Abstract

This study investigates the association of a broad set of variables with the ethical decision making of management accountants in Libya. Adopting a cross-sectional methodology, a questionnaire including four different ethical scenarios was used to gather data from 229 participants. For each scenario, ethical decision making was examined in terms of the recognition, judgment and intention stages of Rest’s model. A significant relationship was found between ethical recognition and ethical judgment and also between ethical judgment and ethical intention, but ethical recognition did not significantly predict ethical intention—thus providing support for Rest’s model. Organizational variables, age and educational level yielded few significant results. The lack of significance for codes of ethics might reflect their relative lack of development in Libya, in which case Libyan companies should pay attention to their content and how they are supported, especially in the light of the under-development of the accounting profession in Libya. Few significant results were also found for gender, but where they were found, males showed more ethical characteristics than females. This unusual result reinforces the dangers of gender stereotyping in business. Personal moral philosophy and moral intensity dimensions were generally found to be significant predictors of the three stages of ethical decision making studied. One implication of this is to give more attention to ethics in accounting education, making the connections between accounting practice and (in Libya) Islam. Overall, this study not only adds to the available empirical evidence on factors affecting ethical decision making, notably examining three stages of Rest’s model, but also offers rare insights into the ethical views of practising management accountants and provides a benchmark for future studies of ethical decision making in Muslim majority countries and other parts of the developing world.

Similar content being viewed by others

Introduction

Much research has been conducted on ethical issues, moral development and ethical decisions within the general area of business. Some of that research has examined the ethical reasoning, moral development and ethical decision-making processes of accounting students and, to some extent, practising accountants, investigating the variables that might influence their decisions (e.g. Buchan 2005; Etherington and Schulting 1995; Johl et al. 2012; Marques and Azevedo-Pereira 2009; O’Leary and Stewart 2007; Svanberg 2011).

However, management accounting is under-represented in research on accounting ethics in general (Bampton and Cowton 2013) and in research into ethical decision making in particular. Yet management accounting is one of the major subject areas in accounting and has an important role to play in ensuring organizational effectiveness, being ‘concerned with the provision of information to individuals within the organization to help them make better decisions and improve the efficiency and effectiveness of existing operations’ (Drury 2004, p. 4). Management accountants have several important responsibilities within their organizations, including budgeting, forecasting, planning, controlling operations, safeguarding assets, managing financial resources and providing information for management control in general (Woelfel 1986).

The aim of this study is to investigate the association of individual variables, organizational variables and moral intensity dimensions variables with the ethical decision making of management accountants. It thus adds to the very limited research on the ethics of practising management accountants. Moreover, it is unique in focusing on Libyan management accountants and, as such, it provides a basis for further research into ethical decision making in other developing countries, particularly Muslim majority ones. A further notable feature of the study is that it examines three stages of Rest’s decision-making model—which is used to frame the research—whereas most of the many previous studies in business ethics focus on only one or two stages.

The paper is structured as follows. First, literature regarding the ethical decision-making process is reviewed, identifying significant related variables and presenting hypotheses. The research method used is then described, followed by presentation and discussion of results. Finally, the conclusions, limitations and suggestions for future research are given.

Literature Review

Ethical Decision Making Background

Ethical decision making is defined as “a process by which individuals use their moral base to determine whether a certain issue is right or wrong” (Carlson et al. 2002, p. 16). Rest’s (1979, 1986) theoretical framework is probably the most influential in terms of research on the ethical decision-making process within organizations. Rest proposed a four-stage ethical decision-making sequence to describe individuals’ cognitive stages when facing an ethical dilemma: (1) ethical recognition—being able to interpret the situation as being ethical or unethical; (2) ethical judgment—deciding which course of action is ethically right; (3) ethical intention—prioritizing ethical alternatives; and (4) ethical behaviour—engaging in ethically driven behaviour. Rest argues that all four stages are conceptually different and that success in one stage does not mean success in other stages. Wotruba (1990) states that these stages generally occur in the sequence implied, although they can affect each other. Since the early 1980s, most ethical decision-making studies and models within the business area have been heavily based upon Rest’s framework. Business researchers from different countries in areas such as marketing, accounting and management have adopted this framework.

However, most individual studies have focused on only one or two stages of Rest’s framework (e.g. Sweeney and Costello 2009; Weeks et al. 1999; Yetmar and Eastman 2000). According to the comprehensive reviews of O’Fallon and Butterfield (2005) and Craft (2013), taken together, only 18 of more than 250 studies (7 %) have investigated the three stages of ethical decision making focused upon in this study (e.g. Bass et al. 1999; Nguyen and Biderman 2008).

Rest’s basic model has been developed by various authors. For example, Treviño (1986) offered an interactionist ethical decision model, influenced by Kohlberg’s (1969) theory, and includes three parts of Rest’s model of the ethical decision-making process. Treviño’s model describes the ethical decision-making process in three stages from recognizing the ethical issue, through to cognitive processing, and then finally engaging in real action. Both individual and organizational variables are incorporated within this process. Treviño proposes that ethical decision making is the outcome of an interaction between individual and organizational variables regarding the individual’s thinking about ethical dilemmas. Including these variables in an ethical decision making framework is an important development, since it adds an explanatory element to Rest’s framework.

Hunt and Vitell (1986) developed a positive theory of marketing ethics by including moral philosophy. Both deontological and teleological evaluations are used in ethical judgments, followed by intentions to act and finally ethically driven behaviour. Hunt and Vitell (1986) argue that ethical judgment does not always agree with the intention of action, and also ethical behaviour is not always consistent with the ethical intention. Although Hunt and Vitell add a stage of teleological evaluation, in which the consequences of the decision are evaluated, they do not suggest a systematic association between possible consequences and subsequent intentions and behaviour (Jones 1991).

