.75% and add up to 43.75%. Figure 2 illustrates the elaborated example.

Illustration of challenges of double counting electricity from specific energy sources due to a parallel application of location-based and market-based electricity accounting method, based on a hypothetical region

3.2.2 Challenges of double counting with average upstream and downstream processes

Following one single method for electricity mix selection, location or market-based, when calculating electricity-related environmental impacts in LCA and GHG accounting is essential to avoid double counting. This method has to be applied consistently throughout all processes of the entire LCA or GHG accounting. However, to make LCAs and GHG accountings operable, they rely on average datasets from LCI process databases, such as Sphera and ecoinvent. For a consistent application of one single method for electricity mix selection, these LCI datasets would also have to follow the same method.

Average LCI datasets mostly use location-based electricity mixes in order to calculate environmental impacts related to grid electricity consumption if no industry-specific data is available (Sphera Solution GmBH 2022; Wernet et al. 2016). Hence, if market-based electricity mix selection is applied for processes controlled by the reporting entity or for which supplier-specific information is available and location-based electricity mixes are chosen for LCI datasets, both methods are applied in one single study. Consequently, this procedure is susceptible to double counting.

Applying market-based and location-based electricity mix selection in one LCA or GHG accounting is illustrated with a simplified example in Figure 3. Here, the reporting entity purchases electricity from RES for their manufacturing facility and accounts for it. The hypothetical final product consists of two parts, which again consist of several parts. The reporting entity obtains supplier-specific information on the manufacturing of part 1. However, the manufacturing entity cannot provide valid contractual agreements for the consumed electricity. Thus, the residual electricity mix is used for electricity consumption. For all other parts, no supplier-specific information is available. Hence, average LCI datasets are used, which usually model electricity input according to location-based consumption mixes.

Overview of simplified example illustrating the parallel use of location- and market-based electricity mixes in one LCA and GHG accounting, when including both market-based electricity and average LCI datasets with location-based electricity inputs

3.3 Potential solutions for avoiding double counting electricity from specific energy sources

A parallel application of both location-based and market-based methods in one region can lead to double counting and consequently under- or overestimations of electricity-related environmental impacts. Hence, there is a need to enable and use consistent electricity accounting rules in LCA and GHG accounting. The consistent use of one method is especially important for LCAs and GHG accounting that evaluate and compare emission reduction targets of different corporations or products, since the achievement of these targets might be different depending on which electricity accounting method was used.

A consistent application of the location-based method can be relatively straightforward, since all grid electricity consumption in a specific region would be associated with the same emission factor. Environmental accounting for a specific source of electricity, such as RES, would only be possible if the electricity generation system and the electricity consuming facility are directly connected, and hence do not use the public grid for electricity transfer among each other.

In order to avoid double counting with a consistent location-based accounting, the simplest solution is to allow only one emission factor per region (e.g. country level) and predefined time period (e.g. annual resolution). This emission factor would then be applied to all electricity-consuming processes in the region during the specific time period. Hence, the same emission factor for electricity consumption would be used for processes known to the reporting entity and all LCI datasets. If emission factors with different temporal and spatial resolutions are permitted, an accounting system among the different electricity mix resolutions is necessary, in order to avoid double counting and thereby an under- or overestimation of electricity-related environmental impacts.

For the market-based method, avoiding double counting is more challenging. In order to avoid double counting, the market based-method needs to be applied consistently throughout the life cycle. For processes known to the reporting entity, this is relatively straightforward. If contractual agreements are acquired that fulfil the necessary criteria to claim grid electricity from a specific energy source, associated environmental impacts should be calculated according to the specific emission factors. If no valid contractual agreements are acquired, environmental impacts related to grid electricity consumption should be calculated according to the regional residual electricity mix. In this case, countries with a full tracking system that do not have a residual electricity mix (see Sect. 3.4.2) and countries with a subsidy scheme preventing the issuing of EACs (see Sect. 3.4.3) require special arrangements. Also, solutions for the following two challenges must be found: electricity consumption during a product’s use phase and the utilization of average LCI data sets.

