Abstract

This paper formulates a model of economic growth to study the effects of broad capital taxation (of profits, dividends, and capital gains) on macroeconomic outcomes in small open economies. A framework of exogenous growth permits modeling countries in transition to a country-specific steady state and to discern steady-state and transitory effects of shocks on economic outcomes. The chosen framework is amenable to structural estimation and, in view of the parsimony of the model, fits data on 79 countries over the period 1996–2011 well. The counterfactual analysis based on the estimated model suggests that capital-tax reductions induce positive effects on output and the capital stock (per unit of effective labor) that are economically significant and are accommodated within time windows of 5 years without much further economic response after that. The responses of economic aggregates are found to be relatively strongest to changes in corporate-profit-tax rates and weaker for dividend and capital-gains taxes.

Similar content being viewed by others

Notes

Korinek and Stiglitz (2009) show in a lifecycle model that only anticipated changes in dividend taxation distort economic growth.

Most previous theoretical models discussed capital taxation in a relatively narrow definition—through direct taxes on the capital stock or interest payments only, and empirical contributions focused on reduced-form regressions which are only suited to analyze direct short-run responses to small changes in capital taxation (e.g., see Arnold et al. 2011).

This mechanism is similar to the one in Strulik and Trimborn (2012), who considers dynamic effects of taxation on the tax base and on tax revenues in the USA.

We could alternatively use a common discount of the capital gains tax. The Congressional Budget Office finds that, in the USA, about 38% of all capital gains are realized in a given period, so that the actual capital-gains tax would be 38% of the statutory tax rate. As yet another alternative, we could follow Gavin et al. (2007) and introduce adjustment costs for capital owners which could be calibrated to match the percentage of realized capital gains every period and, hence, would be similar to adjusting the capital-gains tax as mentioned before. However, these alternative approaches would require reliable data on the realized capital gains for each period and each country in this paper’s analysis, which are not available. For this reason, we focus on the statutory capital-gains tax.

All countries in the world that have an income tax have in principal some sort of source-based taxation: income that is generated in the USA is taxed in the USA, although the income recipient might not be a citizen or resident of the USA. As source-based taxation leads to double taxation, some countries have tax treaties to reduce double taxation. We abstract from the latter in this paper.

This assumption seems reasonable for most smaller economies, but one might argue that the tax policies in the USA or China might have an impact on the world as a whole. In this paper we only consider effects of relatively small changes in the tax rates by one percentage point. Unless even such minor changes lead to a significant reallocation of capital in the world economy, the net return on investment in the world should not be significantly affected by changes of the capital-tax structure even in relatively large countries such as the USA or China.

The equity of domestic firms is owned by domestic and foreign individuals, and we denote total equity of domestic firms owned by foreign individuals as \(E^f\). \(E^d\) is equity of domestic firms owned by domestic individuals. Note that individuals have a home bias and own a disproportional share of the domestic capital stock; see French and Poterba (1991). We take this bias as given. Dividends can be paid to either domestic individuals \(D^d\) or foreign individuals \(D^f\). Thus, \(D=D^d+D^f\) and \(E=E^d+E^f\).

We abstract from growth effects related to selection effects in a heterogeneous-firm setting as, e.g., in Bauer et al. (2014).

\(b > (1-\tau _g)^2 \frac{\delta \phi - r(1-\phi )}{(x + n + \delta )r(1-\tau _p)(\phi (1-\tau _g) + (1-\phi )(1-\tau _d) )}\) implies that \(\frac{\partial \tilde{\hat{k}}}{\partial \tau _g} < 0\).

Note that \(d\dot{\hat{\nu }}\) is the difference between the change in total capital holdings, \(\dot{\hat{\nu }}_{ss}\), in the steady state, which is zero by definition, and the change in total capital holdings we observe after a change in the tax rate that leads to changes in the capital stock of the domestic firm, \(\dot{\hat{\nu }}_{t}\). At each point in time, \(\nu _{t+1} = \nu _t + \dot{\hat{\nu }}_t\).

We use corporate-profit-tax rates, corporate-dividend-tax rates, and corporate-capital-gains-tax rates in our analysis. A great share of assets owned (even indirectly) by individuals are held by institutional investors, such as pension funds and life insurance. For these institutional investors, the corporate rates apply. For example, Gonnard et al. (2009) estimate that institutional investors held equity worth about 12,500 billion US dollars in 2007, with total asset holdings of US residents estimated at close to 17,000 billion US dollars at this point in time. Thus, about 70% of all assets were held by institutional investors, for whom corporate tax rates apply.

Note that we use annual data (GDP, employment, etc.) to calibrate the model, thus we are not able to consider changes in capital tax rates at a sub-annual level. Therefore, we use the maximum rate during a year. Moreover, in most countries, most of the time tax reforms become effective at the beginning of the year. Lastly, note that most countries have a flat tax on corporate income, capital gains, and dividends, and thus the maximum statutory rate is the only rate in a country.

