Abstract

We study the effects of firm-level microeconomic fluctuations on aggregate productivity in the United Kingdom. We show that a standard measure of residual productivity growth of the largest UK firms (the ‘granular residual’) produces results that are partly counter-intuitive and statistically insignificant. To combat this, we propose a refinement to the widely used control function approach to estimating technology shocks in a production function, which is aimed at accounting for firm-level heterogeneity and the potential existence of common shocks. Using this approach, we find that idiosyncratic firm-level shocks matter for the UK; the ‘granular residual’ can explain around 30% of aggregate UK productivity dynamics. We also show that simplifications of our approach, which do not control for firm-level heterogeneity and the existence of common shocks, do not perform well empirically, highlighting the importance of identifying firm-specific shocks correctly in order to properly test the ‘granularity hypothesis’.

Similar content being viewed by others

Notes

See, for example, Jorda et al. (2013) and Cerra and Saxena (2008). Explanations for the UK’s weak productivity dynamics in the aftermath of the financial crisis have highlighted issues around labour hoarding, misallocation of labour and capital (see e.g. Barnett et al. (2014b) and Oulton and Sebastia-Barriel (2017)), an elevated number of ‘zombie firms’ (see e.g. Carney (2017)), and increased firms’ power in product and factor markets (see e.g. Haldane (2018)). Furthermore, Tenreyro (2018) and Mason et al. (2018) offer evidence pointing to the importance of very few sectors in driving weak productivity growth in the UK, with finance and manufacturing being the largest contributors, and Schneider (2018) argues that the weakness has been driven by shortfalls in the top quartile of the productivity distribution.

Di Giovanni et al. (2014) and Friberg and Sanctuary (2016) find significant effects of firm-level shocks for France (explaining 80% of the variation in total sales growth) and Sweden (explaining 52% of the variation in total sales growth), respectively, while Gnocato and Rondinelli (2018) find that idiosyncratic TFP shocks to large firms explain around 30% of aggregate TFP volatility in Italy. However, a recent paper by Gutierrez and Philippon (2019) finds that the contribution of shocks to the largest firms has become much smaller in the last decade compared to preceding decades. In similar vein, Yeh (2021) finds that the GR contribution to the variation in US GDP growth is only 15%, when properly accounting for the lower volatility of the larger firms.

Another popular decomposition is that of aggregate TFP proposed by Levinsohn and Petrin (2012). We could not implement this decomposition as we do not have the data required for this exercise readily available in the dataset we use in this paper.

Appendix B provides a description of the data used in the analysis throughout this paper.

By contrast, the Levinsohn and Petrin (2012) decomposition of aggregate TFP growth, for example, makes several simplifying assumptions in order to identify such shocks, namely that the production functions have constant returns to scale and are separable in intermediate inputs and value-added, and that output and input markets are perfectly competitive, in addition to the assumed cost-minimising behaviour on the part of firms. The approach we use does not rely on these assumptions.

See Baqaee and Farhi (2019) for a more detailed discussion.

See Section 7 in Baqaee and Farhi (2019).

Gabaix (2011) also considers an alternative de-meaning procedure, where the average productivity is computed within the industry a given firm belongs to (instead of amongst the set of K largest firms). This yields results that are very similar to those obtained under his benchmark approach, which we thus focus on here.

Using the same data (sample 2004–2018) as in the previous section, we find that for the UK these correlations are positive, but not close to 1. The correlation coefficient between \(G{R}_{t}^{B}\) and \(G{R}_{t}^{E}\) is 0.68 and between \(G{R}_{t}^{B}\) and ΔΦt it is 0.17.

Assuming that the aggregation production function is Cobb-Douglas and that there is constant factor utilisation, real GDP growth is given by Δyt = ΔTFPt + αΔkt + (1 − α)Δlt where α denotes the labour share of total income, and yt, kt, and lt denote (the log of) real GDP, aggregate capital, and aggregate labour. Aggregate labour productivity growth is given by Δyt − Δlt = ΔTFPt + α(Δkt − Δlt). It is thus to be expected that real GDP growth, TFP growth, and aggregate labour productivity growth will be positively correlated. For instance, the correlation coefficient between aggregate labour productivity growth and TFP (GDP) growth in the UK over 1970-2016 was 0.96 (0.76).

In all the analysis that follows, we use SIC 1-digit sectors to maximise the sample size, but the results are also robust to a somewhat smaller sample with SIC 2-digit sectors. This is reassuring since in some settings, the depth of the sector splits can matter; see e.g. Blackwood et al. (2021).

