Abstract

One of the key elements in the planned pension reform in the Netherlands is to abolish the implicit subsidy from younger to older workers inherent in pension schemes with age independent contribution and accrual rates. This paper investigates the impact of changes in contribution rates on wages, labor costs and labor supply using a rich administrative data set covering individual employees in the Netherlands for the period 2006–2012. With a panel-based approach and data on both marginal and average contribution rates we aim to provide insight into the mechanisms underlying the incidence and labor supply (in hours) effects of pension contributions. For a two-year change in pension contributions we find that 70% of this change is passed on to the labor costs of employers, while 30% is passed on to the net wage of the employee. No significant effects are found for labor supply. At least in the short and medium run, our results seem at variance with the standard demand-and-supply model for the labor market, but are consistent with a bargaining model.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

One of the key objectives of the planned pension reform in the Netherlands is to abolish the implicit subsidy from younger to older workers inherent in pension schemes with age independent contribution and accrual rates. This is regarded as a necessary step to make pensions more robust and future-proof in view of the aging population and increasing flexibility of labor markets. Since a similar pension accrual is cheaper as the time horizon is longer (due to discounting) this policy implies that younger workers tend to pay too much for their pension whereas older workers pay too little. This is not so much of a problem if one spends the whole career in the same job or sector, but with increasing mobility,Footnote 1 this system tends to become more and more unfair and distortionary. Moreover, this system is in particular beneficial to workers with a steep career path, thus favoring the higher educated workers at the cost of lower educated workers. Abolishing this uniform contribution policy is therefore considered necessary to make the pension system more transparant and actuarially fair.Footnote 2

The pension reform envisages the transition from the current defined benefit (DB) type of contract to more modern defined contribution (DC) contracts. Rather than building up pension entitlements (’defined benefits’) workers in the new contract will accumulate wealth in personal capital accounts; at retirement this wealth is converted into a lifelong pension. Since DC contracts are actuarially fair by nature the implicit subsidy from younger to older workers will be automatically abolished in going from DB to DC contracts. For these new contracts it has been agreed that contributions rates will remain uniform across ages. As a consequence, accruals will tend to decrease by age in the new pension system.

This change of system, however, gives rise to a serious transition problem as an important group of workers who paid ’too much’ in the past will no longer be compensated by paying ’too little’ during the rest of their working carreer. This in particular hurts workers in their mid ages, that is those around the 40 years of age. It has been agreed that these groups should be compensated during the transition by additional measures.

In determining how much workers of different age groups are affected by the transition to the new system—and may need to be compensated—we need insight in the incidence of the pension contributions and their impact on labor supply. For example, if net wages for each group are adjusted accordingly there would be less need for additional compensation measures.

Pension contributions are typically shared between employees and employers; on average employers pay for some 70 per cent of contributions, and employees 30 per cent, but this varies a lot across pension plans. In some plans employers take care of the full contribution (e.g. the banking sector), while in others contributions are entirely paid by the workers (e.g., self-employed professionals).

It should be noted that one cannot simply look at—the change in—statutory contribution rates for employers and employees. What matters is who in the end is affected by the change in contributions, that is the real economic incidence of pension contributions. With perfect markets the statutory division between employers and employees is irrelevant; this is called the Invariance of Incidence Proposition (IIP). The IIP assumes flexible wages, and equal salience of employer and employee contributions. There is growing evidence, however, that the real world is more complex, and that behavioural effects and the institutional setting could play an important role in how labor supply, labor cost and wages are affected by a change in social security contributions (see e.g., Saez et al. (2012); Lehmann et al. (2013); Alvaredo et al. (2017); Adam et al. (2019); Bozio et al. (2017)).

The transition is further complicated by the large diversity in pension plans. Due to the decentralized character of second pillar pensions in the Netherlands there is a large variety across sectors, companies and professional groups. In total, there were some 600 different pension plans during the observation period of our data, 2006–2012. Due to consolidation this number has been reduced in the past decade to some 200 plans today.Footnote 3 The majority of employees (89 per cent) are in DB type contracts, but there is also a substantial group (11 per cent) having a DC plan. A special feature of existing DC plans is that employer contributions are ’progressive’, that is they increase with the age of the worker; the employee part of the contribution is uniform and independent of age. The progressive contribution rate reflects the aim of a uniform accrual in terms of pension benefits, similar to the DB schemes.

Then, also going from progressive employer contributions to uniform contributions in existing DC contracts, might affect incomes (including future pensions) of different age groups in this scheme. Furthermore, the labor market position may be influenced as well; lower employer contributions for older workers may strengthen their labor market position relative to younger workers (Knoef et al. 2020). Therefore, even in a DC environment there could be a need for additional compensatory measures in the transition from the current to the new system. As an alternative, DC plans can opt to continue their schedule for existing participants. Notably, this exemption may trigger a different—voluntary—transition before the nationwide transition to the new pension scheme. Namely, a transition of a DB plan to a current DC plan including the age-increasing contribution rate. Then, final pension benefits of existing participants are not affected, but only in case both gross wages and the age-increasing pension contribution rates are unaffected by this transition. Again, it is the incidence of pension contributions that matters.

Unlike pure taxes, for social security contributions also the benefit side is relevant. In theory, labor supply depends on the implicit tax, that is the contribution net of the implied benefit to the individual (Summers 1989; Gruber 1997; Ooghe et al. 2003; Disney 2004). In the presence of imperfect markets, however, future pension benefits may not be perfect substitutes to straight wages (Blinder 1982). Indeed, there is ample evidence that employees are likely to perceive pension contributions as a net tax due to mental accounting, myopia, limited visibility, less tangibility or a limited understanding of the pension system (Iturbe-Ormaetxe 2015; Brinch et al. 2017; Bozio et al. 2020; Luchak and Gunderson 2000; Dominitz et al. 2003).Footnote 4 Lack of salience may be particularly relevant for Dutch DB pensions as the link between contributions and individual benefits is known to be obscured due to the opaqueness of the system. Since data on the benefits of second pillar pensions are not available for the Netherlands, this paper will concentrate entirely on the contribution side of pensions.Footnote 5

In determining how workers of different age groups are affected by the pension reform it is important to obtain insight into mechanisms underlying the incidence of pension contributions. In this paper we estimate the impact of pension contribution rates on labor supply, labor cost and wages using a unique longitudinal administrative dataset for the Netherlands in the period 2006–2012. We focus at the level of pension funds, and within pension funds at certain groups of workers.