The capital stock only includes fixed, reproducible assets that sum up to gross fixed capital formation in the National Accounts; see Inklaar and Timmer (2013).

We thank Credit Suisse for providing us with the data for the MSCI Global Equity Index.

The theoretical model predicts that these observations are not consistent with convergence to a steady state. This pertains mainly to developing countries and oil-producing countries such as Azerbaijan, Moldova, Qatar, Russia, and Sri Lanka.

As suggested by the literature, we exclude countries that have disproportionately large financial sectors, such as Luxembourg.

The existing literature measures Tobin’s q as the ratio between a physical asset’s market value and its replacement value. We relate the average Tobin’s q to macroeconomic fundamentals and the estimated adjustment-cost parameter, \(\widehat{b}\).

\(\lambda \) is computed for the average country in our data. Standard errors for \(\lambda \) are derived using the delta method.

The representative country is calibrated to have the average values of capital stock, technology growth, population growth, capital tax rates, capital share of output, etc., of the year 2008 across all countries covered.

We need the initial total capital holdings, \(\nu \), and the home bias, s, to perform this exercise. The corresponding data are only available for a subset of 50 of the 79 countries covered.

Note that \(\hat{y} = \hat{k}^{\alpha }\), where \(\alpha \) is a constant. This implies that \(\frac{\dot{\tilde{y}}}{\tilde{y}} = \alpha \frac{\dot{\tilde{k}}}{\tilde{k}}\) and the dynamics of capital are essentially the same as those of output.

We compute the present-discounted utility under the benchmark and counterfactual tax policies as the consumption per unit of effective labor, using an instantaneous log utility function, \(U = \int \exp (rt) ln(c_t)~\mathrm{d}t\). Since the model has an infinite time horizon, we approximate the present-discounted utility using 1000 periods. In the 1000th period, the incremental discounted utility of this period is generally less than 1E−17 and assumed to be negligible.

We use the steady-state capital stock of the representative country as a benchmark. This means that only some combinations of capital taxes are compatible with this equilibrium, e.g., very high levels of corporate-profit tax, low levels of dividend taxes, or low levels of capital-gains taxes will never yield the same steady-state level of capital as in the benchmark (representative) economy.

Note that we hold the dividend/payout ratio constant in all panels. As discussed earlier, this will be an appropriate assumption for small changes of capital taxes around the initial tax policies, but it will lose precision with a greater distance to the initial tax policies.

For the representative country, with average tax rates, we use the per capita transfers given Eq. (30) in the Appendix 4 with the steady-state capital level from Eq. (4) to determine steady-state transfers. We solve Eq. (30) for the capital-gains tax, \(\tau _g\), and the dividend tax, \(\tau _d\), respectively, and substitute the previously computed tax revenues and a one percentage point higher corporate-income tax rate to find the tax-revenue-neutral rates for capital gains and dividend taxation.

The tax-revenue-maximizing corporate-income-tax rate is about 71%, the dividend-tax rate is 77%, and the capital-gains tax rate is 12%. These tax rates are not the optimal tax rates in terms of present-discounted utility.

That is comparable to the changes we calculated in Table 4, where the capital-gains-tax change was \((22.8-4.71)\times 0.102 - 0.017 = 1.828\) units and the dividend-tax change was \((6.47 - 3.92)\times 0.008 - 0.017 = 0.003\) units.

Labor-technology- and employment-growth rates have the same effect on all the steady-state capital stocks and the speed-of-convergence parameters. Therefore, we will only consider changes in the labor-technology-growth rates in this section.

Recall that the steady-state capital is decreasing in \(\alpha \) given that \(\tilde{k} > 1\).

\(D = \phi (1-\tau _p) \Pi = \gamma \), where \(\gamma = (1-\tau _p) \Pi - I\). Substituting \(\gamma \) yields \(\phi (1-\tau _p) \Pi = (1-\tau _p) \Pi - I\). Solving for I gives \(I = (1-\phi )(1-\tau _p)\Pi \), where the right term is the definition of retained earnings, R.

If the capital-gains- and dividend-tax rates do not change dramatically, the average dividend/payout ratio should as well be relatively constant. Still this limits the counterfactual experiments within the model, as only small changes of the tax rates can be considered.

These effects represent elasticities, i.e., a percentage-point decline of output per unit of efficiency labor due to an increase of the corporate-profit tax rate by one percentage point. Most empirical studies focus on multiplier effects, i.e., how many monetary units of GDP are lost when one monetary unit is raised by capital taxes. Blanchard and Perotti (2002) estimates that the short-run multiplier for the USA is around −0.74. Revenues from corporate-profit tax are usually around 10% of GDP in the USA. Thus, we can calculate the elasticity in terms of the statutory corporate-profit tax rate as follows: The statutory corporate-profit tax for US firms was 36% in 2007/2008. We normalize GDP to 100 units so that tax revenues from corporate-profit taxes are around 10 units. Given the tax rate, the tax base would be 27.77 units. Now we compute the tax rate necessary to increase the tax revenues from corporate-profit taxation at 11 units, which is 39.6%. From Blanchard and Perotti (2002), we know that one additional unit of tax revenues reduces GDP by about 0.74%. The implied elasticity is \(-\frac{0.74}{39.6-36} = -0.22\) which is relatively close to our estimate of \(-0.157\).