As summarized in Sect. 3.1.3, the PEF mandates the use of location-based electricity mixes if a product’s use phase is related to electricity consumption. However, for consistent market-based method application, market-based electricity mixes need to be used for all phases of a product’s life cycle. The most conservative approach for market-based electricity mix selection would be to choose the residual mix for calculating electricity-related environmental impacts in the use phase. However, this approach could lead to an impact overestimation of the use phase, since it would neglect that many (private) electricity consumers use electricity from RES based on contractual agreements or non-certificate-based reliable tracking systems (EEG 2021; Hauser et al. 2019). A comparison of direct CO2 emissions related to residual mixes and total supplier mixes, which includes contractual agreements that are used for electricity claims within the country, emphasises this point. For example, in Ireland, the residual mix is associated with more than three times higher direct CO2 emissions than the total supplier mix (AIB 2022).

One valid solution for estimating the average use phase environmental impacts of a product would therefore be the usage of a sector-specific total supplier mix for the use phase. For example, use phase electricity consumption of products, which are usually used by private households, would be calculated according to the total supplier mix of private households. Since such sector-specific total supplier mixes are not readily available, we suggest the application of a country-specific total supplier mix as an intermediate solution until more adequate data is available.

As outlined in Sect. 3.2, average LCI datasets mostly use location-based electricity mixes to calculate environmental impacts related to grid electricity consumption if no industry-specific data is available. However, if electricity from RES can be exclusively accounted for processes controlled by or known to the reporting entity, all LCA data needs to follow the market-based method, in order to avoid double counting.

Instead of using location-based electricity mixes in LCI database processes, we suggest that residual electricity mixes are used as default input for the calculation of grid electricity-related environmental impacts in LCI data base processes. If a supplier can prove the consumption of electricity from specific energy sources via own electricity generation or contractual agreements, this specific electricity should be accounted for. This would require a recalculation of LCI datasets if data is not already calculated on a supplier-specific basis. The involved effort is critically discussed in Sect. 4.

In conclusion, the avoidance of double counting electricity from specific energy sources is only possible via the consistent application of one electricity accounting method. For the location-based method, the simplest solution for avoiding double counting is the utilization of one fixed emission factor for each specific region and time period. If different regional and temporal resolutions are to be allowed, an accounting system needs to be developed in order to avoid under- or overestimations of total environmental impacts. In market-based electricity accounting the application of residual mixes is crucial, whenever no valid electricity supplier information is available and relevant amounts of electricity are consumed. Market-based electricity mixes should be consistently applied, both for electricity consumption in processes known to the reporting entity and in processes unknown to the reporting entity, for which average LCI datasets are used.

3.4 Illustrative case study: residual mix calculation and challenges for LCA application

Using an illustrative case study, this chapter addresses challenges with residual mix calculation and application. In Sect. 3.4.1, the case study is described and the issuance-based residual mix calculation method is applied. Based on this illustration, two main challenges for residual mix application in LCA and GHG accounting are discussed: the non-availability of a residual mix (3.4.2) and the inclusion of electricity that is traced by a non-certificate-based reliable tracking system (RTS) (3.4.3). The issuance-based calculation methodology, which is currently used for European residual mix calculation (Kuronen et al. 2020), is explained in detail in Sect. 2 of the supporting information.

3.4.1 Case study description and application of issuance-based residual mix calculation

This section applies the issuance-based method in a simplified case study of a residual mix calculation area, consisting of five countries. In this simplified model, countries have both physical and market-based electricity trade. The market-based electricity trade only occurs via EAC transfer. No physical electricity trade and no EAC trade takes place with countries outside the residual mix area. Furthermore, losses occurring from the generation to the consumption of electricity, such as T&D losses or losses due to electricity storage, are not considered. Hence, electricity generation in the model residual mix area is equal to electricity consumption.

Table 2 shows the production and consumption data of the five countries in the model residual mix area. Table 3 shows the market-based EAC trade among the countries. “Issuance” stands for EACs that have been provided for electricity generation within the country. “Cancellation” marks an EAC as having been consumed, at the request of an end-user, so that its attributes cannot be claimed by another end-user. “Expiry” marks the point at which an issued EAC is no longer eligible for cancellation and is thereby not claimed by any electricity user within the residual mix calculation period.

