Abstract

This study examines the nonlinear dependence between carbon market and stock market in China under normal and extreme market conditions by employing two novel nonlinear approaches, namely, quantile coherency and causality-in-quantiles methods. Given our results on the overall and sector level of stock market, we find that there is a negative dependence between the two markets under bearish and normal market states in the short- and medium-term respectively, while the dependence becomes positive under bearish and bullish market states in the long-term. Furthermore, we also prove that the Granger causality from carbon market to stock market exists. However, no evident impacts from stock market to carbon market have been found. Additionally, at sector stock market, we discover heterogeneity across market conditions. And emission-intensive sector stock indices are more affected by carbon prices.

Similar content being viewed by others

Data Availability

The datasets used and/or analyzed during the current study are available from the corresponding author on reasonable request.

Notes

This data is available at https://www.edf.org/climate/report-progress-chinas-carbon-markets.

Following Chang and Zhang (2018), this study uses the prices of previous trading days to fill in the missing values in carbon market. In addition, we also try to solve this problem by deleting missing values and find that this does not change our main conclusion. The space is limited, and relevant results are available on request.

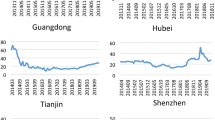

The sample stocks of CSI300 cover about 70% of the market value of the Shanghai and Shenzhen markets, which can reflect the overall trend of China’s A-share market. In addition, we also use the Shanghai Composite Index and Shenzhen Component Index to conduct robustness tests and find that the results are not significantly different. The relevant results are not provided due to the finite space, but they are available if requested.

The results are not provided due to the finite space, but they are available if requested.

References

Badeeb RA, Lean HH (2018) Asymmetric impact of oil price on Islamic sectoral stocks. Energy Econ 71:128–139

Balcılar M, Demirer R, Hammoudeh S, Nguyen DK (2016) Risk spillovers across the energy and carbon markets and hedging strategies for carbon risk. Energy Econ 54:159–172

Baruník J, Kley T (2019) Quantile coherency: a general measure for dependence between cyclical economic variables. Economet J 22(2):131–152

Busch T, Hoffmann VH (2007) Emerging carbon constraints for corporate risk management. Ecol Econ 62(3–4):518–528

Chang K, Zhang C (2018) Asymmetric dependence structure between emissions allowances and wholesale diesel/gasoline prices in emerging China’s emissions trading scheme pilots. Energy 164:124–136

Cong R, Lo AY (2017) Emission trading and carbon market performance in Shenzhen, China. Appl Energy 193:414–425

Daskalakis G, Psychoyios D, Markellos RN (2009) Modeling co2 emission allowance prices and derivatives: evidence from the European trading scheme. J Bank Finance 33(7):1230–1241

Dong K, Sun R, Dong X (2018) CO2 emissions, natural gas and renewables, economic growth: assessing the evidence from China. Sci Total Environ 640:293–302

Han M, Ding L, Zhao X, Kang W (2019) Forecasting carbon prices in the Shenzhen market, China: the role of mixed-frequency factors. Energy 171:69–76

Jena SK, Tiwari AK, Hammoudeh S, Roubaud D (2019) Distributional predictability between commodity spot and futures: evidence from nonparametric causality-in-quantiles tests. Energy Econ 78:615–628

Jeong K, Härdle WK, & Song S (2012) A consistent nonparametric test for causality in quantile. Econometric Theory, 861–887

Ji Q, Xia T, Liu F, Xu JH (2019) The information spillover between carbon price and power sector returns: evidence from the major European electricity companies. J Clean Prod 208:1178–1187

Jiang Y, Feng Q, Mo B, Nie H (2020) Visiting the effects of oil price shocks on exchange rates: quantile-on-quantile and causality-in-quantiles approaches. North Am J Econ Finance 52:101161

Jiang Y, Lei YL, Yang YZ, Wang F (2018) Factors affecting the pilot trading market of carbon emissions in China. Pet Sci 15(2):412–420

Jiménez-Rodríguez R (2019) What happens to the relationship between EU allowances prices and stock market indices in Europe? Energy Econ 81:13–24

Kumar S, Managi S, Matsuda A (2012) Stock prices of clean energy firms, oil and carbon markets: A vector autoregressive analysis. Energy Econ 34(1):215–226

Lin B, Jia Z (2019) What will China’s carbon emission trading market affect with only electricity sector involvement? A CGE based study. Energy Econ 78:301–311

Liu L, Chen C, Zhao Y, Zhao E (2015) China’s carbon-emissions trading: overview, challenges and future. Renew Sustain Energy Rev 49:254–266

