Abstract

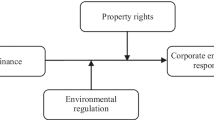

In the context of green finance, whether listed companies in heavily polluting industries can convert the external pressure of environmental information disclosure into internal motivation is critical to achieving environmental governance goals. This paper selects 946 listed companies of 16 heavily polluting industries in the Shanghai and Shenzhen stock markets as samples to explore whether environmental information disclosure can help companies increase bank credit support and reduce debt financing costs to transform their external pressures into internal motivation. The empirical results show that there is a significant positive correlation between environmental information disclosure and bank credit decisions. From the perspective of financing scale, heavily polluting companies have the inherent motivation to disclose environmental information actively and proactively to obtain more credit support. There is no significant relationship between the corporate debt financing cost and environmental information disclosure. This paper puts forward some critical policy suggestions for government decision makers, heavily polluting enterprises, and financial institutions.

Similar content being viewed by others

Data availability

The data used to support the findings of this study are available from the corresponding author upon request.

Change history

25 February 2022

Ruili 2021 was removed as it was a duplicate of the reference Wang 2021.

References

Aggarwal R, Dow S (2012) Corporate governance and business strategies for climate change and environmental mitigation. Eur J Financ 18:311–331

Akerlof GA (1970) The market for “lemons”: quality uncertainty and the market mechanism. Q J Econ 84:488–500

Alvis KL (2013) Do declines in bank health affect borrowers’ voluntary disclosures? Evidence from international propagation of banking shocks. J Account Res 52:541–581

Bergh DD, Connelly BL Jr, Ketchen DJ Jr, Lu MS (2014) Signaling theory and equilibrium in strategic management research: an assessment and a research agenda. J Manag Stud 51:1334–1360

Biais B, Foucault T, Moinas S (2015) Equilibrium fast trading. J Financ Econ 116:292–313

Bradley SW, Shepherd DA, Wiklund J (2011) The importance of slack for new organizations facing ‘tough’ environments. J Manag Stud 48:1071–1097

Brammer S, Millington A (2008) Does it pay to be different? An analysis of the relationship between corporate social and financial performance. Strateg Manag J 29:1325–1343

Brooks C, Oikonomou I (2018) The effects of environmental, social and governance disclosures and performance on firm value: a review of the literature in accounting and finance. Br Account Rev 50:1–15

Buysse K, Verbeke A (2003) Proactive environmental strategies: a stakeholder management perspective. Strateg Manag J 24:453–470

Certo ST (2003) Influencing initial public offering investors with prestige: signaling with board structures. Acad Manag Rev 28:432–446

Connelly BL, Certo ST, Ireland RD, Reutzel CR (2011) Signaling theory: a review and assessment. J Manag 37:39–67

Cooper SA, Raman KK, Yin J (2018) Halo effect or fallen angel effect? Firm value consequences of greenhouse gas emissions and reputation for corporate social responsibility. J Account Public Policy 37:226–240

Cui J, Jo H, Na H (2018) Does corporate social responsibility affect information asymmetry? J Bus Ethics 148:549–572

Dejean F, Martinez I (2009) Environmental disclosure and the cost of equity: the French case. Account Eur 6:57–80

Dell'Ariccia G, Laeven L, Suarez GA (2017) Bank leverage and monetary policy’s risk-taking channel: evidence from the United States. J Financ 72:613–654

Eichholtz P, Holtermans R, Kok N, Yonder E (2019) Environmental performance and the cost of debt: evidence from commercial mortgages and REIT bonds. J Bank Financ 102:19–32

El-Kassar A, Singh SK (2019) Green innovation and organizational performance: the influence of big data and the moderating role of management commitment and HR practices. Technol Forecast Soc Changes 144:483–498

Fonseka M, Rajapakse T, Richardson G (2019) The effect of environmental information disclosure and energy product type on the cost of debt: evidence from energy firms in China. Pac Basin Financ J 54:159–182

Franco F, Urcan O, Vasvari FP (2015) Corporate diversification and the cost of debt: the role of segment disclosures. Account Rev 91:1139–1165

Gao H, Zhu H, Meng F (2018) Does the quality of environmental information disclosure affect the cost of debt financing? Empirical evidence from listed companies in environmentally sensitive industries in China. J Nanjing Audit Univ 15:20–28

Jiang C, Zhang F, Wu C (2021) Environmental information disclosure, political connections and innovation in high-polluting enterprises. Sci Total Environ 764:144248

Jin Y, Gao X, Wang M (2021) The financing efficiency of listed energy conservation and environmental protection firms: evidence and implications for green finance in China. Energy Policy 153:112254

Kreps DM, Paul M, John R, Robert W (1982) Rational cooperation in the finitely repeated prisoners’ dilemma. J Econ Theory 27:245–252

Li W, Zhang Y, Zheng M et al (2019) Research on green governance and evaluation of Chinese listed companies. Manag World 35:126–133

Liu S, Liu C, Yang M (2021) The effects of national environmental information disclosure program on the upgradation of regional industrial structure: evidence from 286 prefecture-level cities in China. Struct Chang Econ Dyn 58:556–561

