Abstract

In this paper, we investigate the performance of four semi-parametric estimators in the wavelet domain in order to estimate the parameter of stationary long-memory models. The goal is to consider a wavelet estimate for the fractional differencing parameter d where the time series exhibit heavy tails. We show by Monte Carlo experiments that the wavelet Exact Local Whittle-type estimator improves considerably the other suggested wavelet-based estimators in terms of smaller bias, Root Mean Squared Error and variance. Furthermore, the simulation results show that the wavelet periodogram estimators perform better in most cases than wavelet ordinary least square estimate methods when the sample size is increased.

Similar content being viewed by others

Notes

See Whittle (1951) for more details about the estimation method.

In this paper, we will concentrate on the fractional integrated stationary processes.

See Beran (1994) for more details on long memory processes.

A robust theoretical framework for critically sampled wavelet transformation is Mallat’s Multiresolution Analysis (for more details, see Mallat 1989).

In practice, the Discrete Wavelet Transform (DWT) is implemented via a pyramid algorithm (see Mallat 1989) which is a design method underlying the conception of the DWT and the construction of the wavelet bases.

A modified version of the DWT is the non-decimated or Maximal Overlap Discrete Wavelet Transform (MODWT). The MODWT algorithm carries out the same filtering steps as the standard DWT, but does not subsample (decimate by 2); therefore the number of scaling and wavelet coefficients at each level of the transform is the same as the number of sample observations (see Percival and Walden 2000; Gençay et al. 2002; Crowley 2007 for more details).

See Jensen (1999) for more details about the estimation method.

The Hurwitz zeta function is a generalization of the Riemann zeta function that is defined by \(\zeta (r)=\frac{1}{\Gamma (r)}\int _{0}^{+\infty }\frac{ u^{r-1}}{\exp \left( u\right) -1}du=\frac{1}{1-2^{1-r}}\sum _{n=1}^{+\infty } \frac{(-1)^{n-1}}{n^{r}}\).

See Shimotsu and Phillips (2005) for more details about the consistency of the estimate.

Here, we do not report the results, these are available upon request.

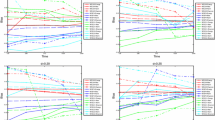

We use two others bandwidths \(m=\left[ T^{0.6}\right] \) and \(m=\left[ T^{0.7} \right] \) for these estimators. We can observe that an estimate of the fractional differencing parameter d with the bandwidth \(m=\left[ T^{0.6} \right] \) and \(m=\left[ T^{0.7}\right] \) provides large bias values than an estimate with bandwidth \(m=\left[ T^{0.8}\right] \), which justifies our choice.

A preliminary analysis of stationarity of the series in level shows evidence of presence of unit roots. So, we consider the series in first difference.

We have fitted a symmetric \(\alpha \)-stable ARMA model to filter the Nord Pool series.

References

Andrews, D., & Guggenberger, P. (2003). A bias-reduced log periodogram regression estimator for the long-memory parameter. Econometrica, 71, 675–712.

Beran, J. (1994). Statistics for long memory processes. New York: Chapman & Hall.

Boubaker, H., & Péguin-Feissolle, A. (2013). Estimating the long-memory parameter in nonstationary processes using wavelets. Computational Economics, 42, 291–306.

Crowley, P. (2007). A guide to wavelets for economists. Journal of Economic Surveys, 21, 207–267.

Daubechies, I. (1992). Ten lectures on wavelets. Philadelphia: SIAM.

Doukhan, P., Oppenheim, G., & Taqqu, M. S. (2003). Theory and applications of long-range dependence. Boston: Birkhauser.

Gençay, M., Selçuk, F., & Whitcher, B. (2002). An introduction to wavelets and other filtering methods in finance and economics. London: Academic Press.

Geweke, J., & Porter-Hudak, S. (1983). The estimation and application of long memory time series models. Journal of Time Series Analysis, 4, 221–238.

