Abstract

I examine developments in the application of performance-based regulation (PBR) to electricity distribution and transmission in the United States. Applications of comprehensive PBR to electricity distribution had been slow to diffuse in the U.S. prior to roughly 2000. PBR mechanisms are now being applied more frequently to electricity distribution, which reflects the changing structure of the electric power industry and the increasing obligations that are being placed on electric distribution companies. The new obligations are a consequence primarily of aggressive targets for decarbonizing the electricity sector in nearly half the states and the goal of using “clean” electricity to electrify transportation, buildings, and other sectors. PBR should be viewed as a set of “building blocks” that can be adopted in various combinations and should recognize that PBR and traditional cost-of-service regulation (COSR) are properly viewed as complements rather than substitutes. Recent reforms in the regulation of distribution companies in Great Britain—“RIIO”—have been influential in the U.S. The main reforms contained in RIIO are discussed. There has been essentially no application of PBR by the Federal Energy Regulatory Commission (FERC) to owners of transmission assets or to independent transmission operators. FERC has applied targeted incentives to encourage investment in transmission facilities and membership in independent system operator organizations. However, the regulation of transmission rates relies primarily on COSR in the form of formula rates and has poor incentive properties. Regulation of independent system operators is a challenge because they are non-profit organizations with no equity to put at risk. Reforms here are suggested.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

“All Regulation is Incentive Regulation”.Footnote 1

“…it would be simpleminded to make a strong distinction between [cost of service] regulations and [incentive] regulations… the contrast between the two modes is mostly one of emphasis.”Footnote 2

“There is a fundamental evolution taking place in the way electricity is being produced and consumed in Massachusetts. This evolution has been driven, in large part, by a number of legislative and administration policy initiatives to address climate change and to foster a clean energy economy…”.Footnote 3

1 Introduction

There is by now an extensive and mature theoretical literature on incentive regulation of legal monopolies (e.g., Armstrong & Sappington, 2004, 2007; Sappington, 2005; Laffont & Tirole, 1993). At least some of the teachings of this literature—especially simple price-cap or indexed price regulation (Laffont & Tirole, 1993, p. 17)—have guided reforms to traditional cost-of-service regulatory (COSR) practices in several U.S. industries; regulated telephone service at both the federal and state levels is the most widely cited (Lowry and Kaufman, 2002, pp. 408–409; Sappington et al., 2001; Sappington & Weisman, 2010) (see their Table 1).

Incentive regulation mechanisms have been applied for many years to the regulation of electric utilities in countries other than the U.S., including Great Britain, Chile, Argentina, Japan, New Zealand, Australia, and Canada. In an earlier paper (Joskow, 2014, p. 310),Footnote 4 I concluded “Formal comprehensive incentive regulation mechanisms have been slow to spread in the U.S. electric power industry [reference omitted], though rate freezes, rate case moratoria, and other alternative regulatory mechanisms have been adopted in many states, sometimes informally, since the mid-1990s.”

The early applications of incentive regulation principles in the electric power sector tended to be very partial (e.g., focused on the performance of generating plants, Joskow & Schmalensee, 1986, p. 39), quasi-automatic adjustment mechanisms in response to high rates of inflation in the 1970s and early 1980s, or were temporary de facto price cap mechanisms (e.g. short-term rate freezes) that emerged as settlementsFootnote 5 of rate cases—often in connection with vertical and horizontal restructuring, stranded cost recovery, and mergers, especially in the late 1990s and early 2000s as industry restructuring occurred. Administrative convenience rather than clearly articulated performance goals drove many of these experiments.

More recently—especially since around 2015—the situation with regard to the applications of incentive regulation mechanisms to electric distribution companies in the U.S. has changed considerably: Incentive regulation mechanisms of some type have now been introduced into the electricity distribution regulatory process in a majority of U.S. states. Comprehensive incentive regulation mechanisms have been or are now being introduced or evaluated in about a dozen states.

There are a few things that are worth noting about this recent trend: First, these initiatives are never called “incentive regulation” by regulators and policy makers in the U.S. The policy phrases used routinely now are “performance-based regulation” (PBR) or “alternative regulatory mechanisms (ARM).” I will use the term PBR in the rest of this article. I have been told by a few regulators that the term “incentive regulation” sounds like a potential giveaway to utilities, while “performance-based regulation” sounds like the focus is on holding the utilities’ feet to the fire. Perhaps this should remind us that language matters to successfully apply theoretical results to public policy; but the advances in PBR regulation of electric distribution utilities in the U.S. reflects more than just politically appealing language.

Second, I am sorry to conclude that the extensive theoretical literature and the details of optimal regulatory mechanism design in different contexts that has emerged from that literature has left very few clearly visible footprints in the policy discussion and in the design of PBR mechanisms in practice in the U.S. I have reviewed perhaps 100 regulatory reports, regulatory commission orders, advisory and consulting firm educational materials that have been provided to policymakers, and media discussions of PBR regulation in the course of preparing this article. Discussions of important concepts—such as imperfect and asymmetric information, adverse selection, managerial effort and moral hazard, rent extraction/efficiency tradeoffs, and the use of incentive-compatible menus—are rarely if ever mentioned. Advisory and consulting firm reports, presentations, and general guidance—which involves organizations such as the Regulatory Assistance Project (RAP), Rocky Mountain Institute (RMI), and U.S. national labs, especially the National Renewable Energy Laboratory (NREL) and the Lawrence Berkeley National Laboratory (LBNL or LBL)—have played a primary role in educating policy makers and promoting PBR.

These reports have few citations to the key papers and books in the academic literature. The reports rely on fairly simple incentive and disincentive concepts that are applied in practical ways to the nuts and bolts of the regulation of (primarily) electricity distribution utilities. They also draw on the experiences in other countries and in various U.S. states—especially the recent regulatory reforms in Great Britain—as those experiences related to the regulation of electric distribution companies.

Nevertheless, several of the more comprehensive mechanisms that have been introduced to regulate electricity distribution in the U.S. have features that can be readily found in the theoretical incentive regulation literature even if the relationships between the theory and applications are not specified clearly.

Simple price-cap mechanisms alone (Laffont & Tirole, 1993, p. 17) are never used in practice as the core PBR structure for regulating electricity distribution utilities in the U.S. Nor indeed was a simple price-cap mechanism alone used to regulate distribution companies in Great Britain during the first decade of the twenty-first century (Joskow, 2014, pp. 309–326). Automatic inflation and productivity adjustments are often included as a component of more comprehensive PBR mechanisms; but the length of time between formal regulatory reviews is typically three-to-five years, so ratchets that rely on COSR to reset prices play a significant role, along with sets of specific performance metrics and incentives, profit sharing mechanisms, reopeners, revenue decoupling, limited cost pass-throughs for extraordinary costs, and other more targeted incentive mechanisms.

The goals of mitigating the regulated monopoly’s market power, stimulating cost efficiencies, and encouraging innovation—while meeting economic and legal constraints that require regulatory mechanisms to allow regulated firms to cover their “reasonable” costsFootnote 6—continue to guide the evolution of PBR mechanisms for electric distribution utilities in the U.S. There is also considerable respect for the limited information that regulatory agencies have at their disposal, the limited resources that the typical state regulator can draw upon, uncertainties about future cost opportunities, uncertainties about future electricity demand and distribution utilities services, and uncertainties about the expectations that will be placed on distribution utilities in the future.

Overall, PBR applied to electricity distribution in the U.S. is best viewed as a complement to COSR regulation—not a complete substitute—as Laffont and Tirole (1993) recognize. The post-RPI-X regulatory mechanisms that have been adopted in Great Britain for major distribution companies that are subject to the jurisdiction of the regulator (OFGEM) in Great Britain, called RIIO-1 (ED1) and now RIIO-2 (ED2),Footnote 7 which were developed through its “RPI-X@20” review process from 2008 to 2010,Footnote 8 have been especially influential for regulatory reforms of electricity distribution recently in the U.S.