Based on Rest’s (1986) model, Jones (1991) proposed an issue-contingent model of ethical decision making. Jones argues that, although most models of ethical decision making in business ethics research were developed on Rest’s (1986) sequential, four component model, none of these models incorporated the characteristics of the moral issue itself as either an independent variable or a moderating variable (Jones 1991). Jones claims that characteristics of the ethical issue itself are crucial determinants of the decision-making process, and therefore should be included in the model of ethical decision making.

Thus, business ethics decision-making research has been built using theoretical models derived from Rest’s (1986) model of ethical decision making (Groves et al. 2008). Traditionally, one or more stages (recognition, judgment, intention and behaviour) have been treated as the outcome variables, while researchers have investigated individual and organizational variables and moral intensity characteristics as predictor variables (Loe et al. 2000; O’Fallon and Butterfield 2005). As mentioned earlier, most prior research has focused on only one or two stages of ethical decision making(O’Fallon and Butterfield 2005), whereas this study looks at three out of the four stages (ethical recognition, ethical judgment and ethical intention). Only the final stage, ethical behaviour, is omitted, because of its sensitivity and the related difficulties in measuring it (i.e. observing subjects engaged in ethical/unethical behaviour).

This study examines five individual variables (age, gender, work experience, educational level and personal moral philosophy), four organizational variables (type of industry, organizational size, code of ethics and ethical climate) and three dimensions of moral intensity (magnitude of consequences, social consensus and temporal immediacy). The theoretical framework is shown in Fig. 1.

Theoretical framework

There were several reasons for selecting the particular variables shown in Fig. 1 from the range of variables covered in the literature. Firstly, some of these variables—for example age, gender, code of ethics, ethical climate, magnitude of consequences and social consensus—have been studied more than other variables in business ethics research (O’Fallon and Butterfield 2005). This would be sufficient reason for including them in the study, but little research has investigated these variables within developing countries (Al-Khatib et al. 1995; Shafer 2008) such as Libya. Secondly, some variables—such as type of industry, level of education and some dimensions of moral intensity (e.g. temporal immediacy)—have been paid insufficient attention by business ethics researchers across countries (e.g. Craft 2013). The previous literature relating to the included variables is reviewed below.

Individual Variables

A number of individual variables including demographic characteristics, traits of personality and beliefs have been proposed to have a significant relationship with ethical decision-making stages (e.g. Haines and Leonard 2007; Marta et al. 2008; Shafer 2008; Vitell and Patwardhan 2008). For some of the variables, the empirical results look mixed, but on closer examination it is found that any significant results are all, or mostly, in a particular direction. One of the possible reasons for other studies finding no significant relationship is limited sample size, but this cannot be determined conclusively in the case of any particular study.

Gender

The possible influence of gender on ethical decision making has been studied more than any other variable in business ethics research (O’Fallon and Butterfield 2005). Differences associated with gender have been theoretically explained in various ways. Socialization theory (Gilligan 1982) hypothesizes that men and women bring different sets of values to the workplace because of early socialization. Women, accordingly, tend to evaluate ethical issues in terms of their caring view of others, understanding relationships and responsibility to the entire community; whereas men tend to recognize ethical issues from a perspective of rules, fairness, rights and justice. In their meta-analysis, Jaffee and Hyde (2000) find support for this theory. On the other hand, structural theory suggests that the occupational environment and the rewards and costs structure within the workplace will overcome the impact of gender differences caused by early socialization (Betz et al. 1989). Thus, women and men will respond equally to ethical issues in the workplace (Reidenbach et al. 1991). In their reviews, Ford and Richardson (1994), Loe et al. (2000), O’Fallon and Butterfield (2005) and Craft (2013)Footnote 1 report more than one hundred results and conclude that gender often tends to produce no significant results, but when differences are found, women are more sensitive to ethical issues than men (e.g. Fang and Foucart 2013; Ferrell and Skinner 1988; Fleischman and Valentine 2003; Galbraith and Stephenson 1993; Oumlil and Balloun 2009). More recent research (e.g. Kuntz et al. 2013; Walker et al. 2012) has shown similar varied results. Given that the results tend to show either no difference or that females are more ethical than males, this study hypothesizes:

H1a

Females have significantly higher ethical recognition, judgment and intention.

Age

Kohlberg’s theory of moral development suggests a positive impact of age on moral development as individuals generally move from lower to higher stages of moral reasoning as they grow older (Borkowski and Ugras 1998). However, research shows inconsistent and mixed results (Craft 2013; O’Fallon and Butterfield 2005). Some studies (e.g. Bateman and Valentine 2010; Brady and Wheeler 1996; McMahon and Harvey 2007; Walker et al. 2012) indicate that age is positively and significantly correlated with ethical decision making, while others find no significant relationship (e.g. Kuntz et al. 2013; Marta et al. 2004; Pierce and Sweeney 2010). However, it is not generally suggested that ethical decision making is negatively correlated with age. Thus, this study hypothesizes:

H1b

Age is positively related to ethical recognition, judgment and intention.

Educational Level

Based on the argument that the length of formal education is an important influence on an individual’s moral development (Kohlberg 1981), many researchers suggest that educational level has a positive impact on the ethical decision-making process (e.g. Browning and Zabriskie 1983; Kracher et al. 2002; Pierce and Sweeney 2010). However, some researchers (e.g. Dubinsky and Ingram 1984; Marques and Azevedo-Pereira 2009) have not found a significant relationship between the two. Again, though, it is not generally suggested that increased educational level is negatively associated with ethical decision making. Thus, this study hypothesizes:

H1c

Level of education is positively related to ethical recognition, judgment and intention.

