Abstract

This paper provides a new explanation for the choice of commodity tax principle when introducing network externalities into the intra-industry trade model. First, regardless of the destination or origin principle, when the network externalities are strong (weak), the optimal commodity tax rate in the presence of network externality is positive (negative) and higher (lower) than that without network externality. Second, the interplay between network externalities and trade costs affects the difference in commodity tax rates, influencing the differences in firms’ profits, consumer surplus, tax revenues, and social welfare. Third, if the origin principle’s commodity tax rate is higher (lower) than the destination principle’s, the origin principle’s social welfare level is lower (higher) than the destination principle’s.

Similar content being viewed by others

Notes

Katz and Shapiro (1985) consider that a consumer’s utility level comes not only from the quantity of the good consumed by the consumer but also increases with the number of others who consume the good. The following are potential sources of the positive consumption externality: (1) the direct physical effect of the increase in the number of purchasers of the product, such as the network externality of an increase in the number of mobile phone; (2) the indirect effect, for example, when the number of PCs of similar type purchased increases, so will the number and type of software provided to the PCs; (3) when a purchased good is durable, the availability of post-purchase services usually increases with the number of consumers of the durable good.

Haufler et al. (2005) assume an oligopolistic market for Good 1. For simplicity, they assume that the production of Good 1 requires a fixed cost, and the fixed cost is such that only one firm in each country will make positive profits. Therefore, the domestic and foreign firm forms a duopoly in their respective countries. We omit the fixed cost, since it plays no role in the analysis of this paper.

In reality, \(c = 0\) implies redefining the consumer’s basic willingness to pay for Good 1 as the amount that the consumer’s basic willingness to pay for Good 1 exceeds the constant marginal cost \(c\).

The traditional literature usually treats trade cost \(s\) as the transportation cost.

The domestic and the foreign firms’ total outputs of Good 1 are, respectively, \(x + x^{*}\) and \(y + y^{*}\).

In this paper, we treat Good 1, which is produced by both domestic and foreign firm, as two brands.

With \(Z = (x + x^{*} ) + (y + y^{*} )\), it implies that the products of both \(X\) and \(Y\) firms are fully compatible. Fujiwara (2011a, 2011b) demonstrates, regardless of the Good 1’s compatibility, the decrease in trade costs and tariffs has a significant impact on social welfare levels when network externalities are present. Similarly, we assume that Good 1 is fully compatible, and that only considering the network externalities does not affect the results.

To avoid the possibility of corner solutions where all consumers buy the product, this paper follows the assumption of Katz and Shapiro (1985) that there is no lower bound on the basic willingness to pay \(r\). We thank the reviewer for this comment.

Following Katz and Shapiro (1985), when consumers buy Good 1 from firms \(X\) and \(Y\), \(p - nZ\) and \(p^{*} - nZ\) are respective of the expected hedonic price of Good 1, the price adjusted for the network externality sizes.

To compare with most traditional literature, this paper specifies a specific tax rather than an ad valorem tax.

Brander (1981) mentions oligopolistic firms compete in a Cournot fashion, so each firm considers the output of other firms to be given, and each firm’s strategy is naïve under Cournot competition. In reality, oligopolistic firms are unlikely to use this strategy, so such an assumption is vulnerable to be criticized. However, since the cost of gathering and processing information is prohibitively expensive, very sophisticated strategies are unlikely to be implemented. Limiting our attention to a simple strategy is not necessarily a drawback.

The subscripts represent the partial derivatives.

The equilibrium prices, \(\hat{p}^{D}\) and \(\hat{p}^{*D}\), are not always positive. This is because we normalize the unit cost to zero, thus a negative price corresponds to a price below unit cost. As long as the firms can make a positive profit per unit after tax in a particular market, i.e., there is a sufficiently large negative tax (subsidy), they will produce a positive output for that market. We appreciate the reviewer for this insight.

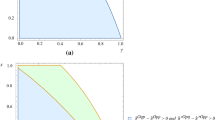

Please see Appendix 1 for conditions of \(\hat{y}^{D} = \hat{x}^{*D} > 0\).

The aim of extracting a foreign firm’s profit is to increase the market share of the domestic firm and shift some tax burden onto foreigners.

Please see Appendix 2 for conditions of \(\hat{y}^{O} = \hat{x}^{*O} > 0\).

