Abstract

This research inquiry explores the interplay between environmentally sustainable practices, technological innovations and small- and medium-sized enterprises (SMEs) performance in Mexico's tourism sector. The tourism industry in Mexico holds immense economic significance, contributing significantly to employment and revenue generation. However, the sector also faces challenges related to environmental sustainability. Thus, the objective of this research is to assess how the integration of sustainable environmental practices influences the operational outcomes of SMEs. Furthermore, it also aims to conclude the role of technological innovation, Information and Communication Technology (ICT), digitalization and gender in this relationship. A structural equation modeling approach was applied to a sample of 797 Mexican SMEs in the tourism sector. Our findings provide evidence of several contributions: first, environmental sustainability practices improve performance; second, technological innovation, ICT and digitalization play a critical mediating role in specific relationships to foster performance; finally, incentives encourage sustainable practices related to environmental improvement, especially when the SME's CEO is a woman. The results of this study hold practical significance for the SME sector, as it demonstrates that by adopting sustainable practices, SMEs can strengthen their market position, improve technological innovativeness, minimize environmental impact and capitalize on emerging business prospects.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The United Nations General Assembly's endorsement of the Sustainable Development Goals (SDGs) in 2015 urges all firms to harness their creativity and innovation to address the substantial hurdles posed by sustainable development. As a result, more and more companies are integrating the SDGs into their business strategies, creating concrete and measurable commitments that contribute to sustainable development (Meijide Vidal, 2020). However, empirical evidence has indicated that there exists room for further expansion in the realm of environmental management practices within SMEs (Brammer et al., 2012; Madan Shankar et al., 2017). It is because SMEs often prioritizing day-to-day operations, relegating environmental concerns to a secondary status (Sommer, 2017; Studer et al., 2008). In addition, SMEs face high barriers to implementing environmentally sustainable practices due to the intricate challenge of estimating the costs and gains of such initiatives. The initial investments might outweigh the near-term economic benefits that will not be immediately realized (Anwar & Li, 2021). For these reasons, these companies must receive financial assistance, tax benefits, technical support, or training incentives, which make it easier for SMEs to adopt environmentally sustainable practices (Baporikar, 2022; Sommer, 2017). Although research on incentives to promote sustainability in SMEs is growing substantially in recent years (Anwar & Li, 2021; Lamoureux et al., 2019; Ullah et al., 2021), a noticeable void remains in the body of research concerning the gender disparity in the attainment of these incentives.

The quest for environmental conservation leads companies to invest heavily in innovation and ICT (León-Gómez et al., 2022). Incorporating these innovative technologies will favor alternative and renewable energies that will reduce CO2 emissions (Latif et al., 2017; Lee & Brahmasrene, 2014). At the same time, SMEs that invest in ICT will possess the essential means for data mechanisms, processing capabilities and data interchange that will favor the digitization processes of their business activity (Gavrila Gavrila & de Lucas Ancillo, 2021). However, implementing innovative and technological processes is often costly and time-consuming (Chalova & Bragina, 2020; Niaki et al., 2019). Furthermore, the swift rate of technological evolution can pose challenges for organizations to stay abreast, creating a sense of risk and uncertainty (Peter, 2023). Thus, adopting these technological and innovative processes has aroused certain researchers' interest to analyze their impact on business performance (Pangarso et al., 2022). Consequently, the subsequent aim of this research is to delve into the complex relationships among technological innovation, ICT and digitalization and their effect on companies’ performance.

Therefore, the aims of this research are to test whether the influence of incentives on the adoption of environmentally sustainable practices in SMEs can be explained from a gender perspective, to test whether the adoption of environmentally sustainable practices favors the influence of technological innovation and ICT implementation on SMEs' performance and to unravel the role of innovation, ICT and digitalization in business performance. Therefore, the central inquiries that this investigation aims to address are as follows: Does environmental sustainability exert an influence technological innovation, ICT, digitalization and performance? Does the influence of environmental sustainability on performance get mediated by the other variables? Do companies react differently to sustainability incentives based on the gender of the manager?

To answer these questions, we have analyzed a database of 797 Mexican SMEs located within Mexico's tourism sector. We conducted an analysis using a partial least squares structural equation model (PLS-SEM). Our investigation centers on Mexican SMEs operating within the tourism sector because SMEs play an essential role in Mexico's tourism sector for several reasons (Economic Cooperation and Development (OECD) Studies on Tourism, 2017; Organisation for Economic Cooperation and Development (OECD), 2023):

-

1.

Economic contribution: holds an essential position in Mexico's economy, as the sector directly contributes to 8.5% of the country's GDP.

-

2.

SMEs are a significant source of growth in the Mexican economy, and there are over 4.1 million SMEs in Mexico.

-

3.

SMEs in the tourism sector significantly contribute substantial revenue to businesses such as hotels, tour operators and restaurants.

-

4.

Job creation: The tourism industry creates employment prospects that often do not demand extensive training, presenting a valuable option for individuals with limited formal education or those facing disadvantaged situations. In Mexico, 4.49 million people work in this sector as of 2022.

This study has significant theoretical and practical contributions. From a theoretical standpoint, by examining the impacts of technological innovation, ICT and digitalization on business performance, this research try to elucidate the core factors and approaches that have the potential to enhance the competitiveness and growth of Mexican tourism SMEs in the digital era. Similarly, this investigation adds to our comprehension of how gender diversity in management positions can encourage the adoption and promotion of sustainable practices within these specific company settings. On the other hand, analyzing the influence of technological innovation, ICT and digitalization on the performance of Mexican tourism SMEs has several practical implications for managers. It allows them to identify areas for improvement, design innovation strategies, implement effective technological solutions, optimize data management and adapt to the ever-changing competitive environment. These implications can help tourism SMEs enhance their operational efficiency, competitiveness and profitability within the market. In addition, examining the gender perspective in sustainability incentives enables managers to recognize the significance of including women in leadership roles to drive sustainable practices. It can motivate Mexican tourism SMEs to establish policies and programs that promote equal opportunities and women empowerment at all levels of the organization. Finally, it also has implications for policymakers, as this research shows that promoting corporate sustainability, especially through women's leadership, will ensure that the Mexican tourism sector contributes significantly to the achievement of the UN SDGs.

The study is structured in a way that helps it achieve its objectives. The research process starts by outlining the hypotheses in Sect. 2. Section 3 elucidates the methodologies employed in this research. Next, the results and findings are presented and discussed in Sects. 4 and 5. The final section, Sect. 6, highlights the practical and theoretical contributions of the study, in addition to its inherent limitations.

2 Literature review

2.1 The influence of environmental sustainability on firm performance and the mediated effect of innovation, ICT and digitalization

Research on sustainable environmental practices is an area of great interest within the SME sector (Martins et al., 2022). SMEs are generally relatively slow in adopting environmental sustainability practices (Ortiz-Martínez et al., 2023; Shields & Shelleman, 2015). There are several reasons for this, the first being that these companies prioritize their daily operations, relegating environmental concerns to a secondary status (Sommer, 2017). Furthermore, unlike large companies, SMEs lack the financial and human resources, time, specific know-how and organizational structures to adopt environmental sustainability practices (Nicholas et al., 2011; Ortiz-Martínez et al., 2023). Consequently, these companies face significant barriers to implementing environmentally sustainable environmental practices in their business management (Anwar & Li, 2021). Recent evidence suggests that incentives are essential in encouraging such companies to implement environmental measures (Anwar & Li, 2021; Chowdhury & Shumon, 2020). Incentives that help SMEs to embrace sustainability in their business can be categorized as either external (including normative, incentives of a financial nature, educational support and external market demand) or internal (awareness of and sensitivity to environmental improvement and the increase in corporate performance that can be achieved) (Parker et al., 2009). Therefore, SMEs must receive financial assistance, tax breaks, technical support, or training incentives to make adopting environmentally environmental sustainability practices easier (Baporikar, 2022). Consequently, we posit the initial research hypothesis:

H1:

Sustainability incentives promote the adoption of environmental sustainability practices.