References

Abel, A. B. (1982). Dynamic effects of permanent and temporary tax policies in a q-model of investment. Journal of Monetary Economics, 9(3), 353–373.

Abel, A. B. (2007). Optimal capital income taxation. National Bureau of Economic Research Working Paper Series.

Aghion, P., Akcigit, U., & Fernández-Villaverde, J. (2013). Optimal capital versus labor taxation with innovation-led growth, National Bureau of Economic Research Working Paper Series, No. 19086.

Altig, D., Auerbach, A. J., Kotlikoff, L. J., Smetters, K. A., & Walliser, J. (2001). Simulating fundamental tax reform in the United States. The American Economic Review, 91(3), 574–595.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297.

Arnold, J. M., Brys, B., Heady, C., Johansson, A., Schwellnus, C., & Vartia, L. (2011). Tax policy for economic recovery and growth. The Economic Journal, 121(550), 59–80.

Auerbach, A. J. (1979). Wealth maximization and the cost of capital. The Quarterly Journal of Economics, 93(3), 433–446.

Auerbach, A. J. (1991). Retrospective capital gains taxation. The American Economic Review, 81(1), 167–178.

Auerbach, A. J., & House, C. L. (2009). By how much does GDP rise if the Government buys more output? Comments and Discussion, Brookings Papers on Economic Activity, (pp. 232–249).

Auerbach, A. J., & Siegel, J. M. (2000). Capital-gains realizations of the rich and sophisticated. American Economic Review, 90(2), 276–282.

Baier, S. L., & Glomm, G. (2001). Long-run growth and welfare effects of public policies with distortionary taxation. Journal of Economic Dynamics and Control, 25(12), 2007–2042.

Barro, R. J., & Sala-i-Martin, X. (2004). Economic growth (2nd ed.). New York: McGraw Hill.

Bauer, C., Davies, R. B., & Haufler, A. (2014). Economic integration and the optimal corporate tax structure with heterogeneous firms. Journal of Public Economics, 110, 42–56.

Blanchard, O., & Perotti, R. (2002). An empirical characterization of the dynamic effects of changes in government spending and taxes on output. The Quarterly Journal of Economics, 117(4), 1329–1368.

Blanchard, O., Perotti, R., Rhee, C., & Summers, L. (1993). The stock market, profit, and investment. The Quarterly Journal of Economics, 108(1), 115–136.

Blanchard, O. J., & Leigh, D. (2013). Growth forecast errors and fiscal multipliers. The American Economic Review, 103(3), 117–120.

Caballero, R. J. (1999). Aggregate Investment. In: J. B. Taylor, & M. Woodford (Eds.), Handbook of macroeconomics, Vol. 1, Part B, Chap. 12, (pp. 813–862). Amsterdam: Elsevier.

Chamley, C. (1986). Optimal taxation of capital income in general equilibrium with infinite lives. Econometrica, 54(3), 607–622.

Conesa, J. C., & Dominguez, B. (2013). Intangible investment and ramsey capital taxation. Journal of Monetary Economics, 60(8), 983–995.

Conesa, J. C., Kitao, S., & Krueger, D. (2009). Taxing capital? Not a bad idea after all!. American Economic Review, 99(1), 25–48.

Dackehag, M., & Hansson, Å. (2012). Taxation of income and economic growth: An empirical analysis of 25 Rich OECD countries, Technical Report.

Feenstra, R. C., Inklaar, R., & Timmer, M. P. (2013). The next generation of the Penn world table, Technical Report.

Ferede, E., & Dahlby, B. (2012). The impact of tax cuts on economic growth: Evidence from the Canadian Provinces. National Tax Journal, 65(3), 563–594.

Fidora, M., Fratzscher, M., & Thimann, C. (2007). Home bias in global bond and equity markets: The role of real exchange rate volatility. Journal of International Money and Finance, 26(4), 631–655.

French, K. R., & Poterba, J. M. (1991). Investor diversification and international equity markets. The American Economic Review, 81(2), 222–226.

Gavin, W. T., Kydland, F. E., & Pakko, M. R. (2007). Monetary policy, taxes, and the business cycle. Journal of Monetary Economics, 54(6), 1587–1611.

Gonnard, E., Kim, E. J., & Ynesta, I. (2009). Recent trends in institutional investors statistics. OECD Journal: Financial Market Trends, 2008(2), 1–22.