Third, as I will discuss below, the use of standard theoretical and empirical PBR concepts in the regulation of electricity distribution has not extended to the regulation of transmission owners and independent system operators in the US. The state of PBR that is applied to transmission companies and the system operator are far more advanced in Great Britain—both during the “RPI-X” period (Joskow, 2014, pp. 326–332), and under the more recent RIIO reforms. This is despite—or perhaps because of—the dramatic shift of regulatory responsibility for transmission rates and services from state regulators to the Federal Energy Regulatory Commission (FERC) since the late 1990s, especially where vertically integrated utilities have unbundled transmission service from distribution and generation.

Moreover, non-profit independent system operators (single state ISOs or multi-state RTOs)Footnote 9 now manage the operation of both organized competitive wholesale markets for electricity in conjunction with the management of the operation of the transmission networks that serve about 2/3 of the retail customers in the U.S. They also have responsibility for transmission planning in their regions and, in principle, across ISO/RTO boundaries.

While FERC has introduced a set of targeted incentives to encourage more investment in transmission networks, transmission service price regulation still relies primarily on traditional COSR in a form that is antithetical to the goals of PBR. The experience in Great Britain with PBR regulation of transmission companies and the system operator under the RPI-X regime and its replacement by the RIIO framework to transmission owners and the system operator has had little if any influence on the regulation of transmission and system operators in the U.S.

I have previously discussed the application of the so-called RPI-X framework to transmission owners and the system operators in Great Britain (Joskow, 2014). In light of the lack of influence of both RPI-X and RIIO on transmission and system operations in the U.S., I will not discuss the RPI-X regime further here. Nor will I discuss the RIIO framework that is applied to transmission owners and the system operator in Great Britain further here, aside from a few references in the context of the regulatory and organization framework for transmission and system operations in the U.S.

Finally, the quotations at the beginning of the article reflect the realities of regulation of electric distribution and transmission in practice in the U.S. Of course, all regulatory mechanisms provide incentives that affect the behavior of the firms that are subject to these regulatory mechanisms. The incentives and associated behavior may be consistent with advancing the regulator’s objective function or inconsistent with it.

However, in the context of this article, this observation has important implications. There has been a tendency in the incentive regulation literature to characterize regulatory mechanisms as either/or choices: Regulated firms either are or are not subject to COSR or PBR.

This is a false dichotomy: COSR in practice has always varied considerably from pure textbook COSR—except perhaps for some formula rate mechanisms which I will discuss further below. Moreover, introducing PBR is not an either/or decision. There are many possible components of PBR mechanisms that can and have been introduced over time. This is why we see responses to the question “how many states have adopted PBR regulation?” vary widely. One report observed that 39 states had at least some form of PBR mechanism (PEPCO, 2020). On the other hand, there are only a handful of states that have implemented comprehensive PBR mechanisms similar to those in Great Britain and a few more that are in the process of doing so.

In the end, one needs to examine the incentive properties of the package of PBR mechanisms that have been introduced—typically in parallel with fairly frequent recalibration that uses COSR—as a touchstone for price and nonprice performance results, the derivation of new starting prices (the ratchet), and changes in the design of the PBR mechanisms.

Finally, the nature of the obligations that are being placed on electricity distribution and transmission companies in the U.S. has changed considerably: This reflects decarbonization policies, competition policies, and changes in the technologies that are used in all segments of the electric power sector. This has increased the administrative burdens on state regulatory agencies, which as I will show below, typically have very limited resources compared to OFGEM in Great Britain. The expectation that PBR mechanisms can reduce this burden—whether this is a reasonable assumption or not—has increased the state regulators’ interest in PBR mechanisms.

This article proceeds as follows: The next section provides a brief description of the U.S. electric power sector and how it has evolved over the last 30 years. Section 3 focuses on the changing obligations that are being placed on electric distribution companies in the U.S. Section 4 discusses the building blocks of the PBR mechanisms that are being applied to electric distribution companies in the U.S. Section 5 discusses recent reforms in the regulation of distribution utilities in Great Britain following a major review of the existing regulatory arrangements: the “RPI-X@20” review. The new package of regulatory arrangements that were adopted and subsequently revised is called RIIO (Revenue = Incentives + Innovation + Output). I discuss these developments in regulatory practice in Great Britain here since RIIO has influenced the speed and direction of PBR as applied to distribution utilities in the U.S. The changes in both countries reflect similar changes in the responsibilities now given to distribution utilities—especially as they relate to decarbonization of the electricity sector. The final substantive section discusses the contemporary regulatory framework for transmission owners and transmission system operating organizations in the U.S. A brief section of conclusions completes the article.

The primary conclusions are as follows: PBR mechanisms that have many similarities to recent RIIO reforms in Great Britain are expanding—but slowly—in the U.S. However, it is important to view PBR as applied to the distribution of electricity as being composed of a set of “building blocks” that can be combined to create a comprehensive PBR plan. These building blocks are often adopted sequentially as regulators become more comfortable with PBR mechanisms.

The expansion of PBR has been gradual for a number of reasons, including: the limited staff and budgetary resources that are available to state regulators; and misunderstandings by U.S. policymakers as to how the RPI-X mechanism that applied to electricity distribution and transmission—as opposed to application of simple price-cap mechanisms to certain telecom services—evolved over time in Great Britain to be much more than a simple price-cap mechanism.

Finally, largely due to the decentralized and heterogenous structure of the ownership of transmission companies and the reliance on non-profit system operators, there has been little effort to apply PBR mechanisms to the operating costs, investments costs, planning, or other performance criteria for either transmission or system operations in the U.S. This is quite different from the experience in Great Britain, where PBR—including the more recent RIIO framework—has been applied to transmission owners and the system operator for almost 25 years. The Federal Energy Regulatory Commission (FERC) has used a set of targeted incentives to stimulate investment in new transmission facilities, to create separate transmission companies, and to join ISO/RTOs. These initiatives to expand competitive opportunities for the development of new transmission facilities may be a partial substitute for PBR for transmission owners—but progress here has been slow.

2 The U.S. Electric Power Sector in Brief

The U.S. has a diverse electric power sector composed of investor-owned utilities (IOU), municipal and state-owned utilities, cooperative utilities, and federal power generation and marketing agencies.

Historically, circa 1985, IOUs accounted for about 75% of the end-use customers served and a similar fraction of electricity generated. Utilities varied (and continue to vary) widely in size. Almost all IOUs were vertically integrated into generation (G), transmission (T), and distribution (D) (including bundled retail supply of energy); these are the primary structural components of electricity supply (Joskow & Schmalensee, 1983, Chapter 2). Most IOUs operated their own transmission networks as control area operators while others, primarily in the Northeast, joined centrally dispatched power pools like PJM (Mid-Atlantic region) or NEPOOL (New England).

Most municipal and cooperative utilities only distributed electricity; they purchased generation services from proximate IOUs, federal and state power suppliers (e.g., TVA, Bonneville, New York Power Authority), and cooperative G&T organizations. Some large municipal and state-sponsored utilities were and still are vertically integrated (e.g., Los Angeles Department of Water and Power or LADWP); some had generation and transmission but did not and still do not distribute electricity to end-use consumers (e.g., Brazos Coop); and many were and are just distributors.

I will focus on IOUs in this article.

IOUs that distribute electricity to end-use customers were and are regulated primarily by state regulatory commissions. There are 49 state regulatory commissions and a regulatory commission that covers the District of Columbia.Footnote 10 FERC played a much less significant role historically than is the case today: It regulated wholesale power supply agreements between IOUs and between IOUs and other types of utilities, including the terms and conditions of power pooling arrangements such as PJM, NEPOOL, etc., and the terms of any underlying transmission contracts to support these power trading arrangements. As a consequence of vertical integration and the then existing FERC regulations that governed transmission access and pricing, the vast bulk of transmission costs were regulated by state public utility commissions and included in the IOU’s retail cost of service.

There were many complaints about access to transmission services and the terms and conditions of transmission contracts by municipal and cooperative distribution utilities prior to 1996. This was the case since vertically integrated IOUs did not then have obligations to offer transmission service; and when they did, they relied on negotiated contracts rather than posting generally available tariffs that specified the terms and conditions of transmission service. Nor did they have an obligation to expand transmission capacity to accommodate requests for transmission service. Antitrust complaints with regard to transmission access and pricing were frequently used by municipal and cooperative distribution companies to obtain access to IOU transmission networks in order to buy power from other suppliers.