In this framework, previous studies have shown interest in analyzing the effect of integrating environmental sustainability practices on the operational outcomes of SMEs (Chege & Wang, 2020; Hanaysha et al., 2022). So far, there hasn't been much consensus on how much of an effect this connection has. A few studies have suggested that adopting eco-friendly practices can yield favorable effects on a business performance (Gallardo-Vázquez & Sanchez-Hernandez, 2014; Orlitzky & Bejamin, 2001), as these practices allow companies to achieve a competitive potential in the market that will allow them to generate cost savings and market gains (Mill, 2006). In contrast, other authors, such as Lazonick and O’Sullivan (2000), use the principal-agent theory to contend that firms' principal obligation lies in generating profits for their shareholders. Accordingly, involvement in environmental sustainability practices might lead to profit reduction and incur substantial costs within the context of agency relationships. Additionally, other researchers have also corroborated the detrimental effects of this connection. They argue that implementing environmentally sustainable practices comes with a significant cost for businesses, ultimately leading to decreased financial performance (Barnett & Salomon, 2006; Ekins & Zenghelis, 2021). In conclusion, the controversy about the empirical evidence concerning the consequences of implementing environmentally sustainable practices on the business performance of SMEs has led us to establish the subsequent hypothesis:

H2:

Environmental sustainability practices positively impact on business performance.

On the other hand, researchers have recently examined whether implementing sustainable practices affects SMEs' innovative capacity (Rustiarini et al., 2022). Aligned with this trend, many researchers have empirically analyzed the positive role of environmental sustainability in technology innovation and believe that environmental sustainability practices are an important requisite for innovation (Wang et al., 2022). Technological innovation is a broad term that refers to the process of developing new technologies or improving existing ones. It involves recognizing new opportunities, generating ideas and transforming those ideas into new or enhanced products, services or processes (Scherer, 2001). Technological innovation is seen as a beneficial resolution to reconcile the tension between the economic advancement of these enterprises and the imperative of environmental preservation. Thus, it is widely accepted that economic objectives are insufficient to attain enduring sustainability (Rustiarini et al., 2022), but technological innovation could help SMEs to achieve it (Alraja et al., 2022; Le & Ikram, 2022). It is because SMEs committed to sustainable practices will adopt innovative technological processes to enhance productivity, efficiency and cost-effectiveness. This leads to diminished product waste, chemicals and emissions, ultimately contributing to the creation of a future characterized by enhanced sustainability (Ahmad et al., 2023; Alraja et al., 2022). To test this idea, we have proposed the following hypothesis:

H3a:

Environmental sustainability practices positively impact on technological innovation.

Conversely, recent advancements in the realm of innovation substantiate the notion that organizations actively involved in innovative endeavors tend to experience heightened business performance (Artz et al., 2010; González-Fernández & González-Velasco, 2018). This phenomenon arises from the fact that enterprises that create more pioneering products and services attain a competitive edge over their rivals (Gallardo-Vázquez et al., 2019). Innovative offerings encounter reduced competition during their market introduction, affording the company the opportunity to augment profits and establish a distinct identity in comparison to their competitors (Atalay et al., 2013; Hashi & Stojčić, 2013). Several literature reviews have focused on the outcomes and success factors of product innovations (Dangelico, 2016; Zubeltzu-Jaka et al., 2018). For this reason, we have proposed the next hypothesis:

H3b:

Technological innovation positively influences business performance.

Previous studies have also questioned whether environmentally sustainable practices can indirectly affect business performance (Frezza et al., 2019; Zhang et al., 2022). Within this context, technological innovation becomes highly relevant. Technological innovation enables companies to reduce their carbon footprint, conserve resources and reduce waste (Rubicon, 2023). Thus, it will allow companies to generate cost savings by reducing energy and resource consumption, thus improving performance (Hair & Sequeira, 2019; Rubicon, 2023). However, so far, no study has addressed the mediated effect of technological innovation on the influence of sustainable environmental practices on business performance. Consequently, we formulate the research hypothesis:

H3c:

Technological innovation mediates the connection between environmental sustainability practices and business performance.

Recently, there has been a great development in ICT, which encompasses the resources and tools employed for the processing, management and dissemination of information through technological mediums like multimedia PCs, phones, digital cameras and more (León-Gómez et al., 2022). This strong development has been triggered by the growing interest in reducing the harmful effects of business activity on the environment (Añón Higón et al., 2017; Azam et al., 2022). The search for environmental conservation is leading companies to invest heavily in ICTs to optimize their production processes (León-Gómez et al., 2022). The incorporation of this type of technology will favor the use of cleaner inputs (Dedrick, 2010) and alternative and renewable energies (Latif et al., 2017; Wang et al., 2015) which will reduce CO2 emissions (Lee & Brahmasrene, 2014). As a result, investment in ICT reduces environmental degradation as it favors the use of alternative and clean energies (Latif et al., 2017; Wang et al., 2015). Thus, the implementation of ICTs will increase energy efficiency and reduce emissions intensity (Añón Higón et al., 2017). Building upon this foundation, we put forth the subsequent research hypothesis:

H4a:

Environmental sustainability practices encourage ICT implementation.

At the same time, SMEs that invest in this type of technology improve the digitalization process of their business activity (Thrassou et al., 2020). Digitalization can be viewed as an internal process that companies embark upon to transform their existing business model into a digitally-oriented ICT firms structure (Gartner, 2020). Thus, the basis of any digitalization process is the acquisition of the necessary ICT. Investing in this type of technology will allow the digitalization process of SMEs to be carried out as the business will have the essential components for data input, processing capabilities and data exchange mechanisms (Gavrila Gavrila & de Lucas Ancillo, 2021). Drawing from this premise, we articulate the subsequent research hypothesis:

H4b:

ICT implementation improves digitalization processes.

The influence of environmental sustainability practices on digitization processes is a complex and versatile area. Because environmental sustainability practices can enhance the uptake of digital processes but can also disrupt them (Xu et al., 2022), some previous studies claim that environmental sustainability practices can only indirectly cause a positive effect on digitization (Veit & Thatcher, 2023). In this context, ICTs are of great relevance. As mentioned above, concern for environmental conservation has led companies to invest heavily in ICTs that favor the use of cleaner and renewable energy (Latif et al., 2017). In turn, investment in this type of technology will facilitate the digitalization process of companies (Gartner, 2020; Gavrila Gavrila & de Lucas Ancillo, 2021). Against this background, we have proposed the following research hypothesis:

H4c:

The relationship between the application of environmental sustainability practices and digitalization processes is mediated by ICT.

Many studies have recently questioned the influence of digitalization processes on performance (Miranda Ramos et al., 2021; Timmermans et al., 2014). Digitalization has excellent advantages for companies, especially in improving the optimization of production processes and customer loyalty (Crittenden et al., 2019; Ribeiro-Navarrete et al., 2021; Scott et al., 2019). Despite these advantages, there is still a debate about the high cost for companies to implement digitalization processes in their day-to-day activities (Chalova & Bragina, 2020). However, there needs to be a general agreement on whether the high costs of implementing digitization processes will impact business performance. Thus, we have proposed the next hypothesis:

H4d:

Digitalization positively impacts business performance.

Although previous studies have shown that digitization does not have a direct influence on performance (Miranda Ramos et al., 2021; Timmermans et al., 2014), there is still no agreement on its indirect role in performance. Factors related to digitization have been investigated from various perspectives, but the most relevant at present is the one related to ICT (Gartner, 2020; Thrassou et al., 2020). ICT will support companies' digitization processes by enabling them to automate and optimize production processes and thus improve productivity, cost savings, production efficiency, substantial mitigation of human errors and the cultivation of an innovative culture (Parida et al., 2019; Scott et al., 2019). All these factors will culminate in the generation of value for enterprises (Hannila et al., 2022), resulting in higher business performance (Rialti et al., 2019). On these grounds, we posit the ensuing hypothesis:

H4e:

The relationship between ICT implementation and performance is mediated by digitalization.

2.2 The impact of environmental sustainability incentives from a gender perspective

Once the existing relationships between environmental sustainability, innovation, ICT and digitalization and their effects on business performance have been analyzed, we thought it appropriate to analyze whether the incentives to carry out environmental sustainability practices produce a different effect based on the gender of the manager of the companies.

In SMEs, CEOs play a fundamental role in shaping their strategies, policies and objectives (Mason & Simmons, 2014). Therefore, according to Fernández-Gago et al. (2018), their characteristics impact the company's performance and social and environmental advancement. Based on this idea, gender diversity is considered a significant aspect of corporate governance, including environmental sustainability management. In this vein, several theories have been proposed to explain the detrimental effects of companies actions based on gender (Valls Martínez et al., 2022).