In contrast with the large literature on taxable income,Footnote 6 the literature on the response to payroll taxes and social security contributions (including pension contributions) is relatively limited (Saez et al. 2012, 2019; Adam et al. 2019). This is remarkable as payroll taxes average at 21.6% of labor cost, while income taxes average at 13.1% of labor cost in OECD countries.Footnote 7 The Dutch averages of 21.9% for payroll taxes (excluding pension contributions) and 14.5% for income taxes are not very different from the OECD averages. On top of this, a typical Dutch worker faces a marginal pension contribution rate of 22.5% in 2020. This percentage is among the highest worldwide.Footnote 8

The empirical literature on the response of wages and labor supply to (payroll) taxes distinguishes two different approaches. One approach is to exploit discontinuities in the payroll tax schedule and consider the cross-sectional distribution below and above the thresholds to identify the incidence. Examples include Kleven (2016), Alvaredo et al. (2017), and, for a similar analysis for the Netherlands, Bosch and Micevska-Scharf (2017). The other approach is to exploit tax variation over time and across individuals in a panel framework. This was pioneered in the seminal paper by Gruber and Saez (2002) on the elasticity of US taxable income to income taxes. Lehmann et al. (2013) follow a similar approach to analyze the incidence of payroll taxes in France at a one-year horizon. Using the fact that payroll taxes in France are fully paid by employers whereas the income tax is paid by the employees, they can compare their impact to assess the role of statutory rates. Their finding that the payroll tax is fully on employers while the income tax is effectively borne by workers suggests that statutory rates have a dominant impact, at least in the short run. A plausible explanation is that gross wages (excluding employer payroll taxes) are sticky in France at this time horizon. A similar finding is reached by Adam et al. (2019) for the United Kingdom.

We follow Lehmann et al. (2013) and Adam et al. (2019) and apply a panel analysis to analyze the impact of—marginal and average— contribution rates on total labor cost (per worker), hourly labor cost, and hours worked (regular hours and overtime hours). In contrast to these studies, we focus on pension contributions and look at the impact on a two year horizon. As pension contribution rates differ by individual pension fund we can exploit three sources of variation in contribution rates, thus improving the identification of the model. First, contribution rates vary across pension funds. Second, workers with a different income within the same pension fund face a different contribution rate (in terms of their labor cost) due to non-linearities (caps and floors) in the contribution rate schedule.Footnote 9 Third, there is considerable variation over time due to discretionary decisions on pension contributions by individual pension funds throughout our observation period. Finally, also the statutory shares of pension contributions paid by employees and employers vary over time and across pension funds. All these sources of variation can help us to provide more insight into the incidence of pension contributions.

Our main findings are as follows. First, labor supply (hours per worker) is unresponsive to both the marginal and average pension contribution rate. This may reflect inelastic preferences on working hours, or institutional barriers due to e.g. regulation on working hours. Second, the response of labor cost per worker to a change in average pension contribution rates is 70%; for the marginal rate no significant effect is found. This is at variance with the standard demand and supply model of wages according to which marginal rates are expected to be decisive. Rather, it may lend support to bargaining models, or point to institutional rigidities.

It may be noted that the finding of a 70%–30% split in incidence between employers and employees happens to be similar to the average of the statutory rates. At first sight this may seem in line with Lehmann et al. (2013) who explain their results by sticky gross wages. However, the distribution between employers’ and workers’ contributions varies substantially across pension funds. We tested for funds with different (changes in) employee and employer shares, and still find a similar coefficient (\(-0.7\)). This suggests that sticky wages—and therefore incidence according to statutory rates—are less convincing as an explanation, at least for the case of the Netherlands. This seems to leave us with the bargaining model as the most likely explanation of our results.

Our contribution to the literature is threefold. First, to our knowledge, we are the first to estimate the incidence of pension contributions in (quasi) mandatory funded pension schemes. Second, we provide insight into the role of labor market institutions in determining wages at the decentralised level of companies or industries. Third, we contribute to the recent research on the differential effects of average and marginal tax rates on the incidence of social security contributions.

The paper is organized as follows. Section 2 describes the Dutch institutional setting and our dataset. Section 3 briefly discusses the conceptual framework and relevant literature. In Sect. 4 we present our empirical methodology. Estimation results are given in Sect. 5. Section 6 concludes.

2 Institutional Setting and Data

The Dutch pension system consits of three pillars with a flat-rate basic state old-age pension as the first pillar, quasi-mandatory labor-related pensions as second pillar, and voluntary individual pension saving as third pillar. Statistics Netherlands estimates the relative size of the 2011 entitlements by pension pillar at 50% (first pillar), 44% (second), and 6% (third) (Bruil et al. 2015). The first pillar is financed on a Pay-As-You-Go basis, and the second and third pillar are funded. The Dutch second pillar is large by international standards. In total, accumulated savings in the Dutch second pillar scheme ranges up to over 200 per cent of GDP in 2020.Footnote 10 Measured as a share of GDP it is among the highest worldwide. Our analysis concerns this large second pillar of labor-related or ’occupational’ pensions.

Pensions in the second pillar are organized at a decentral level along sectoral, occupational, or company lines resulting in a large diversity of pension plans and contribution schemes. Pensions are mandatory for most employers and employees due to collective labor agreements; more than 85% of the workers is covered by a second pillar pension scheme.Footnote 11 Pension savings in the second (and up to some limit in the third pillar) are tax favored according to an EET (exempt-exempt-taxed) scheme: contributions are tax deductible whereas pension benefits are taxed according to the income tax; accumulated pension wealth is exempted from the capital income tax.

Second pillar pensions can be of the defined benefit (DB) type or the defined contribution (DC) type. About 94% of Dutch second pillar pension contributions is paid to a DB schemeFootnote 12, in most cases a sector-wide pension fund. In DB schemes participants build up entitlements (’pension rights’) at an annual accrual rate of about 1.8 per cent of the earned wageFootnote 13 (in excess of the threshold), thus aiming at a pension of about 70% of the average wage rate throughout one’s career. Contributions are uniform across ages of workers, and usually shared between employers and employees. Since both the contribution rate and the acrual rate are uniform across ages, the system is not actuarially fair; for any positive discount rate young workers pay too much whereas older workers pay too little.Footnote 14 The contribution rate is determined in consultation with (representatives of) employers and employees. Contribution rates may vary over time and between pension funds depending on the price of pension accruals—as determined by the interest rate, retirement age and life-expectancy—or in response to shocks to the funding ratios of pension funds.

DC schemes are mostly adopted by individual companies and some smaller sectors. These pensions are managed by company pension funds or by insurance companies. Participants’ contributions are accumulated in personal capital accounts and invested on financial markets. Employer contribution rates usually increase with the age of the participant.