The first three countries have no special requirements for electricity tracking, but strongly differ in their electricity generation profile as well as the acquisition of EACs. Their electricity is mainly based on renewable (RES), fossil (FOS) and nuclear (NUC) energy sources, respectively. The “Subsidy Country” has a subsidy scheme for electricity from RES in place and forbids the issuance of EACs for this subsidized electricity from RES (sRES), as done under the German Renewable Energy Sources Act (EEG) (EEG 2021; EU 2018). The “Full tracking Country” mandates the full tracking of all produced and consumed electricity, as done in Austria (RIS 2013).

Based on Tables 2 and 3, the market-based residual electricity mix and the total supplier mix can be calculated. Figure 4 illustrates the step-by-step calculation procedure for these market-based electricity mixes of the “Renewable Country” (a) and the “Subsidy Country” (b), as well as all countries share in the attribute mix (c).

Illustration of market-based electricity mix calculation for the “Renewable Country” (a) and the “Subsidy Country” (b), as well as the attribute mix calculation (c)

Of its 150 TWh total electricity generation, the “Renewable Country” generates 140 TWh from RES. For all electricity from RES, the country issues EACs, which are hence deducted from the domestic residual mix. It is assumed that 10 TWh of issued EACs from RES expire and are added again to the domestic residual mix, which thus consists of 10 TWh from RES and 10 TWh from FOS. To determine the untracked consumption, the 30 TWh of cancelled EACs are deducted from the physical electricity consumption. The volume of untracked consumption (100 TWh) is 80 TWh higher than the domestic residual mix volume. Thus, the “Renewable Country” is classified as a “Deficit Country” and its deficit in the final residual mix of 80 TWh is filled with the attribute mix. This attribute mix is calculated by adding all residual mix surpluses from the “Surplus Countries”, which have a lower volume of untracked consumption than of the domestic residual mix. The attribute mix calculation is explained in detail in Sect. 2 of the supporting information. By adding the 30 TWh of cancelled EACs to the final residual mix, the total supplier mix is calculated, which consists of 33% RES, 48% FOS and 19% NUC.

The “Subsidy Country” produces a total of 300 TWh of electricity. 120 TWh are produced from RES, of which 100 TWh are electricity from sRES, for which the country does not allow the issuance and trade of EACs. In the residual mix calculation, this electricity is treated as tracked by a non-certificate-based RTS. Electricity generated and tracked by a non-certificate-based RTS is considered as if EACs have been issued and canceled in the country. Further including the 10 TWh of issued EACs the volume of the “Subsidy Country’s” domestic residual mix is 190 TWh, which is 90 TWh higher than the untracked consumption. The 100 TWh surplus of the domestic residual mix is added to the attribute mix. Both the “Subsidy Country's” final residual mix and its contribution to the attribute mix have the same electricity shares. Adding the EAC cancellations to the final residual mix results in the total supplier mix, consisting of 68% RES, 28% FOS and 2% NUC.

A step-by-step illustration of the market-based electricity mix calculation for the three other countries can be found in Sect. 3 of the supporting information. Since, in the “Full tracking Country” all produced and consumed electricity is traced via EACs, the country has no residual mix and does not play a role in the attribute mix calculation. The “Full tracking Country's” total supplier mix is a result of all cancelled EACs. The final residual mixes and total supplier mixes of all countries can be found in Figure 5.

Market-based electricity mixes of the model residual mix area: final residual mix (a) and total supplier mix (b) for the base case; final residual mix (c) and total supplier mix (d) for the case that only EACs from RES are accountable

3.4.2 Countries without residual mix

Some countries, such as Austria, have a mandatory full-disclosure system for electricity (RIS 2013). Within a full-disclosure country, every produced and consumed electricity unit must be tracked via market-based instruments, such as EACs. The countries’ untracked consumption should therefore be zero. If this is the case, no residual electricity mix exists (AIB 2022; Krebs and Frischknecht 2021). Furthermore, the tracked cancellation of EACs within a country can equal or even surpass the annual consumption, without a mandatory full-disclosure system.