Liu X, Jin Z (2020) An analysis of the interactions between electricity, fossil fuel and carbon market prices in Guangdong, China. Energy Sustain Dev 55:82–94

Liu X, Zhou X, Zhu B, Wang P (2020) Measuring the efficiency of China’s carbon market: a comparison between efficient and fractal market hypotheses. J Clean Prod 271:122885

Lyu J, Cao M, Wu K, Li H (2020) Price volatility in the carbon market in China. J Clean Prod 255:120171

Maghyereh A, Abdoh H (2020) Tail dependence between Bitcoin and financial assets: evidence from a quantile cross-spectral approach. Int Rev Financial Anal 71:101545

Nishiyama Y, Hitomi K, Kawasaki Y, Jeong K (2011) A consistent nonparametric test for nonlinear causality—specification in time series regression. J Econom 165(1):112–127

Oberndorfer U (2009) EU emission allowances and the stock market: evidence from the electricity industry. Ecol Econ 68(4):1116–1126

Oestreich AM, Tsiakas I (2015) Carbon emissions and stock returns: evidence from the EU Emissions Trading Scheme. J Bank Finance 58:294–308

Raggad B (2018) Carbon dioxide emissions, economic growth, energy use, and urbanization in Saudi Arabia: evidence from the ARDL approach and impulse saturation break tests. Environ Sci Pollut Res 25(15):14882–14898

Shin, Y., Yu, B., Greenwood-Nimmo, M., 2014. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. Festschrift in Honor of Peter Schmidt. Springer, New York, NY, pp. 281–314.

Sun L, Xiang M, Shen Q (2020) A comparative study on the volatility of EU and China’s carbon emission permits trading markets. Phys A: Stat Mech Appl 560:125037

Tan X, Sirichand K, Vivian A, Wang X (2020) How connected is the carbon market to energy and financial markets? A systematic analysis of spillovers and dynamics. Energy Econ 90:104870

Tian Y, Akimov A, Roca E, Wong V (2016) Does the carbon market help or hurt the stock price of electricity companies? Further evidence from the European context. J Clean Prod 112:1619–1626

Tiwari AK, Trabelsi N, Alqahtani F, Bachmeier L (2019) Modelling systemic risk and dependence structure between the prices of crude oil and exchange rates in BRICS economies: evidence using quantile coherency and NGCoVaR approaches. Energy Econ 81:1011–1028

Wang X, Wang Y (2019) Volatility spillovers between crude oil and Chinese sectoral equity markets: Evidence from a frequency dynamics perspective. Energy Econ 80:995–1009

Wen F, He Z, Dai Z, Yang X (2014) Characteristics of investors’ risk preference for stock markets. Econom Comput Econom Cybernet Stud Res 48:235–254

Wen F, Wu N, Gong X (2020) China’s carbon emissions trading and stock returns. Energy Econ 86:104627

Wen, F., Zhao, L., He, S., Yang, G. (2020b) Asymmetric relationship between carbon emission trading market and stock market: evidences from China. Energy Econ, 104850.

Zeng S, Nan X, Liu C, Chen J (2017) The response of the Beijing carbon emissions allowance price (BJC) to macroeconomic and energy price indices. Energy Policy 106:111–121

Zhang L, Li Y, Jia Z (2018) Impact of carbon allowance allocation on power industry in China’s carbon trading market: computable general equilibrium-based analysis. Appl Energy 229:814–827

Zhao L, Wen F, Wang X (2020) Interaction among China carbon emission trading markets: nonlinear Granger causality and time-varying effect. Energy Econ 91:104901

Zhao XG, Wu L, Li A (2017) Research on the efficiency of carbon trading market in China. Renew Sustain Energy Rev 79:1–8

Zhu B, Huang L, Yuan L, Ye S, Wang P (2020) Exploring the risk spillover effects between carbon market and electricity market: a bidimensional empirical mode decomposition based conditional value at risk approach. Int Rev Econ Financ 67:163–175

Funding

This work is supported by the National Natural Science Foundation of PRC (71971098, 72001090).

Author information

Authors and Affiliations

Contributions

Jiang Yonghong: data curation, formal analysis, and investigation. Liu Lu: data curation, formal analysis, investigation, methodology, project administration, writing, review, and editing, software. Mu Jinqi: conceptualization, formal analysis, writing, review, and editing.

Corresponding author

Ethics declarations

Ethics approval and consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Nicholas Apergis

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Jiang, Y., Liu, L. & Mu, J. Nonlinear dependence between China’s carbon market and stock market: new evidence from quantile coherency and causality-in-quantiles. Environ Sci Pollut Res 29, 46064–46076 (2022). https://doi.org/10.1007/s11356-022-19179-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-022-19179-x