Unfortunately, there is no central registration of the contribution schemes of individual pension plans. For this research we therefore have constructed a new data set by carefully spelling out the pension contracts of individual pension schemes. For practical reasons, we restrict our data set to the 30 main pension funds. This also implies that our data set covers only DB type pensions; the landscape of DC schemes is too scattered to obtain a reliable data set with reasonable effort. This limitation should be kept in mind when interpreting our results.

Pension contributions are levied on the earned pensionable wageFootnote 15 as far as it exceeds a certain lower threshold (in Dutch ‘franchise’). This threshold is usually close to the minimum wage and reflects the first pillar pension benefit to be expected for the future. Thresholds and caps are usually indexed with the inflation, but can occasionally also be adjusted by discretionary policies of pension funds.

Gross wages are determined by a collective bargaining process between representatives of employers and employees. Most collective labor agreements have a contract term of about two years.Footnote 16 Given this decentralised system of pensions and wage setting, there is a large variation across pension funds in labor costs, contribution rates, accrual rates, and thresholds and caps, and their evolution over time (Fig. 1, 2 and Table A.1–A.5 in the online Appendix). Within pension funds, labor cost and hours worked vary among individuals (Fig. 3) leading to a large within pension fund variation too (Fig. 4). Together this allows us to identify responses in labor supply, wages and labor cost to changes in contribution rates with great precision. Shares of employer and employee contributions fluctuate as well, though with a smaller magnitude over time (Table A.9 in the online Appendix).

Due to the thresholds and caps on pensionable wages we can also identify the effects of marginal and average contribution rates, separately. Interestingly, for average contribution rates there is a difference between regular contractual hours and hours in overtime. This is due to the peculiarity that the thresholds and caps are linear in the number of contractual hours of an individual worker. This is different for overtime work; these additional earnings do not affect the threshold and the cap. As a result, the average contribution rate of a worker is independent of his contractual hours, while this average rate does change with overtime hours. In practice, only a minority of workers work in overtime, since labor supply of most workers is constrained by regular hours; our data set reports positive overtime hours for about one in seven workers. For the marginal contribution rate only depends on whether the current wage is between the lower cap and the upper case, for both contractual and overtime hours. In our basic model we focus on total hours, and we will test for regular and overtime hours separately, thereafter.

Marginal pension contribution rate between threshold and cap (in thousands of euros) of several pension funds for fulltime employee, 2010

Average pension contribution rates by gross wage (in thousands of euros) of several pension funds for fulltime employee, 2010

Individual variation, 2010

Individual variation within ten large pension funds, change 2008–2010. In both boxplots, whiskers extend to include all data points within 1.5 interquartile range of the upper and lower quartile

2.1 Data

We use a rich administrative dataset that contains detailed job-level and earnings variables for the entire working population. The data is on a monthly basis, starting in January 2006 and ending in December 2012.Footnote 17 For each job and each month, we observe the number of days worked, hours worked (regular and overtime), and earnings.Footnote 18 Earnings are reported in full, and on forms directly filed by employers to the fiscal administration. The earnings variables can be considered reliable as the fiscal administration checks tax filings.

Unfortunately, pension contributions are missing in the administrative records. To fill this gap we have constructed a new data set on the contribution schemes from the pension funds’ annual reports focusing on the 30 largest pension funds. Our data covers about 80% of active participants in second pillar pension schemes.Footnote 19 Then, merging the job-level data with the nation-wide registration database with personal records provides us with a very detailed labor market and socio-demographic information on individuals. Our analysis is based on a sample of wage earners born between 1957 and 1987 and aged between 21 and 55 years in our sample period. Older ages are excluded since early retirement schemes may affect the participation decision and hours worked. For each year, we only include individuals who worked the entire year and did not change job to another collective labor agreement in the last two years.

An individual with a change in status on the covariate having partner or the covariate having children, is dropped in the corresponding years. Other years of such individuals are included as we do not expect an effect on labor income. Descriptives statistics are in online Appendix A.

3 Conceptual Framework and Literature

We analyse the impact of pension contributions on (hourly) labor cost, gross wages, net wages, and hours worked. Labor costs equal gross wages plus employer contributions. For labor supply we focus on the hours decision; the participation decision (the extensive margin) falls beyond the scope of our analysis as we focus on individuals in the same job (or pension fund) during the entire observation period. We also neglect behavioral responses other than the hours response. The taxable income literature points to the existence of such non-hours responses (Blomquist and Selin 2010): individuals can increase productivity by supplying more effort without increasing the hours worked, and also there can be a shift from high taxed income to more tax favorable fringe benefits. In both cases the impact of a higher tax rate on effective labor supply may be overstated. We believe that these effects are fairly small compared to the decision on reported hours worked.

3.1 Standard Demand and Supply Model for Labor

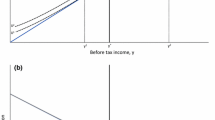

According to the standard textbook model, in a perfect labor market the incidence of (payroll) taxes is fully determined by the wage elasticities of demand (\(\varepsilon _D < 0\)) and supply (\(\varepsilon _S > 0\)). This model assumes fully flexible wages and perfect information on employer and employee taxes (including contribution rates). Consider Fig. 5 showing the demand and supply schedule as a function of the net wage. In the absence of taxes (and pension contributions), the gross wage and labor cost would be equal to the net wage. Now consider the impact of an increase in employee contributions or employer contributions. Both are regarded as a tax by the worker leading to an upward shift in the supply schedule in Fig. 5 and a new equilibrium with a higher hourly labor cost \((w/h)'\), a lower volume of labor \(E'\) and lower net net wages. The magnitude of the effects depends on the demand elasticity relative to the supply elasticity. Net wages decrease by more if hourly labor costs increase less as the supply elasticity is lower (that is, a steeper supply curve in the graph). It is often assumed that the demand elasticity for labor is high relative to the supply elasticity so that the real burden of taxation is primarily on the workers (Saez et al. 2019). Taking \(\varepsilon _S\) as the compensated supply elasticity a higher tax leads to a fall in net wages by \(\varepsilon _D/(\varepsilon _S - \varepsilon _D)\) and a rise in labor cost by \(\varepsilon _S/(\varepsilon _S - \varepsilon _D)\).

In this framework the division of tax rates between employers and workers is irrelevant. This ‘Invariance of Incidence Proposition’ (IIP) requires gross wages to be fully flexible: gross wages fall if the share of employer contributions rise, and they rise if the share of employee contributions are raised. Only if—by coincidence—the split in tariffs is equal to the weights following from the elasticities then the actual incidence would be equal to the statutory incidence. A change in the pension contribution rate would then leave the gross wage unaffected. For the Netherlands, this would occur if the demand elasticity happens to be half of the supply elasticity; then the real incidence matches with the usual \({2}/{3}-{1}/{3}\) division for employers and employees − in statutory rates.