For processes controlled by the reporting entity or with supplier-specific information, a complete tracking of all produced and consumed electricity is beneficial for accurate market-based accounting of electricity-related environmental impacts. As described in Sect. 3.3, a double counting free utilization of average LCI datasets is only possible, if these datasets also use market-based electricity mixes. However, the proposed approach of using residual electricity mixes as default in average LCI datasets is not applicable for countries without residual mix.

Several solutions to this issue are possible. One possibility is to use the country’s total supplier mix. With this mix, country-specific market-based activity is considered, but this mix still includes cancelled EACs. Another possibility is to use the average residual electricity mix of the corresponding residual mix area. This mix can be calculated on a short-term basis, without any system changes. For countries taking part in the GO system, this would be the European average residual mix. We propose this as a conservative intermediate solution.

Another solution would be to only account for EACs of RES and exclude all EACs of non-RES from the residual electricity mix calculation. Allowing only the accounting of EACs from RES would result in a residual mix for the “Full tracking Country” and would consequently change the market-based electricity mixes of the other countries in the residual mix area as well. Figure 5 shows the residual mixes and total supplier mixes for the base case (as described in Sect. 3.4.1) and if only EACs from RES could be accountable.

If only electricity from RES could be individually accounted for, all European countries would currently have a residual electricity mix (AIB 2022). In the event that a country’s cancellation of EACs from RES is equal to or surpasses its electricity consumption, this country would again not have a residual electricity mix. In this case, we propose using the country’s total supplier mix for calculating electricity-related environmental impacts in background processes. This mix would consequently only include electricity from RES. Since EACs from RES would be cancelled for all electricity consumption in this country, using the total supplier mix would not lead to significant over or under- or overestimations of electricity-related environmental impacts.

3.4.3 Non-certificate-based reliable tracking systems

According to article 19 of the recast of the Renewable Energy Directive (EU) 2018/2001, member states can decide not to issue GOs to an RES-based electricity producer that receives financial support and thus account for the market value of GOs on a national level (EU 2018). A prominent example is electricity from RES that has received financial support under the German EEG. According to §80 of the EEG, there is a prohibition on double marketing energy from renewable energy (EEG 2021). Consequently, the energy that has received financial support under subsidy schemes, such as the EEG, cannot be exclusively claimed. Sect. 4 of the supporting information contains additional information on the accounting of EEG-subsidized electricity.

As illustrated for the Subsidy Country (see Sect. 3.4.1), generated electricity, which is tracked by a non-certificate-based RTS, is not part of the residual mix. However, this electricity can also not be accounted for on an individual level. We suggest including subsidized electricity, which is tracked by a non-certificate-based RTS, in consistent market-based accounting according to § 78 EEG (EEG 2021).

Thus, electricity-consuming entities may substitute a proportion of their market-based electricity mix with the share of electricity tracked by a non-certificate-based RTS, in accordance with their respective surcharge payment, in the last step of the electricity disclosure procedure (Hauser et al. 2019). This holds true, regardless of the acquisition of EACs or other contractual agreements verifying the exclusive claims. If the subsidy scheme does not request a surcharge but still prohibits the exclusive claiming of subsidized electricity, this electricity should be distributed equally among all electricity consumers. Alternative approaches are outlined in Sect. 4 of the supporting information.

Since a significant number of electricity-intensive companies are fully or partially exempt from surcharge payments, such as the EEG surcharge, we suggest a conservative approach for the inclusion of subsidized electricity, which is tracked by a non-certificate-based RTS. By default, companies should account for their electricity-related environmental impacts according to the residual electricity mix without the subsidized electricity. Only if a company proves their payment of the relevant surcharge, it may account for the subsidized electricity according to its payments.

4 Discussion

The results of this paper show that a double-counting free accounting of electricity-related environmental impacts can only be achieved, via the consistent application of one electricity accounting method: market-based or location-based. For the location-based method, a consistent application throughout the whole LCA would be relatively straightforward, since LCA databases use location-based emission factors unless electricity generation is specified differently by industry. The consistent application of the market-based approach is more challenging, since it requires the application of residual electricity mixes whenever no supplier-specific electricity data is available. One main challenge is that LCI datasets, in which electricity-related environmental impacts are calculated using residual electricity mixes, are currently not available in LCI databases and their implementation would be related to significant efforts (Sphera Solution GmBH 2022; Wernet et al. 2016). This is especially true since not only Europe but also other countries are using or are starting to implement EAC systems (Bricaud 2022).