Gourio, F., & Miao, J. (2011). Transitional dynamics of dividend and capital gains tax cuts. Review of Economic Dynamics, 14(2), 368–383.

Gourio, F., & Miao, J. (2010). Firm heterogeneity and the long-run effects of dividend tax reform. American Economic Journal: Macroeconomics, 2(1), 131–168.

Gruener, H. P., & Heer, B. (2000). Optimal flat-rate taxes on capital—a re-examination of Lucas’ supply side model. Oxford Economic Papers, 52(2), 289–305.

Hall, R. E. (2001). The stock market and capital accumulation. American Economic Review, 91(5), 1185–1202.

Hall, R. E. (2004). Measuring factor adjustment costs. The Quarterly Journal of Economics, 119(3), 899–927.

Hungerford, T. L. (2010). The economic effects of capital gains taxation. Congressional Research Service June: Technical Report.

Inklaar, R., & Timmer, M. (2013). Capital, Labor and TFP in PWT 8.0. Mimeo.

Jones, L. E., Manuelli, R. E., & Rossi, P. E. (1993). Optimal taxation in models of endogenous growth. Journal of Political Economy, 101(3), 485–517.

Judd, K. L. (1985). Redistributive taxation in a simple perfect foresight model. Journal of Public Economics, 28(1), 59–83.

Keuschnigg, C. (2005). Öffentliche Finanzen: Einnahmenpolitik. Tübingen: Mohr Siebeck.

Kindermann, F., & Krueger, D. (2014). The redistributive benefits of labor and capital income taxation: How to best screw (or not) the top 1%. Mimeo.

King, R. G., & Rebelo, S. (1990). Public policy and economic growth: Developing neoclassical implications. Journal of Political Economy, 98(5), S126–S150.

Korinek, A., & Stiglitz, J. E. (2009). Dividend taxation and intertemporal tax arbitrage. Journal of Public Economics, 93, 142–159.

Laitner, J., & Stolyarov, D. (2003). Technological change and the stock market. American Economic Review, 93(4), 1240–1267.

Lansing, K. J. (1999). Optimal redistributive capital taxation in a neoclassical growth model. Journal of Public Economics, 73(3), 423–453.

Lee, Y., & Gordon, R. H. (2005). Tax structure and economic growth. Journal of Public Economics, 89, 1027–1043.

Lucas, R. E, Jr. (1990). Supply-side economics: An analytical review. Oxford Economic Papers, 42(2), 293–316.

Mendoza, E. G., Milesi-Ferretti, G. M., & Asea, P. (1997). On the ineffectiveness of tax policy in altering long-run growth: Harberger’s superneutrality conjecture. Journal of Public Economics, 66(1), 99–126.

Russo, B. (2002). Taxes, the speed of convergence, and implications for welfareeffects of fiscal policy. Southern Economic Journal, 69(2), 444–456.

Sercu, P., & Vanpée, R. (2008). Estimating the costs of international equity investments. Review of Finance, 12(4), 587–634.

Stokey, N. L., & Rebelo, S. (1995). Growth effects of flat-rate taxes. Journal of Political Economy, 103(3), 519–550.

Straub, L., & Werning, I. (2014). Positive long run capital taxation: Chamley–Judd revisited. Mimeo.

Strulik, H., & Trimborn, T. (2012). Laffer strikes again: Dynamic scoring of capital taxes. European Economic Review, 56(6), 1180–1199.

Turnovsky, S. J. (2000). Methods of macroeconomic dynamics (2nd ed.). Cambridge, MA: MIT Press.

Turnovsky, S. J., & Bianconi, M. (1992). The international transmission of tax policies in a dynamic world economy. Review of International Economics, 1(1), 49–72.

Uhlig, H. (2010). Some fiscal calculus. The American Economic Review, 100(2), 30–34.

Uhlig, H., & Yanagawa, N. (1996). Increasing the capital income tax may lead to faster growth. European Economic Review, 40(8), 1521–1540.

Weber, S. (2010). Bacon: An effective way to detect outliers in multivariate data using stata (and mata). Stata Journal, 10(3), 331–338.

Acknowledgements

The authors thank Ron Davies, Michael Devereux, Clemens Fuest, Kimberley Scharf, and the anonymous referees for their helpful comments. The views expressed in this paper are those of the authors’ and do not necessarily reflect those of the Swiss National Bank. Financial support by the Swiss National Science Foundation (SNSF) is gratefully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1: Current-value Hamiltonian formalizing the household problem

Writing the maximization problem of households for generic period t as a current-value Hamiltonian, we obtain

where \(\mu \) and a are the present-value and current-value Lagrange multipliers of wealth, respectively. The resulting first-order conditions (FOCs) for the choice variables of interest to households are

and

In Eq. (16) we assume, as in Turnovsky and Bianconi (1992), that individuals take the dividend yields on their equity as given, which allows us to express the FOCs in terms of dividend yield, \(\frac{d^d}{q}\), and the growth-rate of the value of equity, \(\frac{\dot{q}}{q}\). Equation (17) is the long-run (steady-state) arbitrage condition. In equilibrium, the rate of return on investment in the domestic country, on the left-hand side of Eq. (16), has to match the net rate of return on investment in the rest of the world, r.