Granger, C. W. J., & Joyeux, R. (1980). An introduction to long-memory time series models and fractional differencing. Journal of Time Series Analysis, 1, 15–29.

Hosking, J. (1981). Fractional differencing. Biometrika, 68, 165–176.

Hudgins, D., & Crowley, P. (2018). Stress-testing US macroeconomic policy: A computational approach using stochastic and robust designs in a wavelet-based optimal control framework. Computational Economics,. https://doi.org/10.1007/s10614-018-9820-y.

Hurvich, C., Deo, R., & Brodsky, J. (1998). The mean squared error of Geweke and Porter-Hudak’s estimator of the long memory parameter of a long-memory time series. Journal of Time Series Analysis, 19, 1095–1112.

Jach, A., & Kokoszka, P. (2010). Robust wavelet-domain estimation of the fractional difference parameter in heavy-tailed time series: An empirical study. Methodology and Computing in Applied Probability, 12, 177–197.

Jensen, M. (1999). Using wavelets to obtain a consistent ordinary least squares estimator of the long-memory parameter. Journal of Forecasting, 18, 17–32.

Kokoszka, P. S., & Taqqu, M. S. (1995). Fractional ARIMA with stable innovations. Stochastic Processes and their Applications, 60, 19–47.

Kokoszka, P. S., & Taqqu, M. S. (1996). Parameter estimation for infinite variance fractional ARIMA. The Annals of Statistics, 24, 1880–1913.

Lee, J. (2005). Estimating memory parameter in the us inflation rate. Economics Letters, 87, 207–210.

Mallat, S. (1989). A theory for multiresolution signal decomposition: The wavelet representation. IEEE Transactions on Pattern Analysis and Machine Intelligence, 11, 674–693.

Morris, J. M., & Peravali, R. (1999). Minimum-bandwidth discrete-time wavelets. Signal Processing, 76, 181–193.

McCulloch, J. H. (1986). Simple consistent estimators of stable distribution parameters. Communication in Statistics-Simulation and Computation, 15, 1109–1136.

Meyer, I. (1993). Wavelets: Algorithms and applications. Philadelphia: SIAM.

Mikosch, T., Gadrich, T., Klüppelberg, C., & Adler, R. J. (1995). Parameter estimation for ARMA models with infinite variance innovations. The Annals of Statistics, 23, 305–326.

Mittnik, S., Rachev, S. T., & Paolella, M. S. (1998). Stable paretian modeling in finance: Some empirical and theoretical aspects. In R. Adler, R. Feldman, & M. S. Taqqu (Eds.), A practical guide to heavy tails: Statistical techniques and applications (pp. 79–110). Boston: Birkhäuser.

Nielsen, M. (2000). On the construction and frequency localization of orthogonal quadrature filters. Journal of Approximation Theory, 108, 36–52.

Percival, D. B., & Walden, A. T. (2000). Wavelet methods for time series analysis. Cambridge: Cambridge University Press.

Shimotsu, K., & Phillips, P. (2005). Exact local whittle estimation of fractional integration. Annals of Statistics, 20, 87–127.

Stoev, S., & Taqqu, M. S. (2005). Asymptotic self-similarity and wavelet estimation for long-range dependent FARIMA time series with stable innovations. Journal of Time Series Analysis, 26, 211–249.

Veitch, D., & Abry, P. (1999). A wavelet-based joint estimator of the parameters of long-range dependence. IEEE Transactions on Information Theory, 45, 878–897.

Whittle, P. (1951). Hypothesis testing in time series analysis, New York.

Willinger, W., Taqqu, M. S., & Teverovsky, V. (1999). Stock market prices and long-range dependence. Finance and Stochastics, 3, 1–3.

Acknowledgements

The author expresses his sincere thanks to the editor and the anonymous referee for their helpful comments and valuable suggestion.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Boubaker, H. Wavelet Estimation Performance of Fractional Integrated Processes with Heavy-Tails. Comput Econ 55, 473–498 (2020). https://doi.org/10.1007/s10614-019-09897-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-019-09897-9