Due to the amount of effort involved in changing the default electricity mix from location-based to market-based residual electricity mixes in LCI datasets, the practical relevance of double counting needs to be discussed. Since, for many products, the largest share of environmental impacts originates from the supply chain rather than from electricity consumption during final product manufacturing (Wernet et al. 2016), the amount of double counting as illustrated in chapter 3.2.2 might be rather low. Nonetheless, there is a strong push towards increasing the primary data share in LCAs and GHG accountings through initiatives, like Catena-X, Pathfinder or Together for Sustainability (Together for Sustainability 2022). These initiatives also provide information on how to include electricity from specific energy sources in the primary data share. Thus, the sourcing and environmental accounting of electricity from RES along the supply chain might gain in relevance. Consequently, also consistent residual mix application, in order to avoid double counting, is likely to gain relevance.

Since a consistent application of both the location-based or the market-based method can effectively avoid double counting, the advantages and disadvantages of both methods for incentivizing a real-world reduction in electricity-related environmental impacts need to be critically discussed.

A benefit of the exclusive application of the location-based method is that it representatively evaluates the environmental impacts of the physically consumed electricity. Since it is not possible to reduce electricity-related emissions via the acquisition of electricity from specific energy sources, such as RES, the location-based method can lead to an increased incentive for energy efficiency measures for entities that wish to reduce their environmental impacts (Brander et al. 2018). Furthermore, if the location-based method is applied with high spatial and temporal granularity, it might also incentivize load management optimizations to consume grid electricity when RES are available and thus emission factors are low (Stoll et al. 2014). Even though there are some discussions on EACs with high temporal resolution (Kuronen 2021; Pototschnig and Conti 2021), the market-based approach currently does not offer this potential.

By taking away the possibility to actively source and environmentally account for electricity from RES, a purely location-based electricity accounting system creates strong regional differences in the accounting of electricity-related environmental impacts. However, these differences have mostly not been influenced by the electricity-consuming entities and could thus be seen as unjustified. Furthermore, the exclusive application of the location-based method takes away an incentive to influence grid electricity generation by choosing a specific electricity source, such as RES.

The contribution of the market-based method and accompanying EAC systems to emission reductions and the expansion of RES is critically discussed in the literature. Central discussion points are missing incentives for the expansion of electricity from RES, due to low EAC prices and reduced necessity for energy efficiency measures (Bjørn et al. 2022; Brander et al. 2018; Hulshof et al. 2019). The supporting information (Sect. 1) contains a summary of these discussions. The avoidance of double counting could increase demand for contractual agreements, such as EACs. Reasons for this possible demand increase can be found both on a country level and in corporate supply chains. Currently, the interest in EACs in countries like Norway with very high shares of electricity from RES is rather low (Sustainability Impact Metrics 2022), since consumers assume that electricity comes from RES regardless of EACs. The demand for contractual agreements could increase if location-based accounting and emission reduction target setting for corporations would not be possible. On a supply chain level, demand for EACs could increase, since final producers might put pressure on their suppliers to purchase electricity from RES in order to avoid having to include products with residual mixes as electricity input in their LCA or GHG accounting. An increase in demand might lead to higher prices for such contractual agreements. However, a price elevation, sufficient to incentivize the construction and operation of additional RES-based power plants, is by no means certain. Thus, an agreement on stricter quality criteria for accountable electricity from RES might be necessary, to ensure the contribution of the market-based method to the energy transition.

Both the location-based and market-based method offer the potential for contributing to a transition towards a decarbonized electricity system. However, it is questionable if these potentials are realized, if both methods are applied in parallel. Thus, a consistent application of one electricity accounting method throughout the whole life cycle should be mandatory. With regards to which method should be used, one option would be to always demand LCA and GHG accounting calculations according to both location-based and market-based method. This would also need to include reduction targets of environmental impacts according to both methods. Another option could be to agree on one method for specific use cases and questions, for example, corporate GHG reductions according to the SBTi.

