Abstract

U.S. Government support for minority owned banks (MOBs) dates to the late 1960s. Evidence through the early 1990s suggested these banks are relatively inefficient. This study updates that research, using Stochastic Frontier Analysis (SFA) and panel data from 2003 to 2014 on minority owned banks and other banks. It is, as far as we know, the first such study to exclude outliers in SFA estimation, while recovering the outliers for efficiency estimation. Initial results identify a disruption in cost efficiency during 2008, with statistically distinct regimes for 2003–2007 and 2009–2014. Including recovered observations alters the patterns of MOB efficiency in significant ways, and leads us to conclude that current MOB inefficiency is mainly limited to Asian American owned and Multi-racial and minority serving banks. Tests for the effects of government deposits under a U.S. Treasury program suggest these did not adversely effect efficiency among covered MOBs, but may have improved survival rates for those MOBs subsequent to the financial collapse.

Similar content being viewed by others

Notes

We do not address the related possibility that large banks increasingly penetrated markets previously dominated by MOBs, but are pursuing that issue in future research.

The effective date of these rules is often a few months after finalization and, for a very few rules, years later.

It would be simplest to perform this task by including an exclusionary “if” statement in the sfpanel command (discussed below). However, doing so yields different results than excluding the observations entirely prior to running sfpanel estimation. We presume the latter are more accurate, and run the SF analyses presented here after excluding outliers entirely, then rerun the estimation while constraining all coefficients to values initially found, and apply those coefficients to all observations. This approach yields identical cost efficiency estimates to the fifth digit beyond the decimal point for non-outliers.

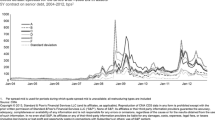

Heteroskedasticity may be related to bank scale, and normalization by either total earning assets (as in Berger et al. 2009) or equity (as in Berger and Mester 1997) may be used for this purpose. However, during this period, equity often fluctated due to forces outside of the banks direct control, including tightened capital requirements (Department of the Treasury, Federal Reserve Bank and Federal Deposit Insurance Corporation 2011), and injections of capital by the U.S. Treasury under the Troubled Asset Relief Program (Cornett et al. 2013).

Wang and Schmidt (2002) recommend use of a single-step estimator to remove this source of bias. The conditional mean estimator of BC95 allows direct entry of the MOB dummies in such a single-step estimator, but the results are implausible. Instead of yielding absolutely larger, same-signed coefficients, as Wang and Schmidt predict, the coefficients are opposite-signed. More troubling, regressing measured efficiency from that single-step estimator against the MOB dummies absolutely increases the MOB coefficients while leaving the signs unchanged, recommending the two-step approach taken here.

The Kumbhakar and Heshmati (1995) approach uses a standard random effects regression estimator. However, the random effects regression command (xtreg) in Stata does not permit the use of constraints, so outliers cannot be recovered.

The joint effect of BlkBs, HispBs, NatBs, and MultBs is entirely captured by the four AfHispNat and poverty categorical variables for MOBs, requiring the exclusion of one of the four specific groups in the estimation.

Banker et al. (2010a) and Hsiao et al. (2010) include the capital adequacy ratio and the nonperforming loan ratio as controls for the inverse of undercapitalization and bank risk. These variables are not used as controls in the second stage regressions because the Tier 1 capital/asset ratio is positively correlated with the poverty measure described below (r = .113), the nonperforming loan ratio is positively correlated with the proportion of African Americans, Hispanics and Native Americans in the markets, particularly after 2009 (r = .130) and, among the MOBs, the nonperforming loan ratio post-2009 is closely correlated with both the poverty measure (r = .148) and the proportion of African Americans, Hispanics and Native Americans in their markets (r = .235). Since it is unlikely that either capital adequacy or nonperforming loans cause the demographic composition of bank markets, the variables are not included.