Although conceptually debatable, this assumption has been commonly made in the recent literature on estimating production functions. More generally, as much as possible, we conform to the data choices made in the original paper, including using fixed assets as the measure of capital. There is currently a lively debate on whether and how to expand on the definition of firm–level capital stocks to include measures of intangible capital; however, given the measurement challenges related to this, we consider it to be beyond the scope of this paper. See also Appendix B for more details on the data.

Strictly speaking, we are really measuring revenue TFP (TFPR), as in the absence of firm–level price data, the true underlying measure of firm–level technological progress cannot be estimated. This is a caveat to keep in mind in any analysis that uses these types of approaches, and implies that the TFP measure may include a demand shock component (see Barterlsman and Wolf (2018)).

Lee, Stoyanov and Zubanov (2019) elaborate on this point more thoroughly. They find that controlling for firm-specific fixed effects outperforms the standard control function estimation approach in terms of capturing persistent unobserved heterogeneity in firm productivity.

In principle, there is no reason why the loading in the μt needs to be unitary. For example, Gabaix and Koijen (2019) consider a more general specification in a factor model set-up. They assume that the loading on μit is a function of known firm-specific obervarbles, namely the firm’s size. This approach is challenging to implement in our setup due to the relatively small sample size. We do, however, consider a case where we allow for a heterogeneous effect of the common shock across firms within a given sector that is dependent on the firms’ level of market capitalisation. More specifically, we set a threshold dummy to equal 1 if firm i had above-median market capitalisation within its sector at time t − 1. In this case, the common shock may have a differential effect on firms depending on their market capitalisation, consistent with the idea that a listed firm’s “beta” (in the context of a CAPM model) may be correlated with its level of market capitalisation. This assumption is rather ad hoc, which is why we do not present the model here, but the results are broadly similar (and slightly better) in terms of the statistical significance of the GR to those presented below for our preferred model.

For details of the mechanics of the exercise, see Appendix A.

The results shown in Fig. 4 are based on the ONS Business Structure Database, which provides an annual snapshot of around 2–2.5 million UK firms.

This finding is also corroborated by the so-called sales herfindahls, which measure the variation of firm-level turnover. We find very similar values (5–8%) for the UK over the past 20 years as Gabaix (2011) found for the US, which suggests that the distribution of UK firms is sufficiently skewed for idiosyncratic volatility of large firms to be macroeconomically relevant.

By construction, using total turnover results in the highest ratio in any given year.

We use the Thomson Reuters Worldscope dataset for this analysis. See Appendix B for details.

More specifically, we exclude SIC07 section K (‘Financial and insurance activities’) and division 19 (‘Manufacture of coke and refined petroleum products’). Intuitively, the exclusion of financial and insurance activities is related to the idea that ’granular shocks’ as conceived in this setup are very difficult to estimate for those firms, as the “sales” of financial firms do not align well with the meaning ("gross output”) used in this paper. We exclude the manufacture of coke and refined petroleum products as the large fluctuations of global oil prices are likely to render our estimates of Shockit a poor proxy for the actual idiosyncratic shock to firm productivity. Although Gabaix (2011) additionally excluded the energy sector as a whole, we do not deem this to be necessary in the case of the UK, as the shocks to the largest firms in this sector we identify are not positively correlated with global energy prices, potentially because these firms generally have a strong domestic focus.

We have also carried out the analysis using the same sample for all the models, i.e., a somewhat smaller sample for which all the required data is available to estimate all of the five models listed in Table 1. The results are not presented here, but they are very similar to the main results presented below.

The aim of the regressions is not to find the best possible fit for modelling UK aggregate productivity; clearly, other explanatory variables would be important in such an exercise. Rather, the aim is to study the relevance of the GR terms alone—which should be a composite of idiosyncratic, exogenous disturbances which in principle require no control variables—similarly to Gabaix (2011).

If we use a similar shorter sample with the Worldscope data, the R-squared is 0.14 and contemporaneous correlation between productivity growth and the benchmark GR is 0.11. Note that this is not fully comparable with the ONS data, which has a narrower sector coverage and a more extensive firm coverage (i.e. many smaller firms, whereas we focus only on the largest firms) than preferred for our purposes.

It is worth noting that this is driven by pre-GFC dynamics.

We also examined how the within–year variation of the GR contributions of the top 100 firms has changed over time to see whether there are large outliers in particular time periods. However, there is no clear pattern in this variation over time, which reassures us that the GR dynamics are not driven by a small number of very large firms.