Appendix 2: Present-discounted value of the firm

Total dividend payments are paid either to domestic individuals, \(D^d\), or to foreign ones, \(D^f\), according to their equity, \(E^d\) and \(E^f\), respectively. The total value of equity in the economy is \(V = q E\). The change in the total value of equity in the domestic economy equals the change in the value of equity plus the change in equity:

Total investment has to be equal to retained earnings, R, plus the change in equity, \(q \dot{E}\):

Combining Eqs. (1) and (18) with (B), we obtain a first-order differential equation for the change in total value of equity:

where \(\gamma \equiv (1 - \tau _p) \Pi - I\) are the net profits less investment.

We define

and take the derivative of \(V=qE\) to obtain

substitute R from equation (B) in Eq. (1), and solve for \(q \dot{E}\):

Substituting (21) in Eq. (20) results in

which, after defining \(\gamma \equiv (1 - \tau _p) \Pi - \dot{K} - \delta K\), may be written as

Solve (16) for \(\dot{q}\) using the arbitrage condition from the FOCs in Eqs. (16) and (17) to obtain

Substituting this in Eq. (22) and using \(V\equiv qE\) as well as the fact that the dividend yields are the same for domestic and foreign individuals, \(\frac{D^d}{V^d} = \frac{D^f}{V^f}\), which implies that \(E^d D^f = E^f D^d\), obtains

which gives Eq. (19).

Assuming that the firm distributes a share \(\phi \in (0,1)\) as dividends and retains \(1 - \phi \) of the profits, dividend payments are defined as:

Substituting this in Eq. (19) yields,

where we define for notational convenience \(1- \tau \equiv \frac{(\phi (1-\tau _d) + (1-\phi ) (1 - \tau _g)}{1-\tau _g} (1-\tau _p)\). In the steady state, \(\dot{V} = 0\) and Eq. (23) implies that the value of the firm then satisfies

From the individual FOCs in Eqs. (16) and (17) it follows that in the steady state with \(\dot{q} = 0\) the firm value has to be

Both Eqs. (24) and (25) have to hold simultaneously so that in equilibrium the individual valuation of the firm is consistent with its optimal behavior, which is the case if \(D=\gamma \). As the dividends are \(D = \phi (1-\tau _p) \Pi \), this implies that all investments are financed by retained earnings.Footnote 34 We assume that the dividend/payout ratio is constant and the representative firm does not optimize its capital structure with regard to the capital-gains and dividend tax rates. For an individual firm the model would suggest that the dividend/payout ratio depends on the capital-gains and dividend tax rates and, consequently, the dividend- payout ratio would be either zero or unity for an individual firm.Footnote 35

We may integrate Eq. (23) to obtain the present value of a firm:

Appendix 3: \(\tilde{k}\) and \(\lambda \)

The FOCs corresponding to the Hamiltonian in Eq. (3) are

where we use the homotheticity of the production function and the capital-adjustment-cost function to write all expressions in terms of units of effective labor.

Steady-state equilibrium

Using \(\dot{\hat{k}} = \hat{i} - (x + n +\delta ) \hat{k} \) in Eq. (26), the change of \(\hat{k}\) is expressed as

Since \(\dot{\hat{k}} = 0\) in the steady state, the solution to the above equation for the steady-state value, \(\tilde{\eta }\), is

which is independent of \(\hat{k}\) and represents a horizontal locus in a phase diagram with \(\hat{k}\) on the abscissa. Similarly, we rewrite Eq. (27) and substitute Eq. (26) to obtain

The two differential Eqs. (28) and (29) may now be used to construct the phase diagram of the dynamic system in \(\hat{k}\)-\(\eta \)-space. The \(\dot{\hat{k}} = 0\) locus represents Eq. (28), whereas the \(\dot{\eta } = 0\) locus represents Eq. (29). The latter is downward-sloping near the steady-state, if \(\frac{r}{1-\tau _g} > x + n\). To show this, we use that \(\dot{\eta } = 0\) and \(\tilde{\eta }\) from Eq. (5) in Eq. (29) and apply the implicit function theorem to obtain \(\frac{\partial \eta }{\partial \hat{k}} = \frac{(1 - \tau ) f_{\hat{k}\hat{k}}(\hat{k})}{\frac{r}{1-\tau _g} - (x + n)}\). As \(f_{\hat{k}\hat{k}}(\hat{k}) < 0\), we have \(\frac{\partial \eta }{\partial \hat{k}} < 0\), if and only if \(\frac{r}{1-\tau _g} > x + n\). Hence, the \(\dot{\eta } = 0\)-locus is downward sloping around the steady state. Using that in \(\dot{\eta } = 0\) and substituting Eq. (5) yields the steady-state value of capital per unit of effective labor, \(\tilde{\hat{k}}\), as:

Dynamics We are interested in the dynamics of the capital stock, investment, and output after changes in capital taxation. Therefore, we linearize the two dynamic Eqs. (28) and (29) around their steady states to obtain an analytic expression of the speed of convergence. Considering

after substituting \(\tilde{\eta }\) from Eq. (5) and \(\tilde{\hat{k}}\) from Eq. (4), the two eigenvalues, \(\lambda _{1,2}\), are

where \(\zeta = \frac{r}{1-\tau _g} - (x+n)\) and \(\omega = x + n + \delta \).