References

Altunbas Y, Gardener EPM, Molyneux P, Moore B (2001) Efficiency in European banking. European Economic Rev 45:1931–1955

Altunbas Y, Molyneux P, Thornton J (1997) Big-bank mergers in Europe: an analysis of the cost implications. Economica 64:317–329

Amin M, Isa Z, Fontaine R (2013) Islamic banks: contrasting the drivers of customer satisfaction on image, trust, and loyalty of Muslim and non-Muslim customers in Malasia. Int J Bank Marketing 31:79–97

Banker RD, Chang H, Lee S-Y (2010a) Differential impact of Korean banking system reforms on bank productivity. J Bank Finance 34:1450–1460

Banker RD, Cummins JD, Klumper PJM (2010b) Performance measurement in the financial services sector: frontier efficiency methodologies and other innovative techniques. J Bank Finance 34:1413–1416

Battese GE, Coelli T (1995) A model for technical inefficiency effects in stochastic frontier production function for panel data. Empir Economics 20:325–332

Baumann C, Hamin H, Tung RL (2012) Share of wallet in retail banking: a comparison of caucasians in Canada and Australia vis-à-vis Chinese in China and overseas Chinese. Int J Bank Marketing 30:88–101

Belotti F, Daidone S, Ilardi G, Atella V (2013) Stochastic frontier analysis using Stata. Stata J 13:719–758

Berger A, Hasan I, Zhou M (2009) Bank ownership and efficiency in China: what will happen in the world’s largest nation? J Bank Finance 33:849–870

Berger A, Humphrey D (1997) Efficiency of financial institutions: international survey and directions for future research. European J Operational Research 98:175–212

Berger A, Leusner JH, Mingo JJ (1997) The efficiency of bank branches. J Monetary Economics 40:141–162

Berger A, Mester LJ (1997) Inside the black box: what explains differences in the efficiencies of financial institutions. J Bank Finance 21:895–947

Berger A, De Young R (1997) Problem loans and cost efficiency in commercial banks. J Bank Finance 21:849–870

Berger AN, Humphrey DB (1992) Measurement and efficiency issues in commercial banking. In: Griliches Z (ed) Output Measurement in the Service Sectors. University of Chicago Press, Chicago, p 245–279

Bhaskar RR, Gopalan YK, Kliesen KL (2010) Commercial real estate: a drag for some banks but maybe not for US economy. Federal Reserve Bank of St. Louis Region. Economist, January, 10-11

BLS. US Bureau of Labor Statistics (2013) Consumer price index, All urban consumers. BLS, Washington DC, ftp://ftp.bls.gov/pub/special.requests/cpi/cpiai.txt. Accessed 28 April 2014

Brimmer A (1992) The dilemma of Black banking: lending risks vs. community service. Rev Black Political Economy 20:5–29

Burhouse S, Chu K, Goodstein R, Northwood J, Osaki Y, Sharma D (2014) FDIC national survey of unbanked and underbanked households. FDIC. https://www.fdic.gov/householdsurvey/2013report.pdf. Accessed 20 November 2015

Cole JA (1985) Black banks: a survey and analysis of the literature. Rev Black Political Economy 14:29–50

Consumer Financial Protection Bureau (2013) CFPB study of overdraft programs. CFPB, Washington DC, http://files.consumerfinance.gov/f/201306_cfpb_whitepaper_overdraft-practices.pdf. Accessed October 27, 2014

Cornett MM, Li L, Tehranian H (2013) The performance of banks around the receipt and repayment of TARP funds: Over-achievers versus under-achievers. J Bank Finance 37:730–746

Critchfield T, Davis T, Davison L, Gratton H, Hanc G, Samolyk K (2004) Community banks: Their recent past, current performance, and future prospects. FDIC Bank Rev 16:1–31. http://www.fdic.gov/bank/analytical/banking/2005jan/article1.html. Accessed 10 June 2014

Department of the Treasury, Federal Reserve Bank and Federal Deposit Insurance Corporation (2011) Risk-based capital standards: Advanced capital adequacy framework—Basel II; Establishmen of a risk-based capital floor. Department of the Treasury, Washington, DC, http://www.fdic.gov/news/news/press/2011/pr11103a.pdf. Accessed 28 April 2014

DeYoung R, Hunter WC, Udell GF (2004) The past, present, and probable future for community banks. J Financial Services Res 25:85–133

Elyasiani E, Mehdian S (1992) Productive efficiency performance of minority and nonminority-owned banks: a nonparametric approach. J Bank Finance 16:933–948

FDIC (2003-2013) Minority Depository Institutions. FDIC, December 31

FDIC (2012) FDIC Community Banking Study. FDIC, December http://www.fdic.gov/regulations/resources/cbi/report/cbi-full.pdf. Accessed 20 June 2014

FDIC (2014) Preservation and Promotion of Minority Depository Institutions. Report to Congress for 2013. Report FDIC-024-2014. https://www.fdic.gov/regulations/resources/minority/congress/report-2013.pdf. Accessed 26 November, 2015