The theory of gender socialization posits that the early life experiences of women instill in them a heightened sense of care for others, which leads to greater sensitivity to ethical and environmental matters compared to men (Ibrahim et al., 2009). This theory suggests that there are differences in the attitudes of women and men toward competition and ethical decision-making. Liu (2018) argues that these gender-based distinctions imply that companies led by female directors or managers exhibit a reduced inclination to engage in fraudulent, evasive, or unethical conduct. This perspective is reinforced by research findings that underscore women's heightened awareness of the risks associated climate change (Bear et al., 2010; Choi & Park, 2014; Nielsen & Huse, 2010; Valls Martínez et al., 2019).

Social role theory posits that disparities between genders in terms of their caregiving and household responsibilities, rather than their inherent nature, lead to educational differences (de Cabo et al., 2011). In accordance with this theory, behavior is shaped by stereotypes and beliefs, which result in a distinct management approach based on gender (Eagly et al., 2003). Specifically, women exhibit a heightened level of sensitivity and empathy toward issues faced by stakeholders, encompassing environmental concerns (Bernardi & Threadgill, 2010; Liao et al., 2019). Consequently, gendered roles are assumed by both women and men within organizational contexts. As a result, companies with women occupying senior management positions typically prioritize the interests of stakeholders (Yarram & Adapa, 2021).

Based on resource dependency theory, firms are open systems and the board of directors or managers in SMEs serves as the main tool for interacting with the environment (Pfeffer, 1973). Under this theory, alterations in the environment lead to shifts in the necessary resources, consequently influencing the makeup of the board of directors and the management team. Therefore, a more diverse board of directors and management team has greater capability to acquire the necessary resources and fulfill its social and environmental responsibilities (Valls Martínez et al., 2020). In addition, women managers, as a vital component of human capital, can play a role in bridging the company with its surroundings (Tingbani et al., 2020).

Stakeholder theory posits that stakeholders, such as shareholders, customers, suppliers, lenders, governments and others, have interests in both financial and non-financial consequences, which also encompass environmental considerations. In line with this idea, enterprises are responsible for addressing the environmental damage they cause and operate within society (Freeman, 1984). The unique moral reasoning exhibited by women can aid companies in comprehending the demands of stakeholders (Francoeur et al., 2019). Research has shown that female directors and managers tend to be stakeholder-oriented, focused on ethical practices and socially responsible behavior (Al-Shaer & Zaman, 2016).

Applying these theories, we can consider that a company's management may be different depending on the gender of its CEO. Therefore, its management of environmental sustainability may also be different (Eliwa et al., 2023). In such a way, companies' response to existing sustainability incentives will be different based on the gender of their manager. For this reason, we establish the next hypothesis.

H5:

The relationship between incentives and environmental sustainability exhibits notable differences between men and women.

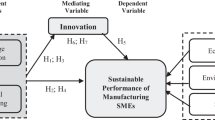

Finally, Fig. 1 depicts the proposed model alongside the hypotheses formulated in this research.

Conceptual model

3 Methods

3.1 Sample and procedure

The sample used to carry out this research was obtained through telephone surveys developed by a firm with expertise in this yield during the first quarter of 2022. The survey was carried out with the CEOs of the companies since they are the ones who have the best knowledge about the reality of the companies, as well as about their future strategy (Van Gils, 2005).

The sample enterprises were chosen and stratified through simple random sampling, obtaining the list of companies from the DENUE. The National Statistical Directory of Economic Units (DENUE) is the minimum infrastructure of the National Economic Information Subsystem (SNIE), whose purpose is to provide both specialized and non-specialized users with the identification, location and contact data of Mexican companies.

After eliminating incomplete or erroneous responses, the sample comprises 797 observations obtained from SMEs dedicated to the hotel industry or bars and restaurants.

Table 1 displays the composition of the sample. As appears in Table 1, 81.68% of the firms are bars or restaurants. Regarding the size, most businesses are micro-sized (57.21%), followed by small businesses (34.5%). Regarding age, 60% of the businesses analyzed are less than ten years old.

Before carrying out the fieldwork, a pretest was conducted with ten trusted companies. The objective was to ensure that the survey was perfectly understandable. Once the final sample was obtained, the necessary checks were carried out to rule out problems derived from non-response bias and the common method. Concerning the former, two groups were established to distribute the sample, 85% of the first responses were included in one group, and the remaining responses were in the second. The ANOVA test showed that there were no significant differences in the responses between the two groups. According to Podsakoff et al. (2003), a single factor test was carried out to rule out the second common method bias since all the data came from the same source (Hair et al., 2019a, 2019b). The findings demonstrate that six factors explain 65.45% of the overall variance and with the primary latent factor accounting for 28.19%. These results allow us to dismiss the possibility of a problem stemming from the common method bias.

To check if the sample size is appropriate to confirm the effects found in this research, we used G*Power 3.1.9.4 software (Mayr et al., 2007). Considering the existence of three relationships with the final dependent variable, if an effect size is presumed to get a power of 0.80, an effect size of 0.15 and an alpha level of 0.05, the results determine that a minimum sample of 119 observations is necessary (Cohen, 1988), which is considerably below the sample size employed in this study.

3.2 Measurement variables

With the aim of checking the hypotheses raised in this study, six latent variables have been created (incentives, sustainability, innovation, ITC, digitalization and performance). All latent variables have been defined as composites in mode A due to our assumption of a definitive linkage between the construct and their corresponding indicators (Sarstedt & Cheah, 2019), and in mode A (reflective) due to the high level of correlation between the indicators used to construct each variable (Rigdon, 2016). A 5-point Likert scale (from 1 for strongly disagree to 5 for strongly agree) was used to measure all latent variables.

Incentives: Based on previous studies (Cantele & Zardini, 2020; Ortiz-Martínez et al., 2023), this latent variable is made up of five indicators. The objective is to measure the benefits that companies find from sustainability.

Environmental sustainability: This latent variable is made up of seven items adapted from prior research (Ilyas et al., 2020; Ortiz-Martínez et al., 2023). This variable measures the degree of commitment to environmental sustainability of the companies surveyed.

Innovation: Consisting of 7 indicators, this variable analyzes changes in products, services and processes by analyzed companies (Briones Peñalver et al., 2018; Freeman, 2013; Palacios-Manzano et al., 2021).

ICT: This latent variable has been created with eleven items drawn from prior research (Karakara & Osabuohien, 2020; Malaquias et al., 2016; Santos-Jaén et al., 2022). This variable encompasses inquiries regarding the utilization of ICT in SMEs.

Digitalization: On the basis of previous studies, this variable is made up of eight items (Eller et al., 2020; Nasiri et al., 2020; Niemand et al., 2021). This variable assesses the extent to which the analyzed companies have embraced digitalization.

Performance: A latent variable comprising of eight items has been created to gauge the financial and non-financial performance of the scrutinized firms. This variable has been created from previous literature (Fernández-Gámez et al., 2019; García-Lopera et al., 2022; León-gómez et al., 2021). For this reason, related to productivity, profitability and quality, among others, have been asked.

3.3 Statistical procedures

Within the framework of PLS-SEM, composites can be categorized into two distinct types: Mode A (correlation weights), in which the constituent indicators are projected to exhibit correlations, and Mode B (regression weights), where the indicators are assumed to be uncorrelated (Gimeno-Arias & Santos-Jaén, 2022). In our model, all latent variables are of type Mode A. As indicated in the previous section, our model comprises six type A composites, making PLS-SEM the best technique for analyzing the relationships between variables (Cepeda-Carrion et al., 2019; Hair et al., 2019a, 2019b). In addition, this technique is very appropriate when multiple relationships and moderating effects are to be analyzed (Hair et al., 2019a, 2019b), as in the case of our model. This model has been run for confirmatory and explanatory purposes. The SmartPLS 4.0.7 software (Ringle et al., 2022) was used for this purpose. According to Streukens and Leroi-Werelds (2016), the bootstrapping procedure was performed with 10,000 samples.

4 Results

To analyze the proposed model, as usual in PLS-SEM (Hair et al., 2013), we will start by analyzing the measurement model. Then, after confirming the reliability and validity of the model have been verified, we will proceed to analyze the relationships established in the model by analyzing the structural model (direct and indirect effects). Finally, we will apply a moderation analysis to test the hypotheses about CEO gender.

4.1 Measurement model analysis

In accordance with Hair et al., (2019a, 2019b), the reliability of the indicators that made up the latent variables is demonstrated by verifying that their standardized factor loadings exceed the minimum value of 0.7. Table 3 displays how the vast majority of indicators exceed this minimum threshold. If those that do not exceed it are above 0.4, they can be maintained if there is a theoretical justification for doing so (Hair et al., 2018).