Appendix 4: Transfers

We write the government’s budget constraint as a function of capital:

where total transfers F have to be equal to total tax revenues. Tax revenues per unit of effective labor, \(\hat{f}\), are given by

Appendix 5: Taxes

1.1 Corporate-profit-tax rates (\(\tau _p\))

For corporate-profit taxes, we utilize the maximum tax rate levied at the national level on corporate profit in a country of residence. In federal states, the total corporate tax rate is calculated as the weighted average of the local (sub-national) taxes combined with federal tax rates (e.g., for Germany or Canada as reported by the OECD) or the tax rate prevailing in the economic center (e.g.,for Switzerland, where the rates of the canton of Zurich are taken).

The primary sources for corporate-profit-tax rates are the following:

-

Ernest and Young Worldwide Corporate Tax Guide 1998–2012

-

Coopers and Lybrand International Tax Summaries 1996–1997

-

International Bureau of Fiscal Documentation Global Corporate Tax Handbook 2007–2012

-

Price Waterhouse Coopers Corporate Taxes - Worldwide Summaries 1999–2000, 2001–2003, 2012–2013

1.2 Capital-gains-tax rates (\(\tau _g\))

For corporate capital-gains taxes, we utilize the maximum tax rate levied at the national level on corporate capital gains in a country of residence.

The primary sources for corporate capital-gains-tax rates are the following:

-

Ernest and Young Worldwide Corporate Tax Guide 1998–2012

-

Coopers and Lybrand International Tax Summaries 1996–1997

-

International Bureau of Fiscal Documentation Global Corporate Tax Handbook 2007–2012

-

Price Waterhouse Coopers Corporate Taxes—Worldwide Summaries 1999–2000, 2001–2003, 2012–2013

1.3 Dividend-tax rates (\(\tau _d\))

For corporate dividend taxes, we utilize the maximum tax rate levied at the national level on after-tax income, classified as dividends, which are distributed to (mostly corporate) shareholders. Shareholder taxation is not taken into account. If an imputation system (as, e.g., in Australia) is stated in the tax code, the tax rate on dividends is set to zero. In some cases, tax codes allow for differentiated dividend-tax rates conditional on holding requirements of the recipient. Then, we choose tax rates applied to dividends paid to corporations holding 10% or less of the distributing entity. In such cases, dividend taxation decreases with higher shares held by the receiving entity and the dividend-tax rates represent the upper bound upper bound.

Corporate-profit tax. 79 countries, 1996–2011

The primary sources for corporate dividend-tax rates are the following:

-

Ernest and Young Worldwide Corporate Tax Guide 1998–2012

-

Coopers and Lybrand International Tax Summaries 1996–1997

-

International Bureau of Fiscal Documentation Global Corporate Tax Handbook 2007–2012

-

Price Waterhouse Coopers Corporate Taxes - Worldwide Summaries 1999–2000, 2001–2003, 2012–2013

The summary statistics for the three capital-taxes rates is shown in Table 6. Figures 7, 8 and 9 present the cross-country distribution of the tax rates for each year in the data, using whisker plots. The area around the median (a horizontal bar) indicated by a box refers to the interquartile range (IQR), whereas the extended lines, the whiskers, indicate values within a maximum of 1.5 times the IQR around the median. The corporate-profit-tax rates in Fig. 7 show a relatively high degree of variability over time, even at the median. The median capital-gains-tax rate in Fig. 8 decreases smoothly and only modestly over the sample period. The distribution of dividend-tax rates in Fig. 9 is skewed toward zero with the median being constant at zero throughout the sample period.

Capital-gains tax. 79 countries, 1996–2011

Dividend tax. 79 countries, 1996–2011

Appendix 6: Total asset holdings and home bias

See Table 7.