Effect of an increase in the pension contribution rate on hourly labor costs. Notes: This figure shows the effect of an increase in the pension contribution rate on hourly labor costs following a standard labor demand and supply model

Average wages are irrelevant for marginal decisions. This holds for the standard model, but also in a wider class of models that derive wages and labor supply from maximizing some objective function (see Lehmann et al. (2013) for a discussion). Average tax rates may, however, affect the equilibrium in a different manner, namely through the income effect on labor supply. Higher average tax rates then results in a larger supply of labor, leading to lower hourly wages and labor cost in equilibrium for any finite \(\varepsilon _D\).

3.2 Beyond the Standard Model

So far we have considered a homogenous market with one type of labor. In a more realistic setting with segmented markets the demand elasticities may vary according to the circumstances, depending on how easily employers can substitute workers for another and how easily they can adjust their production capacity in response to changing labor cost. On the supply side we focus on the hours decision; this depends on the preferences of individual workers on working hours and the ease at which hours worked can be adjusted within their job. Here, the institutional characteristics of the labor market and the type of labor contracts may play a dominant role. To gain further insight, we consider both regular, contractual hours and overtime hours. For the latter, one may expect a higher elasticity than for regular hours.

In practice, average rates also prove important for the impact of social security contributions as shown in Adam et al. (2019) and Lehmann et al. (2013)), and also in our analysis. For this we need a different framework than the standard model. For example in a bargaining model employers and workers share the quasi-rents (‘surplus’) according to their bargaining power. As the surplus depends on average taxes, there can be a direct effect on wages and labor cost as in the model of Kalai and Smorodinsky (1975)Footnote 20

While in the bargaining framework average contribution rates could matter, there is still no role for the statutory split of contribution rates between employers and employees. There is growing evidence that such institutional factors can have an important impact, certainly in the shorter term. Several explanations are at hand here. First, taxes and in particular SSC rates may be less salient than presumed in theoretical models (Chetty 2009). There is evidence that the employer contribution tends to be less visible for workers than a contribution that is paid out of net wages (Iturbe-Ormaetxe 2015). Also, employers may consider the sum of SSC contributions as a burden for the company without assigning them to individual workers. Saez et al. (2019) suggest that also equity concerns may curb wage differentiation between (generations of) workers within a firm or sector. Other evidence suggests that gross wages may be sticky in the short and medium term (Lehmann et al. 2013; Adam et al. 2019). This may be due to e.g. frictions that make adjustments costly, periodical centralized wage bargaining, or the presence of strong labor unions that resist adjustment in wages. With sticky gross wages, SSC contributions will be distributed between employers and employees according to the statutory rates. In this paper we take an agnostic and explorative empirical approach just aiming to provide more insight into what effects are important in practice, and how these could be related to theory.

4 Estimation Methodology

4.1 Model Specification

We estimate a panel-based first difference model for four different outcome variables. This is a standard approach in the elasticity of taxable income literature (Gruber and Saez 2002; Lehmann et al. 2013; Weber 2014; Adam et al. 2019). Firstly, we estimate the elasticity of real labor cost w per worker to the marginal \(\tau\) and the average \(\rho\) net-of-tax rates (that is, 1 minus tax rate; we use ’tax rate’ also for SSC contributions here):

where w is the real labor cost of the individual employee i, in year t, and \(\Delta\) is the two-year change between period \(t-2\) and t.Footnote 21 The considered individuals are affiliated to the same pension fund in periods \(t-2\), \(t-1\) and t.

A two-year difference \(\Delta\) is also adopted in the baseline specification in Weber (2014). This delay of two years can be motivated by the delay from wage adjustments in collective labor agreements. Then, each \(\beta\) coefficient in (1) is a combination of the one-year response in year t to changes in contribution rates starting in the years \(t-1\) and t, and the two-year response in year t to changes in contribution rates starting in year \(t-1\). Responses to earlier changes in contribution rates are captured by the error term \(u_{it}\). Weber (2014) contains an in-depth analysis on the econometric issues in estimating Eq. (1). In our sensitivity analysis (online Appendix B), effects are not very different for one-year differences (which are studied in Lehmann et al. (2013)) and three-year differences (as in Gruber and Saez (2002) and Kleven and Schultz (2014)).

Equation (1) includes both the marginal net-of-tax rate \(\tau\) and the average net-of-tax rate \({\bar{\rho }}\). The exogenous variables in \(X_{i,t-2}\) include individual characteristics, pension fund dummies, year dummies, and a ten-piece linear spline of base-year labor cost \(f(\log w_{i,t-2})\) and base-year labor cost growth \(g(\log ( w_{i,t-2} ) - \log ( w_{i,t-3} ) )\) (see Sect. 4.3). The error term \(u_{it}\) can capture time-variation in omitted variables as well as unobserved heterogeneity across individuals. Similar to the standard approach in the tax literature (Gruber and Saez 2002), we obtain changes in net-of-tax rates by applying the pension scheme in year t on the inflated base-year gross wage: \({\hat{gw}}_{i,t-2} = {gw}_{i,t-2} \pi _{t-2} \pi _{t-1}\) with \(\pi _{t-i}\) the average growth in gross wages gw between period \(t-i\) and \(t-i+1\).

Following Lehmann et al. (2013), we take the coefficient \(\beta _\tau\) as representing the compensated elasticity. This elasticity is measured by assuming that the amount of taxes (and pension contributions) remains constant. The change in the average rate is measured such that the initial labor cost w is compensated for the effects of changes in the tax rate schedule; this is indicated by the upper bar above \(\rho\).

Our second estimation involves the elasticities of the real hourly labor cost \({\bar{w}} = w/h\) for worker i,

In the absence of behavioral responses in effort (without supplying more hours), the coefficients on the net-of-tax rate in (2) reflect the incidence of pension contributions in hourly labor cost. Coefficients close to zero indicate that the burden is on workers, whereas coefficients close to one indicate incidence on employers.

Thirdly, we can estimate the elasticities of hours worked,

The estimates for the elasticities \(\beta _{\tau }\) and \(\beta _{\rho }\) in (3) refer to the behavioral effect in terms of the hours response. In the basic model we estimate this equation for total hours. Afterwards, we will repeat this estimation for regular hours and overtime hours separately.