Any net revenues from wholesale sales and purchases of power and of transmission service were credited back against the state-regulated cost of service (Joskow, 2005). State regulatory agencies were also responsible for oversight of system planning for the future. For a detailed discussion of the structure and regulation of the industry circa the early 1980s, see Joskow and Schmalensee (1983).

The structure of the IOU sector and the division of regulatory responsibility between state and federal regulators began to change in the 1980s: slowly at first and then more rapidly. The changes involved support for the development of an independent power generation sector, starting with the Public Utility Policy Act of 1978 (PURPA). PURPA stimulated development of non-utility independent cogeneration and small power projects that satisfied PURPA’s technology and size restrictions during the 1980s. The Energy Policy Act of 1992 created a broader class of independent power producers (Exempt Wholesale Generators—EWG—that are now referred to collectively as Independent Power Producers (IPP)) that are subject to FERC oversight.

FERC in turn promoted competitive wholesale markets where both regulated utility generators and IPPs could trade electricity that they generated to meet demand more efficiently. FERC allowed independent power producers to be exempt from formal rate regulation if they could demonstrate that they did not have market power in the wholesale market. A few states began to require vertically integrated utilities to seek competitive bids for additional power supplies rather than just assuming that they would build their own new power plants. Thus, vertical integration began to unravel slowly as an independent power sector grew. However, transmission access and pricing continued to be a barrier to more rapid expansion of competitive regional wholesale power markets.

In 1996, FERC (2023a) began to require all jurisdictional utilities to file and implement open access non-discriminatory transmission tariffs and related system information so as to make their transmission systems available to all generators, intermediaries, and their wholesale customers at cost-based rates (FERC Orders 888, 889, 890).Footnote 11 Strong encouragement followed for the creation of independent non-profit system operators (ISOs or RTOs) (FERC Order 2000/2000A) and the development of organized wholesale spot markets for energy, ancillary services, and in most cases capacity, managed by the ISO/RTOs.Footnote 12

ISO/RTOs cover regions that represent about 2/3 of U.S. electricity consumers. In these regions they are responsible for: managing organized wholesale markets for energy, capacity, ancillary services, congestion revenue rights, transmission system operations (including congestion management and operating reliability), interconnections for new generators and merchant transmission projects, transmission system planning, and transmission cost allocation; managing the ISO’s open access transmission tariff (OATT); developing the annual transmission revenue requirement for each transmission owner (TO), which is submitted by the transmission owner to FERC to support its transmission service prices; and developing the associated transmission rates for transmission services that are available in the OATT.

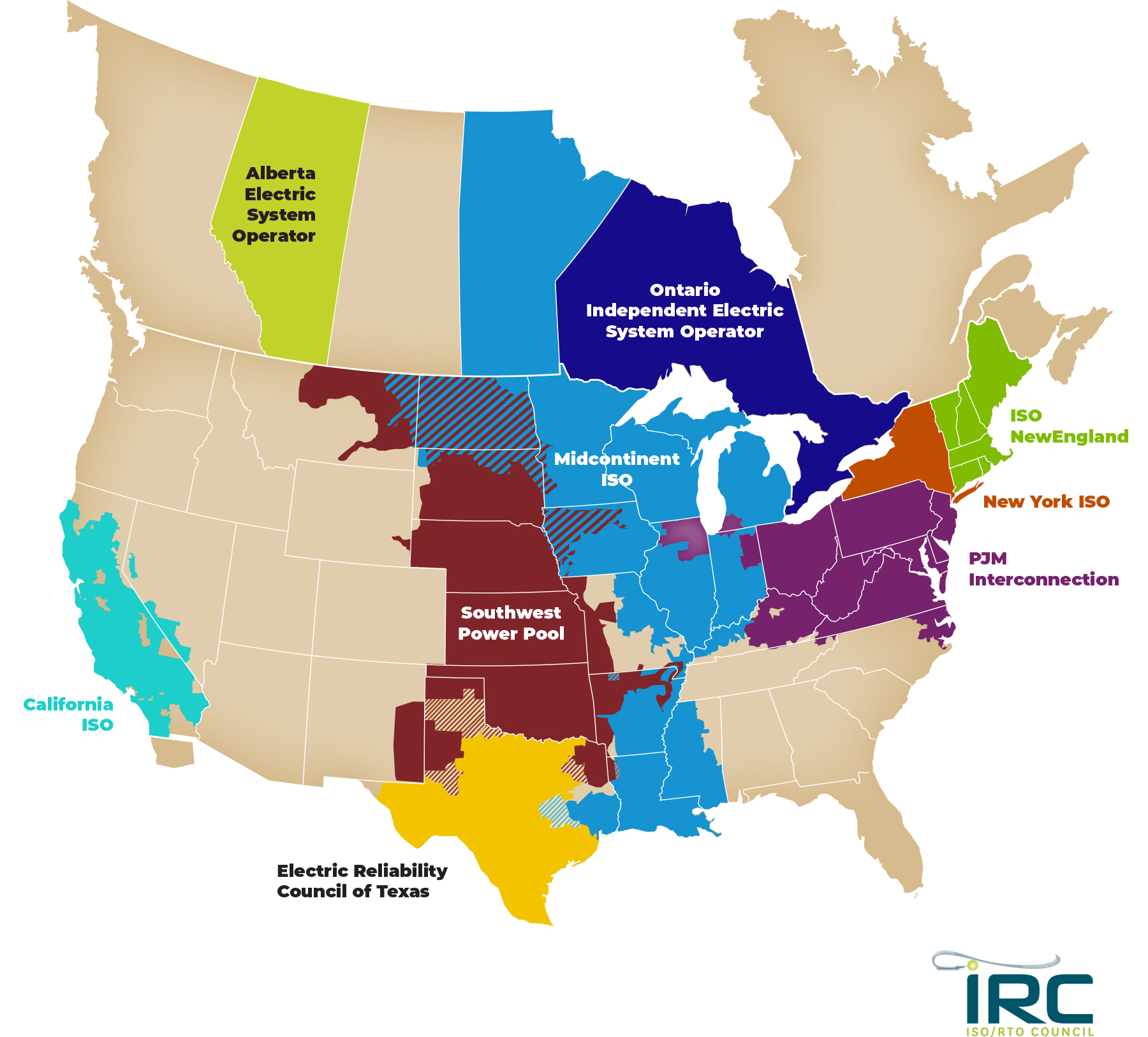

ISO/RTOs are independent non-profit organizations with members that represent all components of electricity supply and demand. ISO/RTOs are regulated by FERC.Footnote 13 They do not own any transmission assets aside from the facilities, equipment, and software that are required to perform their system operator functions. Figure 1 provides a map of the U.S. (and Canada)Footnote 14 that shows the regions in which utilities have joined ISO/RTOs and regions where they have not. The map provides the name, location, and acronym for each of the ISO/RTOs in the U.S. I will use the acronyms for the ISO/RTOs when I refer them in the discussion below. The Southeast and the West (aside from California) are the primary areas where utilities have not joined ISOs, though discussions have advanced considerably regarding the creation of a Western RTO.Footnote 15

ISO/RTO regions in U.S. and Canada Source: ISO/RTO Council. http://isortotest.org/wp-content/uploads/2018/05/ISO-RTO-Map-2018.jpg

These federal actions were complements to restructuring initiatives at the state level. Starting with California, a number of states initiated restructuring programs that separated the ownership of generation (potentially competitive) from transmission and distribution (which would continue to be regulated as both legal and natural monopolies).Footnote 16 Most of these states have also implemented retail supply competition and associated unbundling requirements that require the incumbent utilities’ distribution and transmission platforms, under traditional regulatory arrangements, to pass along to retail customers the costs of the service that is supplied on these platforms.

Independent power producers account for almost 45% of the electricity that is generated in the U.S. today, while the traditional (now partially vertically integrated) utilities (IOU, Muni, Coop, Federal) now account for 53% of generation—compared to nearly 100% in 1980—and the rest is customer-based generation. Customer-based generation—primarily rooftop photovoltaic (PV)—has also expanded rapidly in the last ten years. Moreover, for utilities that became members of ISO/RTOs, the regulation of transmission rates was effectively shifted fully from the states to FERC.