Appendix 7: Robustness

In this section, we analyze the robustness of the our baseline results in column (4) of Table 2. In the model, heterogeneity in terms of the speed-of-convergence parameter arises from macroeconomic fundamentals such as capital shares in output. If the capital-adjustment-cost parameter would be country specific, even more heterogeneity could be introduced. In this section, we check the persistence of our results when allowing capital-adjustment costs to vary systematically with GDP per capita, average capital taxes, and time. Moreover, we consider different measures of the dividend/payout ratio, \(\phi \). We briefly discuss the effects of taking the effective tax rate instead of the statutory tax rate. Under the aforementioned specifications, estimated capital-adjustment costs do not significantly change and neither does the average convergence parameter \(\lambda \) relative to the benchmark results. Lastly, we restrict our sample to OECD countries. All estimations are based on our preferred specification, namely column (4) in Table 2, which uses the first-differenced convergence equation and a control function; see Eq. (15). All sensitivity checks are summarized in Table 3.

Country heterogeneity

Capital-adjustment costs might vary systematically with GDP per capita and the general level of capital taxation in a country. To control for this kind of heterogeneity, we parameterize the adjustment-cost factor as follows: \(b = \xi _1 + \xi _2 z\), where z is either GDP per capita or total capital tax, (\(\tau _p + \tau _d + \tau _g\)). We normalize the mean GDP per capita and the mean total capital tax to zero. Hence, we can interpret the estimate of \(\xi _1\) as the average capital-adjustment cost parameter, \(\overline{b}\), and \(\xi _2\) as the effect of variable z on the dispersion of the capital-adjustment-cost parameter around the mean.

We estimate the parameterized capital-adjustment-cost parameter using our preferred specification. The results are given in columns (1) and (2) of Table 3. The average capital-adjustment costs are slightly higher than in our preferred specification, and countries with higher GDP per capita have lower capital-adjustment costs, while high-tax countries have higher capital-adjustment costs. But these effects are far from being statistically significant. Moreover, the average \(\lambda \) is very close to the one without considering the effect of GDP per capita or total capital tax rates.

Time trends and pre-Financial-Crisis results

Technological progress or common, unobserved time-trending factors might reduce capital-adjustment costs over time. To control for this effect, we again parameterize b and take the year 1998 as a base year with \(z=0\). The results for the corresponding estimation are given in column (3) of Table 3. The coefficient \(\xi _1\) is much higher than in all other specifications, but as we take the year 1998 as a base year, we can only interpret it as the average capital-adjustment cost in that year. We find that capital-adjustment costs are falling with time, but this effect is not significant. We cannot reject the hypothesis that the average capital-adjustment costs in that specification are different from the ones in the benchmark specification in column (4) of Table 2.

Next, we restrict the sample to observations prior to the Financial Crisis (up until 2007) in column (4) of Table 3. According to the results, the average capital-adjustment-cost parameter is not significantly different from the benchmark estimate, and the convergence parameter \(\lambda \) is almost identical to the reference estimate.

Dividend/payout ratio \(\phi \)

In our preferred specification we use the average observed \(\phi \) over all countries. In column (5) of Table 3, we use the observed dividend/payout ratios for the subset of countries for which we have data. In column (6) we estimate \(\phi \) as an independent variable. The results in terms of capital-adjustment costs, b, speed of convergence, \(\lambda \), and Tobin’s q are all very similar to the benchmark estimates in column (4) of Table 2. Moreover, the estimated \(\phi \) in column (6) of Table 3 is not significantly different from the dividend/payout ratio of about 0.61 we observe for a subset of 70 countries for which we have data.

To compute \(\phi \), we took for each country the total dividends paid by each firm over the whole sample period from Standard and Poor’s Compustat data set and divided them by the total profits of each firm over the whole sample period. Compustat contains almost 24,000 companies in 70 countries between 1996 and 2012. We excluded firms where either dividend payments or income was missing or negative. Summary statistics for these variables are provided in Table 8.

The share of corporate after-tax profits which is paid as dividends to shareholders is calculated as:

where \(s_j = 1,2,\ldots ,S_j\) indicate firms in country j and \(T= 17\) years (1996–2012).

-

Total dividends: To calculate total dividends we use the annual amount of dividends in current million US dollars from the corporate-income statement as stated in Standard and Poor’s Compustat database.

-

Net income: To calculate net income we use annual income after all expenses in current million US dollars from the corporate-income statement as stated in Standard and Poor’s Compustat database.

OCED countries

Our baseline estimation in column (4) of Table 2 includes a broad set of countries. In column (8) of Table 3 we restrict our sample to OECD countries. Neither the capital-adjustment cost parameter b nor the speed-of-convergence parameter \(\lambda \) is significant different from our baseline estimation.