Finally, we study the separate effects of employee rates (\(\tau ^e\) and \(\bar{\rho ^e}\)) and employer rates (\(\tau ^r\) and \(\bar{\rho ^r}\)) by splitting the explanatory variables in (1),

The employee net-of-rate is measured with respect to the gross wage. The employer net-of-rate we measure with respect to labor cost w. This transformation ensures that the net wage simply equals the product \(\rho ^e \rho ^r w\).

In the baseline model, individuals are weighted by the inverse of the corresponding pension fund size as measured by the number of participants in that year. This is important because the largest pension funds are much larger than the other pension funds (Table A.6). If we were to apply equal weighting, our estimates would be strongly tilted towards the largest pension funds and we would lose a large part of the variation between different pension funds. As a sensitivity test, we perform unweighted regressions.

We use robust standard errors that adjust for heteroskedasticity and cluster standard errors by pension fund since individuals within the same pension fund tend to face similar shocks to pension contributions and labor cost.

A possible concern is that exogenous factors changed substantially during our sample period, thereby affecting our estimates. However, social security contributions were very stable throughout our sample period. For instance, the first pillar contribution rate was stable at a flat 17.9% of gross income. Individuals were entitled from age 65 onwards on a flat pension benefit of the first pillar pension.

4.2 Potential Endogeneity of Pension Contributions

A causal interpretation of the pension contribution rates is only valid in our estimation equations if the change in contribution rates (\(\Delta \log \tau\) and \(\Delta \log {\bar{\rho }}\)) is uncorrelated with the error term u. However, several sources of endogeneity can result in a nonzero correlation.

First, there could be omitted variables such as pension fund characteristics and macro-economic shocks that simultaneously affect labor cost and contribution rates. To correct for this, we include pension fund dummiesFootnote 22 and year dummies as exogenous variables in \(X_{i,t-2}\). Year dummies can capture fluctuations in macroeconomic conditions due to e.g., stock market returns, changes in discount rates, and inflation rates. Still, time-varying characteristics of pension funds are a source of variation. One way to correct for this is to include interacted pension fund and year dummies. Unfortunately, this would also take away relevant variation caused by pension contributions. Second, because of nonlinearities in the pension contribution system (Fig. 2), there could be reverse causality. The lower threshold for gross wages on pension contributions implies that the marginal contribution rate can change with income and thus with labor cost. To resolve this issue, we instrument the change in the marginal contribution rate (\(\Delta \tau\)) by a prediction of this rate. The prediction is based on the inflated base year’s gross wage, i.e., \({\hat{gw}}_{i,t-2} = {gw}_{i,t-2} \pi _{t-2} \pi _{t-1}\).Footnote 23 Let \(C_{it}(w)\) denote the pension contribution rate that corresponds to labor cost w of individual i in year t. An instrument for the marginal net-of-contribution rate is

Using (5), we instrument the two-year change in the marginal net-of-pension contribution rate,

In the baseline model we drop all observations with labor cost above 50,000 euro. The predicted change in marginal rates is often zero if labor cost exceed 50,000 euro (Fig. 1 and Table A.3). As a consequence, the dependence of labor cost on contribution rates is differnt above the cap, if existent (Fig. 2).

Notice that the average net-of-contribution rate \(\rho\) is already included as a predicted rate in (1)–(4) to ensure that the effect on \(\rho\) is a compensated elasticity (see Sect. 4.1).

4.3 Changes in Labor Cost Unrelated to Pension Contributions

Another methodological concern relates to mean reversion. An unexpected low income in period \(t-2\) is more likely to be followed by a higher income in period t. This is problematic in estimating Eq. (1), since base-year income \(w_{i, t-2}\) (and thus \(\Delta w_{i, t}\)) is then correlated with the error term \(u_{it}\). A related concern is an exogenous change in labor cost unrelated to pension contributions and taxes. For instance, technological progress might affect labor cost per worker if it favors high-skilled workers compared to low-skilled workers. This can shift the wage distribution.

Including a function of base-year income might control for both methodological concerns. This function can be linear (Auten and Carroll 1999) or more complicated such as a flexible 10-piece spline (Gruber and Saez 2002). Nonetheless, the source of the two types of methodological concerns differs which calls for different corrections. This motivates us to follow Kopczuk (2005) and Kleven and Schultz (2014) who use two ten-piece linear splines, one spline based on base year growth rates \(\log (w_{i,t-2}/w_{i,t-3})\) to control for mean reversion, and another spline based on base year levels \(\log (w_{i, t-2})\) to control for shifts in the wage distribution. Notice that the additional lag term in the growth spline disables a year of dependent observations in the regression.

5 Estimation Results

5.1 Preliminary Evidence at Pension Fund Level

Figure 6 depicts the two-year log change in labor cost (\(\Delta \log (w)\)) and in the average net-of-tax rate for pension contributions (\(\Delta \log (\rho )\)). As a preliminary result for Eq. (1), a linear trend line across the full set of points has a slope coefficient of −1.13. This estimate is not significantly different from minus one, since the corresponding standard error equals 0.18. Thus, it indicates that labor costs per worker change with the pension contribution. The pension funds at banks are potential outliers with a pronounced impact on the slope coefficient (Table A.9).Footnote 24 Dropping the banks from the sample yields a similar slope coefficient of −1.05 with standard error 0.29. This is a rough indication that the employers bear the major share of changes in pension contributions in these years.

Two year log-change average net-of-tax rate \(\rho\) and two year log-change labor cost w. Annual changes at pension fund level. Red squares correspond to the three pension funds of banks, blue dots are from non-banks. Sample period 2006–2012

The preliminary results are at the pension fund level. It does not exploit within pension fund variation (Figure A.1), nor does it allow for pension fund-specific effects in (1). For instance, certain participants may face a larger increase in wage rates than others within the same pension fund. In addition, pension funds might adopt different policies in pension contribution rates and also the wage growth can differ between different sectors. This illustrates that the (implicit) assumption of a pension fund-independent intercept in Fig. 6 can be violated. The full analysis with individual employee data in Sect. 5.2 resolves the issues.

5.2 Main Results

The first-stage results using tax changes at the individual level as explanatory variables can be found in Table A.10. The coefficient is significant and positive (0.432) and the instrument is not weak (F-test statistic is 244.7).

Table 1 documents the estimation results for Eq. (1) with total labor cost per worker as the dependent variable. Six different specifications are reported. Column (1) is the baseline specification. Full results are given in Table A.11 in the online Appendix. Column (2) differs from the baseline by omitting the weighting of participants according to the pension fund size. In column (3), participants of the public sector fund ABP are excluded to account for the fact that political factors may affect their contribution rates, accrual rates, and the employee-employer incidence differently for a public sector pension fund than a private sector pension fund. Likewise, the results without the banking sector can differ from other sectors (column (4)): pension funds in the banking sector tend to charge higher and more volatile contribution rates (Table A.9 and Fig. 6). Moreover, employee contributions tend to be low, or even absent. Column (5) shows the impact when including incomes above 50K, which exceed the cap on pensionable wages in a substantial number of cases (Table A.3). Column (6) reports the results with additional noise from social security contributions.