With the aim to validate construct’s reliability, as stated by Dijkstra and Henseler (2015), it is necessary that the values for Cronbach's alpha, the composite reliability and the Dijkstra–Henseler rho ratio are greater than 0.7. This requirement is met in all six latent variables created in our model, as shown in Table 3. As for the convergent validity of these variables, the values obtained for the mean must be greater than 0.5 (Hair et al., 2019a, 2019b). This requirement is met in our model, as can be seen in the results of Table 2.

This model also complies with the Fornell–Larcker criterion (Fornell & Larcker, 1981). According to this criterion, the square root of the AVE of each latent variable is greater than the correlation with the rest of the constructs, as seen in Tables 3 and 4. Likewise, it is also fulfilled that all the levels of the heterotrait–monotrait (HTMT) ratio do not surpass the established maximum of 0.85. These findings allow us to certify the discriminant validity of the model (Sarstedt et al., 2022).

To conclude the assessment of the internal model, the correct fit of the model was validated. For this purpose, it has been verified that the values of the normalized root mean square residual (SRMR) is under 0.08 and that the value of the normalized fit index (NFI) is above 0.9 (Henseler et al., 2014; Hu & Bentler, 1998). These two conditions are fulfilled for both the estimated model and the saturated model.

4.2 Structural model analysis

The analysis of the model structure began by discarding the existence of multicollinearity problems in the model. For this purpose, the Variance Inflation Index (VIF) of the latent variables was studied, verifying that in no case exceeded the maximum recommended value of 3 (Hair et al., 2019a, 2019b). As can be seen in Table 5, the values fluctuate between 1 and 1.314, so the existence of multicollinearity problems can be ruled out.

The following is an analysis of the relationships established in the structural model. For this purpose, the path coefficients' size, sign and significance will be studied. Table 6 and Fig. 2 display the findings that permit us to determine the acceptance or rejection of the proposed hypotheses.

Results

Regarding the direct effects, the results demonstrate as the impact of incentives on environmental sustainability is positive and significant (β = 0.452***), supporting H1. However, the direct effect of environmental sustainability on innovation is not significant (β = 0.331 ns), hence H2 is not supported. In contrast, environmental sustainability’s impacts on innovation and ICT are positive and significant (β = 0.331*** and β = 0.423***, respectively), so H3a and H4a are supported. Similarly, the effect of innovation on performance is also positive and significant (β = 0.494***), supporting H3b. Besides, H4b is also supported since the direct effect of ICT on digitalization is positive and significant (β = 0.708***). Finally, H4d is rejected since the direct effect of digitalization on performance is not significant (β = 0.043 ns).

R2 measures the variance explained by the predictor variables in relation to the total variance of an endogenous variable. R2 is calculated as the square of the multiple correlation coefficients between the predictor variables and the endogenous variable. It provides an indication of the model's ability to forecast and elucidate the dependent variable. R2 values range from 0 to 1, where a value closer to 1 indicates a higher predictive and explanatory capability of the model (Chin, 2010). Therefore, the coefficient of determination (R2) shows as the exogenous variables in the model explain 20.4% of the variance in environmental sustainability, 10.9% of the variance in innovation, 25.2% of the variance in ICT, 50.2% of the variance in digitalization and 27.7% of the variance in performance. All of these results are above the 10% minimum established by Falk and Miller (1992). These findings confirm the good explanatory capacity of the model, especially for the digitalization variable.

According to Cohen (1988), the effect size (f2) measures the relative importance of a predictor variable compared to other predictor variables in the model. f2 is calculated by dividing the increment in R2 caused by a particular predictor variable by the residual variance. It indicates how much a predictor variable adds to the model in terms of additional explanation compared to other predictor variables. f2 values are typically interpreted as small (0.02), medium (0.15), or large (0.35) Cohen (2013), where higher values indicate a greater importance of the predictor variable in the model. In this model, as established by Cohen (1988), the effect of ICT on digitalization is large, while the effect size of the other accepted hypotheses is medium, except for the effect of environmental sustainability on innovation, which is small.

In order to evaluate the mediating hypotheses, we also analyzed the variance accounted for (VAF). VAF establishes the size of the indirect effect with respect to the total effect (Hair et al., 2021a, 2021b). The findings supporting H3c since the indirect effect of environmental sustainability on performance through innovation is positive and significant (β = 0.163***), suggesting a full mediation because the direct relationship between environmental sustainability and performance is not supported. Moreover, about 71.49% of the total effect is indirect. The results also show a full mediation in relation to the indirect effect of environmental sustainability on digitization through ICT since no direct effect has been considered, and the indirect effect is significant and positive (β = 0.356***); consequently, H4c is supported. Conversely, digitalization does not mediate the relationship between ICT and performance since the indirect effect is not significant (β = 0.031 ns), rejecting H4e. Finally, H4f is also rejected since the indirect effect of environmental sustainability on performance through ICT and digitalizations sequentially is not significant (β = 0.015 ns).

4.3 Moderation analysis

In order to analyze the hypotheses related to the possible moderating effect of gender (H5), a multigroup analysis was carried out (Valls Martínez et al., 2021). For this purpose, a MICOM analysis has been carried out in three steps; configuration invariance, compositional invariance and full measurement model invariance (Henseler et al., 2016).

The first step, configurational invariance, aims to establish that the constructs in both groups exhibit the same characteristics, and that the data processing and algorithm configuration are uniform. The subsequent step, compositional invariance, verifies that the original correlations surpass 5% and all p values exceed 0.05. These findings signify the achievement of compositional invariance. Lastly, the equivalence of the mean and variance of the composites reveals that all disparities lie within the confidence interval, and all p values exceed 0.05 (although these values are not shown in the table). The outcomes presented in Table 7 affirm the measurement invariance for all variables implicated in the moderating hypotheses, thus allowing us to conduct the MGA.

Further, a permutation test was then conducted to determine if there were differences between genders. As can be seen in Table 8, p value is under 0.05 in the relationship between incentives and sustainability (h5a) and sustainability and innovation (H5d) (Hair et al., 2017). Therefore, these two moderating hypotheses are accepted, and the other two (H5b) and (H5d) are rejected.

However, in order to confirm the results, other tests have been carried out. On the one hand, a nonparametric MGA analysis was performed, and it was found that in the accepted hypotheses p value is under 0.05 or above 0.95 indicating significant changes. These results have not been included in the tables because they are the same as those of the permutation. On the other hand, the Welch–Satterhwait test also yields a p value under 0.05, confirming the result (Zimmerman, 2004). To conclude, the parametric test results are also similar, confirming the two previously accepted moderations. The results can be seen in Table 8.

Having accepted hypotheses H5a and H5d, it is worth analyzing their results. As shown in Table 8, the effect of incentives on sustainability is significantly greater for women (β = 0.555***) than for men (β = 0.372***). The same situation occurs in the relationship between environmental sustainability and innovation, where the impact is more significant in the case of companies managed by women (β = 0.419***) compared to those managed by men (β = 0.261***).

Figure 2 illustrates the standardized path coefficients and R2 values. These coefficients illustrate the degree to which the predictor variables contribute to the variance of the dependent variables. Additionally, the provided R2 values specify the fraction of variance in each endogenous variable that can be attributed to the predictive variables.

4.4 Endogeneity assessment

Finally, our objective was to eliminate any potential endogeneity issues within our model. To achieve this, we adopted the methodology outlined by Huit et al. (2018) to do so. Based on the data with which our model has been carried out, it has been considered that the most appropriate approach is the one set forth by (Park & Gupta, 2012) specifically through the creation and analysis of Gaussian Copulas (GC).

The initial step involves examining whether constructs that might be susceptible to endogeneity exhibit non-normal distributions. To accomplish this, we utilize the Cramer–von Mises test on the standardized composite scores of sustainability, innovation, ICT, digitalization and performance (Becker et al., 2021). The findings reveal that the scores of none of the constructs follow a normal distribution. Consequently, we can investigate endogeneity using GC analysis.

In the second step, we applied the GC in SmartPLS4. There is an endogeneity problem if the GC is significant (p < 0.05) (Cepeda-Carrión et al., 2023). As can be seen in Table 9, this does not occur in any case. Therefore, we can exclude the presence of endogeneity issues in the proposed model (Shmueli et al., 2019).