The implications of this paper go beyond the electricity sector, since the avoidance of double counting is important in all cases where different types of energy or materials are mingled before consumption. According to the GHG protocol, “steam, heat, and cooling energy systems may also use contractual instruments to convey attributes and claims” (WRI & WBCSD 2015). Also for gas networks, avoiding double counting is likely to become more and more important, due to the rising relevance of green hydrogen and biogases (Abad and Dodds 2020). In terms of materials, the necessity for double counting free accounting methods arises due to very different environmental impacts associated with recycled materials or different production routes for one material, as in the case of steel (Suer et al. 2022).

5 Conclusion

Grid electricity consumption entails a significant contribution to the LCA and GHG accounting of most organizations and products. Hence, double counting of electricity from specific energy sources, such as RES, can lead to under- or overestimations of corresponding environmental impacts. This paper analyses environmental accounting specifications for electricity-related environmental impacts in LCA and GHG accounting in frequently applied standards. Thereby, it reveals challenges of double counting electricity from specific sources, such as RES.

The challenges mainly exist due to a parallel application of the market-based and location-based electricity accounting method. Exclusively claiming the consumption of grid electricity from specific energy sources, such as RES, is only possible without double counting, if residual electricity mixes are consistently used in every electricity-consuming step, for which no valid market-based contractual agreements are obtained. Improper residual grid mix calculation and application can lead to under- or overestimations of environmental impacts related to electricity consumption. In turn, location-based average grid electricity emission factors can only be applied, if no entity can exclusively claim the consumption of grid electricity from specific energy sources. Thus, there is a need to enable and use consistent electricity accounting rules in LCA and GHG accounting.

Data availability

The authors declare that all data supporting the findings of this study are available as stated within this published article (and its Supporting Information).

References

Abad AV, Dodds PE (2020) Green hydrogen characterisation initiatives: definitions, standards, guarantees of origin, and challenges. Energy Policy 138:111300. https://doi.org/10.1016/j.enpol.2020.111300

Agez M, Majeau-Bettez G, Margni M, Strømman AH, Samson R (2020) Lifting the veil on the correction of double counting incidents in hybrid life cycle assessment. J Ind Ecol 24:517–533. https://doi.org/10.1111/jiec.12945

AIB (2022) European residual mixes results of the calculation of residual mixes for the calendar year 2020 Association of Issuing Bodies. https://www.aib-net.org/facts/european-residual-mix

Baumgärtner N, Delorme R, Hennen M, Bardow A (2019) Design of low-carbon utility systems: exploiting time-dependent grid emissions for climate-friendly demand-side management. Appl Energy 247:755–765. https://doi.org/10.1016/j.apenergy.2019.04.029

Betten T, Shammugam S, Graf R (2020) Adjustment of the life cycle inventory in life cycle assessment for the flexible integration into energy systems analysis. Energies 13:4437. https://doi.org/10.3390/en13174437

Bjørn A, Lloyd SM, Brander M, Matthews HD (2022) Renewable energy certificates threaten the integrity of corporate science-based targets. Nat Clim Chang 12:539–546. https://doi.org/10.1038/s41558-022-01379-5

Brander M, Gillenwater M, Ascui F (2018) Creative accounting: a critical perspective on the market-based method for reporting purchased electricity (scope 2) emissions. Energy Policy 112:29–33. https://doi.org/10.1016/j.enpol.2017.09.051

Bricaud C (2022) What is an energy attribute certificate – EAC? Bricaud, Cyril. https://www.ecohz.com/wiki/what-is-an-energy-attribute-certificate-eac. Accessed 30 Nov 2022

EEG (2021) Gesetz für den Ausbau erneuerbarer Energien (Erneuerbare-Energien-Gesetz - EEG 2021). Bundesministerium für Wirtschaft und Klimaschutz. https://www.clearingstelle-eeg-kwkg.de/eeg2021

EU (2018) DIRECTIVE (EU) 2018/ 2001 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL - of 11 December 2018 - on the promotion of the use of energy from renewable sources (recast). European Union. Official Journal of the European Union. https://eur-lex.europa.eu/legalcontent/EN/TXT/?uri=uriserv:OJ.L_.2018.328.01.0082.01.ENG