Recall that for Models 3–5, the input data and hence the sample of firms is identical for each year, whereas it is slightly different for Models 1–2. However, this distinction for Models 3–5 makes no difference for the correlations in Table 2.

For brevity, we do not report these results here. They are available from the authors upon request.

The results of the exercise are robust to different firm size samples, including ones consisting of millions of firms. Due to the prohibitively long simulation times of samples of very large firms, here we show the results for a sample of 100,000 firms.

Note that this is the general case of Model 5 introduced in the main text, as we need to allow for some randomness in the simulation to make it plausible.

References

Ackerberg DA, Caves K, Frazer G (2015) Identification properties of recent production function estimators. Econometrica 83(6):2411–2451

Baqaee D, Farhi E (2019) The macroeconomic impact of microeconomic shocks: beyond Hulten’s theorem. Econometrica 87(4):1155–1203

Barnett A, Batten S, Chiu J, Franklin J, Sebastia-Barriel M (2014a) The UK productivity puzzle. Bank of England Quarterly Bulletin, 2014Q2

Barnett A, Chiu J, Franklin J, Sebastia-Barriel M (2014b) The productivity puzzle: a firm-level investigation into employment behaviour and resource allocation over the crisis. Bank of England Working Paper, No. 495

Bartelsman E, Wolf Z (2018) “Measuring productivity dispersion”, In: Grifell-Tatjé E, Lovell CA, Sickles RC (eds), The Oxford handbook of productivity analysis. Oxford University Press, United States of America

Blackwood G, Foster L, Grim C, Haltiwanger J, Wolf Z (2021) Macro and micro dynamics of productivity: From devilish details to insights. Am Econ J Macroecon 13(3):142–172

Carney M (2017) Policy panel: investment and growth in advanced economies. Speech at 2017 ECB Forum on Central Banking, Sintra, Portugal

Cerra V, Saxena SC (2008) Growth dynamics: the myth of economic recovery. Am Econ Rev 98(1):439–457

De Loecker J, Warzynski F (2012) Markups and firm-level export status. Am Econ Rev 102(6):2437–2471

Di Giovanni J, Levchenko A, Mejean I (2014) Firms, destinations, and aggregate fluctuations. Econometrica 82(4):1303–1340

Friberg R, Sanctuary M (2016) The contribution of firm-level shocks to aggregate fluctuations: the case of Sweden. Econ Lett 147:8–11

Gabaix X (2011) The granular origins of aggregate fluctuations. Econometrica 79(3):733–772

Gabaix X, Koijen RSJ (2022) Granular instrumental variables. NBER Working Paper, No. 28204

Gnocato N, Rondinelli C (2018) Granular sources of the Italian business cycle. Banca D’Italia Working Papers, No. 1190

Goodridge P, Haskel J, Wallis G (2018) Accounting for the UK productivity puzzle: a decomposition and predictions. Economica 85:581–605

Gutierrez G, Philippon T (2019) Fading stars. NBER Working Paper, No. 25529

Haldane A (2018) Market power and monetary policy. Speech at the Federal Reserve Bank of Kansas City Economic Policy Symposium, Jackson Hole, Wyoming, United States of America

Jorda O, Schularik M, A. Taylor (2013) When credit bites back. J Money Credit Banking 45(2):3–28

Lee Y, Stoyanov A, Zubanov N (2019) Olley and Pakes style production function estimators with firm fixed effects. Oxford Bull Econ Statistics 81:79–97

Levinsohn J, Petrin A (2012) Measuring aggregate productivity growth using plant-level data. RAND J Economics 43(4):705–25

Lin S, Perez MF (2014) Do firm-level shocks generate aggregate fluctuations? Mimeo, United States of America

Mason G, Mahoney M, Riley R (2018) What is holding back UK productivity? Lessons from decades of measurement. Natl Inst Econ Rev 246(1):24–35

Melitz M, Polanec S (2015) Dynamic Olley-Pakes productivity decomposition with entry and exit. RAND J Econ 46:362–375

Oulton N, Sebastia-Barriel M (2017) Effects of financial crises on productivity, capital and output. Rev Income Wealth 63(1):90–112

Riley R, Rosazza-Bondibene C, Young G (2015) The UK productivity puzzle 2008-13: evidence from British businesses. Bank of England Working Paper, No. 531

Schneider P (2018) Decomposing differences in productivity distributions. Bank of England Working Paper, No. 740

