Abstract

In this paper we propose a new methodology for the estimation of fundamental property asset-level investment time series performance and operating data based on real estate investment trusts (REITs). The methodology is particularly useful to develop publicly accessible operating statistics for investment real estate, such as income or expenses per square foot. Commercial property operating statistics are relatively under-studied from an investment perspective. We show how the methodology can be used to estimate the time series of property values, net operating income, cap rates, operating expenses and capital expenditures, per square foot of building area, by property type (sector) at the quarterly frequency for multiple specific geographic markets from 2004 through 2018. We show illustrative empirical results for Los Angeles offices and Atlanta apartments. The methodology allows estimation of actual quantity levels, not just dimensionless index numbers (longitudinal relative). It allows for an “additive” model structure that is more parsimonious, thereby addressing the need for granular market segmentation. We also introduce a Bayesian framework that allows the estimation of reliable time series even in small markets.

Similar content being viewed by others

Notes

Two existing sources of commercial property operating data are noteworthy: the Building Owners & Managers Association (BOMA), and the National Council of Real Estate Investment Fiduciaries (NCREIF). While useful, these sources leave room for a new contribution. BOMA is not focused on the investment industry and lacks investment performance statistics. And the properties represented in both the NCREIF and BOMA data sources are somewhat special subsets of the broader population of medium-to-large scale (so-called “prime” or “Class A”) investment property in the United States. For example, many of the properties covered by BOMA or NCREIF are owned or held by corporate users or private funds with deep pockets and unique objectives and constraints. Their optimal management may differ from that of other types of investors including in particular REITs, who tend to hold properties long term for maximization of total return.

In this paper we use the terms “commercial real estate” and “investable real estate” interchangeably and as defined by Real Capital Analytics Inc. The definition refers to properties that are owned and traded for investment purposes (including private rental apartments), excluding corporate and owner-occupied properties, and that are valued at at-least $2.5 M, thereby excluding “mom-and-pop investor” properties. Almost half of the total $1.5 T REIT holdings consists of the four major traditional investment property sectors that also dominate in the NCREIF portfolio: office, industrial (warehouse), retail, and apartments.

Many NCREIF properties are held in closed-end funds that have finite lifetimes typically of 7 to 10 years, or in open-end funds where investors can cash out their units with relatively short notice. Most NCREIF properties are owned ultimately by deep pocket tax-exempt institutions, whereas REIT-owned properties are ultimately subject to income tax paid on dividends and realized capital gains by taxable investors in REIT stocks which include not only institutions but also individual retail investors.

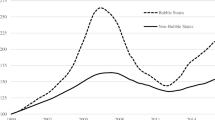

A big picture perspective on the relationship between REIT based real estate investment performance versus appraisal based can be obtained by higher level, less formal analyses of REIT returns, as exemplified in Riddiough et al. (2005).

The EV largely reflects the stock market capitalization of the firm’s equity, plus the value of the firm’s debt, including mortgages. Although the debt is valued at book value, in general debt book value corresponds closely to market value of the debt.

The only exception is in the purely additive specification we label “time + pt + loc” where parameter µ is already a common trend in itself. In this case κ replaces µ.

Economic statisticians draw a distinction between “value” and “price” in which value equals price times quantity and can change over time due either to change in price or change in quantity, whereas price reflects a constant quantity. In the case of a complex good like real estate, “quantity” effectively includes many quality dimensions. For example, the “value” of a building that sold at two points in time could change in part to reflect the aging of the building, reflecting a depreciation or reduction in the “quantity” of building, and such change in value in itself would not represent a “price” change in the economic statistics terminology. The “price” versus “value” distinction is different in real estate, where “price” refers to a transaction of exchange of ownership, while “value” may refer to a “valuation” estimated or indicated by some source, such as in our case, the stock market share prices of REITs. In this paper we use the two terms somewhat interchangeably, though in the present section we are attempting to introduce the distinction.

See Table 2 (below) for a list of the 15 metros and their weights in the representative property.

In practice, “forward-looking” cap rates are most common, based on Year “t + 1” NOI and end of Year “t” property asset valuation, though “backward-looking” cap rates (based on Year “t” NOI and end of Year “t” property asset valuation) are also employed. In our results, effectively, our yields are backward-looking.

We use the SNL variable labeled “Property Size”, which is defined as the total interior area of the building or buildings in square feet.

Comparison of our base “level” specification with a GK based index historically published by NAREIT confirms that our base results are consistent with the GK methodology.

These averages are based on the time + pt + msa and time x pt + msa models only, as these give the most realistic looking results.

The variable where this would happen the most is our OPEX variable. In total we observe 120 NNN leases, where the tenant pays the OPEX.

References

Betancourt, M., & Girolami, M. (2015). Hamiltonian Monte Carlo for hierarchical models. Current Trends in Bayesian Methodology with Applications, 79, 30.

Bokhari, S., & Geltner, D. (2019). Commercial buildings capital consumption and the United States national accounts. Review of Income and Wealth, 65, 561–591.

de Haan, J., & Diewert, W. E. (2011). Handbook on residential property price indexes, chapter Hedonic regression methods, 50–64 (Eurostat Methodologies & Working papers).