FDIC Federal Deposit Insurance Corporation (2002) FDIC definition of minority depository institution http://www.fdic.gov/regulations/resources/minority/MDI_Definition.html. Accessed 20 June 2014

Federal Reserve Bank (2003-2013) Minority-Owned Banks. Federal Reserve Statistical Release, December 31

Federal Reserve Bank (2014) Selected Interest Rates – H.15 http://www.federalreserve.gov/releases/h15/data.htm. Accessed 20 June 2014

Forsyth GD (2013) Trough to peak: A note on risk-taking in the Pacific northwest's banking sector. Contemp Economic Policy 31:378–391

Fries S, Taci A (2005) Cost efficiency of banks in transition: evidence from 289 banks in 15 post-communist countries. J Bank Finance 29:55–81

Gabaix X, Laibson D (2006) Shrouded attributes, consumer myopia, and information suppression in competitive markets. Quart J Economics 21:505–540

GAO. General Accounting Office (2013) Dodd-Frank Regulations: Agencies Conducted Regulatory Analyses and Coordinated but Could Benefit from Additional Guidance on Major Rules. GAO, Washington DC, Report GOA-14-67

Gardner M (1982) Black-owned commercial banks: a new look at their performance and management. Rev Black Political Economy 12:91–101

Gilbert RA, Meyer AP, Fuchs JW (2013) The future of community banks: lessons from banks that thrived during the recent financial crisis. Review, Federal Reserve Bank of St. Louis 95:115–143

Guntz S (2011) Sustainability and profitability of microfinance institutions. Research paper 4/2011. Center for Applied International Finance and Development. https://www.th-nuernberg.de/fileadmin/Fachbereiche/bw/studienschwerpunkte/international_business/Master/CAIFD/ResearchPapers/SustainabilityAndProfitabilityOfMicrofinanceInstitutions_Guntz.pdf. Accessed 25 November, 2015

Hasan I, Hunter WC (1996) Management efficiency in minority- and women-owned banks, Economic Perspectives, Federal Reserve Bank of Chicago, 20-28

Hsiao HC, Chang H, Cianci AM, Huang L-H (2010) First financial restructuring and operating efficiency: evidence from Taiwanese commercial banks. J Bus Finance 34:1461–1471

Hughes JP, Mester LJ (1993) A quality and risk adjusted cost function for banks: evidence on the “too-big-to-fail” doctrine. J Productivity Anal 4:293–315

Hughes JP, Mester LJ (1998) Bank capitalization and cost: evidence of scale economies in risk management and signalling. Rev Economics Stat 80:314–325

Humphrey DB (1993) Costs and technical change: effects from bank deregulation. J Productivity Anal 4:9–34

Immergluck D (2004) Credit to the Community: Community Reinvestment and Fair Lending Policy in the U.S.. M.E. Sharpe, Armonk, NH

Iqbal Z, Ramaswamy K, Akhigbe A (1999) The output efficiency of minority-owned banks in the united states. International Rev Economics and Finance 8:105–114

Jacewitz S, Kupiec P (2012) Community bank efficiency and economies of scale. Federal Deposit Insurance Corporation report (December) http://www.fdic.gov/regulations/resources/cbi/report/cbi-eff.pdf. Accessed 28 April 2014

Jarsulic M (2010) Anatomy of a Financial Crisis. Palgrave McMillan, New York

Jondrow J, Lovell C, Materov I, Schmidt P (1982) On the estimation of technical efficiency in the stochastic production function model. J Econometrics 19:233–238

Kashian R, Drago R (2015) Fee or free checking? noninterest checking account fees, competition, and multimarket banking. Appl Economics. doi:10.1080/00036846.2015.1109043

Kashian R, McGregory R, Drago R (2015) ATM fees at Black and Hispanic owned banks: a comparative analysis. Rev Black Political Economy. doi:10.1007/s12144-015-9228-z

Kashian R, McGregory R, Grunfelder-Mcrank D (2014a) Whom do Black-owned banks serve? Communities banking. Boston Federal Reserve Bank. (Summer):29–31

Kashian R, McGregory R, Lockwood N (2014b) Do minority-owned banks pay higher interest rates on cd’s? Rev Black Political Economy 41:13–24

Keeton W, Harvey J, Willis P (2003) The role of community banks in the U.S. economy. Federal Reserve Bank of Kansas City. Economic Rev Q2:15–43