Work Experience

When considering the effect of work experience on the ethical decision-making process, Kohlberg’s (1969) theory provides a framework which could suggest a relationship between work experience and moral development (Treviño 1986). Glover et al. (2002) argue that greater experience may be associated with greater awareness of what is ethically acceptable. Dawson (1997) also proposes that ethical standards change with years of experience. Ford and Richardson (1994) and Loe et al. (2000) conclude that empirical research continues to present mixed results. Nevertheless, recent studies (e.g. Fang and Foucart 2013; O’Leary and Stewart 2007; Pierce and Sweeney 2010; Valentine and Bateman 2011) generally indicate a positive relationship between work experience and ethical decision making, consistent with Kohlberg’s (1969) theory and Treviño’s (1986) argument. Thus, this study hypothesizes:

H1d

Work experience is positively related to ethical recognition, judgment and intention.

Moral Philosophy

Personal moral philosophy is another individual variable that has been extensively studied. Business ethics researchers agree that individuals within organizations will respond based on their own moral philosophies when encountering situations having an ethical content (Shultz and Brender-Ilan 2004; Singhapakdi et al. 2000). For example, Hunt and Vitell (1986) stress the importance of moral philosophies—deontology and teleology—in their model of ethical decision making.

The most common model of personal moral philosophy that has been examined in the business ethics literature (e.g. Marta et al. 2008) is Schlenker and Forsyth’s (1977) two-dimensional model consisting of idealism and relativism. Forsyth (1980, p. 175) posits that these dimensions are distinct; while moral idealism refers to “the degree to which an individual focuses upon the inherent rightness or wrongness of actions regardless of the results of those actions”, moral relativism refers to “the extent to which individuals reject universal moral rules or standards”. In making ethical decisions, moral idealists use idealistic rather than practical criteria; those who have high idealism believe that desirable results can be attained, and harming others is universally and always bad and should be avoided (Swaidan et al. 2004). Relativists, on the other hand, assume that moral rules are relative to the society and culture in which they occur (Schlenker and Forsyth 1977). Thus, moral relativists do not accept universal moral rules and codes in making ethical decisions.

Forsyth (1980, 1992 developed an instrument, the Ethics Position Questionnaire (EPQ), to measure these two dimensions of personal moral philosophy. Using the EPQ, empirical research, in general, has produced consistent results suggesting that moral idealism has a significant positive relationship with ethical decision making, and moral relativism has a significant negative relationship with ethical decision making (Craft 2013; O’Fallon and Butterfield 2005). Based on the above, this study hypothesizes:

H1e

Idealism is positively related to ethical recognition, judgment and intention.

H1f

Relativism is negatively related to ethical recognition, judgment and intention.

Organizational Variables

Organizational variables are defined as “characteristics of the decision setting (versus characteristics of the decision maker or the decision) that should influence the decision-making process and outcomes” (Ross and Robertson 2003, p. 214). These variables include, for example, codes of ethics, ethical climate, organizational size, top management, organizational structure and organization culture. Treviño’s (1986) model proposes that organizational variables often influence an individual’s ethical decisions.

Code of Ethics

Codes of ethics have been widely researched in the business ethics literature because of their potentially significant relationship with ethical decisions (Loe et al. 2000; O’Fallon and Butterfield 2005). Stevens (1994, p. 64) defines codes of ethics as “written documents through which corporations hope to shape employee behaviour and produce change by making explicit statements as to desired behaviour”. Thus, a code of ethics in an organization can provide important guidance for the behaviour of employees (Pater & Anita, 2003; Schwartz, 2002).

It is argued that a code of ethics might not be sufficient by itself to ensure that the individuals within organizations make ethical decisions (Webley and Werner 2008). For example, successfully communicating a code of ethics to all members and enforcing it could also be necessary for a code of ethics to work (Chia-Mei and Chin-Yuan 2006; Cleek and Leonard 1998). Nevertheless, research has generally suggested that the presence of a code of ethics is positively related to ethical decision making (Loe et al. 2000; O’Fallon and Butterfield 2005; e.g. Kaptein 2011; McKinney et al. 2010; Pflugrath et al. 2007). Thus, the following hypothesis is formulated:

H2a

The presence of a code of ethics is positively related to ethical recognition, judgment and intention.

Ethical Climate

Ethical climate is another important organizational variable that has been found to have some significant influence on employees’ ethical decisions (Ortas et al. 2013). Victor and Cullen (1988, p. 101) define it as “the prevailing perceptions of typical organizational practices and procedures that have ethical content”. They argue that the ethical climate at the workplace will be a crucial source for employees’ information relating to the “right” or ethical behaviours within organizations. Based on theories from moral philosophy (e.g. Williams 1985) and moral psychology (Kohlberg 1981), Victor and Cullen (1988) theorize that ethical climate within organizations differs along the three categories of ethical theory (egoism, benevolence and principle) and the three loci of analysis (individual, local and cosmopolitan). Nine types of ethical climate result (see Table 1). It is by far the most completely developed framework and has been used by several researchers (Miao-Ling 2006).

Victor and Cullen (1987, 1988) suggest that climates characterized by self-interest (egoistic/individual) and firm interest (egoistic/local) are more likely to be correlated with questionable or unethical behaviour. In contrast, climates that emphasize following law and professional codes (principle/cosmopolitan) and social responsibility or serving the public interest (benevolent/cosmopolitan) should be associated with more ethical decisions. In their surveys, Loe et al. (2000) and O’Fallon and Butterfield (2005) review thirty-four studies and conclude that there is increasing evidence that ethical climates’ dimensions have a significant relationship with individuals’ decisions. More recently, some studies (Beeri et al. 2013; Elango et al. 2010; Lu and Lin 2013) indicate a significant impact of ethical climate on ethical decision stages, while some others (e.g. Buchan 2005; Shafer 2008) provide no significant results. Thus, this study hypothesizes:

H2b

Ethical climate types are significantly related to ethical recognition, judgment and intention.