References

Agrawal, D. R., & Mardan, M. (2019). Will destination-based taxes be fully exploited when available? An application to the U.S. commodity tax system. Journal of Public Economics, 169, 128–143.

Antoniou, F., Hatzipanayotou, P., & Tsakiris, N. (2019). Destination-based vs. origin-based commodity taxation in large open economies with unemployment. Economica, 86, 67–86.

Behrens, K., Hamilton, J. H., Ottaviano, G. I. P., & Thisse, J. F. (2007). Commodity tax harmonization and the location of industry. Journal of International Economics, 72, 271–291.

Behrens, K., Hamilton, J. H., Ottaviano, G. I. P., & Thisse, J. F. (2009). Commodity tax competition and industry location under the destination and the origin principle. Regional Science and Urban Economics, 39, 422–433.

Brander, J. A. (1981). Intra-industry trade in identical commodities. Journal of International Economics, 11, 1–14.

Brander, J. A., & Krugman, P. R. (1983). A ‘Reciprocal Dumping’ model of international trade. Journal of International Economics, 15, 313–321.

Fujiwara, K. (2011a). Tariffs and trade liberalization with network externalities. Australian Economic Papers, 50, 51–61.

Fujiwara, K. (2011b). Network externalities, transport costs, and tariffs. Journal of International Trade and Economic Development, 20, 729–739.

Goolsbee, A., & Klenow, P. J. (2000). Evidence on learning and network externalities in the diffusion of home computers. University of Chicago.

Goolsbee, A., & Zittrain, J. (1999). Evaluating the costs and benefits of taxing internet commerce. National Tax Journal, 52, 413–428.

Hashimzade, N., Khodavaisi, H., & Myles, G. (2005). Tax principles, product differentiation and the nature of competition. International Tax and Public Finance, 12, 695–712.

Haufler, A., Schjelderup, G., & Stähler, F. (2005). Barriers to trade and imperfect competition: the choice of commodity tax base. International Tax and Public Finance, 12, 281–300.

Katz, M., & Shapiro, C. (1985). Network externalities, competition and compatibility. American Economic Review, 75, 424–440.

Keen, M., & Lahiri, S. (1998). The Comparison between destination and origin principles under imperfect competition. Journal of International Economics, 45, 323–350.

Klimenko, M. M., & Saggi, K. (2007). Technical compatibility and the mode of foreign entry with network externalities. Canadian Journal of Economics, 40, 176–206.

Lockwood, B. (2001). Tax competition and tax co-ordination under destination and origin principles: a synthesis. Journal of Public Economics, 81, 279–319.

McCracken, S. (2015). The choice of commodity tax base in the presence of horizontal foreign direct investment. International Tax and Public Finance, 22, 811–833.

McCracken, S., & Stähler, F. (2010). Economic integration and the choice of commodity tax base with endogenous market structures. International Tax and Public Finance, 17, 91–113.

OECD. (2017). International VAT/GST guidelines. OECD Publishing.

Wu, T. C. (2019). Trade costs and the choice of international commodity tax base revisited: the role of transboundary pollution. International Journal of Economic Theory, 15, 361–383.

Wu, T. C., Liang, C. Y., & Lee, Y. C. (2020). Trade costs and the choice of international commodity tax principle – the role of vertical product differentiation. Academia Economic Papers, 48, 217–260.

Yu, W., & Wang, L. F. S. (2017). Network externalities and tariff structure. Asia-Pacific Journal of Accounting & Economics, 24, 485–496.

Zodrow, G. R. (2003). Network externalities and indirect tax preferences for electronic commerce. International Tax and Public Finance, 10, 79–97.

Acknowledgments

We appreciate an anonymous referee for their insightful comments and suggestions on an earlier version of this paper. This paper’s findings, interpretations, and conclusions are entirely those of the authors. All remaining errors are ours.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1

\(\hat{y}^{D} = \hat{x}^{*D} > 0\) if and only if one of the following four conditions holds:

Appendix 2

\(\hat{y}^{O} = \hat{x}^{*O} > 0\) if and only if one of the following four conditions holds:

Rights and permissions

About this article

Cite this article

Wu, TC., Yen, CT. & Chang, HW. Network externalities, trade costs, and the choice of commodity taxation principle. Int Tax Public Finance 30, 1203–1224 (2023). https://doi.org/10.1007/s10797-022-09740-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-022-09740-2