In addition, we have also investigated the potential presence of endogeneity resulting from the omission of variables while attempting to explain the dependent variable (Hair et al., 2021a, 2021b). To address this concern, we adhered the methodology delineated by Antonakis et al. (2014) and included control variables such as size, age and the percentage of the company's capital owned by the owner’s family. After the inclusion of these control variables, we re-executed the PLS algorithm and noted that the outcomes remained consistent with the prior run that lacked the control variables. This suggests that the excluded variables have been effectively managed within this model.

5 Discussion and conclusion

Sustainability is of utmost importance for SMEs in the tourism sector in Mexico. As a country that heavily relies on tourism, it is imperative for companies to adopt sustainable practices to ensure the preservation of natural resources, cultural heritage and local communities. By implementing sustainable measures, SMEs can not only reduce their environmental impact but also improve their reputation, attract eco-conscious tourists and increase their profitability in the long run. Thus, SMEs in the tourism sector in Mexico should prioritize sustainability in their operations and decision-making processes. By doing so, they can play a significant role in advancing the country's sustainable development goals, enhance their competitiveness and positively impact the environment and society. However, the effect of gender on the implementation of sustainable strategies and their impact on business performance has not been sufficiently studied. Hence, this research introduces fresh evidence to the existing body of research, underscoring the significance of environmentally responsible practices, given their impact on innovation, ICT and digitalization, thereby influencing the performance of SMEs within Mexico's tourism sector. Likewise, additional empirical evidence is required to better understand the role of SME CEO gender in the interplay between sustainability incentives and environmental sustainability practices.

First of all, this research results align with those already obtained by (Chowdhury & Shumon, 2020; Ortiz-Martínez et al., 2023) by demonstrating that the financial and non-financial support SMEs receive through incentives is crucial for increased environmental contribution. In addition, our results favor those of who concluded that SMEs do not find a stimulus to motivate them to implement sustainable practices (Parker et al., 2009), as they show that incentives for SMEs will help them to have more financial and human resources, knowledge and organizational structure to adopt practices that favor the implementation of the SDGs in their business activity. In adopting environmentally sustainable practices, our results differ from previous studies that show a direct effect on performance when the company adopts environmentally sustainable practices (Gallardo-Vázquez et al., 2019; Orlitzky & Bejamin, 2001). The outcomes of this study indicate suggest that for a positive relationship to exist, this relationship must be mediated by technological innovation. As Ekins and Zenghelis (2021) have pointed out, environmental sustainability practices come at a high cost to firms, translating into lower performance. Therefore, our research highlights significance of innovation as a pivotal element within the nexus connecting sustainable practices and business performance. By encouraging and supporting technological innovation, companies can unleash the complete potential of sustainable practices, thereby fostering a favorable influence on both the environment and society, all the while improving their bottom line.

On the other hand, this study has demonstrated, as did the previous study of (Azam et al., 2022), the strong implication of adopting environmentally sustainable practices on innovative technologies in SMEs. Firstly, our findings affirm that environmentally sustainable practices encourage the implementation of ICT in SMEs. Incorporating this technology will favor using cleaner inputs and alternative and renewable energies to reduce CO2 emissions (Latif et al., 2017). In turn, our results affirm that implementing ICT will improve digitization processes, as investing in this technology will allow companies to have the necessary data entry mechanisms, processing capacity and data exchange to favor digitization processes (Gavrila Gavrila & de Lucas Ancillo, 2021). This research enhances the existing literature by suggesting the indirect linkage between sustainable environmental practices and digitization, where ICT implementation meditates. This finding is significant for the SME sector as it highlights the importance of formulating a comprehensive digital strategy that integrates sustainable practices and ICT implementation. Such a strategy can help SMEs align their sustainability goals with their digitalization efforts, thus creating a virtuous cycle of innovation, growth and environmental stewardship.

Moreover, the findings of this study do not support the theory of several scholars (Crittenden et al., 2019; Ribeiro-Navarrete et al., 2021), which argue that digitization processes in firms improve business performance. It is because implementing digitization processes entails a high cost for companies that will impact their performance (Chalova & Bragina, 2020). Our results affirm that digitalization has little effect on the performance of SMEs. Instead, digitalization mediated the linkage between ICT implementation and performance. Consequently, the study's emphasis on the mediating role of digitalization underlines the need for SMEs to develop a comprehensive digital strategy that aligns with their business objectives and performance goals. Such a strategy can help SMEs identify the most influential ICT tools and platforms to implement and the most appropriate digitization initiatives to undertake.

Finally, this study addresses the needs shown by (Bear et al., 2010; Choi & Park, 2014; Nielsen & Huse, 2010; Valls Martínez et al., 2019) for further studies on the effect of gender on the connection between sustainability incentives and the adoption of environmentally sound practices. Our findings show how sustainability incentives behave differently depending on the gender of firm management. Women's greater concern for environmental conservation has led to a greater effect of sustainability incentives in female-led firms, as compared to their male-led counterparts.

This research has important theoretical contributions. This research provides frameworks and insights that help SMEs to understand and take advantage of the synergies between sustainability, technological innovation, ICT and digitization. First, this study underscores the notion that sustainability and business success are not mutually exclusive but are intertwined. The results suggest that organizations that adopt and integrate sustainable practices into their technology innovation strategies can achieve superior performance results. Similarly, the results suggest that organizations that effectively embrace digitization and strategically implement ICT can achieve better performance. By leveraging digital technologies to streamline operations, improve efficiencies, improve customer experiences and facilitate data-driven decision-making, companies can gain a competitive advantage and achieve superior financial, operational and market performance. Conversely, our study enhances the comprehension of how gender diversity in management positions can encourage the adoption and promotion of sustainable practices in these types of companies.

The evidence emerging from this study leads to several practical implications for SMEs in the tourism sector. Firstly for managers, the results show the significance of integrating sustainable practices in the day-to-day activities of SMEs. By reducing costs, enhancing reputation, increasing competitiveness, complying with regulations, improving employee engagement and accessing capital, SMEs can position themselves for long-term success. In addition, the importance of ICT, innovation and digitalization in this field is also shown. The mediating role of these factors enables SMEs to develop a more strategic and practical approach to digital transformation, which can improve performance and competitiveness in the digital economy. On the other hand, for shareholders, our results provide new information on the contribution of women to sustainability in SMEs, showing that incentives will have a greater impact on the uptake of sustainable practices in SMEs where the CEO is a woman. Finally, for politicians, investing in environmentally sustainable practices can help countries align with the UN's proposed SDG targets and achieve a range of positive outcomes, including improved environmental performance, increased economic growth, better public health, more significant social equity and enhanced international cooperation.

The principal limitation of this research is its regional character within Mexico, so it needs to provide evidence from an international point of view. Consequently, conducting a supplementary study to corroborate our findings in different countries would be intriguing because we have analyzed the role of gender in a strongly male-dominated organizational context. However, the role of gender may be different in other national contexts where the same issue is highly relevant. On the other hand, this study has been based exclusively on the tourism sector, so the conclusions obtained cannot be generalized to other sectors. Therefore, future research could develop an analysis to outline ways to promote sustainability as a business model for SMEs globally. Finally, this research has only analyzed environmental sustainability, so future studies could also analyze sustainability from its social and economic aspects.

Data availability

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.

References

Ahmad, N., Youjin, L., Žiković, S., & Belyaeva, Z. (2023). The effects of technological innovation on sustainable development and environmental degradation: Evidence from China. Technology in Society, 72, 102184. https://doi.org/10.1016/j.techsoc.2022.102184

Alraja, M. N., Imran, R., Khashab, B. M., & Shah, M. (2022). Technological innovation, sustainable green practices and SMEs sustainable performance in times of crisis (COVID-19 pandemic). Information Systems Frontiers, 24(4), 1081–1105. https://doi.org/10.1007/s10796-022-10250-z

Al-Shaer, H., & Zaman, M. (2016). Board gender diversity and sustainability reporting quality. Journal of Contemporary Accounting & Economics, 12(3), 210–222.

Añón Higón, D., Gholami, R., & Shirazi, F. (2017). ICT and environmental sustainability: A global perspective. Telematics and Informatics, 34(4), 85–95. https://doi.org/10.1016/j.tele.2017.01.001

Antonakis, J., Bendahan, S., Jacquart, P., & Lalive, R. (2014). Causality and endogeneity: Problems and solutions. In D. V. Day (Ed.), The Oxford Handbook of leadership and organizations (pp. 93–117). Oxford University Press.