Luo W, Guo X, Zhong S, Wang J (2019) Environmental information disclosure quality, media attention and debt financing costs: evidence from Chinese heavy polluting listed companies. J Clean Prod 231:268–277

Lv M, Xu G, Shen Y et al (2018) Heterogeneous debt governance, contract incompleteness and environmental information disclosure. Account Res 5:67–74

Meng X (2010) Interactive relation between corporate social responsibility disclosure and the cost of capital: an analysis framework based on asymmetric information. Account Res 22:25–29

Minnis M (2011) The value of financial statement verification in debt financing: evidence from Finland. Int J Audit 2:88–108

Ni J, Kong L (2016) Environmental information disclosure, bank credit decisions and debt financing costs—empirical evidence from China’s Shanghai and Shenzhen A-share listed companies in heavily polluting industries. Econ Rev 1:147–156

Niu H, Zang X, Zhang P (2020) Institutional changes and effect evaluation of China’s green finance policy: taking the empirical research of green credit as an example. Manag Rev 32:3–12

Qiu Y, Shaukat A, Tharyan R (2016) Environmental and social disclosures: link with corporate financial performance. Br Account Rev 48:102–116

Rosa FL, Liberatore G, Mazzi F, Terzani S (2018) The impact of corporate social performance on the cost of debt and access to debt financing for listed European non-financial firms. Eur Manag J 36:519–529

Roychowdhury S, Shroff N, Verdi RS (2019) The effects of financial reporting and disclosure on corporate investment: a review. J Account Econ 68:101246

Schiemann F, Sakhel A (2019) Carbon disclosure, contextual factors, and information asymmetry: the case of physical risk reporting. Eur Account Rev 28:791–818

Shen H, Ma Z (2014) Regional economic development pressure, corporate environmental performance and debt financing. Financ Res 2:153–166

Spence M (2002) Signaling in retrospect and the informational structure of markets. Am Econ Rev 92:434–459

Strausz R (2017) A theory of crowdfunding: a mechanism design approach with demand uncertainty and moral hazard. Am Econ Rev 107:1430–1476

Tang J, Li P (2008) An empirical study on environmental information disclosure: evidences from the chemical industry in China’s securities market. China Popul Res Environ 5:112–117

Tzouvanas P, Kizys R, Chatziantoniou I, Sagitova R (2020) Environmental disclosure and idiosyncratic risk in the European manufacturing sector. Energy Econ 87:104715

Wan M, Wasiuzzaman S (2021) Environmental, social and governance (ESG) disclosure, competitive advantage and performance of firms in Malaysia. Clean Environ Syst 2:100015

Wang R (2021) Management governance, environmental accounting information disclosure and financing constraints. Accounting Newsletter 3:73–76

Wang X, Xu X, Wang C (2013) Public pressure, social reputation, internal governance and corporate environmental information disclosure: evidence from listed companies in China’s manufacturing industry. Nankai Manag Rev 2:82–91

Wu MW, Shen CH (2013) Corporate social responsibility in the banking industry: motives and financial performance. J Bank Financ 37:3529–3547

Xing C, Zhang Y, Tripe D (2021) Green credit policy and corporate access to bank loans in China: the role of environmental disclosure and green innovation. Int Rev Financ Anal 12:101838

Zhang C (2017) Political connections and corporate environmental responsibility: adopting or escaping? Energy Econ 68:539–547

Zhang Z, Zhang C, Cao D (2019) Is the certification of enterprise environmental management system effective? Nankai Manag Rev 22:123–134

Zhu N, Lai X (2020) Research on China’s green credit efficiency evaluation and improvement path. Financ Superv Res:41–58

Zhu W, Sun Y, Tang Q (2019) Substantial or selective disclosure: the impact of corporate environmental performance on the quality of environmental information disclosure. Account Res 3:10–17

Acknowledgements

The authors would like to express their sincere gratitude to the anonymous reviewers and the editors for their truly valuable comments.

Funding

This work was supported by the National Natural Science Foundation of China (No. 71704098, 72001191, 72003110), Key Research Project of Financial Application in Shandong Province (No. 2021-JRZZ-25), and Key Project of Philosophy and Social Science Foundation of Jinan City (No. JNSK21B18).

Author information

Authors and Affiliations

Contributions

Mo Du: conceptualization, writing—original draft, writing—review and editing. Shanglei Chai: funding acquisition, formal analysis, writing—original draft. Wei Wei: funding acquisition, writing—review and editing. Shuqi Wang: methodology. Zhilong Li: data curation.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Conflict of interest

The authors declare no competing interests.

Additional information

Responsible Editor: Nicholas Apergis

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Du, M., Chai, S., Wei, W. et al. Will environmental information disclosure affect bank credit decisions and corporate debt financing costs? Evidence from China’s heavily polluting industries. Environ Sci Pollut Res 29, 47661–47672 (2022). https://doi.org/10.1007/s11356-022-19229-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-022-19229-4