Accordingly, the U.S. electric power sector has become even more diverse than it was in 1985. There are about 135 “major” IOUs that distribute electricity in the U.S.Footnote 17; some are fully unbundled from generation and retail supply, and many are partially vertically integrated. Only about 12 states have adopted full unbundling and retail supply competition. IOU distribution utilities covering about 2/3 of U.S. electricity customers are members of independent transmission organizations (ISOs or RTOs). Many of these IOU distribution utilities are under joint ownership by a holding company; this has especially been the case since the repeal of the Public Utility Holding Company Act (PUHCA) in 2005, which ended most of the restrictions on the formation of public utility holding companies and transferred some regulatory authority from the Securities and Exchange Commission to FERC and the U.S. Department of Justice.Footnote 18 A map of the service areas for the members of the Edison Electric Institute (EEI), which is the trade association for IOUs, can be found on EEI’s web site.Footnote 19

About 22 states and the District of Columbia have adopted aggressive decarbonization targets for their electricity sectorsFootnote 20; these targets call for the expansions of investment in wind, solar PV generation, and other carbon-free electricity generation technologies, as well as storage, which has been primarily developed by independent power producers. Recently, there has been a renewed interest in nuclear power (existing and new), and carbon capture and storage technologies.Footnote 21

The general decarbonization “model” that these states are following is to decarbonize their electricity sectors deeply and then to use “clean” electricity to support the electrification of transportation (electric vehicles: EV) and the electrification of space and water heating in buildings, which will thereby displace fossil fuels, and the electrification of some other sectors. In most cases, the distribution utilities are expected to play an intermediary role: They purchase power from independent suppliers so as to meet state-specified renewable portfolio or clean energy standards for the demand that they continue to serve; they implement rates that are designed to promote and integrate (and often subsidize) distributed energy resources (DER) such as rooftop and community solar PV; they facilitate the expansion of EV charging infrastructure; they manage customer energy efficiency and demand response programs; and they expand and modernize their network infrastructure, so as to accommodate what is anticipated to be a large increase in electricity demand that will result from the electrification of major end-use sectors.

3 The Changing Structure and Obligations of Electric Distribution Companies in the U.S.

Why have U.S. regulators become much more interested in PBR mechanisms for electric distribution utilities in the last five-to-ten years? In a nutshell, the role of electric distribution companies has changed considerably in the last two decades—but especially in the last five-to-ten years. The changes have increased the dimensions of the objective function that regulators seek to optimize, and accordingly the regulators have placed additional obligations on regulated distribution utilities—and in the process further complicated the task of regulating them.

There are several drivers of these changes: First, in states that restructured their vertically integrated utilities, electricity distribution became the primary target of state regulatory responsibility.

Second, it took perhaps a decade for state commissions to manage and adapt to the changes that were brought about by restructuring. More than a dozen states adopted retail energy supply competition and/or municipal aggregation options.Footnote 22 The changes required significant attention by state regulators in order to put the supporting institutions in place and to respond to “teething problems” that emerged. State commissions also participated in the transition to ISO/RTOs and competitive wholesale markets in general to play a role in defining and adjusting to FERC’s rules for organized wholesale markets, transmission pricing, transmission investment, and transmission planning.

Third, electricity distribution companies in the U.S. have been given a dramatically expanded set of responsibilities compared to their traditional obligations to deliver commodity electricity to customers economically, safely, and reliably—the traditional focus of COSR and associated service-quality standards. Many of these new commitments reflect the central role that the electricity sector is expected to play in meeting state and federal decarbonization commitments and goals. These include: energy procurement from independent power producers of carbon-free energy (wind and solar); integration of rooftop and community PV and other DER; distribution-level storage; investing in a “smart grid” with enhanced communications, control, and metering capabilities; supporting the development and integration EV charging stations; designing and implementing customer energy efficiency programs; and other obligations that have been motivated by decarbonization policies and the technological changes that are accompanying them.

Importantly from an incentives perspective, many of the costs that are being incurred by distribution utilities to meet both traditional energy delivery responsibilities and these new obligations were traditionally treated as automatic pass-throughs into regulated retail rates with no margin and no profit opportunity for the distribution utility. As these costs are automatic pass-throughs (rather than rate-based capital expenditures upon which the utility can earn a return or subject to the incentive properties of regulatory lag—more on this below) and have become a growing fraction of the regulated distribution charges, the weak incentive properties of COSR—especially the biases toward owning capital facilities rather than buying comparable services from third parties—became more obvious to regulators.

As a result, regulators have become more interested in PBR mechanisms that can provide financial incentives to make pursuing these obligations efficiently “interesting” to distribution utilities from a profit opportunity perspective and not just another regulatory mandate that is difficult for regulators to oversee.

As a consequence of concerns about the biases in resource allocation choices that are associated with COSR regulation, there is also growing interest in requiring distribution utilities to: identify distribution services that were traditionally provided by the distribution utility itself and included in COSR protocols but could in principle be opened to competitive suppliers; implement competitive processes so as to evaluate and procure such services from competitors; and require the distribution company to “host” these services. If distribution utilities provide hosting services, there will be lost profit opportunities and no compensating financial benefit unless a new regulatory mechanism is added to stimulate efficient competitive procurement processes and hosting.

The standard prescription that the primary goal of good regulation of natural monopolies should be to replicate as closely as possible the prices, costs, and service-quality attributes that would be realized in a hypothetical competitive market has therefore become more complicated. This prescription implied cost minimization, efficient (second-best) prices, budget balance, and monopoly rent extraction, and service quality that balanced the cost and benefits of network outages and of improvements in customer service. The objective function for distribution companies and their regulators has become more complex, and regulators are understanding that regulatory reforms are needed to match these new responsibilities with standards and associated incentive arrangements.

Moreover, it would be unlikely that some of the new responsibilities and associated services that have been imposed on distribution utilities would even be provided by firms in a hypothetical competitive market: How many firms would pay consumers not to use their products or subsidize competing suppliers? It is worth noting that several of these new responsibilities appear to be examples of “taxation by regulation” (Posner, 1971)—in the sense that the costs that are associated with meeting these new responsibilities are passed through to electricity customers in non-bypassable and non-transparent distribution delivery charges while they could instead be funded through state and federal taxation.

Finally, regulators and utilities expect that electricity demand—and the associated need for network investments to support it reliably—will begin to increase rapidly as a consequence of the electrification of transportation, buildings, and other sectors. Higher rates of inflation and higher interest rates have in the past and are expected in the future also to drive a growing number of formal rate cases with reliance on COSR. (Variations in the number of rate cases and regulatory lag are discussed further below.)

Absent changes in regulatory procedures, these changes should be expected to drive the need for more annual formal rate cases under traditional COSR so as to adjust rates to reflect a growing rate base from the growth in network investments and to reflect rising operating costs, and to monitor several additional performance metrics. In the absence of some kind of multi-year regulatory pricing mechanisms and compatible performance standards and incentives, this would further increase the administrative burden for state regulators.Footnote 23

Accordingly, state commissions and state legislatures have been more interested in examining and implementing alternative regulatory mechanisms that are better matched to these changes in policy-driven obligations, can rely more on incentives rather than mandates, and operate more “automatically” without creating the poor efficiency incentives that are associated with more frequent reliance on formal COSR review to reset rates, monitor service quality, and oversee utility performance in pursuing state and federal policy goals.

In this regard, contributing to the slow introduction of PBR mechanisms is likely to be the limited human and financial resources that state regulatory agencies have available to regulate electric and gas utilities.Footnote 24 Nor does the typical state regulatory commission have budgetary resources to hire many costly outside consultants. Table 1 displays the latest number of employees for OFGEM, the electricity and gas regulator in Great Britain,Footnote 25 and several U.S. state regulatory commissions that are responsible for electric distribution regulation, as well as for gas distribution regulation, and other state-regulated sectors such as water, transportation, telecom, insurance, and energy-facility siting, depending on the state.