Kumbhakar SC, Heshmati A (1995) Efficiency measurement in Swedish dairy farms: an application of rotating panel data, 1976-88. Am J Agric Econ 77:660–674

Kumbhakar SC, Lien G, Hardaker JB (2014) Technical efficiency in competing panel data models: a study of Norwegian grain farming. J Productivity Anal 41:321–337

Kumbhakar SC, Lovell CAK (2000) Stochastic frontier analysis. Cambridge University Press, Cambridge

Lawrance EC (1991) Poverty and the rate of time preference: evidence from panel data. J Polit Economy 99:54–77

Leibenstein H (1966) Allocative efficiency vs. “X-efficiency”. Amer Econ Rev 56:392–516

Macartney S, Bishaw A, Fontenot K (2013) Poverty rates for selected detailed race and Hispanic groups by state and place: 2007-2011. American Community Survey Briefs. https://www.census.gov/prod/2013pubs/acsbr11-17.pdf. Accessed 20 November 2015

Mountain DC, Thomas H (1999) Factor price misspecification in bank cost function estimation. J International Financial Mark, Inst Money 9:163–182

Papke LE, Wooldridge JM (1996) Econometric methods for fractional response variables with an application to 401(k) plan participation rates. J Appl Econometrics 11:619–632

Pessarossi P, Weill L (2013) Do capital requirements affect bank efficiency? Evidence from China, BOFIT Discussion Paper 28, http://www.suomenpankki.fi/bofit/tutkimus/tutkimusjulkaisut/dp/Documents/2013/dp2813.pdf. Accessed 15 August 2014

Pew Charitable Trusts (2014) Overdrawn: Persistent Confusion and Concern About Bank Overdraft Practices. Pew Charitable Trusts, Philadelphia, PA

Price D (1990) Minority-owned banks: history and trends. Federal Reserve Bank of Cleveland. https://www.clevelandfed.org/Research/Commentary/1990/0701.pdf. Accessed 1 July 2013

Ruggles S, Genadek K, Goeken R, Grover J, Sobek M (2015) Integrated public use microdata series: Version 6.0 [Machine-readable database]. University of Minnesota, Minneapolis

Sealey CW, Lindley JT (1977) Inputs, outputs, and a theory of production and cost at depository financial institutions. J Financ 32:1251–1266

Simpson WG, Kohers T (2002) The link between corporate social and financial performance: Evidence from the banking industry. J Bus Ethics 35:97–109

Snow J (2014) Zip code to zcta crosswalk. American Academy of Family Physicians, Washington DC, http://www.udsmapper.org/zcta-crosswalk.cfm Accessed 15 June 2015

Stango V, Zinmann J (2009) What do consumers really pay on their checking and credit card accounts? Explicit, implicit, and avoidable costs. American Economic Rev 99:424–429

Stango V, Zinmann J (2014) Limited and varying consumer attention: evidence from shocks to the salience of bank overdraft fees. Rev Financial Stud 27:990–1030

Stiroh KJ (2004) Diversification in banking: is noninterest income the answer? J Money, Credit, Banking 36:853–882

St. Louis Federal Reserve Bank (2014) Dodd-Frank regulatory reform rules. http://www.stlouisfed.org/regreformrules/. Accessed 20 August 2014

Tholmer EJ, Tillman HR (2014) Promoting an inclusive financial system: spotlight on minority depository institutions. Community Banking Connections 3rd-4th quarter 12-15.

Uchida H, Gregory FU, Nobuyoshi Y (2012) Loan officers and relationship lending to SMEs. J Financial Intermediation 21:97–122

VanHoose D (2007) Theories of bank behavior under capital regulation. J Bank Finance 31:3680–3697

Wang HJ, Schmidt P (2002) One-step and two-step estimation of the effects of exogenous variables on technical efficiency levels. J Productivity Anal 18:129–144

Wang JC, Inklaar R (2013) Real output of bank services: what counts is what banks do, not what they own. Economica 80:96–117

Van der Westhuizen G (2014) Bank efficiency and financial ratios: rating the performance of the four largest south african banks. J Appl Bus Res 30:93–104

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interests.

Rights and permissions

About this article

Cite this article

Kashian, R., McGregory, R. & Drago, R. Minority owned banks and efficiency revisited. J Prod Anal 48, 97–116 (2017). https://doi.org/10.1007/s11123-017-0510-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11123-017-0510-x