Treviño et al. (1998) argue that a reduced number of ethical climate dimensions could be used to describe the principal characteristics of an organization’s ethical context. In the present study, four out of the nine types of ethical climate are investigated (organization interest, social responsibility, personal morality, and law and professional code). These types have been the most investigated in previous studies. Social responsibility and personal morality may be found within countries, like Libya, where religion and cultural dimensions are expected to play a significant role in individuals’ ethical decisions (e.g. Singhapakdi et al. 2001). Law and professional code and organization interest have been investigated in several studies, especially in developed countries (e.g. DeConinck 2004; Parboteeah and Kapp 2008; Wimbush et al. 1997), but only a few studies have investigated these types of ethical climate in developing countries (Shafer 2008, 2009).

Organizational Size

Organizational size is another characteristic that can have an impact on employees’ ethical decision making and is also a typical control variable in organizational research. Differences in work environment between large and small organizations exist (Appelbaum et al. 2005). It is argued that large organizations might have business advantages that small organizations might not; therefore, small organizations might be under pressure to make an unethical decision to compete with larger organizations (Clarke et al. 1996; Vitell and Festervand 1987). In contrast, Ford and Richardson (1994) conclude that there is a significant negative relationship between organizational size and individuals’ ethical decision making such that, when the size of an organization increases, individuals’ ethical behaviour decreases. However, more recent research has revealed a positive significant relationship between organizational size and ethical decisions or no significant relationship (Doyle et al. 2014; Marta et al. 2008; Pierce and Sweeney 2010; Sweeney et al. 2010). Given the thrust of the more recent empirical research, this study hypothesizes:

H2c

Organizational size is positively related to ethical recognition, judgment and intention.

Industry Type

Industry type has sometimes been found to have an impact on individual ethical decisions (e.g. Ergeneli and Arıkan 2002; Forte 2004; Roozen et al. 2001; e.g. Shafer et al. 2001) and, again, is a typical control variable in organizational research. For example, individuals who work at a place where potentially dangerous products are produced may be more sensitive to recognizing ethical issues than individuals who work for companies producing relatively safe products. Thus, this study hypothesizes:

H2d

Ethical recognition, judgment and intention will be different based on industry type.

Moral Intensity

Jones (1991) noted that various ethical decision-making models (e.g. Ferrell and Gresham 1985; Rest 1986; Treviño 1986) included several individual and organizational variables, but none incorporated the characteristics of ethical issue itself. However, for example, the issue of misusing equipment in an organization is not as severe as releasing a dangerous product into the market (McMahon and Harvey 2007). Jones used Rest’s (1986) ethical decision-making model to build his new construct, which he labelled ‘moral intensity’. According to Jones (1991, p. 372), moral intensity is “a construct that captures the extent of issue-related moral imperative in a situation”. It consists of six components: the magnitude of consequences of an unethical act (the sum of the harm or benefit to victims or beneficiaries in a moral act), social consensus (the degree of social acceptance that a given act is good or evil), probability of effect (the probability that a given act might actually take place and the probability of its potential for harm or good), temporal immediacy (the length of time between the present and the onset of consequences of the moral act in question), proximity (feeling of nearness that the moral agent has for victims) and concentration of effect (an inverse function of the number of people affected by an act of given magnitude).

Since the late 1990s, moral intensity has been given more attention by researchers. Loe et al. (2000), O’Fallon and Butterfield (2005) and Craft (2013) report fifty-six studies related to the impact of moral intensity dimensions on ethical decision making. Most of these studies (e.g. Karacaer et al. 2009; May and Pauli 2002; McMahon and Harvey 2007; Singhapakdi et al. 1996; Sweeney and Costello 2009) reveal a positive significant relationship with the ethical decision-making process. These results are supported by recent research (e.g. Valentine and Bateman 2011; Valentine and Hollingworth 2012). Although some studies (e.g. Barnett and Valentine 2004; Davis et al. 1998; May and Pauli 2002; Svanberg 2011) show no significant relationship, research in general shows a significant and positive relationship between moral intensity dimensions and ethical decision-making stages.

In practice, researchers have examined a limited range of moral intensity dimensions (Craft 2013). The role of magnitude of consequences and social consensus in ethical decisions has been investigated in different areas such as marketing, management and accounting, revealing more consistent results than the other moral intensity dimensions (O’Fallon and Butterfield 2005). Furthermore, there has been limited research concerning the relationship between temporal immediacy and ethical decision making (O’Fallon and Butterfield 2005), where temporal immediacy is positively related to moral intensity.

Based on the above, this study hypothesizes:

H3a

Magnitude of consequences is positively related to ethical recognition, judgment and intention.

H3b

Social consensus is positively related to ethical recognition, judgment and intention.

H3c

Temporal immediacy is positively related to ethical recognition, judgment and intention.

Method

A cross-sectional research design was employed to collect data from Libyan management accountants. Participants were assured that their participation would be voluntary and all responses kept confidential. Since all participants were Arabic native speakers, the questionnaire was translated into Arabic by one of the researchers, who is an Arabic native speaker, and checked by three Arabic academics with more than 20 years of work experience in teaching English language courses. Arabic questionnaires were piloted to fifteen Libyan PhD students studying at four British universities.