Aside from California and New York, most state commissions that are responsible for regulation of electric distribution companies and that would be responsible for guiding PBR design and implementation, have very modest staff resources. Moreover, they typically have regulatory responsibilities outside of electricity and gas distribution. For example, the California commission (CPUC) has regulatory responsibility for electric distribution and (some) generation, natural gas distribution and intrastate gas pipelines, water, intra-state rail safety, and some aspects of communications. On the other hand, FERC—unlike OFGEM—has no jurisdiction over electric or gas distribution utilities, or the non-energy sectors that fall under many state regulatory agency responsibilities.Footnote 26

4 Building Blocks of PBR Mechanisms for Electricity Distribution Companies in the U.S.

4.1 PBR and COSR in Practice

In the academic literature, there has been a tendency to characterize the introduction of PBR mechanisms as an either/or decision and to view the alternative as textbook COSR regulation. This view is at best naïve and at worst uninformed. If we apply the statements that are attributed to Kahn and to Laffont and Tirole in the heading of this article, all utilities in the U.S. are subject to some kind of incentive regulation. Indeed, a recent filing (which relied on testimony from the Edison Electric Institute) before the Maryland Public Utilities Commission argues that 39 states are subject to some form [emphasis added] of PBR regulation.Footnote 27 Yet, I have been able to identify only about a dozen states that operate under or are planning to implement comprehensive (as defined below) PBR plans that reflect similar mechanisms to those that have been adopted by RIIO for distribution in Great Britain.

The resistance to PBR plans among U.S. regulators also in part reflects a misunderstanding of what PBR implies in general and what “RPI-X” as applied in practice to electricity distribution and transmission utilities in Great Britain at the beginning of the twenty-first century actually means. The use of the phrase “RPI-X” has been interpreted incorrectly as referring to the simple price cap mechanisms that have largely replaced COSR regulation in the telecommunications sector in the U.S., Great Britain, and many other countries since the mid-1980s.

As I have discussed previously (Joskow, 2014), RPI-X regulation of distribution and transmission in Great Britain is a short-hand phrase for what ultimately became a much more complex set of incentive mechanisms than was often portrayed by U.S. regulators who were already familiar with the use of simple price caps for certain telecommunications services. The regulators viewed the telecommunications and electricity distribution situations as being quite different: Price caps in telecommunications were transitional regulatory mechanisms that would fade away as competition replaced the need for regulation. But the regulators did not believe that the regulation of electricity distribution was going away anytime soon.

The recent changes in the regulatory framework made after the RPI-X@20 review in Great Britain have created even further distance from a simple price-cap mechanism applied to electricity distribution. I will discuss some of these changes that have been unleashed by RIIO in Great Britain in Sect. 5 below.

Furthermore, COSR regulation continues to play an important role in PBR plans that rely, in part, on external price and productivity indices and benchmarks to adjust revenues and prices over time. COSR regulation is used to establish the starting set of prices or revenues at the beginning of the typical term of such a PBR mechanism and then is used again to reset (ratchet) prices when the next term of the PBR begins. In this sense, PBR and COSR are complements—not substitutes—as the quotation from Laffont and Tirole (1993) at the beginning of this article points out.

If we examine the earliest papers of which I am aware that propose the use of a simple RPI-X price cap mechanism (Baumol, 1982; Littlechild, 1983), there is actually no detailed discussion of how either the initial prices are set or how they would be reset after a period of time if regulation continued to be justified to mitigate monopoly power problems. Both papers focus on the application of a simple price-cap mechanism to adjust the incumbents’ prices—AT&T and its local exchange affiliates in the U.S., and British Telecom (BT) in Great Britain)—over time. I think that it would be reasonable to assume that both papers have in mind using the existing pre-price-cap prices as the starting prices and do not need to discuss how those prices were determined. Both papers also recognize that some type of regulatory review and adjustment to the price-cap mechanism would be necessary—though there are no details that are presented as to how the resets would be accomplished.

Baumol (1982, p. 17) recognizes and indeed supports COSR regulatory reviews from time-to-time that could reset prices and the parameters of any subsequent price-cap mechanism. “No commission should or can be expected, after adopting such a rule, to leave the task of rate adjustment entirely to the formula forever thereafter. Rather, an essential part of the program …is a process of monitoring of the performance of the formula by the regulatory agency, which should be expected to subject it to a formal review process from time to time. A general rate case would, for example, constitute an appropriate occasion for such a review.”

Similarly, Littlechild (1983, p. 35) suggests that an automatic referral to the Monopolies and Mergers Commission (MMC) after, say, five years (from the initial introduction of the price-cap mechanism) would be appropriate. “By that time, the extent and strength of competition should become more apparent, and it may be appropriate to extend or restrict the scope of the [regulated] ‘monopoly basket’; to change the value of X or to rebase the calculation; to abolish the tariff reduction scheme altogether or to impose additional constraints.”

Littlechild (1983) also recognizes that a simple price-cap mechanism could create incentives to reduce service quality but argues that identifying all of the relevant quality attributes would be too difficult. He suggests instead that a general clause that commits BT to maintain quality be added to its license. As we shall see service quality and other performance mechanisms, as well as license conditions, are now important components of PBR in the U.S. and in Great Britain.

It is interesting that two scholars came up with essentially the same adjustment mechanism for the same industry at almost the same time but for different reasons. Both the context and emphasis on continuing regulation are quite different in the two papers: Baumol’s proposal is motivated by the effects of more rapid inflation combined with regulatory lag on the earnings of the regulated telecommunications companies as well as the administrative burden of more frequent rate cases in response to more rapid inflation during the 1970s. The price-cap mechanism is seen as a way to adjust prices automatically between formal rate cases and make it possible to reduce the number of formal rate cases while reducing the earnings erosion that was adversely affecting the regulated firms’ earnings. The word “competition” does not appear in his paper.

Littlechild’s proposal is part of a very thoughtful analysis of alternative regulatory mechanisms that had been proposed at that time as the initial regulatory mechanisms to accompany the privatization of British Telephone (BT). Littlechild’s report places a great deal of emphasis on the potential role of expanding competition for BT’s services over time. If we “read between the lines”, it appears that he anticipated that competition could grow significantly as long as BT could not engage in practices to stamp it out. Over time, competition would make it possible to substantially reduce the scope of regulation to mitigate monopoly power.Footnote 28 He was quite prescient in this regard: Competition did grow in both the U.S. and Great Britain; COSR regulation has faded away over time; and competition now governs most telecommunications services (Sappington & Weisman, 2010).

However, as we noted above, regulation of electricity distribution and transmission companies is not expected to fade away anytime soon. Indeed, as I have discussed, the scope of regulation of electricity distribution has expanded as distribution utilities’ obligations have expanded. For electricity distribution any acceptable dynamic price adjustment mechanism that is based on external indices will have ratchets where prices are reset every three-to-five years (or so) with the use of a very detailed set of fairly standard COSR formulas.

For example, if we examine the 550-page regulatory order that was issued by the Massachusetts Department of Public Utility in 2022 (MDPU, 2022) to revise a comprehensive PBR plan for NSTAR (the electricity distribution and transmission company that serves Boston and surrounding communities), a little over 100 pages focuses on the PBR plan and 450 pages is devoted to the application of traditional COSR regulation principles to establish the starting revenue cap (revenue requirement) in the PBR plan and then the associated rates for each class of customers. The earlier NSTAR order with a PBR plan that was issued in 2017 (MDPU, 2019a) was 786 pages—of which over 600 pages was devoted to applying COSR regulatory principles to set the starting values for revenues and prices. So too in Great Britain under RPI-X (Joskow, 2014) and under RIIO (OFGEM, 2017).

In this regard, let me note that in a world where the regulator is uncertain about the utility’s costs, whether it is a low-cost or high-cost type (adverse selection) and uncertain about managerial effort (moral hazard), and where there is a rent-extraction goal and budget-balance constraint, a simple price cap mechanism is highly unlikely to be optimal—except perhaps in the case where it is merely a transition mechanism on the path to deregulation and competition. Indeed, menus of contracts, profit-sharing or sliding-scale arrangements (Lyon, 1996), and ratchets are likely to provide a better balance between performance incentives and rent extraction goals (e.g., Laffont & Tirole, 1993; Schmalensee, 1989). If simple price caps alone were optimal, Laffont and Tirole would have written a much shorter book.