Tenreyro S (2018) The fall in productivity growth: causes and implications. Speech at Peston lecture theatre. Queen Mary University of London, United Kingdom

Yeh C (2021) Revisiting the origins of business cycles with the size-variance relationship. Mimeo, United States of America

Acknowledgements

We would like to thank Xavier Gabaix, John Moffat and Ricardo Reis for the useful discussions. We would also like to thank participants at the 2019 Scottish Economic Society Conference in Perth, UK, the 2019 EWIPA conference in London, UK, the 2019 North American Econometric Society Conference in Seattle, USA and the 2019 African Econometric Society Conference in Rabat, Morocco, as well as three anonymous referees for their useful comments. The views expressed in this paper are those of the authors, and not necessarily those of the Bank of England or its committees. Nikola Dacic’s contribution to this paper was done while he was employed by the Bank of England. This work contains statistical data from ONS which is Crown Copyright. The use of the ONS statistical data in this work does not imply the endorsement of the ONS in relation to the interpretation or analysis of the statistical data. This work uses research datasets which may not exactly reproduce National Statistics aggregates. We remain solely responsible for the contents of this paper and any errors or omissions that could remain.

Author information

Authors and Affiliations

Corresponding authors

Ethics declarations

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix A. Simulation exercise

We conduct a simulation exercise in a hypothetical economy consisting of N = 100,000 firmsFootnote 32, where we then randomly draw the employment shares of the firms from a Zipf distribution to conform to the power law requirement of the GR discussed in the main text. We allow the firms to be hit by random idiosyncratic and common productivity shocks (described below in more detail), and calculate the GR measure for the largest 100 firms based on Models 1 and 5 in the main text. Finally, the aggregate whole–economy productivity growth rate is then regressed on the different GR measures to estimate the significance of the GR coefficients and the (adjusted) R2 of the regressions. In the results shown below, we assume that there are L = 1000 loops of the simulation, and each loop consists of T = 100 time periods.

We want to match the definitions of the shock processes as closely as we can with models 1 and 5 introduced in the main text. First, to simulate a world where there are no idiosyncratic shocks, we assume that firm-level productivity (or TFP) ωit follows an AR(1) process of the following form:

where (unlike in the empirical models we use in the main text) we assume that ρ = 1 for simplicity. There is also a shock common to all firms, μt. β is the coefficient on the common shock, which is here allowed to be random, rather than 1.Footnote 33 We also allow for a firm fixed–effect ci, although in practice, this has very little effect on the results. The common shock is drawn from a N(1, 1) distribution, which implies an average growth rate of the economy of 1%. The intuition of the model in equation (A1) is that since there are no idiosyncratic shocks, a correctly estimated GR should be zero.

Second, we simulate a more general version of the model, but now allowing for idiosyncratic, firm–specific shocks χit:

We also allow for two versions of this model; one where the idiosyncratic shocks are drawn from a N(0, 1) distribution, and one where they are drawn from the same distribution, but the size of each shock is divided by 10. We do this because we want to examine what the effect of the relative size of the idiosyncratic vs the common shock is on the significance of the GR.

To calculate aggregate productivity in this example, we again use the Melitz and Polanec (2015) definition at time t:

where the employment shares sit ≥ 0 sum to 1 and ϕit denotes the log of firm i’s productivity at time t. For simplicity, we will assume that the firm employment (si) stays constant over time.

With these simulated results, we then calculate the GR for the largest 100 firms for each time period, using Model 1 for equation (A1), and Model 5 for equation (A2). Finally, we estimate an OLS regression that has the following form, for each of the 1,000 loops (and where the sample size is T = 100 for each loop):

where ALPt is aggregate productivity growth at time t, c is a constant, GRt is the relevant GR measure and et is an i.i.d. error term.

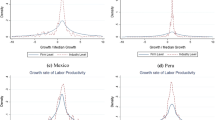

Figures 10 and 11 show the main results in terms of the estimated adjusted R2 for each of the 1,000 loops of the simulation, for the three types of shock processes. There are a number of points worth highlighting:

-

First, the exact shape of the Zipf law distribution can cause significant volatility in all the GR estimates, as suggested by the fact that the GR estimates are much more volatile in Fig. 10 (which draws the firm sizes again for each loop, though not for each t) than in Fig. 11 (which keeps the firm sizes fixed so that the share of the largest 100 firms is around 0.3, which is the average share in Fig. 10).

