Abstract

This study forecasts a particular type of economic uncertainty (inflation uncertainty) in the United States and Euro Area over 1997–2017. By using monthly data, we compute inflation uncertainty based on three models: symmetric and asymmetric generalized autoregressive conditional heteroscedasticity models and a stochastic volatility model. While the first two provide symmetric and asymmetric measures of inflation uncertainty, respectively, the third measure offers greater flexibility when measuring uncertainty. The analysis of the out-of-sample forecasts for inflation uncertainty shows the superiority of the stochastic volatility model for forecasting the dynamics of inflation uncertainty in both the short (1 year) and medium (4 years) terms. This finding is particularly interesting, as it allows researchers to better estimate the main inflation cost, namely inflation uncertainty, as well as its effect on the real economy.

Similar content being viewed by others

Notes

Further, economic uncertainty, which is always unobserved (Charles et al. 2018), has always been challenging to measure and several proxies have been used: the VIX (Bloom et al. 2012), conditional variance models (Scotti 2012; Rossi and Sekhposyan 2017), the economic policy index (Baker et al. 2015), and perceived uncertainty from consumer surveys (Leduc and Sill 2013).

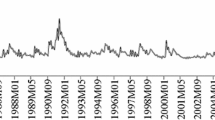

It reached 1.5 and 2.96% in 2010 and 2011, respectively. It then changed to about 1.74% in 2012, 1.5% in 2013, 0.76% in 2014, 0.73% in 2015, and 2.07% in 2016.

It decreased to 1.64 and 0.92% in 2008 and 2009, respectively before reaching 2.23, 2.75, and 2.22% in 2010, 2011, and 2012.

p and q denote the lag order of the autoregressive and moving average parts, respectively. They are specified by using the information criteria and autocorrelation functions.

The lags for a GARCH model might be specified by using information criteria, too. However, a GARCH(1,1) provides a suitable specification with which to capture the main volatility properties.

Other methods of modelling stochastic volatility include Gaussian error models and heavy tails and serial dependence; however, the t-distribution is more appropriate (Chan 2013).

For more details on the MDM statistic, see Harvey et al. (1997).

The GARCH model is estimated by using the quasi-maximum likelihood technique of Bollerslev and Wooldridge (1992).

To save space, we do not report the estimation results of the GARCH and GJR-GARCH specifications, but they are available upon request.

For the medium term forecasting, the period of models estimation is from June 1997 to January 2013 for the case of US and from February 1997 to January 2013. The forecasting period is from February 2013 to January 2017.

For the short-term forecast, the period of the model estimation runs from June 1997 to January 2016 for the United States and from February 1997 to January 2016 for the Euro Area. The forecasting period is therefore from February 2016 to January 2017.

References

Bachmann, R., Elstner, S., & Sims, S. (2013). Uncertainty and economic activity: Evidence from business survey data. American Economic Journal: Macroeconomics, 5, 217–249.

Baker, S. R., Bloom, N., & Davis, S. J. (2015). Measuring economic policy uncertainty. National Bureau of Economic Research Working Paper 21633.

Bårdsen, G., Jansen, E. S., & Nymoen, R. (2002). Model specification and inflation forecast uncertainty. Annales d’Économie et de Statistique, 67(68), 495–517.

Bauer, C., & Neuenkirch, M. (2017). Forecast uncertainty and the Taylor rule. Journal of International Money and Finance, 77, 99–116.

Ben Nasr, A., Balcilar, M., Ajmi, A. N., Aye, G., Gupta, R., & Eyden, R. (2015). Causality between inflation and inflation uncertainty in South Africa: Evidence from a Markov-switching vector autoregressive model. Emerging Markets Review, 24, 46–68.

Berument, H., Yalcin, Y., & Yildirim, J. (2009). The effect of inflation uncertainty on inflation: Stochastic volatility in mean model within a dynamic framework. Economic Modelling, 26(6), 1201–1207.

Bloom, N., Bond, S. R., & Van Reenen, J. (2007). Uncertainty and investment dynamics. Review of Economic Studies, 74(2), 391–415.

Bloom, N., Floetotto, M., Jaimovich, N., Saporta-Eksten, I., & Terry, S.T. (2012). Really uncertain business cycles. National Bureau of Economic Research Working Paper 18245.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31, 307–327.

Bollerslev, T., & Wooldridge, J. (1992). Quasi-maximum likelihood estimation and inference in dynamic models with time-varying covariance. Econometric Review, 11, 143–172.

Chan, J. C. C. (2013). Moving average stochastic volatility models with application to inflation forecast. Journal of Econometrics, 176(2), 162–172.

Chan, J. C. C. (2017). The stochastic volatility in mean model with time-varying parameters: An application to inflation modelling. Journal of Business & Economics Statistics, 35(1), 17–28.

Charles, A., Darné, O., & Tripier, F. (2018). Uncertainty and the macroeconomy: Evidence from a composite uncertainty indicator. Applied Economics, 50(10), 1093–1107.

Diebold, F. X., & Mariano, R. S. (1995). Comparing predictive accuracy. Journal of Business and Economic Statistics, 13, 253–263.

Engle, R. F. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of UK inflation. Econometrica, 50, 987–1008.

Glosten, L., Jagannathan, R., & Runkle, D. (1993). Relationship between the expected value and volatility of the nominal excess returns on stocks. Journal of Finance, 48, 1779–1802.

Golub, J. (1994). Does inflation uncertainty increase with inflation? Economic Review Federal Reserve Bank of Kansas City, 79, 27–38.

Harvey, D. I., Leybourne, S. J., & Newbold, P. (1997). Testing the equality of prediction mean squared errors. International Journal of Forecasting, 13, 281–291.

Holland, S. (1993). Comment on inflation regimes and the sources of inflation uncertainty. Journal of Money Credit and Banking, 25, 514–520.

Jurado, K., Ludvigson, S. C., & Ng, S. (2015). Measuring uncertainty. American Economic Review, 105, 1177–1216.

Koopman, S. J., & Hol Uspensky, E. (2002). The stochastic volatility in mean model: Empirical evidence from international stock markets. Journal of Applied Econometrics, 17(6), 667–689.

Lahiri, K., & Lui, F. (2006). Modelling multi-period inflation uncertainty using a panel of density forecasts. Journal of Applied Econometrics, 21, 1199–1219.

Leduc, S., & Sill, K. (2013). Uncertainty shocks are aggregate demand shocks. Journal of Monetary Economics, 82, 20–35.

Poon, S.-H., & Granger, C. W. J. (2003). Forecasting volatility in financial markets: A review. Journal of Economic Literature, 41(2), 478–539.

Rossi, B., & Sekhposyan, T. (2015). Macroeconomic uncertainty indices based on nowcast and forecast error distributions. American Economic Review, 105(5), 650–655.

Rossi, B., & Sekhposyan, T. (2017). Macroeconomic uncertainty indices for the Euro Area and its individual member countries. Empirical Economics, 53(1), 41–62.

Scotti, C. (2012). Surprise and uncertainty indexes: Real-time aggregation of real-activity macro surprises. Unpublished manuscript, Federal Reserve Board.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Ftiti, Z., Jawadi, F. Forecasting Inflation Uncertainty in the United States and Euro Area. Comput Econ 54, 455–476 (2019). https://doi.org/10.1007/s10614-018-9794-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-018-9794-9