Finally, Baumol’s proposal was motivated by regulatory lag: a real regulatory phenomenon that has received inadequate attention in my view in the incentive regulation literature’s characterization of COSR. Prior to the introduction of formal incentive regulation plans, which defined how rates would adjust over time between rate cases, there were sometimes long periods of time when the prevailing rates of the regulated firm were not “tested” in a rate case.

Instead, “regulatory lag” has been the norm during many time periods. This means that after prices are set in a rate case, several years may pass until the next regulatory review takes place that resets prices. Kahn (1971, Volume II, p. 48) observes that “The regulatory lag… is it to be regarded not as a deplorable imperfection of regulation but as a positive advantage. Freezing rates for the period of the lag imposes penalties for inefficiency, excessive conservatism, and wrong guesses and offers rewards for the opposites: companies can for a time keep the higher profits they reap from superior performance and suffer the losses from a poor one.”Footnote 29 One can see the seeds of price-cap regulation in these observations—well before Baumol (1982) and Littlechild (1983).

During certain periods of time, COSR regulation for electric utilities has been more regulatory lag than formal application of COSR through annual formal rate cases. In earlier work, I found that about a third of the utilities had zero formal rate reviews between 1958 and 1972, and another third of the companies had one rate review (Joskow, 1974, Table 3). Lowry et al., (2017, their Table 2) report rate-case activity for a longer period of time—1948–1977—with similar patterns of rate-case activity. EIA reports the number of electric utility rate cases for each year from 1980 through 2018 from third party sources (USEIA, 2019),and S&P Global (2023) extends the time series to 2022, though it has been suggested to me that the S&P Global may overstate the number of rate cases in recent years by counting some formula rate adjustments as rate cases.

Overall, the number of annual rate cases varies widely over the 1948–2022 period. During much of this period the probability that a utility was subject to review in a formal rate case was quite low. However, the number of formal rate cases began increasing about 2000, around the time that the restructuring process began—and the number of rate cases continued to increase through 2022. This is consistent with the recent perception by regulators that the administrative burden of formal rate cases has been growing.

Moreover, in most cases, the utility initiated the rate case and not the regulator.Footnote 30 The decision by a utility to trigger a rate case seems to be driven primarily by changes in interest rates, inflation, and the accumulation of capital investments that have not yet been included in the rate base and rates. Restructuring activity, including mergers, may also trigger a formal rate case. Eventually, these factors cause actual earnings to fall to or below what the regulated firm expected that it would receive in a formal rate case (Joskow, 1973); and, as a result, the utility triggers a formal rate case by filing for a general price increase.

Accordingly, during some periods of time utilities can go for many years without filing for new rates and effectively operate with a fixed price capFootnote 31—which can lead to the efficiency benefits that are discussed by Kahn. However, regulatory lag is an “accidental” consequence of COSR in practice that does not generally reflect strategic decisions by regulators to implement a set of PBR mechanisms to provide better incentives.

In my view, since COSR is a complement to PBR rather than a substitute, if one wants to understand the incentive properties of real PBR programs with dynamic price or revenue adjustments that are based on external indices but that turn to COSR regulation to set and reset prices every three-to-five years, then one needs to understand the details of COSR regulation.Footnote 32

4.2 The Building Blocks of PBR of Distribution Utilities in the U.S.

In the U.S. context, the best way to think about what is broadly referred to as PBR regulation is as a set of PBR “building blocks” that can be adopted individually or combined into a more comprehensive package. As a practical matter, the building blocks tend to be adopted sequentially: with many regulators’/utilities’ adopting one component and then proceeding to adopt others over time. So far, only about a dozen state regulators/utilities have adopted or are in the process of adopting comprehensive PBR mechanisms that include all of the building blocks; but many have “stuck their toes in the water” with at least one component from the set of PBR building blocks to which I now turn.

It is now common practice to break PBR regulation of distribution utilities in the U.S. down into four basic components:

-

1.

Performance incentive mechanisms (PIMs) that are targeted at a set of specific performance metrics.

-

2.

Revenue decoupling mechanisms (Decoupling).

-

3.

Multi-year rate plans (MVRPs) where prices or revenues are adjusted according to exogenous indices between general rate cases (like a dynamic price adjustment mechanism with a fixed term, after which prices are reset with the use of COSR)

-

4.

Performance Incentives that accompany New Initiatives and Pilot Programs.

I will discuss each component in turn.

4.2.1 Performance Incentive Mechanisms (PIMs)

The introduction of PIMs by state regulators to provide benchmarks and incentives for various non-price performance indicia can be traced back to the late 1980s, when a few commissions created incentive mechanisms in connection with energy efficiency programs for which electric and gas distribution utilities in some states were given significant responsibilities. Utility expenditures on energy efficiency programs are typically cost-passthroughs that are recovered automatically by formula adjustments between general rate cases.

However, since the goal of these programs is to stimulate customer adoption of energy efficiency recommendations that also lead to a reduction in electricity consumption, the utility would lose net revenues between formal rate cases due to regulatory lag. Thus, energy efficiency programs did not appear to be a particularly interesting business opportunity for utilities, and many utilities were initially either slow to adopt them and/or did not pursue them with great enthusiasm.

In the late 1980s, the late CEO of New England Electric System (subsequently acquired by National Grid), John Rowe, argued to me that “the rat needs to smell the cheese” and proposed that utilities be given incentives (potential rewards and penalties) that would be based on meeting, exceeding, or falling short of energy savings and associated net benefit benchmarks that would (in turn) be based on independent assessments of performance. The idea of building positive financial incentives into the energy efficiency programs caught on.

As of 2017, 25 states had adopted energy efficiency program incentive arrangements (Brattle, 2017, Appendix A-5).

PIMs gradually expanded to focus on one or typically several of the following quality attributes:

-

Customer Service and Billing Performance Measures

-

Customer Satisfaction Metrics (e.g. customer complaints, service response times)

-

Reliability Metrics (e.g., SAIDI, SAIFI, CAIDI, power quality measures)Footnote 33

-

Employee Safety Metrics (e.g., restricted work injury index)

-

Distribution Efficiency Metrics (e.g., line losses)

-

Generator Performance Metrics (for vertically integrated utilities)

-

Load factor and peak load reduction targets.

As of 2017 about 16 states had adopted at least some of these additional PIMs (Brattle, 2017, Appendix A-2).

More recently, even more PIMs are being added in response to the changing regulatory and policy responsibilities. These include:

-

Targets for expanding distributed generation and storage

-

Targets for the expansion of EV storage facilities (utility-owned and third-party)

-

Targets for moving customers to voluntary time-of-use (TOU) and critical peak pricing rates

-

Targets for expanding customer demand response capabilities

-

Environmental metrics (e.g., greenhouse gas (GHG) emissions)

-

Targets for “smart grid” deployment

-

Targets for “beneficial electrification” (e.g., heat pump adoption).

Adoption of the more recent PIMs is becoming more common in states that have adopted aggressive decarbonization and electrification targets. Regulators that have adopted at least one of these types of PIMs include New York, Vermont, Illinois, North Carolina, Washington, Hawaii; and states that are in the process of doing so include Connecticut, Maryland, and Nevada (Rocky Mountain Institute, 2022 and a communication from Mark Lowry with updated information).

One of the challenges in establishing PIMs is determining the appropriate targets or benchmarks for satisfactory performance. This is challenging due to: limited data availability; natural variation from one year to the next; lack of comparability across utilities in different regions of the country; differences between urban areas with significant underground distribution infrastructure and rural areas with primarily above ground infrastructure; and the technical challenges of doing sound benchmarking analyses.

Two approaches are often used: The first is to benchmark the utility against its own historical performance, and challenge the utility to meet or exceed its historical performance. If the utility consistently beats the benchmarks, they can be tightened. The second is to use industry benchmarks: trimming the data to take account of variations in exogenous drivers of performance in an effort to identify comparable utilities.