-

Second, even though we know the the GR for the case with the common shock only should be zero by construction, Model 1 shows a significantly positive GR throughout the 1,000 loops (with an average of 0.32 for the case with random firm sizes, and 0.22 for the fixed firm sizes).

-

Third, Model 5 detects a significantly positive GR (with an average of 0.23 for the case with random firm sizes, and 0.22 for the fixed firm sizes) for the idiosyncratic shock, when this shock is relatively variable compared to the common shock, but detects a GR that is effectively 0, when the shock is relatively less variable – just as would be expected based on the definition of Model 5.

Simulation results for adjusted R2 – random firm size

Simulation results for adjusted R2 – fixed firm size

Appendix B. Data

Data used in various parts of our analysis comes from three data sources: Refinitiv Worldscope, Office for National Statistics (ONS) Business Structure Database (BSD), and OECD/ONS labour productivity data. This appendix describes the data we use from these datasets in detail.

Worldscope from Refinitiv is a proprietary dataset that includes financial account information on large (mainly listed) UK firms since the 1980s. For our analysis, we use data on the following variables:

-

Turnover for the largest firms for each year. Where data on international turnover exists, we compute domestic turnover as the difference between total and international turnover. This is more comparable with how national aggregates are constructed, given the nature of the UK as a small, open economy.

-

Employment, used as the denominator in the firm-level labour productivity calculation. For those firms that report international sales, we assume—given lack of data—that the share of domestic employment in total employment is the same as the share of domestic turnover in total turnover. This will affect the employment weights of the individual firms, where applicable. However, this results in productivity (turnover divided by employment) being the same, whether measured by total turnover and employment or by their domestic counterparts. Given data limitations, we think this is a reasonable (and only available) choice.

-

Cost of goods sold, used as a measure of variable costs in the control function approach to estimating production functions.

-

Net property, plant and equipment as a measure of firm–level capital.

Turnover, cost of goods sold and firm–level capital are deflated with the aggregate ONS GDP and gross fixed capital formation deflators.

Importantly, we have noticed a number of mistakes in the Worldscope data on employment and international sales (and to a lesser extent, cost of goods sold). Intuitively, employment and international sales are not financial account items, which likely explains the presence of errors in the recording of it in the Worldscope dataset. While correcting for all mistakes in the entire data would not be feasible, we have gone through the largest errors for those firms that contribute most to the dynamics of the GR measures and replaced the erroneous observations with the correct ones from the annual reports of the firms in question, when these have been available. In particular, the number of corrections we do are the following:

-

Cost of good sold; corrections for 10 firms.

-

International sales; corrections for 70 firms.

-

Employment; corrections for 30 firms.

It is worth emphasising that after these corrections, we consider the data to be of good quality for the analysis we are carrying out. There is no reason to doubt the vast majority of data on turnover, cost of goods sold and firm–level capital, as these are recorded in firms’ financial accounts. The employment data is of lower quality, but we do not rely on it for our main results in any case.

BSD covers the universe of all UK enterprises, based on an annual snapshot from the Inter-Departmental Business Register (IDBR). On average, there are over 2 million enterprises annually in the BSD. In the IDBR, turnover is updated via administrative sources (HMRC VAT and PAYE records) and ONS Business Surveys. We use enterprise level turnover for calculating the power law distributions, based on the BSD vintage of 2017.

To calculate the productivity contributions of the largest firms for the Melitz and Polanec (2015) methodology, we use the ONS ARD database. This database includes firm-level financial account data based on the Annual Business Inquiry (ABI), Annual Business Survey (ABS) and employment data based on the Business Register and Employment Survey (BRES). We use reporting unit level turnover and employment data to calculate estimates of turnover productivity. Note that the data is only available for 2004–2018, with methodological breaks during this period, so the results should only be seen as indicative and motivating the main analysis using the Worldscope data. Importantly, we cannot use this dataset in our proposed control-function approach as there exists no data on fixed capital in the ARD database.

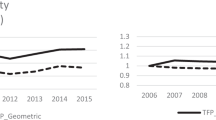

ONS labour productivity data is used for the regressions reported in Tables 3–5, where aggregate labour productivity (output per head) is the independent variable. In addition to this, Fig. 1 uses OECD data on hourly labour productivity for selected economies. All the ONS and OECD aggregate data is publicly available.

Rights and permissions

Springer Nature or its licensor holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Dacic, N., Melolinna, M. The empirics of granular origins: some challenges and solutions with an application to the UK. J Prod Anal 58, 151–170 (2022). https://doi.org/10.1007/s11123-022-00635-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11123-022-00635-2