Anwar, M., & Li, S. (2021). Spurring competitiveness, financial and environmental performance of SMEs through government financial and non-financial support. Environment, Development and Sustainability, 23(5), 7860–7882. https://doi.org/10.1007/s10668-020-00951-3

Artz, K. W., Norman, P. M., Hatfield, D. E., & Cardinal, L. B. (2010). A longitudinal study of the impact of R&D, patents, and product innovation on firm performance. Journal of Product Innovation Management, 27(5), 725–740. https://doi.org/10.1111/j.1540-5885.2010.00747.x

Atalay, M., Anafarta, N., & Sarvan, F. (2013). The relationship between innovation and firm performance: An Empirical evidence from Turkish automotive supplier industry. Procedia - Social and Behavioral Sciences, 75, 226–235. https://doi.org/10.1016/j.sbspro.2013.04.026

Azam, A., Rafiq, M., Shafique, M., & Yuan, J. (2022). Towards achieving environmental sustainability: The role of nuclear energy, renewable energy, and ICT in the top-five carbon emitting countries. Frontiers in Energy Research, 9, 971. https://doi.org/10.3389/fenrg.2021.804706

Baporikar, N. (2022). ICT Adoption implications for SME innovation and augmentation. International Journal of Innovation in the Digital Economy, 13(1), 1–20. https://doi.org/10.4018/ijide.292488

Barnett, M. L., & Salomon, R. M. (2006). Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strategic Management Journal, 27(11), 1101–1122. https://doi.org/10.1002/smj.557

Bear, S., Rahman, N., & Post, C. (2010). The impact of board diversity and gender composition on corporate social responsibility and firm reputation. Journal of Business Ethics, 97(2), 207–221. https://doi.org/10.1007/s10551-010-0505-2

Becker, S., Datta, N., Lami, L., & Rouzé, C. (2021). Energy-constrained discrimination of unitaries, quantum speed limits, and a Gaussian Solovay–Kitaev theorem. Physical Review Letters, 126(19), 190504. https://doi.org/10.1103/PhysRevLett.126.190504

Bernardi, R., & Threadgill, V. (2010). Women directors and corporate social responsibility. EJBO: Electronic Journal of Business Ethics and Organizational Studies, 15(2), 15–21.

Brammer, S., Hoejmose, S., & Marchant, K. (2012). Environmental management in SMEs in the UK: Practices, pressures and perceived benefits. Business Strategy and the Environment, 21(7), 423–434. https://doi.org/10.1002/bse.717

Briones Peñalver, A. J., Bernal Conesa, J. A., & de Nieves Nieto, C. (2018). Analysis of corporate social responsibility in Spanish agribusiness and its influence on innovation and performance. Corporate Social Responsibility and Environmental Management, 25(2), 182–193. https://doi.org/10.1002/csr.1448

Cantele, S., & Zardini, A. (2020). What drives small and medium enterprises towards sustainability? Role of interactions between pressures, barriers, and benefits. Corporate Social Responsibility and Environmental Management, 27(1), 126–136. https://doi.org/10.1002/csr.1778

Cepeda-Carrion, G., Cegarra-Navarro, J. G., & Cillo, V. (2019). Tips to use partial least squares structural equation modelling (PLS-SEM) in knowledge management. Journal of Knowledge Management, 23(1), 67–89. https://doi.org/10.1108/JKM-05-2018-0322

Cepeda-Carrión, I., Alarcon-Rubio, D., Correa-Rodriguez, C., & Cepeda-Carrion, G. (2023). Managing customer experience dimensions in B2B express delivery services for better customer satisfaction: A PLS-SEM illustration. International Journal of Physical Distribution & Logistics Management. https://doi.org/10.1108/IJPDLM-04-2022-0127

Chalova, M. V., & Bragina, Z. V. (2020). Production Digitalisation in Medium IT-Companies: Through the Example of Order Book. In Proceedings of the Russian Conference on Digital Economy and Knowledge Management (RuDEcK 2020) (Vol. 148, pp. 124–128). Atlantis Press. https://doi.org/10.2991/aebmr.k.200730.023

Chege, S. M., & Wang, D. (2020). The influence of technology innovation on SME performance through environmental sustainability practices in Kenya. Technology in Society, 60, 101210. https://doi.org/10.1016/j.techsoc.2019.101210

Chin, W. W. (2010). How to Write Up and Report PLS Analyses. In V. Esposito Vinzi, W. Chin, J. Henseler, & H. Wang (Eds.), Handbook of partial least squares (pp. 655–690). Springer.

Choi, H. J., & Park, J.-H. (2014). The relationship between learning transfer climates and innovation in public and private organizations in Korea. International Journal of Manpower, 35, 956–972.

Chowdhury, P., & Shumon, R. (2020). Minimizing the gap between expectation and ability: Strategies for SMEs to implement social sustainability practices. Sustainability, 12(16), 6408. https://doi.org/10.3390/su12166408

Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Erbaum Press.

Cohen, J. (2013). Statistical power analysis for the behavioral sciences. Routledge. https://doi.org/10.4324/9780203771587

Crittenden, A. B., Crittenden, V. L., & Crittenden, W. F. (2019). The digitalization triumvirate: How incumbents survive. Business Horizons, 62(2), 259–266. https://doi.org/10.1016/j.bushor.2018.11.005

Dangelico, R. M. (2016). Green product innovation: Where we are and where we are going. Business Strategy and the Environment, 25(8), 560–576. https://doi.org/10.1002/bse.1886

de Cabo, R. M., Gimeno, R., & Escot, L. (2011). Disentangling discrimination on Spanish boards of directors. Corporate Governance: An International Review, 19(1), 77–95. https://doi.org/10.1111/j.1467-8683.2010.00837.x

Dedrick, J. (2010). Green IS: Concepts and issues for information systems research. Communications of the Association for Information Systems, 27, 11. https://doi.org/10.17705/1CAIS.02711

Dijkstra, T. K., & Henseler, J. (2015). Consistent and asymptotically normal PLS estimators for linear structural equations. Computational Statistics and Data Analysis, 81, 10–23. https://doi.org/10.1016/j.csda.2014.07.008

Eagly, A. H., Johannesen-Schmidt, M. C., & van Engen, M. L. (2003). Transformational, transactional, and laissez-faire leadership styles: A meta-analysis comparing women and men. Psychological Bulletin, 129(4), 569–591. https://doi.org/10.1037/0033-2909.129.4.569

Economic Cooperation and Development (OECD) Studies on Tourism. (2017). Tourism Policy Review of Mexico (OECD Publishing (ed.)). https://doi.org/10.1787/9789264266575-en

Ekins, P., & Zenghelis, D. (2021). The costs and benefits of environmental sustainability. Sustainability Science, 16(3), 949–965. https://doi.org/10.1007/s11625-021-00910-5

Eliwa, Y., Aboud, A., & Saleh, A. (2023). Board gender diversity and ESG decoupling: Does religiosity matter? Business Strategy and the Environment. https://doi.org/10.1002/bse.3353

Eller, R., Alford, P., Kallmünzer, A., & Peters, M. (2020). Antecedents, consequences, and challenges of small and medium-sized enterprise digitalization. Journal of Business Research, 112, 119–127. https://doi.org/10.1016/j.jbusres.2020.03.004

Falk, R. F., & Miller, N. B. (1992). A primer for soft modeling. University of Akron Press.

Fernández-Gago, R., Cabeza-García, L., & Nieto, M. (2018). Independent directors’ background and CSR disclosure. Corporate Social Responsibility and Environmental Management, 25(5), 991–1001. https://doi.org/10.1002/csr.1515

Fernández-Gámez, M. Á., Gutiérrez-Ruiz, A. M., Becerra-Vicario, R., & Ruiz-Palomo, D. (2019). The effects of creating shared value on the hotel performance. Sustainability (switzerland), 11(6), 1784. https://doi.org/10.3390/su11061784

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50.

Francoeur, C., Labelle, R., Balti, S., & EL Bouzaidi, S. (2019). To what extent do gender diverse boards enhance corporate social performance? Journal of Business Ethics, 155(2), 343–357. https://doi.org/10.1007/s10551-017-3529-z

Freeman, C. (2013). Economics of industrial innovation. Routledge.

Freeman, R. E. (1984). Strategic management: A stakeholder approach. Cambridge University Press.