The final question is the specification of the incentive arrangements: In many states there is no financial incentive; but performance standards can be set by the regulator (similar to license conditions in Great Britain), and the utilities must prepare and make public a “scorecard” with their performance metrics. This is sometimes referred to as creating “reputational incentives.” Presumably, this information can then be used by the regulatory agency and intervenors in its next formal rate case to adjust allowed returns if there is poor performance.

In some states there are financial penalties for falling outside a range of acceptable performance (a “deadband”); and for some PIMs—especially energy efficiency PIMs—there are both financial rewards and penalties. For example, Massachusetts has defined a set of fairly complex formulas for calculating a deadband, penalty ranges, and financial penalties for a set of PIMs with a maximum aggregate penalty of 2.5% of annual T&D revenues (MDPU, 2016). The maximum penalty is not trivial. In a recent case that involved NSTAR’s rates, the maximum penalty would have been more than 10% of its net income (MDPU, 2022).

An example of actual penalty assessments can be found in a 2020 Massachusetts commission evaluation of Massachusetts Electric’s performance against a set of PIMs. It was assessed a penalty of $13,678,603 for missing some performance benchmarks compared to rate case net income of about $80 million or 15% of net income (MDPU, 2019).

4.2.2 Revenue Decoupling

As energy efficiency programs began to spread in the late 1980s and early 1990s, environmental groups became concerned that utilities would not fully embrace energy efficiency programs because the programs reduced the quantity of electricity sold. More recently, groups that represent DER—especially rooftop and community solar PV—and suppliers of non-wires and other competitive solutions to distribution network congestion and quality issues became concerned that their efforts would be resisted because they could reduce utility sales, rate base, and profits. Regulators with similar objectives also were concerned that regulatory lag would undermine incentives to pursue these programs aggressively.

One approach to these concerns was the introduction of the customer energy efficiency PIMs that I have already discussed. Another—sometimes in conjunction with an energy efficiency program PIM—approach was the introduction of automatic lost-revenue adjustment mechanisms (LRAMs) and more recently a general “decoupling” of revenues and sales that adjusted revenues to compensate for lost margins due to the divergence of sales from the values that were assumed in the most recent rate case.

Under an LRAM, the utility’s revenues are automatically adjusted between rate cases in order to compensate it for lost profits (margins) from realizing sales that were lower as a result of the effects of its energy-efficiency programs than had been assumed in the previous rate case. A general revenue decoupling mechanism is broader: It adjusts revenues and profits for all increases or decreases in quantities sold from the test year values that were used in the last rate case. The lost revenues could be from energy efficiency programs, increases or decreases in customers, rooftop solar PV installation, weather events, etc.

Accordingly, during a regulatory lag period, revenues and profits are not affected by variations in quantities. Note that for these adjustments to work as planned, the regulator needs to define the “margin” between prices and short run marginal costs so as to make the adjustments to restore agreed-to revenues profit neutral. This can be a complicated (and potentially controversial) set of calculations.

The California Commission (CPUC) introduced the first revenue-decoupling mechanism in the early 1980s. It is generally referred to as an ERAM (Electric Rate Adjustment Mechanism). It worked automatically to ensure that the affected utilities received exactly their authorized revenue requirement regardless of variations in quantities over time (Mornay and Comnes, 1990; Eto et al. 1994). The ERAM was supported by energy efficiency advocates so as to remove what they viewed as a bias against utility managed customer energy efficiency programs created under COSR. Others argued that the ERAM would mitigate the gaming of quantity forecasts in general rate cases where forecasts of future quantities are used, and would reduce the financial risk that was faced by utilities in association with variations in earnings between rate cases.

The ERAM was controversial, and at one point the staff of the CPUC recommended that it be ended. It operated from 1982 until 1996—when it was suspended as part of California’s anticipated (but short-lived) retail competition program. A revenue-decoupling mechanism was reintroduced in California in 2001 (Lowry et al., 2017, p. 6.8). There are now about 30 states that have adopted LRAMs or revenue decoupling for at least one of the distribution utilities that they regulate.Footnote 34

4.2.3 Multi-Year Rate Plans (MYRPs)

In the U.S., dynamic adjustment mechanisms—such as price-cap mechanisms with external adjustment indices—are called Multi-Year Rate Plans (MYRPs). The good plans are different from traditional regulatory lag in that the regulator sets a fixed time period between rate reviews ex ante—typically three-to-five years—so that neither the regulator not the utility determines when the next formal rate review will occur. They also build in adjustment for input price inflation, productivity benchmarks, service quality, and other considerations.

It is important to distinguish between two polar types of MYRPs: The type that is a natural component of a PBR plan that provides cost-efficiency incentives adjusts prices or revenues based on external indices of input costs, productivity or other factors. It may be accompanied by a profit-sharing or sliding-scale plan as well as include reopeners for various unanticipated or highly uncertain costs.

The other polar type of MYRP is a dynamic “formula rate” plan, where the utility’s rates are adjusted annually (say) based on realizations of the actual costs that the utility incurs: There are automatic true-ups for the actual operating and capital costs that are incurred by the utility in order to maintain the allowed rate of return that was determined in its last rate case. Some formula rates also provide for adjustment in the benchmark allowed rate of return for changes in external interest rate indices: for example, the yield on 30-year Treasuries. This is not a PBR plan. Formula rates are basically automatic pure COSR plans that have extremely poor incentive properties because they are effectively automatic cost-plus mechanisms based on whatever costs the regulated firm incurs—without formal regulatory reviews of costs and other attributes of performance.

California was the first state to rely on MYRPs of the former type beginning in the early 1980s (Lowry et al., 2017, Sect. 6.2).Footnote 35 In California, the MYRPs now apply to all of the IOUs in the state. The MYRPs have evolved considerably over time: They started with terms of two years; then rose to three years and are now four years for the three largest IOUs in the state (communication from Matt Makos).

A major rate-setting hearing—The General Rate Case (GRC)—establishes rates for the future period with the use of standard COSR principles. The established rates are then escalated over the next three years with the use of a set of external price indices that are applied separately to operating costs and capital costs. There are often specific additional items that are included in the utility’s dynamic cost profile based on approved business plans or as passthroughs for costs that meet a set of specific criteria (Synapse Energy Economics, 2019, p. 15). The details have varied significantly over time.

While the CPUC has characterized the MYRP plans as PBR, MYRPs were also introduced as a matter of administrative convenience since the formal base general rate cases are very detailed and administratively burdensome examinations of the companies’ costs and rates. A three-year cycle in particular makes it convenient to space the reviews for one of the major IOUs each year since there are three major IOUs in California, which conserves scarce regulatory staff resources.

As was noted above, the IOUs in California have been subject to revenue decoupling as well, except for a short time period. In addition, there has been an energy efficiency/demand-side management (DSM) PIM since 2007 (Lowry et al., 2017 p. 6.9) which was terminated in 2000 (communication from Matt Makos. While the CPUC monitors service quality metrics, there are no service quality PIMs at the present time, although the CPUC experimented with them in the past (Lowry et al., 2017 p. 6.14; Regulatory Assistance Project, 2021, p. 18). Instead, there are specific service-quality standards without penalties or rewards. The CPUC has also experimented with power plant performance incentives (Regulatory Assistance Project, 2021, pp. 65–66).

The New York Public Service Commission (NYPSC) has used MYRPs to regulate utilities since the early 1990s, though the details have varied from one utility to another. The regulator added a regulatory mechanism in 2016 (the review was initiated in 2014)—Reforming the Energy Vision (REV)—to help support New York’s aggressive decarbonization goals (NYPSC, 2016). I will discuss REV separately below.

The use of MYRPs in New York was partially stimulated by a desire to improve incentives but also to reduce the administrative burden of the increasing frequency of rate cases for six IOU electric distribution utilities along with the NYPSC’s other regulatory responsibilities (gas distribution, water, steam, intra-state telecommunications, and oversight of cable TV). New York had also been using future test years to set rates in general rate cases for many years, so it had considerable forecasting experience.