The results prove very robust.Footnote 25 The coefficient of the marginal net-of-tax rate (\(\beta _\tau\)) is small and insignificant in all specifications in Table 1. The coefficient for the average net-of-tax rate (\(\beta _\rho\)) is negative and significant, and robust over all specifications. It indicates that labor costs react by about 70% of a change in average pension contribution rates. With the exception of the somewhat more negative coefficient in column (5), the elasticity \(\beta _\rho\) differs in each specification significantly from minus one at the 10% level. This suggests that a smaller, yet significant, part of about 30% is paid by employees by means of a lower net wage.

The employer’s share of 70% is high compared to what is usually found on the basis of plausible demand and supply elasticities (cf. Melguizo and González-Páramo (2013)). The fact that average net-of-tax rates have a significant and negative effect means that employers face a non-negligible incidence. This concurs with the standard model discussed in Sect. 3.1 assuming that demand elasticity is sufficiently high, which seems plausible in our case. That marginal rates are not significant is also at variance with the standard demand and supply model.

Interestingly, the 70–30% split between employers and workers is close to the average statutory incidence of 69%. At first sight, this may suggest that the statutory incidence determines the economic incidence and that gross wages are sticky. However, the result also remains when the statutory employer-employee shares deviate substantially from a 70–30% split, e.g., in the banking sector. Dropping the banking sector (column (4)) does not give a lower value for the employer share. The same split could well be due to the relative power of employers and workers in the bargaining game (see Sect. 3.2). In fact, this bargaining may also be the underlying factor under the statutory split.

To gain more insight in the underlying mechanism we can decompose the impact on total labor cost per worker into the effect on hourly labor cost and on the number of hours worked per worker. Table 2 presents the effects on hourly labor cost. The results are largely the same as for total labor cost. The effect of the marginal net-of-tax is again insignificant; for the average rate the coefficient turns out to be slightly more negative (\(-0.8\)) than for total labor cost. Thus, a 1%-point increase in pension contributions increases hourly labor cost by about 0.8%. This similarity in result for total and hourly labor cost concurs with the insignificant effects found for labor supply, both for the marginal and average rates (Table 3). The low supply elasticity (as measured on the intensive margin) may have to do with (i) preferences, (ii) institutional barriers for individual workers to adjust hours worked, or (iii) non-salience of pension contributions (Brinch et al. 2017).

The absence of a labor supply response is inconsistent with the standard demand and supply model. Even, if only a minority of workers with positive overtime hours would react to the marginal pension contribute rate one would expect a positive impact on labor supply. For bargaining type of models the labor response is not essential to the model; here the tax is shared between employers and workers, irrespective of labor demand and supply responses.

5.2.1 Regular and Overtime Hours

The above results for labor supply remain the same if we look at contractual (regular) hours and overtime hours separately. For overtime hours the usual effects are expected for marginal, and average net-of-tax rates. In contrast, for contractual hours both average and marginal rates collapse as the thresholds (and caps, if existent) vary proportionally with contractual hours worked. For both types of working hours we find insignificant labor supply responses. (Tables 4 and 5). The mostly insignificant elasticities are similar to our findings with aggregate hours worked (Table 3).

5.2.2 Separating Employer and Employee Pension Contribution Rates

Further insight into the role of statutory rates can be found by separately testing for the impacts of employer and employee contribution rates. According to the Invariance of Incidence Proposition (IIP) the statutory split of the pension contributions into employer and employee shares is irrelevant for the (long-run) economic incidence. We attempt to study this using the variation in pension contributions paid by employees and employers in our data. The results of separating employee and employer pension contribution rates (Eq. (4)) are presented in Table 6.

The insignificant results for marginal rates and significantly negative results for average rates are in line with our previous findings. However, the fact that labor costs respond stronger to employee rates than to employer rates (\(|\beta _{\rho e}| > |\beta _{\rho r}|\)) is fairly counter-intuitive. Either one would expect similar results for both rates according to the Invariance of Incidence Proposition (IIP), or stronger effects of employer rates than worker rates if wages would be sticky. One possible explanation could be that employee rates are more salient than employer rates (Iturbe-Ormaetxe 2015). However, although this may seem plausible, it cannot explain the size of the coefficients which are found to be significantly larger than 1 in absolute terms.

Although standard errors of our results in Table 6 are large, we suggest the following three technical explanations for this finding. First, one may question whether there is enough variation between employer and employee contribution rates. As the correlation matrix shows (Table A.12), employer and employee rates are correlated (0.4). This commonality hampers identification of separate effects.

Second, contribution rates show an increasing trend in our sample (Tables A.8 and A.5). This may have an upward effect on \(|\beta _{\rho e}|\) if workers are particularly keen to be compensated for increases in employee rates. Notice that the year fixed effects in Eq. (4) will pick up the general trend, not the specific trend for employee contribution rates.

Third, the variance of average employee rates is about half of the variance for the average employer rate. Also the statutory rates for employees are about half of those for employers (Table A.9). This concurs with the 70–30% economic incidence (employer-employee) found in our analysis. The combination of a strong correlation and small changes in employee rates can inflate the coefficients of the average net-of-pension employee rate and the corresponding standard error. To gain more insight in this explanation, we run sensitivity tests based on different ratios of employer and employee rates (Table 7).

In Table 7 we separate our main sample into subsamples based on either the ratio of the employee-employer pension contribution rate in the base year, or on the two year change in the employee-employer share. Interestingly, we find that the coefficient of average net-of-tax contribution rate is not significantly different from \(-0.7\) even though the statutory splits in the subgroups differ from 70–30%. The labor costs of pension funds with a high \(\frac{\rho e}{\rho r}\) are more sensitive to the pension contributions. Since the difference in incidence between pension funds with high and low \(\frac{\rho e}{\rho r}\) is insignificant, we conjecture that bargaining power underlying the 70–30% split is the dominant driver. Within the group of pension funds with a high employee share, the average net-of-rate coefficient is not significantly different from zero and one. This might be caused by a lack of variation in average net-of-rates between and within pension funds with high employee shares.