The questionnaire included four pre-tested scenarios. The four scenarios were originally developed and produced in a videotape by the Institute of Management Accountants (IMA) in the USA and adapted by Flory et al. (1992). They have been used in accounting studies (e.g. Leitsch 2004, 2006; Sweeney and Costello 2009; Yang and Wu 2009) to examine ethical decision-making stages and moral intensity dimensions. They were considered to illustrate practical accounting issues familiar to Libyan management accountants—a key feature of scenarios (Randall and Gibson 1990; Weber 1992)—but were adjusted to render them more natural for the Libyan context. For example, Arabic names were used, and the circumstances of the decision maker in scenario 4 (college fees) were replaced with different, but structurally similar, circumstances (hospital fees). The four scenarios included approving a questionable expense report (scenario 1), manipulating company books (scenario 2), by-passing company policy (scenario 3) and extending questionable credit (scenario 4). They are reproduced in the Appendix. The ethical violations presented in scenarios 2 and 3 were considered more severe (Flory et al. 1992).

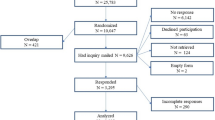

Because of the shortcomings of the postal service and the limited penetration of the internet in Libya, 71 Libyan manufacturing companies were visited to distribute the questionnaires. Based on a list provided by the financial/management accounting manager in each company, the questionnaire was administered to 392 Libyan management accountants working within Libyan companies. A total of 229 (58.40 %) completed questionnaires were collected from the companies. In their review, Randall and Gibson (1990) found that response rates ranged commonly from 21 to 50 % in business ethics literature. Bampton and Cowton (2013) found similar results in accounting ethics research. Thus, the response rate of this study was felt to be more than satisfactory. The issue of non-response bias was considered; using an independent samples t test each time, the mean scores of the three dependent variables (ethical recognition, judgment and intention) of late and early respondents were compared. No significant differences between the two groups were found (p < 0.05). The possibility of social desirability response bias was addressed by asking for the questionnaire to be returned in a sealed envelope and using scenarios rather than asking about the respondent’s own experience and behaviour.

From Table 2, it can be seen that nearly half of the respondents (45 %) are more than 40 years old and 75 % are male. Just over a third of the participants (37 %) have work experience between 5 and 15 years and 58 % have a Bachelor’s degree. Almost two-thirds of the participants (65 %) work in companies that are owned by the state. Further, large numbers of participants (28 and 31 %) work for Food companies and Oil, Gas and Chemicals companies, respectively, while a minority of participants (4 %) work for Textiles and Furniture companies. Finally, more than 62 % of the participants reported that their companies have no code of ethics.

Measures

With regard to ethical decision-making stages and moral intensity dimensions, participants were asked to indicate their agreement on a 5-point rating scale (from (1) ‘strongly disagree’ to (5) ‘strongly agree’). As in the case of much previous research (Leitsch 2006; May and Pauli 2002; McMahon and Harvey 2006; O’Leary and Stewart 2007; Sweeney and Costello 2009; Valentine and Hollingworth 2012; Valentine et al. 2013; Yang and Wu 2009), single-item scales were used to measure the three stages of ethical decision making and the moral intensity dimensions. Ethical recognition was measured by asking participants whether the situation in each scenario included an ethical issue, “the situation above involves an ethical problem” (Singhapakdi et al. 1996). Ethical judgment was measured by asking participants whether they agreed with the decision maker’s decision in each scenario, “[The decision maker] should not do the proposed action” (May and Pauli 2002). Ethical intention was measured by asking participants whether they agreed or not with the action the decision maker made, “If I were [the decision maker], I would make the same decision” (reverse-coded) (Singhapakdi et al. 1996).

Regarding moral intensity dimensions, magnitude of consequences was assessed by “The overall harm (if any) as a result of the action would be very small” (reverse-coded). Social consensus was measured by “Most people would agree that the action is wrong”. Temporal immediacy was measured by “the decision maker’s action will not cause any harm in the immediate future” (reverse-coded).

Personal moral philosophy was measured by adopting the well-established Ethics Position Questionnaire (EPQ) constructed by Forsyth (1980). It has been successfully used and validated by several ethics studies (e.g. Chan and Leung 2006; Dubinsky et al. 2004; Marques and Azevedo-Pereira 2009; Shafer 2008; Singhapakdi and Vitell 1993). The EPQ consists of two scales, each containing 10 items provided with a scale of agreement based on a 5-point rating (from (1) ‘strongly disagree’ to (5) ‘strongly agree’) to measure personal moral philosophy (idealism and relativism). The internal reliability result for this instrument (idealism α = 0.74 and relativism α = 0.79) showed an acceptable level of Cronbach’s alpha for each dimension (Nunnally 1978).

The Ethical Climate Questionnaire (ECQ) developed by Victor and Cullen (1987, 1988) was adopted to measure the ethical climate in Libyan companies. It has been used and validated in a number of prior studies (e.g. Cullen and Victor 1993; DeConinck and Lewis 1997; Fritzsche 2000; Lu and Lin 2013; Malloy and Agarwal 2001; Shafer 2008). The scale of agreement is based on a 6-point rating (from (5) ‘completely true’ to (0) ‘completely false’). Four of the nine ethical climate types were examined in this study: organization interest, social responsibility, personal morality and law and professional code. In their meta-analysis, Martin and Cullen (2006) concluded that in most organizations studied, not all distinct climate types existed. Treviño et al. (1998) argue that evidence shows that a reduced number of the dimensions of ethical climate could be used to explain some characteristics of the moral situation within organizations. These types have been most investigated in previous studies, and therefore are expected to be found within Libyan companies. For example, social responsibility and personal morality may be found within countries where religion and cultural dimensions (power distance, uncertainty avoidance, and collectivism) play a significant role in individuals’ ethical decisions. The internal reliability result of this instrument showed an acceptable level of Cronbach’s alpha for each climate type: organization interest α = 0.72, social responsibility α = 0.74, personal morality α = 0.65 and law and professional code α = 0.79 (Nunnally 1978). Several business ethics studies obtained similar levels of reliability for the four types of ethical climate investigated (e.g. Agarwal and Malloy 1999; Shafer 2008, 2009; Upchurch 1998; VanSandt et al. 2006; Vardi 2001; Venezia and Callano 2008).