MYRPs in New York use external inflation indices to adjust the O&M components of prices between rate cases, and have several contingencies that trigger reopeners or pass-throughs for extraordinary costs or costs that are hard to forecast (Synapse Energy Economics, 2019, p. 15). The New York commission has adopted one-way (e.g., excess) earnings or profit-sharing mechanisms (Lowry et al., 2017, p. 6.16). There are service-quality PIMs and energy-efficiency PIMs. NYPSC has adopted revenue decoupling as well.

A plan that was adopted by the Maine Public Utilities Commission (MPUC) to regulate Central Maine Power provides an interesting case in which a state regulatory agency adopted MYRPs, but then concluded that the MYRPs that it was using had not yielded the benefits that had been anticipated (Lowry et al., 2017, Sect. 6.1). The plan was in operation from 1995 until 2013 in three cycles and then abandoned until very recently. The plans used inflation escalators for revenue requirements between rate cases but gave the company unusual rate design and marketing flexibility. They contained productivity offsets (X factors) and also included service-quality PIMs and energy-efficiency PIMs.

The MPUC was not satisfied with Central Maine Power’s performance under the plan, and the company returned to more traditional COSR regulation in 2014. In June 2023 the MPUC approved a new MYRP for Central Maine Power (MPUC, 2023), which was agreed-to through a settlement process (as were the earlier plans). The term is two years, and the annual revenue adjustments are fixed ex ante and are not adjusted with inflation indices. The plan focuses on a variety of service-quality PIMs and continues the existing revenue-decoupling mechanism. It contains an earnings-sharing mechanism as well, which shares earnings deviations from a benchmark level between the utility and its customers.

Massachusetts, Hawaii, Minnesota, Vermont, Rhode Island, and Maryland have adopted MYRPs in the spirit of RPI-X. Other states are considering doing so or are in the process of designing MYRP mechanisms (e.g., North Carolina, Colorado, Connecticut, Nevada, and Arizona). A few other states have considered doing so and decided against MYRPs (e.g., Michigan). Hawaii adopted an MYRP as part of a very comprehensive PBR plan in December 2020. I will outline its components at the end of this section.

I turn finally to formula rate plans: As was discussed above, formula rate plans are MYRPs that allow utilities to adjust their rates between regulatory reviews based on their own actual costs incurred rather than on exogenous input price indices and productivity benchmarks. This allows utilities to maintain their earnings within a rate-of-return-on-equity band that was established in a previous rate case.

Most of the pure formula rate plans have operated in states in the South. For example, Alabama Power has operated with a formula rate plan in the past. Critics have pointed out that under this plan, as of 2013, Alabama Power did not have a formal contested rate hearing in 30 years so that it received virtually automatic recovery of the costs that it occurred without external benchmarks or regulatory lag (Schlissel and Sommer, 2013). Formula rate plans have worse efficiency properties than COSR in practice.

4.2.4 Performance Plans for New Initiatives and Pilot Programs

Some commissions have introduced an ad hoc set of additional performance incentives that have been targeted at specific initiatives so as to give the distribution utilities incentives to experiment with adapting to state climate policies and changes in the structure of the electric power industry.

New York’s Reforming Energy Vision (REV) framework is an example. While I think that there is more hype than substantial regulatory reform in this regulatory framework in practice, it does represent an important view of: the changing business model for distribution utilities in the era of growth of DER; distribution level storage; non-wires options for responding to distribution system reliability and congestion issues; and a growing interest in some states in spurring third-party solutions to grid development needs that are allowed to compete with the incumbent distribution utility’s proposals.

REV seeks to motivate distribution companies to view themselves as a “platform” on which third-party suppliers of various distribution-level services can compete with the distribution company When a third party is selected to provide the services, the distribution company receives a financial incentive to compensate it for an estimate of its lost profits from choosing a third party to meet the need. The NYPSC envisions that the revenues and earnings from these third-party services will grow over time.Footnote 36

The primary example of the application of REV is the pilot Brooklyn-Queens demand management program that was adopted by ConEdison as an alternative to additional investments in its distribution system to remediate forecast reliability issues in this area due to growing electricity demand. Rather than the costs of the demand management program being a direct pass-through into distribution rates, the costs are to be capitalized, rate-based, amortized over 10 years, and eligible for a return on the sum capitalized. In essence, ConEdison can recover and earn a return on these expenditures over a 10-year period.

As was already noted above, many other utilities in the U.S. have similar PIMs for energy-efficiency program expenses (Lowry et al., 2017, Sect. 6.16),Footnote 37 so this is not quite as innovative as the NYPSC seems to think. I suppose that the idea here is to expand this approach to a wider set of potential distribution “platform” projects and additional projects are being reviewed or have now been approved by the NYPSC.Footnote 38

Another example is a similar “Non-Wires Alternative Requirement” pilot program in California. The utility that hosts a project would now be allowed to charge a fee of 4% of the cost of non-wires alternatives that are selected through competitive solicitations (NREL, 2017, p. 63).Footnote 39

A third example is the incentive arrangement that is being provided to the three IOU distribution companies in Massachusetts, so as to encourage them to agree to manage competitive solicitations for long-term renewable energy contracts for hydroelectric energy from Canada, solar, onshore wind, and offshore-wind and to serve as the counterparty buyer under the long-term contracts that are selected through the competitive solicitations for these carbon-free energy supplies.Footnote 40

Ordinarily, purchased power costs would be treated as a cost pass-through that is subject to the standard prudence/reasonableness review contingencies. Commitments to enter into large long-term contracts that involve taking-on a potentially significant contractual liability and creates potential regulatory risks down the road if the contract price turns out to be above the competitive market price. New England has a very competitive wholesale energy market that is managed by ISO-NE, and Massachusetts has retail supply competition and municipal aggregation; the distribution companies have already lost a significant fraction of their retail energy supply customers—providing the latter with regulated distribution delivery services only.

For example, Eversource—the largest distribution company in Massachusetts—supplies only about 20% of the energy that is consumed by its distribution service (delivery) customers. As a result it may not really “need” as much energy to serve customers or to meet its renewable energy obligations as it is contracting for under these 20-year contracts.Footnote 41

Under the MDPU regulations that are associated with these contracts, however, the utilities would receive a fee for taking on these contractual obligations. The fee is 4% of the cost of the energy that is supplied under the contract.Footnote 42 In addition, the distribution utilities can resell the contracted energy in the ISO-New England wholesale markets and recover any losses that reflect the difference between contract prices and wholesale market prices (or credit any gains) as an additional non-bypassable distribution wires charge. (Eversource still supplies all retail customers with distribution services whether they have chosen a competitive energy supplier or not.)

Basically, the state is leaning on the balance sheets of the distribution utilities and on their distribution service customers in order to support the long-term contracts for renewable energy that the state thinks it needs to meet its decarbonization commitments.

A fourth example is the CPUC’s May 2022 approval of special funding for four residential and commercial pilot programs to examine the costs and benefits of using electric vehicle batteries to supply electricity to homes and businesses during blackouts and as suppliers to the grid (bi-directional charging).Footnote 43 Hawaii and Vermont have also undertaken interesting pilots. If the pilot works well, it could become a standard program with an associated PIM.

4.3 Putting the Components Together to Create a Comprehensive PBR Mechanism

A comprehensive PBR mechanism would put all of these components together into a single integrated package. The multi-year PBR plan that was adopted by Hawaii at the end of 2020, effective June 1, 2021, and to be applied to Hawaiian Electric puts all of these building blocks together: Hawaii—along with Massachusetts, New York, and California—has perhaps the most comprehensive PBR plan in the U.S.Footnote 44

The state of Hawaii has a made a commitment for 100% of its electricity to be generated from renewable sources by 2045.Footnote 45 In 2022, 31.8% of Hawaii’s electricity was generated from renewable sources—the largest fraction of which comes from customer-sited solar PV and wind generation. Hawaiian Electric also manages a competitive procurement program for grid-based solar, wind, and other renewable resources (e.g. geothermal) to help to meet the aggressive decarbonization requirements that currently accounts for a little more than half of Hawaii’s renewable generation.Footnote 46

The Hawaii PBR plan (PUCH 2020) has many similarities to plans that have or are in the process of being implemented in Massachusetts, New York, California, and other states. The plan’s main provisions are summarized in Table 2.Footnote 47