Additional robustness checks are presented in online Appendix B. Our main finding of a 70–30% split for changes in the average rate is robust for (i) considering one-year or three-year differences instead of two-year differences, (ii) omitting the growth spline or income spline, (iii) considering young workers, old workers, men or women separately, or (iv) omitting time variation or within pension fund variation as a source of variation. Notably, the variation between pension funds appears a crucial driver for the average 70–30% split as this split is not obtained for any of the considered large single pension funds in our sample (Table B.7).

6 Conclusion

The pension reform in the Netherlands will abolish the implicit subsidy from younger to older workers due to the uniform contribution policy in current DB pensions. This gives rise to a serious transition problem as a substantial group of—mainly older – workers will suffer a loss in pensions when going from the DB pensions to actuarially fair DC pensions. Additionally, there is a problem with current DC schemes too, as progressive contributions that rise with age are going to be replaced by flat, age-independent rates. Our study aims to shed light on the labor market impact of these changes in contribution policies by considering the incidence of contribution rates. This in turn determines the effects on labor supply, labor cost and wages. Insight into these effects is important to assess the labor market effects of a change in the contribution schedule.

Using a large administrative dataset for the Netherlands we identify the short to medium run impact of marginal and average contribution rates as well as employer and the employee shares in contributions following a similar panel approach as Lehmann et al. (2013) and Adam et al. (2019). Since we also observe hours worked—unlike Lehmann et al. (2013), but like Adam et al. (2019)—we can separate the effect on labor cost into the effects on hourly labor cost and hours worked. This helps us to provide more insight into the incidence of pension contributions and its underlying behavioral effects.

Our main findings are as follows. First, there is no discernable response in labor supply (in hours, contractual as well as overtime) by individual workers to changes in pension contributions. Second, we find little effect of the marginal contribution rates on wages. Third, average contribution rates do have a significant impact on labor cost: changes in average pension contributions are on average for 70% passed through onto employers; workers take only 30% of the burden. Consequently, a 1%-point change in the average pension contribution rate results in a 0.8% change in hourly labor cost, close to the 0.7% change in labor cost. Fourth, when distinguishing employee and employer rates marginal rates are again insignificant while average rates have a strong effect. For the size of the latter coefficients we find however unsatisfactory results, in particular that labor costs are more sensitive to employee rates than to employer rates which is not very intuitive. This finding should be treated with caution as it can be the result of a methodological artefact.

A limitation of our analysis concerns the absence of the benefit side of pensions. For our results, we believe this is less of a problem as previous literature indicates that workers tend to perceive the benefit of pension contributions as fairly small. This holds particularly true for existing DB plans.

Furthermore, our analysis is restricted to the traditional DB plans. Although, these plans are by far dominant in the Netherlands—taking a share of 90% of all pensions—it would be interesting to investigate also the smaller group of existing DC plans too. In the transition towards the new pension system these plans offer a special problem as progressive employer contributions will have to be replaced by age-independent, flat rates, at least for new entrants in such pension funds. Nevertheless, even though these DC pensions fall outside the scope of our empirical analysis some important lessons can be drawn from our results for the larger DB pension plans. On the basis of our results it can be expected that also for the DC plans the standard demand-and-supply model has limited explanatory power, at least in the short and medium term. Institutional factors and collective bargaining mechanisms appear to play a significant role in the responses to changing pension contributions. Also, responses in labor supply (hours) can be expected to be limited.

Our finding of a 70 per cent incidence on employers is high compared to what is predicted by the standard demand and supply model given the absence of a labor supply response. It is also high compared to older research on incidence; in a meta-analyse Melguizo and González-Páramo (2013) conclude that between 60 to 90 per cent of the burden of a labor tax is borne by the employee rather than the employer. Interestingly, the result of a 70–30% split in the burden of taxation matches very well with the statutory division in employer and employee contribution rates. At first sight, this may seem to support earlier findings on sticky wages by Lehmann et al. (2013) and Adam et al. (2019). However, when testing for funds with deviating statutory splits this result proves not robust. For example, also for the banking sector we find a similar 70–30% split in incidence whereas employers take 100% of the statutory rates.

This is not to say that the standard demand and supply model is irrelevant to the incidence of pension contributions, all together. Due to several kinds of institutional and informational barriers adjustments in wages and labor may take more time than considered in our estimation period. Over a longer time horizon it is well possible that the more fundamental factors underlying demand and supply of labor become decisive for the incidence of taxes and social security contributions relative to institutional rigidities and habits that may dominate in the short term. Future research may shed more light into these highly relevant issues.

Notes

This involves transitions to a different pension scheme as well as employee starting as a self-employed (i.e., outside the pension scheme), or vice versa.

Source: Dutch Central Bank, Table 8.17.

In a study for US school teachers, Fitzpatrick (2015) finds that employees only attach a value of 20 per cent to the corresponding increase in pension benefits.

Actually, calculating the value of pension rights at the individual level would have been very hard given the complex and largely implicit character of the Dutch DB contract. Moreover, the benefit side of pensions was fairly stable during the observation period considered in this paper.

OECD (2021), Taxing wages 2021, Table 1.2.

OECD Pensions at a Glance 2021, Table 8.1.

Note that within-pension fund variation between workers of different employers is limited as wages and pension contributions are both determined in sector-wide agreements.

Source: OECD Pension Statistics.

Source: Statistics Netherlands.

Source: Dutch Central Bank.

Since 2015, the maximal accrual rate for the fiscal allowance is 1.875%.

Apart from that, contribution rates can differ from actuarial fairness due to, e.g., temporary mark-ups to recover from low funding ratios, smoothing of contribution rates over time, or individual differences in life expectancy within pension funds.

The pensionable wage is the wage below some upper cap that differs between pension funds. Currently, the caps are maximized by a federal cap (114.866 euro for a fulltime worker in 2022), but this federal cap was only introduced after our sample period.

Evasion of pension contributions is very limited. Employees of non-paying firms have a legal lifelong right to claim a pension accrual at the pension fund, irrespective of the paid historic contribution. This ensures that there is an active policy of pension funds to search for employers who do not pay pension contributions for their employees.

The datasets are accessed through a remote connection to non-public micro datasets of Statistics Netherlands.

Monthly earnings are broken down into regular earnings and overtime earnings.

Source: Dutch Central Bank.

More so than the Nash bargaining model in which marginal tax rates are decisive for the incentive to bargain.

Labor cost w includes certain fringe benefits—which are absent in regular gross wages—insofar the fringe benefits are included in the formal wage for social insurance (‘sv-loon’). In the baseline model, labor cost is exclusive of social security contributions which were very stable throughout our sample period.

An alternative to pension fund dummies is to include funding ratios. Unfortunately, data on funding ratios is not available for the entire sample period.