For measuring categorical variables, participants were asked to provide information about their gender, age, years of experience, educational level, type of industry, their company’s size and whether their companies have a code of ethics or any kind of ethical guidelines.

Data Analysis

Data were entered into SPSS (version 20). Categorical variables of gender, age, educational level, work experience, organizational size, type of industry and code of ethics were analysed using independent samples t tests and one-way independent samples ANOVA tests. Continuous variables of personal moral philosophy, ethical climate types, moral intensity dimensions and ethical recognition and judgment were analysed using hierarchical multiple regression.

The sequence of variable entry into the regression hierarchy reflected the theoretical model—both the stages of Rest’s model and the logic of the various factors (e.g. individual factors are essentially “prior” to the others). When ethical recognition was the criterion variable, the order of predictor variable entry into the regression was individual variables followed by organizational variables and then moral intensity dimensions in the final model. When ethical judgment was the criterion, ethical recognition was entered first, followed by the above order for other variables. Similarly, ethical recognition and ethical judgment were entered first when ethical intention was the criterion. Several previous studies (e.g. Bateman et al. 2013; Marques and Azevedo-Pereira 2009; Sweeney et al. 2010; Sweeney and Costello 2009; Valentine and Bateman 2011; Yang and Wu 2009) have also chosen this order of variable entry.

The data were checked for outlying and influential values but no responses needed removing. Scatterplots of standardized predicted values versus standardized residuals were used to assess assumptions of normality, linearity and homoscedasticity (Tabachnick and Fidell 2007). Only 13 % of the scatterplots showed assumption violations, and regression is reasonably robust to minor violations (Howell 2006). The variance inflation factor showed no multicollinearity, and the Durbin-Watson test showed that errors were independent. The sample size was adequate with at least 15 cases per predictor (Field 2009; Vitell and Patwardhan 2008).

Results

Analysis of Categorical Variables

Means, standard deviations and results for one-way independent groups ANOVA and t tests are shown in Tables 3 and 4. Means indicate that, on average, Libyan management accountants recognized the ethical issue presented in each scenario, judged it as unethical and had limited intention to behave unethically across individual variables, organizational variables and moral intensity dimensions (mean scores were 3 or above). With respect to gender, only two significant results were found in relation to the ethical recognition stage. Moreover, the results were in the opposite direction to that predicted; males displayed significantly higher ethical recognition. Thus, H1a was rejected. Also, there were only two significant differences in ethical recognition based on age and one for work experience and two significant differences in ethical intention based on education level. Thus, H1b, H1c and H1d were rejected.

With regard to categorical organizational variables, similar results were found: two significant differences for organizational size (one in ethical judgment and one in ethical intention) and no significant differences based on code of ethics and type of industry. Accordingly, H2a, H2b and H2c were rejected.Footnote 2

Multiple Regression Analysis of Continuous Variables

Ethical Recognition

Model 1, as shown in Table 5, indicates that personal moral philosophy (idealism and relativism) accounts for 7 to 9 % of the variation in ethical recognition of management accountants in the first three scenarios (p < 0.001). When the types of ethical climate were added (model 2), these proportions increased, ranging from 10 to 12 %, also in the first three scenarios (p < 0.001). However, these increases (∆R 2) were only significant in scenario three (p < 0.05). Finally, by adding moral intensity dimensions to the model (model 3), the proportions again were improved; they explained 14–32 % of the variation in ethical recognition of management accountants. The model was now significant for all scenarios (p < 0.001). With the exception of scenario 1, all increases (∆R 2) were statistically significant (p < 0.001).

The β-values depicted in Table 5 (model 3) indicate that moral idealism had a positive significant relationship with ethical recognition in scenarios 1, 2 and 3. Moral relativism showed a negative significant relationship with ethical recognition in scenario 1 and 3. Thus, hypotheses H1e and H1f were supported with respect to the ethical recognition stage.

There were only a few significant results related to ethical climate types; law and professional codes had only one positive significant relationship in scenario 3 and the same for social responsibility in scenario 1. Finally, there was a significant negative relationship between personal morality and ethical recognition in scenario 1. Therefore, there was limited support for H2b with respect to the ethical recognition stage.

Regarding moral intensity dimensions, a significant positive relationship was found between magnitude of consequences and ethical recognition in scenarios 2 and 3, and similarly for social consensus in scenarios 3 and 4. Temporal immediacy was positively and significantly related to ethical recognition in the four scenarios. Thus, hypotheses H3a, H3b and H3c were supported with respect to the ethical recognition stage.

Ethical Judgment

Table 6 indicates that ethical recognition explained 11–33 % of the variation in ethical judgment, and the model was significant in the four scenarios (p < 0.001). By adding personal moral philosophy components (model 2) and ethical climate types (model 3), these proportions were enhanced ranging from 17 to 36 %, and the models were again significant. Including moral intensity dimensions (model 4) led to a statistically significant improvement in all scenarios (p < 0.001), accounting for 20 to 51 % of the variation in ethical judgment.

The β-values in Table 6 (model 4) indicate that moral idealism had a positive significant relationship with ethical judgment in scenarios 1 and 2. In contrast, moral relativism was not significantly related to ethical judgment in any scenario, and hence there was limited support for H1e and H1f with regard to ethical judgment. With respect to ethical climate types, β-values showed very limited significant relationships. Thus, H2b was rejected with respect to ethical judgment. For moral intensity dimensions, the β-values of magnitude of consequences showed a positive significant relationship in scenario 4 and similarly for temporal immediacy in scenario 1. Social consensus had a positive significant relationship with ethical judgment in scenarios 3 and 4. Thus, these findings provide some statistical support for H3b and limited support for H3a and H3c with regard to ethical judgment. Finally, ethical recognition was a positive significant predictor of ethical judgment in all four scenarios.