Feng, Z., & Liu, P. (2021). Introducing “Focused Firms”: Implications from REIT prime operating revenue. The Journal of Real Estate Finance and Economics, 67, 545–578.

Francke, M. K., & DeVos, A. F. (2000). Efficient computation of hierarchical trends. Journal of Business and Economic Statistics, 18, 51–57.

Francke, M. K., & Van de Minne, A. M. (2017a). The hierarchical repeat sales model for granular commercial real estate and residential price indices. Journal of Real Estate Finance and Economics, 55, 511–532.

Francke, M. K., & van de Minne, A. M. (2017b). Land, structure and depreciation. Real Estate Economics, 45, 415–451.

Gelman, A. (2006). Prior distributions for variance parameters in hierarchical models (comment on article by browne and draper). Bayesian Analysis, 1, 515–534.

Geltner, D., & Kluger, B. (1998). REIT-based pure-play portfolios: The case of property types. Real Estate Economics, 26, 581–612.

Geltner, D., & Ling, D. (2006). Considerations in the design and construction of investment real estate research indices. Journal of Real Estate Research, 28, 411–444.

Geltner, D., & Van de Minne, A. M. (2017). Do different price points exhibit different investment risk and return commercial real estate. Journal of Portfolio Management, 43, 105–119.

Hoffman, M. D., & Gelman, A. (2014). The No-U-turn sampler: Adaptively setting path lengths in Hamiltonian Monte Carlo. Journal of Machine Learning Research, 15, 1593–1623.

McMillen, D. P. (2008). Changes in the distribution of house prices over time: Structural characteristics, neighborhood, or coefficients? Journal of Urban Economics, 64, 573–589.

Riddiough, T. J., Moriarty, M., & Yeatman, P. J. (2005). Privately versus publicly held asset investment performance. Real Estate Economics, 33, 121–146.

Van de Minne, A. M., Francke, M. K., Geltner, D. M., & White, R. (2020). Using revisions as a measure of price index quality in repeat-sales models. Journal of Real Estate Finance and Economics, 60, 514–553.

Acknowledgements

We thank Brad Case, Lora Dimitrova, Jefferson Duarte, Louis Johner, Mariya Letdin, and conference and seminar participants at the 2023 AREUEA National Conference, 2023 FMA European Conference, 2023 International Conference of the French Finance Association (AFFI), 2023 PennState International Conference on Empirical Economics, 2022 Real Estate Markets and Capital Markets (ReCapNet) Conference, 2022 REALPAC/Toronto Metropolitan University Research Symposium, 2021 AsRES/GCREC/AREUEA Joint Real Estate Conference, KTH Royal Institute of Technology, and IESE Business School for their helpful comments. Kumar gratefully acknowledges support from the Danish Finance Institute (DFI). The views expressed herein are those of the authors and all errors remain our own.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing Interests

We confirm that authors do not have conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix. Bayesian Model Details

Appendix. Bayesian Model Details

In this Appendix we will detail the Bayesian model estimation. In order to estimate the model efficiently (i.e. with fast convergence) we log transform the left-hand side variable in all models before running the No-U-Turn-Sampler (NUTS). Logging the dependent variable ensures that the estimated parameters are closer to normally distributed without any large values. To ensure that we do not lose observations due to log transforming zero entries, we add a very small (1E-6) number to our yields.Footnote 13 Unfortunately, this does mean that the estimated parameters cannot be easily interpreted. (Note that we do not log transform the right-hand side.) However, in this study, we do not focus on said parameters, but on the fitted values of our representative property. The trends are calculated by looking at (the exponentiated) fitted values over time of a “representative property”. As explained in “Methodology” section, we also add a common trend to the models. Log transforming the left-hand side, and adding a common trend (κ) results in the following Bayesian models;

where;

Within each cluster the estimate 1 variance parameter. Another pro of estimating the model with the log on the left-hand side, is that we can keep the same priors irrespective of the left-hand side variable. Indeed, the average values (and thus priors) are vastly different for enterprise value per square foot, compared to for example cap rates in levels, but not so much in logs. We thus draw parameter κt=1 from a very uninformative prior (i.e. N (0,10)), whereas the other parameters are largely uninformative (N (0,1)) (Gelman, 2006). The random walks in state Eq. (4), are modelled in first differences, in line with Betancourt and Girolami (2015). The innovations of the random walks have a prior of N (0,1).

We have 2,000 iterations, of which the first half are used as warm-up, over 3 chains. All convergence statistics (\(\overline{R }\) and effective sample sizes, not presented here, but available upon request) are satisfactory.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Geltner, D., Kumar, A. & Van de Minne, A.M. Estimating Commercial Property Fundamentals from REIT data. J Real Estate Finan Econ (2023). https://doi.org/10.1007/s11146-023-09962-z

Accepted:

Published:

DOI: https://doi.org/10.1007/s11146-023-09962-z

Keywords

- Real estate price indices

- Commercial real estate

- REITs

- Structural time series modelling

- Bayesian inference

- Real estate operating statistics

- Capital expenditures

- Operating income and expense