Abstract

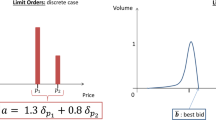

In this paper we build a discrete time model for the structure of the limit order book, so that the price per share depends on the size of the transaction. We deduce the value of a portfolio when the investor trades using market orders and a bank account with different interest rates for lending and borrowing. We also deduce conditions to rule out arbitrage and solve the problem of pricing and hedging an European call option with physical delivery. It is shown that contrary to the perfectly liquid setting, the price of a European call is not given by an expectation, but can be expressed as an optimization problem on a set of equivalent probability measures.

Similar content being viewed by others

References

Agliardi R, Gençay R (2014) Hedging through a limit order book with varying liquidity. J Deriv 22(23):32–49

Bank P, Baum D (2004) Hedging and portfolio optimization in illiquid financial markets with a large trader. Math Financ 14:1–18

Bayraktar E, Ludkovski M (2011) Optimal trade execution in illiquid markets. Math Financ 21(4):681–701

Boyd S, Vandenberghe L (2009) Convex optimization, 7th edn. Cambridge University Press, Cambridge

Cetin U, Jarrow R, Protter P (2004) Liquidity risk and arbitrage pricing theory. Finance Stochast 8:311–341

Çetin U, Rogers L (2007) Modeling liquidity effects in discrete time. Math Finance 17(1):15–29

Cetin U, Soner H, Touzi N (2010) Option hedging for small investors under liquidity costs. Finance Stochast 14:317–341

Cox J, Ross S, Rubinstein M (1979) Option pricing: A simplified approach. J Financ Econ 7:229–263

Cvitanić J, Ma J (1996) Hedging options for a large investor and forward-backward SDE’s. Ann Appl Probab 6:370–398

Delbaen F, Schachermayer W (1994) A general version of the fundamental theorem of asset pricing. Math Ann 300(3):463–520

Dolinsky Y, Soner H (2013) Duality and convergence for binomial markets with friction. Finance Stochast 17:447–475

Foucault T, Kadan O, Kendel E (2005) Limit order book as a market for liquidity. Rev Financ Stud 18(4):1171–1217

Gökay S, Soner HM (2012) Liquidity in a binomial market. Math Financ 22 (2):250–276

Gökay S, Soner HM (2013) Hedging in an illiquid binomial market. Nonlinear Anal: Real World Appl 16:1–16

Harrison J, Pliska S (1981) Martingales and stochastic integrals in the theory of continuous trading. Stochast Process Appl 11:215–260

Harrison JM, Kreps DM (1979) Martingales and arbitrage in multiperiod securities markets. J Econ Theory 20:381–408

Jarrow R (1994) Derivative security markets, market manipulation and option pricing. J Financ Quant Anal 29:241–261

Obizhaeva A, Wang J (2013) Optimal trading strategy and supply/demand dynamics. J Financ Mark 16:1–32

Predoiu S, Shaikhet G, Shreve S (2011) Optimal execution in a general one-sided limit-order book. SIAM J Financ Math 2:183–212

Roch A (2011) Liquidity risk, price impacts and the replication problem. Finance Stochast 15(3):399–419

Shreve SE (2004) Stochastic calculus for finance. II. Springer Finance. Springer, New York. Continuous-time models

Simard C (2014) General model for limit order books and market orders. Social Science Research Network. Available at SSRN: http://ssrn.com/abstract=2435198 or https://doi.org/10.2139/2435198.ssrn

Simard C, Rémillard B (2014) Option pricing in a discrete time model for the limit order book. Social Science Research Network. Available at SSRN: http://ssrn.com/abstract=2472410

Simard C, Rémillard B. (2016) Supplementary to option pricing in a discrete time model for the limit order book. Methodology and Computing in Applied Probability, Link to the supplementary material

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Simard, C., Rémillard, B. Pricing European Options in a Discrete Time Model for the Limit Order Book. Methodol Comput Appl Probab 21, 985–1005 (2019). https://doi.org/10.1007/s11009-017-9610-3

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11009-017-9610-3