Effective tax rates

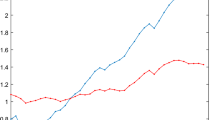

In the previous estimations, we used the statutory tax rates for two reasons. First, ex ante effective tax rates include already a behavioral response of a model firm (e.g., its investment structure and its financing structure), and ex post effective tax rates (i.e., the actual tax revenues generated from the average firm relative to the tax base) depend even more on firm-level responses (e.g., due to the location decisions and tax avoidance through transfer pricing, profit shifting and debt shifting). Second, the effective average tax rates and statutory tax rates on corporate profits are highly correlated. Figure 10 plots the country rank of the statutory corporate-profit tax against the rank of the effective average corporate-profit tax 1998 and 2010. Countries that have high statutory tax rates have usually also high effective average tax rates, as is indicated by the clearly positive correlation. Moreover, we find comparable estimates to the preferred specification using ex ante effective tax rates on corporate profits instead of statutory ones as a further robustness check in column (7) in Table 3. The estimate for the capital-adjustment-cost parameter b is slightly lower, around 15, and the convergence parameter \(\lambda \) is not significantly different from the one in our preferred specification with this specification.

Plot of rank of statutory corporate-profit tax against the rank of effective average corporate-profit tax rate, 1998–2010

Appendix 8: Numerical effects across countries

In this subsection, we describe how the four different tax policies affect a broad set of countries. Tables 9, 10, 11 and 12 show the numerical results in terms of short-run, medium-run, and long-run elasticities of output per unit of effective labor for some selected countries. We also present the country-specific speed-of-convergence parameter and the time it takes until the gap between the (observed) output and the steady-state output is less than 1E−7.

Table 9 gives the results for the general capital-tax increase by one percentage point. Gabon has the strongest decline in steady-state capital stocks (among the 79 countries), where the increase leads to more than a 3.5% decline in the long-run output. The effect is lowest for Iceland with a steady-state elasticity of −0.427. In terms of present-discounted utility, Thailand faces the biggest welfare loss, while Egypt faces the smallest one.

In Table 10, we consider only an increase of the corporate-profit tax by one percentage point. As discussed for the representative country, higher corporate-profit taxes might increase the consumption and the present-discounted utility in some countries. For the majority of countries a higher corporate-profit tax implies a higher utility. The model predicts that Egypt has the biggest gain, while the Philippines face a welfare loss after an increase of the corporate-profit tax by one percentage point. In terms of output, the Gabon again have the strongest decline by more than 1.9%, while Iceland has the lowest one.Footnote 36

The effects of capital-gains taxation are shown in Table 11. The effect in terms of output is very small for Barbados, which comes from the fact that the capital-gains tax in Barbados is zero, while the dividend tax is 15%. Increasing the capital-gains tax (holding the dividend/payout ratio constant) decreases the distortions introduced by capital taxation and hence leads to only very small changes. On the other hand, the effects are strongest for Peru, which has zero dividend taxes and a 30% capital-gains tax. In the latter case, the distortions actually increase more as small differences between dividend and capital-gains taxes increase the capital stock. In terms of welfare (all) countries face negative effects, the strongest ones in Mexico and the weakest in Barbados.

Last, we present the effects for dividend taxation in Table 12. Output declines stronger under dividend taxation than under capital-gains taxation. The effects are strongest in Panama and weakest in Iceland. The welfare effects are mixed for dividend taxation: Some countries actually gain from higher dividend tax rates (e.g., Egypt), while most countries would loose.

In general, a marginal corporate-profit-tax policy has the strongest impact on output per unit of effective labor. Dividend taxation reduces output per unit of effective labor by more than capital-gains taxes in all countries but Argentina, Peru, and Tunisia. The welfare effects are negative for all countries when considering the general tax increase by one percentage point for all capital taxes. Almost all countries in our sample are predicted to gain from a higher corporate-profit-tax rates, while the results are mixed for dividend taxation, and higher capital-gains taxes are found to have negative welfare effects for all countries.

Short-run elasticities of output per unit of effective labor after increasing all capital taxes by one percentage point. Base year 2008. 79 countries

Speed-of-convergence parameter \(\lambda \). Base year 2008. 79 countries

Appendix 9: Short-run elasticities and speed of convergence

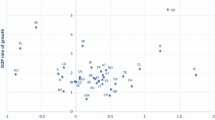

Figure 11 shows the short-run elasticities of output per unit of effective labor after increasing all capital taxes by one percentage point for all 79 countries. The short-run effect of higher capital taxation is very strong in South American countries, South East Asian countries, African countries, and the Middle East. The country with the highest output elasticity is Gabon (−0.902). Most developed countries have rather low elasticities of output, with Iceland having the lowest one (−0.154).

Figure 12 illustrates the speed-of-convergence parameters for different countries. Most developed countries converge relatively slowly to their new steady state, while most developing countries converge rather fast. The short-run elasticities and the speed-of-convergence parameters \(\lambda \), are negatively correlated with an unconditional coefficient of correlation of −0.65.

Rights and permissions

About this article

Cite this article

Bösenberg, S., Egger, P. & Zoller-Rydzek, B. Capital taxation, investment, growth, and welfare. Int Tax Public Finance 25, 325–376 (2018). https://doi.org/10.1007/s10797-017-9454-3

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-017-9454-3

Keywords

- Capital taxation

- Corporate profit taxation

- Dividend taxation

- Capital-gains taxation

- Open economy growth

- Transition paths