European Commission (2021) Comission recommendation on the use of the environmental footprint methods to measure and communicate the life cycle environmental performance of products and organisations. European Commission. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32021H2279

Finkbeiner M, Bach V (2021) Life cycle assessment of decarbonization options—towards scientifically robust carbon neutrality. Int J Life Cycle Assess 26:635–639. https://doi.org/10.1007/s11367-021-01902-4

Gkarakis K, Dagoumas A (2015) Assessment of the implementation of guarantees of origin (GOs) in Europe. In: Németh B, Raisz D (eds) Deregulated electricity market issues in South Eastern Europe, vol 3. Trivent Publishing. https://doi.org/10.22618/TP.EI.20163.389011

Hauser E, Heib S, Hildebrand J, Rau I, Weber A, Welling J, Güldenberg J, Maaß C, Mundt J, Werner R, Schudak A, Wallbott T (2019) Marktanalyse Ökostrom II. German Environmental Agency. https://www.umweltbundesamt.de/publikationen/marktanalyse-oekostrom-i

Hulshof D, Jepma C, Mulder M (2019) Performance of markets for European renewable energy certificates. Energy Policy 128:697–710. https://doi.org/10.1016/j.enpol.2019.01.051

IEA (2021) International Energy Agency; Global Energy & CO2 Status Report 2019. https://www.iea.org/reports/global-energy-co2-status-report-2019/emissions. Accessed 6 Oct 2021

ISO (2006a) Environmental management – life cycle assessment – principles and framework (ISO 14040:2006). International Organization for Standardization. https://www.iso.org/standard/37456.html

ISO (2006b) Environmental management – life cycle assessment – requirements and guidelines (ISO 14044:2006). International Organization for Standardization.. https://www.iso.org/standard/38498.html

ISO (2019a) Part 1: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals (ISO 14064-1:2018). International Organization for Standardization. https://www.iso.org/standard/66453.html

ISO (2019b) Greenhouse gases – Carbon footprint of products – Requirements and guidelines for quantification (ISO 14067:2018). International Organization for Standardization. https://www.iso.org/standard/71206.html

Jaeger FA, Sonntag C, Hartung J, Müller K (2022) Dynamic and localized LCA information supports the transition of complex systems to a more sustainable manner such as energy and transport systems. In: Klos ZS, Kalkowska J, Kasprzak J (eds) Towards a sustainable future - life cycle management. Springer International Publishing, Cham, pp 61–72

Klimscheffskij M, van Craenenbroeck T, Lehtovaara M, Lescot D, Tschernutter A, Raimundo C, Seebach D, Timpe C (2015) Residual mix calculation at the heart of reliable electricity disclosure in Europe—a case study on the effect of the RE-DISS project. Energies 8:4667–4696. https://doi.org/10.3390/en8064667

Krebs and Frischknecht (2021) Life cycle assessment of GO based electricity mixes of European countries 2018. https://treeze.ch/fileadmin/user_upload/downloads/Publications/Case_Studies/Energy//726_LCA_GOelectricityMixes_EuropeanCountries_v1.01.pdf

Kuronen A (2021) Tracking of energy origin. https://grexel.com/tracking-of-energy-origin/. Accessed 15 Sep 2021

Kuronen A, Lehtovaara M, Jakobsson S (2020) Issuance based residual mix calculation methodology. https://www.aibnet.org/facts/european-residual-mix. https://www.aib-net.org/sites/default/files/assets/facts/residualmix/2019/RM%20EAM%20IB%20Calculation%20Methodology%20V1_1.pdf

Lenzen M (2008) Double-counting in life cycle calculations. J Ind Ecol 12:583–599. https://doi.org/10.1111/j.1530-9290.2008.00067.x

Lewandowska A, Kurczewski P, Joachimiak-Lechman K, Zabłocki M (2021) Environmental life cycle assessment of refrigerator modelled with application of various electricity mixes and technologies. Energies 14:5350. https://doi.org/10.3390/en14175350

Olindo R, Schmitt N, Vogtländer J (2021) Life cycle assessments on battery electric vehicles and electrolytic hydrogen: the need for calculation rules and better databases on electricity. Sustainability 13:5250. https://doi.org/10.3390/su13095250