Ethical Intention

Table 7 shows that ethical recognition and ethical judgment (model 2) explained 10 to 33 % of the variation in ethical intention in all scenarios (p < 0.001). When adding personal moral philosophy (model 3), the proportions were improved and explained 14–37 % of the variation in ethical intention in the four scenarios (p < 0.001). Including ethical climate types showed no significant improvement in the model. Finally, adding the dimensions of moral intensity enhanced the model (model 5), accounting for 31–48 % of the variation in ethical intention. These increases (∆R 2) were statistically significant in all scenarios.

The β-values shown in Table 7 (model 5) indicate that moral idealism had a positive significant relationship with ethical intention but only for scenario 1. However, more significant and negative relationships were found regarding the impact of moral relativism on ethical intention. Thus, H1e and H1f were supported with respect to the ethical intention stage. No significant result was found related to the relationship between ethical climate types and ethical intention. Thus, H2b was rejected with regard to the ethical intention stage. The β-values of moral intensity dimensions indicate that magnitude of consequences is positively and significantly related to ethical intention in the four scenarios. However, β-values of social consensus and temporal immediacy revealed limited significant results related to ethical intention. Hence, these results provide a full support for H3a and limited support for H3b and H3c with regard to ethical intention. Finally, while ethical recognition was not a significant predictor of ethical intention, ethical judgment had a positive significant relationship with ethical intention in three of the four scenarios.

Discussion

In this section, the results of this study in terms of the associations between individual variables, organizational variables and moral intensity and the three stages of ethical decision making are discussed.

Individual Variables

In terms of personal moral philosophy, the results indicate that moral idealism was the individual variable that was generally the strongest predictor of the three stages of ethical decision making for management accountants. Moral relativism was sometimes found to be negatively related (but generally less strongly than moral idealism) to the decision. These results are consistent with previous research (e.g. Dubinsky et al. 2004; Sparks and Hunt 1998; Yetmar and Eastman 2000). In their review of the ethical decision-making literature, O’Fallon and Butterfield (2005) come to the conclusion that idealism and relativism revealed fairly consistent results over the last few decades of ethical research. They conclude that idealism is positively related to ethical decision making, while relativism is negatively associated with ethical decision making. Sparks and Hunt (1998, p. 105) suggest two factors to explain the negative relationship between moral relativism and the ethical decision-making stages, ethical recognition in particular: “First, the disbelief in moral absolutes might reduce the likelihood of ethical violations standing out among other issues. In a world where all issues are relativistic shades of grey, ethical issues might blend in with everything else. Second, relativists might consider ethical issues in general to be less important than nonrelativists”.

These findings suggest that Libyan management accountants tend to be idealistic rather than relativistic when making ethical decisions. This indicates that their actions may be influenced more by universal moral rules, which produce positive consequences for all those involved (i.e. absolutists) (Forsyth 1992). Several studies conducted in Muslim countries including Egypt (Attia et al. 1999; Marta et al. 2003), Jordan and Saudi Arabia (Marta et al. 2004), UAE (Al-Khatib et al. 2005), Morocco (Oumlil and Balloun 2009) and Indonesia (Lu and Lu 2010) have shown similar results, i.e. that Muslims are more idealistic and less relativistic. The Islamic tradition places ethical/social activity ahead of individual profit maximization (Beekun et al. 2008; Rice 1999), and Islam urges strict adherence to the ethical injunctions of the Quran. In Libya, Islam is the major source of the written laws and most of the legal environment surrounding business transactions (Kilani 1988). Therefore, strict adherence to the tradition of Islamic faith in Libya would strengthen deontological norms and moral rules in individuals’ ethical systems. The influence of Islam could be one possible explanation for the finding that idealism had a positive relationship with ethical decision making. When this finding is compared with similar results from non-Muslim countries (Al-Khatib et al. 1997; Van Kenhove et al. 2001), this explanation might be questioned, but the present results imply that one approach to enhancing the ethical decision-making process within the Libyan business environment would be to encourage idealistic philosophy and, during the education process for accountants, to help make them aware of the connections between accounting practice and Islam.

In relation to demographic variables, there were few significant differences in the ethical recognition, judgment and intention of management accountants based on their age, gender and level of education. Several researchers investigating the relationship between age and ethical decision-making stages have reported similar results (e.g. Barnett and Valentine 2004; Callan 1992; Marta et al. 2004; McMahon and Harvey 2007). The lack of significant findings for educational level also does not conflict with several studies (e.g. Chan and Leung 2006; Sparks and Hunt 1998). Limited moral development once in work might be one reason for the lack of difference based on age and education level. Moral development literature indicates that without intervention or an appropriate environment, the majority of adult people will never exceed the conventional level suggested by Kohlberg’s model (Steven et al. 2006). Also, past research has demonstrated that accountants tend to be at Stage 4 of moral development or lower (Green and Weber 1997). Another reason might be that Libyan accounting education failed to prepare Libyan accountants to deal with such issues. Although researchers have repeatedly reported that moral development is associated with level of education (Armstrong et al. 2003; Steven et al. 2006), this presumably depends on the nature of the education. If there are ethical failures in accounting practice, it is probable that at least some of the blame can be placed on the education system (Gray et al. 1994).