Frezza, M., Whitmarsh, L., Schäfer, M., & Schrader, U. (2019). Spillover effects of sustainable consumption: Combining identity process theory and theories of practice. Sustainability: Science, Practice and Policy, 15(1), 15–30. https://doi.org/10.1080/15487733.2019.1567215

Gallardo-Vázquez, D., & Sanchez-Hernandez, M. I. (2014). Measuring corporate social responsibility for competitive success at a regional level. Journal of Cleaner Production, 72, 14–22. https://doi.org/10.1016/j.jclepro.2014.02.051

Gallardo-Vázquez, D., Valdez-Juárez, L. E., & Castuera-Díaz, Á. M. (2019). Corporate social responsibility as an antecedent of innovation, reputation, performance, and competitive success: A multiple mediation analysis. Sustainability, 11(20), 5614. https://doi.org/10.3390/su11205614

García-Lopera, F., Santos-Jaén, J. M., Palacios-Manzano, M., & Ruiz-Palomo, D. (2022). Exploring the effect of professionalization, risk-taking and technological innovation on business performance. PLoS ONE, 17(2), e0263694. https://doi.org/10.1371/journal.pone.0263694

Gartner. (2020). Definition of Digital Transformation – Information Technology Glossary. Information Technology Glossary (2020).

Gavrila Gavrila, S., & de Lucas Ancillo, A. (2021). Spanish SMEs’ digitalization enablers: E-Receipt applications to the offline retail market. Technological Forecasting and Social Change, 162, 120381. https://doi.org/10.1016/j.techfore.2020.120381

Gimeno-Arias, F., & Santos-Jaén, J. M. (2022). Using PLS-SEM for assessing negative impact and cooperation as antecedents of gray market in FMCG supply chains: an analysis on Spanish wholesale distributors. International Journal of Physical Distribution & Logistics Management. https://doi.org/10.1108/IJPDLM-02-2022-0038

González-Fernández, M., & González-Velasco, C. (2018). Innovation and corporate performance in the Spanish regions. Journal of Policy Modeling, 40(5), 998–1021.

Hair, S., & Sequeira, M. (2019). Sustainable innovation: business model and technology must evolve together. Sustainability.

Hair, J. F., Astrachan, C. B., Moisescu, O. I., Radomir, L., Sarstedt, M., Vaithilingam, S., & Ringle, C. M. (2021a). Executing and interpreting applications of PLS-SEM: Updates for family business researchers. Journal of Family Business Strategy, 12(3), 100392. https://doi.org/10.1016/j.jfbs.2020.100392

Hair, J. F., Hult, G. T. M., Ringle, C. M., Sarstedt, M., Danks, N. P., & Ray, S. (2021b). Partial least squares structural equation modeling (PLS-SEM) using R. Springer International Publishing. https://doi.org/10.1007/978-3-030-80519-7

Hair, J. F., Ringle, C. M., & Sarstedt, M. (2013). Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Planning, 46(1–2), 1–12. https://doi.org/10.1016/j.lrp.2013.01.001

Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019a). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

Hair, J. F., Sarstedt, M., & Ringle, C. M. (2019b). Rethinking some of the rethinking of partial least squares. European Journal of Marketing, 53(4), 566–584. https://doi.org/10.1108/EJM-10-2018-0665

Hair, J. F., Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2017). Advanced issues in partial least squares structural equation modeling. Sage Publications Sage CA.

Hair, J. F. J., Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2018). Advanced issues in partial least squares structural equation modeling. Sage Publications.

Hanaysha, J. R., Al-Shaikh, M. E., Joghee, S., & Alzoubi, H. M. (2022). Impact of innovation capabilities on business sustainability in small and medium enterprises. FIIB Business Review, 11(1), 67–78. https://doi.org/10.1177/23197145211042232

Hannila, H., Kuula, S., Harkonen, J., & Haapasalo, H. (2022). Digitalisation of a company decision-making system: A concept for data-driven and fact-based product portfolio management. Journal of Decision Systems, 31(3), 258–279. https://doi.org/10.1080/12460125.2020.1829386

Hashi, I., & Stojčić, N. (2013). The impact of innovation activities on firm performance using a multi-stage model: Evidence from the Community Innovation Survey 4. Research Policy, 42(2), 353–366. https://doi.org/10.1016/j.respol.2012.09.011

Henseler, J., Dijkstra, T. K., Sarstedt, M., Ringle, C. M., Diamantopoulos, A., Straub, D. W., Ketchen, D. J., Hair, J. F., Hult, G. T. M., & Calantone, R. J. (2014). Common beliefs and reality about PLS: Comments on Rönkkö and Evermann (2013). Organizational Research Methods, 17(2), 182–209. https://doi.org/10.1177/1094428114526928

Henseler, J., Ringle, C. M., & Sarstedt, M. (2016). Testing measurement invariance of composites using partial least squares. International Marketing Review, 33(3), 405–431. https://doi.org/10.1108/IMR-09-2014-0304

Hu, L.-T., & Bentler, P. M. (1998). Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification. Psychological Methods, 3(4), 424–453. https://doi.org/10.1037/1082-989X.3.4.424

Huit, G. T. M., Hair, J. F., Proksch, D., Sarstedt, M., Pinkwart, A., & Ringle, C. M. (2018). Addressing endogeneity in international marketing applications of partial least squares structural equation modeling. Journal of International Marketing, 26(3), 1–21. https://doi.org/10.1509/jim.17.0151

Ibrahim, N., Angelidis, J., & Tomic, I. M. (2009). Managers’ attitudes toward codes of ethics: Are there gender differences? Journal of Business Ethics, 90(S3), 343–353. https://doi.org/10.1007/s10551-010-0428-y

Ilyas, S., Hu, Z., & Wiwattanakornwong, K. (2020). Unleashing the role of top management and government support in green supply chain management and sustainable development goals. Environmental Science and Pollution Research, 27(8), 8210–8223.

Karakara, A.A.-W., & Osabuohien, E. (2020). ICT adoption, competition and innovation of informal firms in West Africa: A comparative study of Ghana and Nigeria. Journal of Enterprising Communities: People and Places in the Global Economy, 14(3), 397–414. https://doi.org/10.1108/JEC-03-2020-0022

Lamoureux, S. M., Movassaghi, H., & Kasiri, N. (2019). The role of government support in SMEs’ adoption of sustainability. IEEE Engineering Management Review, 47(1), 110–114. https://doi.org/10.1109/EMR.2019.2898635

Latif, Z., Jianqiu, Z., Salam, S., Pathan, Z. H., Jan, N., & Tunio, M. Z. (2017). FDI and ‘political’ violence in Pakistan’s telecommunications. Human Systems Management, 36(4), 341–352. https://doi.org/10.3233/HSM-17154

Lazonick, W., & O’Sullivan, M. (2000). Maximizing shareholder value: A new ideology for corporate governance. Economy and Society, 29(1), 13–35. https://doi.org/10.1080/030851400360541

Le, T. T., & Ikram, M. (2022). Do sustainability innovation and firm competitiveness help improve firm performance? Evidence from the SME sector in Vietnam. Sustainable Production and Consumption, 29, 588–599. https://doi.org/10.1016/j.spc.2021.11.008

Lee, J. W., & Brahmasrene, T. (2014). ICT, CO2 emissions and economic growth: Evidence from a panel of ASEAN. Global Economic Review, 43(2), 93–109. https://doi.org/10.1080/1226508X.2014.917803

León-gómez, A., Ruiz-palomo, D., Fernández-gámez, M. A., & García-revilla, M. R. (2021). Sustainable tourism development and economic growth: Bibliometric review and analysis. Sustainability, 13(4), 2270.

León-Gómez, A., Santos-Jaén, J. M., Ruiz-Palomo, D., & Palacios-Manzano, M. (2022). Disentangling the impact of ICT adoption on SMEs performance: the mediating roles of corpo-rate social responsibility and innovation. Oeconomia Copernicana, 13(3), 831–866. https://doi.org/10.24136/oc.2022.024

Liao, Z., Zhang, M., & Wang, X. (2019). Do female directors influence firms’ environmental innovation? The moderating role of ownership type. Corporate Social Responsibility and Environmental Management, 26(1), 257–263.