Pototschnig A, Conti I (2021) Upgrading guarantees of origin to promote the achievement of the EU renewable energy target at least cost. https://fsr.eui.eu/publications/?handle=1814/69776

RIS (2013) Bundesrecht konsolidiert: Gesamte Rechtsvorschrift für Stromkennzeichnungsverordnung. Fassung Vom 21(10):2021

Ryan NA, Johnson JX, Keoleian GA (2016) Comparative assessment of models and methods to calculate grid electricity emissions. Environ Sci Technol 50:8937–8953. https://doi.org/10.1021/acs.est.5b05216

SBTi (2021) SBTi criteria and recommendations. Science Based Targets initiative. https://sciencebasedtargets.org/resources/files/SBTi-criteria.pdf, https://sciencebasedtargets.org/resources/

Schneider L, Kollmuss A, Lazarus M (2015) Addressing the risk of double counting emission reductions under the UNFCCC. Clim Change 131:473–486. https://doi.org/10.1007/s10584-015-1398-y

Siddik MAB, Chini CM, Marston L (2020) Water and carbon footprints of electricity are sensitive to geographical attribution methods. Environ Sci Technol 54:7533–7541. https://doi.org/10.1021/acs.est.0c00176

Sphera Solution GmBH (2022) GaBi software system and database for life cycle engineering 1992–2022

Stoll P, Brandt N, Nordström L (2014) Including dynamic CO2 intensity with demand response. Energy Policy 65:490–500. https://doi.org/10.1016/j.enpol.2013.10.044

Suer J, Traverso M, Ahrenhold F (2022) Sustainable transition of the primary steel production: carbon footprint studies of hot-rolled coil according to ISO 14067. E3S Web Conf. 349:7004. https://doi.org/10.1051/e3sconf/202234907004

Sustainability Impact Metrics (2022) GOs and RECs in LCA - sustainability impact metrics. Sustainability Impact Metrics. https://www.ecocostsvalue.com/lca/gos-and-recs-in-lca/. Accessed 17 Nov 2022

Together for Sustainability (2022) The product carbon footprint guideline for the chemical industry. Together for Sustainability. https://www.tfsinitiative.com/app/uploads/2023/02/TfS_PCF_guidelines_2022-English.pdf

Weber CL, Jiaramillo P, Marriott J, Samaras C (2010) Life cycle assessment and grid electricity: what do we know and what can we know? Environ Sci Technol 44:1895–1901. https://doi.org/10.1021/es9017909

Wernet G, Bauer C, Steubing B, Reinhard J, Moreno-Ruiz E, Weidema B (2016) The ecoinvent database version 3 (part I): overview and methodology. Int J Life Cycle Assess 21:1218–1230. https://doi.org/10.1007/s11367-016-1087-8

WRI and WBCSD (2004) The greenhouse gas protocol - a corporate accounting and reporting standard (Revised edition). World Business Council for Sustainable Development and World Resources Institute. https://ghgprotocol.org/corporate-standard#supporting-documents

WRI and WBCSD (2011a) Greenhouse gas protocol - product life cycle accounting and reporting standard. World Business Council for Sustainable Development and World Resources Institute. https://ghgprotocol.org/product-standard

WRI and WBCSD (2011b) Greenhouse gas protocol - technical guidance for calculating scope 3 emission. World Business Council for Sustainable Development and World Resources Institute. https://ghgprotocol.org/scope-3-technical-calculation-guidance

WRI and WBCSD (2015) GHG protocol scope 2 guidance - an amendment to the GHG Protocol Corporate Standard. https://ghgprotocol.org/scope_2_guidance

Acknowledgements

We gratefully acknowledge Daria Blizniukova, Isabel Wolf and János Bánk for valuable scientific discussions.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interests

The authors declare no competing interests.

Additional information

Communicated by Shabbir Gheewala.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Holzapfel, P., Bach, V. & Finkbeiner, M. Electricity accounting in life cycle assessment: the challenge of double counting. Int J Life Cycle Assess 28, 771–787 (2023). https://doi.org/10.1007/s11367-023-02158-w

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11367-023-02158-w