In Fig. 6, the maximal value of Cook’s distance is at most 0.27, due to the observation of ABN Amro 2010–2012. Although this maximal value seems reassuring, Cook’s distance measure pertains to individual observations rather than a specific group of observations.

The estimated residuals exhibit in none of the estimates significant positive serial correlation at a two-year lag.

References

Adam, S., Phillips, D., & Roantree, B. (2019). 35 years of reforms: A panel analysis of the incidence of, and employee and employer responses to, social security contributions in the UK. Journal of Public Economics 171.

Alvaredo, F., Breda, T., Roantree, B., & Saez, E. (2017). Contribution ceilings and the incidence of payroll taxes. De Economist, 165(2), 129–140.

Auten, G., & Carroll, R. (1999). The effect of income taxes on household behavior. Review of Economics and Statistics, 81(4), 681–693.

Blinder, A. S. (1982). Private pensions and public pensions: Theory and fact. NBER Working Paper (w0902).

Blomquist, S., & Selin, H. (2010). Hourly wage rate and taxable labor income responsiveness to changes in marginal tax rates. Journal of Public Economics, 94(11), 878–889.

Bosch, N., & Micevska-Scharf, M. (2017). Who bears the burden of social security contributions in the Netherlands? Evidence from Dutch administrative data. De Economist, 165(2), 205–224.

Bozio, A., Breda, T., & Grenet, J. (2020). Does tax-benefit linkage matter for the incidence of social security contributions? iZA Discussion Paper.

Bozio, A., Breda, T., & Grenet, J. (2017). Incidence and behavioural response to social security contributions: An analysis of kink points in France. De Economist, 165(2), 141–163.

Brinch, C., Hernæs, E., & Jia, Z. (2017). Salience and social security benefits. Journal of Labor Economics, 35(1), 265–297.

Bruil, A., Schmitz, C., Gebraad, J., & Bhageloe-Datadin, R. (2015). Totale pensioenaanspraken van Nederland in beeld. Technical report, Statistics Netherlands.

Chetty, R. (2009). Is the taxable income elasticity sufficient to calculate deadweight loss? The implications of evasion and avoidance. American Economic Journal: Economic Policy, 1(2), 31–52.

Deelen, A., & Verbeek, W., (2015). Measuring downward nominal and real wage rigidity–Why methods matter. CPB Netherlands Bureau for Economic Policy Analysis Discussion Paper 315.

Disney, R. (2004). Are contributions to public pension programmes a tax on employment? Economic Policy, 19(39), 268–311.

Dominitz, J., Manski, C. F., & Heinz, J. (2003). Will social security be there for you?: How americans perceive their benefits.

Feldstein, M. (1995). The effect of marginal tax rates on taxable income: A panel study of the 1986 Tax Reform Act. Journal of Political Economy, 103(3), 551–572.

Fitzpatrick, M. D. (2015). How much are public school teachers willing to pay for their retirement benefits? American Economic Journal: Economic Policy, 7(4), 165–88.

Gruber, J. (1997). The incidence of payroll taxation: Evidence from Chile. Journal of Labor Economics, 15(S3), S72–S101.

Gruber, J., & Saez, E. (2002). The elasticity of taxable income: Evidence and implications. Journal of Public Economics, 84(1), 1–32.

Iturbe-Ormaetxe, I. (2015). Salience of social security contributions and employment. International Tax and Public Finance, 22(5), 741–759.

Kalai, E., & Smorodinsky, M. (1975). Other solutions to Nashs bargaining problem. Econometrica, 43(3), 513–518.

Kleven, H. J. (2016). Bunching. Annual Review of Economics, 8, 435–464.

Kleven, H., & Schultz, E. (2014). Estimating taxable income responses using Danish tax reforms. American Economic Journal: Economic Policy, 6(4), 271–301.

Knoef, M., Muns, S., & Van Soest, A. (2020). Arbeidsmarkteffecten van de pensioenpremiesystematiek, netspar Design Paper 165. Netspar: Tilburg.

Kopczuk, W. (2005). Tax bases, tax rates and the elasticity of reported income. Journal of Public Economics, 89(11–12), 2093–2119.

Lehmann, E., Marical, F., & Rioux, L. (2013). Labor income responds differently to income-tax and payroll-tax reforms. Journal of Public Economics, 99, 66–84.

Lever, M., Bonenkamp, J., & Cox, R. (2013). Eindrapportage ‘voor- en nadelen van de doorsneesystematiek’. Den Haag: CPB Policy Brief, Centraal Planbureau.

Luchak, A. A., & Gunderson, M. (2000). What do employees know about their pension plan? Industrial Relations: A Journal of Economy and Society, 39(4), 646–670.

Melguizo, A., & González-Páramo, J. M. (2013). Who bears labour taxes and social contributions? A meta-analysis approach. SERIEs, 4(3), 247–271.

Ooghe, E., Schokkaert, E., & Flechet, J. (2003). The incidence of social security contributions: An empirical analysis. Empirica, 30(2), 81–106.

Saez, E. (2003). The effect of marginal tax rates on income: A panel study of bracket creep. Journal of Public Economics, 87(5), 1231–1258.

Saez, E., Slemrod, J., & Giertz, S. H. (2012). The elasticity of taxable income with respect to marginal tax rates: A critical review. Journal of Economic Literature, 50(1), 3–50.

Saez, E., Schoefer, B., & Seim, D. (2019). Payroll taxes, firm behavior, and rent sharing: Evidence from a young workers tax cut in Sweden. American Economic Review, 109(5), 1717–1763.

SER. (2019). Naar een nieuw pensioenstelsel, sER-advies. Sociaal-Economische Raad: Den Haag.

Summers, L. H. (1989). Some simple economics of mandated benefits. American Economic Review, 79(2), 177–183.

SZW. (2020). Wet toekomst pensioenen, concept Memorie van Toelichting. Ministerie van Sociale Zaken en Werkgelegenheid: Den Haag.

Weber, C. (2014). Towards obtaining a consistent estimate of the elasticity of taxable income using difference-in-differences. Journal of Public Economics, 117, 90–103.

Funding

Casper van Ewijk and Sander Muns received financial support from Instituut Gak. Maja Micevska Scharf received financial support from a Netspar Theme Grant.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary Information

Below is the link to the electronic supplementary material.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Bosch, N., van Ewijk, C., Micevska Scharf, M. et al. The Incidence of Pension Contributions: A Panel Based Analysis of the Impact of Pension Contributions on Labor Cost, Wages and Labor Supply. De Economist 170, 107–132 (2022). https://doi.org/10.1007/s10645-022-09401-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10645-022-09401-z