Liu, C. (2018). Are women greener? Corporate gender diversity and environmental violations. Journal of Corporate Finance, 52, 118–142. https://doi.org/10.1016/j.jcorpfin.2018.08.004

Madan Shankar, K., Kannan, D., & Udhaya Kumar, P. (2017). Analyzing sustainable manufacturing practices—A case study in Indian context. Journal of Cleaner Production, 164, 1332–1343. https://doi.org/10.1016/j.jclepro.2017.05.097

Malaquias, R. F., Malaquias, F. F. O., & Hwang, Y. (2016). Effects of information technology on corporate social responsibility: Empirical evidence from an emerging economy. Computers in Human Behavior, 59, 195–201. https://doi.org/10.1016/j.chb.2016.02.009

Martins, A., Branco, M. C., Melo, P. N., & Machado, C. (2022). Sustainability in small and medium-sized enterprises: A systematic literature review and future research agenda. Sustainability, 14(11), 6493. https://doi.org/10.3390/su14116493

Mason, C., & Simmons, J. (2014). Embedding corporate social responsibility in corporate governance: A stakeholder systems approach. Journal of Business Ethics, 119(1), 77–86. https://doi.org/10.1007/s10551-012-1615-9

Mayr, S., Erdfelder, E., Buchner, A., & Faul, F. (2007). A short tutorial of GPower. Tutorials in Quantitative Methods for Psychology, 3(2), 51–59. https://doi.org/10.20982/tqmp.03.2.p051

Meijide Vidal, D. (2020). Los ODS en la estrategia empresarial. El caso SUEZ. Revista Icade. Revista de Las Facultades de Derecho y Ciencias Económicas y Empresariales, 108. https://doi.org/10.14422/icade.i108.y2019.013

Mill, G. A. (2006). The financial performance of a socially responsible investment over time and a possible link with corporate social responsibility. Journal of Business Ethics, 63(2), 131–148. https://doi.org/10.1007/s10551-005-2410-7

Miranda Ramos, L. F., Lameiras, M., Soares, D., & Amaral, L. (2021). Who is behind the scenes of the ICT backstage? A study of the ICT resources in local governments. In Proceedings of the 14th International Conference on Theory and Practice of Electronic Governance (pp. 165–171). https://doi.org/10.1145/3494193.3494302

Nasiri, M., Ukko, J., Saunila, M., Rantala, T., & Rantanen, H. (2020). Digital-related capabilities and financial performance: The mediating effect of performance measurement systems. Technology Analysis & Strategic Management, 32(12), 1393–1406. https://doi.org/10.1080/09537325.2020.1772966

Niaki, M. K., Torabi, S. A., & Nonino, F. (2019). Why manufacturers adopt additive manufacturing technologies: The role of sustainability. Journal of Cleaner Production, 222, 381–392. https://doi.org/10.1016/j.jclepro.2019.03.019

Nicholas, J., Ledwith, A., & Perks, H. (2011). New product development best practice in SME and large organisations: Theory vs practice. European Journal of Innovation Management, 14(2), 227–251. https://doi.org/10.1108/14601061111124902

Nielsen, S., & Huse, M. (2010). The contribution of women on boards of directors: Going beyond the surface. Corporate Governance: An International Review, 18(2), 136–148. https://doi.org/10.1111/j.1467-8683.2010.00784.x

Niemand, T., Rigtering, J. P. C., Kallmünzer, A., Kraus, S., & Maalaoui, A. (2021). Digitalization in the financial industry: A contingency approach of entrepreneurial orientation and strategic vision on digitalization. European Management Journal, 39(3), 317–326. https://doi.org/10.1016/j.emj.2020.04.008

Organisation for Economic Co-operation and Development (OECD). (2023). Financing SMEs and Entrepreneurs 2022: An OECD Scoreboard. Key Facts on SME Financing.

Orlitzky, M., & Bejamin, J. D. (2001). Corporate social performance and firm risk: A meta-analytic review. Business and Society, 40(4), 369–396.

Ortiz-Martínez, E., Marín-Hernández, S., & Santos-Jaén, J.-M. (2023). Sustainability, corporate social responsibility, non-financial reporting and company performance: Relationships and mediating effects in Spanish small and medium sized enterprises. Sustainable Production and Consumption, 35, 349–364. https://doi.org/10.1016/j.spc.2022.11.015

Palacios-Manzano, M., Leon-Gomez, A., & Santos-Jaen, J. M. (2021). Corporate social responsibility as a vehicle for ensuring the survival of construction SMEs. The mediating role of job satisfaction and innovation. IEEE Transactions on Engineering Management. https://doi.org/10.1109/TEM.2021.3114441

Pangarso, A., Sisilia, K., Setyorini, R., Peranginangin, Y., & Awirya, A. A. (2022). The long path to achieving green economy performance for micro small medium enterprise. Journal of Innovation and Entrepreneurship, 11(1), 16. https://doi.org/10.1186/s13731-022-00209-4

Parida, V., Sjödin, D., & Reim, W. (2019). Reviewing literature on digitalization, business model innovation, and sustainable industry: Past achievements and future promises. Sustainability, 11(2), 391. https://doi.org/10.3390/su11020391

Park, S., & Gupta, S. (2012). Handling endogenous regressors by joint estimation using copulas. Marketing Science, 31(4), 567–586.

Parker, C. M., Redmond, J., & Simpson, M. (2009). A Review of interventions to encourage SMEs to make environmental improvements. Environment and Planning C: Government and Policy, 27(2), 279–301. https://doi.org/10.1068/c0859b

Peter, N. (2023). The connotation of digitalization for a company‘s risk management. MAP Social Sciences, 3(1), 41–50. https://doi.org/10.53880/2744-2454.2023.3.1.41

Pfeffer, J. (1973). Size, composition, and function of hospital boards of directors: A study of organization-environment linkage. Administrative Science Quarterly, 349–364.

Podsakoff, P. M., MacKenzie, S. B., Lee, J.-Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879–903. https://doi.org/10.1037/0021-9010.88.5.879

Rialti, R., Zollo, L., Ferraris, A., & Alon, I. (2019). Big data analytics capabilities and performance: Evidence from a moderated multi-mediation model. Technological Forecasting and Social Change, 149(October), 119781. https://doi.org/10.1016/j.techfore.2019.119781

Ribeiro-Navarrete, S., Botella-Carrubi, D., Palacios-Marqués, D., & Orero-Blat, M. (2021). The effect of digitalization on business performance: An applied study of KIBS. Journal of Business Research, 126, 319–326. https://doi.org/10.1016/j.jbusres.2020.12.065

Rigdon, E. E. (2016). Choosing PLS path modeling as analytical method in European management research: A realist perspective. European Management Journal, 34(6), 598–605. https://doi.org/10.1016/j.emj.2016.05.006

Ringle, C. M., Wende, S., & Becker, J.-M. (2022). SmartPLS 4. Boenningstedt: SmartPLS GmbH. http://www.smartpls.com

Rubicon. (2023). What is Sustainable Technology? Sustainability, Technology.

Rustiarini, N. W., Bhegawati, D. A. S., & Mendra, N. P. Y. (2022). Does green innovation improve SME performance? Economies, 10(12), 316. https://doi.org/10.3390/economies10120316

Santos-Jaén, J. M., León-Gómez, A., Ruiz-Palomo, D., García-Lopera, F., del Valls Martínez, M., & C. (2022). Exploring information and communication technologies as driving forces in hotel SMEs performance: Influence of corporate social responsibility. Mathematics, 10(19), 3629. https://doi.org/10.3390/math10193629

Sarstedt, M., & Cheah, J. H. (2019). Partial least squares structural equation modeling using SmartPLS: A software review. Journal of Marketing Analytics, 7(3), 196–202. https://doi.org/10.1057/s41270-019-00058-3

Sarstedt, M., Hair, J. F., Pick, M., Liengaard, B. D., Radomir, L., & Ringle, C. M. (2022). Progress in partial least squares structural equation modeling use in marketing research in the last decade. Psychology & Marketing, 39(5), 1035–1064. https://doi.org/10.1002/mar.21640

Scherer, F. M. (2001). Innovation and Technological Change, Economics of. In International Encyclopedia of the Social & Behavioral Sciences (pp. 7530–7536). Elsevier. https://doi.org/10.1016/B0-08-043076-7/02308-1

Scott, S., Hughes, P., Hodgkinson, I., & Kraus, S. (2019). Technology adoption factors in the digitization of popular culture: Analyzing the online gambling market. Technological Forecasting and Social Change, 148(July), 119717. https://doi.org/10.1016/j.techfore.2019.119717

Shields, J., & Shelleman, J. M. (2015). Integrating sustainability into SME strategy. Journal of Small Business Strategy, 25(2), 59–78.

Shmueli, G., Sarstedt, M., Hair, J. F., Cheah, J. H., Ting, H., Vaithilingam, S., & Ringle, C. M. (2019). Predictive model assessment in PLS-SEM: Guidelines for using PLSpredict. European Journal of Marketing, 53(11), 2322–2347. https://doi.org/10.1108/EJM-02-2019-0189