The present results may suggest that integrating courses of ethics, perhaps with an Islamic emphasis, in accounting education and paying more attention to ethical training of management accountants could enhance the process of ethical decision making of Libyan accountants. However, this issue may not have been considered yet by the Libyan higher education sector. For example, the Centre for Quality Assurance and Accreditation for Higher Education Institutions in Libya did not include any type of ethical material in its suggested curricula for Libyan universities (Centre for Quality Assurance and Accreditation for Higher Education Institutions 2008). Moreover, the limited professional organization of accountants within Libyan companies means that the training would have to be arranged by the companies themselves rather than being part of continuing professional development instituted by a professional association (cf. Cowton 2009).

Regarding the differences in ethical decision making based on gender, female management accountants were significantly less sensitive than their male counterparts in recognizing the ethical issues in two of the four scenarios—though no significant differences were found in ethical judgment and ethical intention based on gender. These limited significant results, especially for ethical recognition, are only consistent with the study of Marques and Azevedo-Pereira (2009), who found that male chartered accountants were significantly more ethical than female chartered accountants in two out of five scenarios. It is possible that ethical gender differences here may be attributed to other reasons such as age or years of experience (Dawson 1997). The female accountants who participated in this study are generally younger than their male counterparts (56 % of females, but only 27 % of males, had ages less than 35 years) and generally have less work experience (76 % of females but only 48 % of males have less than 15 years’ work experience). The younger and less-experienced females may be less sensitive to ethical issues. However, given the paucity of significant differences in gender, age and work experience in general, this suggestion should be treated cautiously. Future research is needed to see whether any gender differences are based on these variables. With respect to work experience itself, there was only one significant result. Previous studies have reported similar findings (e.g. Nill and Schibrowsky 2005; Roozen et al. 2001). O’Leary and Stewart (2007) found little evidence of the possible impact of work experience but argued that the direction of the relationship is still ambiguous. In their review, O’Fallon and Butterfield (2005) conclude that the relationship between work experience and ethical decision making was inconsistent.

Organizational Variables

There were no significant differences in ethical decision making based on code of ethics and industry type and only two significant differences for organizational size. Knowledge of the existence of a code is a necessary prerequisite for its effectiveness, but the results here suggest that those management accountants who perceive that their company has a code are not significantly different from those who do not (whether the company has a code or not). This might be a particular concern in Libya and other developing countries that have not yet made much progress in developing an accounting profession with a strong code of ethics.

Several researchers (Cooper and Frank 1997; Laczniak and Inderrieden 1987; Verschoor 2002) have argued that a corporate code of ethics by itself may not be sufficient to significantly influence the ethical decision-making process. There are many possible reasons for this result. One is that the content of the code is limited or, in this case, is not particularly relevant to the work of the management accountants. Laczniak and Inderrieden (1987) claim that a code of ethics may be associated with the process of ethical decision making only when combined with sanctions. Rottig and Heischmidt (2007) suggest that a code of ethics should be systematically and empirically examined in conjunction with additional determinants of ethical decision making such as ethical training. The results of this study suggest that managers of Libyan companies should check that the content of their code of ethics is up to date and relevant, communicated to staff and supported appropriately. Future research within a Libyan context could focus exclusively on codes of ethics, and hence investigate more fully their content and organizational factors such as rewards, sanctions, communication and training to see if these things influence the relationship between having a code of ethics and making ethical decisions.

An alternative explanation for this result may be related to other factors such as ownership and type of market (planned market such as in Libya). Agarwal and Malloy (1999) report that, in state-owned organizations, organizational variables are not a significant determinant of ethical decisions. They propose that the organization might not have sufficient impact on its members. As noted in Table 2, the majority of management accountants (65 %) work within companies that are owned by the state and 18 % are joint venture between the state and other parties. This could be a possible reason for the lack of significant findings. Traditionally, different organizations in the public sector may be quite similar in terms of their culture regardless of their types (banks, manufacturers, non-profit organizations, etc.). This may be because they are resourced by similar state means. If these companies were to operate in a free market where their features are different from those that operate in a non-free market, then code of ethics, size and type of industry might have an influence on the ethical decision-making process. Most past research has shown that these variables have a significant positive relationship with ethical decision-making stages within organizations that operate in a free market (e.g. Barnett et al. 1993; Pflugrath et al. 2007; Weeks and Nantel 1992).

With regard to the nine ethical climate types suggested by Victor and Cullen (1987, 1988), past research has found a significant relationship with the ethical decision-making process. However, some have argued that these types do not always exist within organizations (Martin and Cullen 2006). In the present study, four types of ethical climate were examined, and limited significant results were found. Only personal morality was found to have a significant relationship with the ethical decision-making stages in only one scenario and law and professional codes only had one significant relationship with ethical recognition and one with ethical judgment, each in a different scenario. Empirical research has shown similar results, with ethical climate having limited or no significant relationship with ethical decision-making stages (e.g. Buchan 2005; DeConinck and Lewis 1997; Shafer 2008). Briefly, the environment surrounding Libyan companies (i.e. public sector) or the other types of ethical climate may be better predictors of ethical decision-making scores.

Moral Intensity Dimensions

All the issues included in the given scenarios were clear and represent unethical actions, of varying degrees, which could be commonly found in the work setting (Leitsch 2006; Sweeney and Costello 2009). Jones (1991) claims that clear differences of ethical intensity between scenarios are essential in ascertaining moral intensity’s influence. In general, at least some moral intensity dimensions significantly predicted the ethical decision making of Libyan management accountants in this study. This result supports Jones’ (1991) issue-contingent model of ethical decision making and is consistent with several empirical studies (Barnett 2001; Flory et al. 1992; Leitsch 2004, 2006; Sweeney and Costello 2009; Valentine and Hollingworth 2012).

Magnitude of consequences and social consensus significantly predicted management accountants’ ethical decision-making stages in many presented scenarios. This may be because the issues displayed in the scenarios had a clear unethical content. An ethical issue with a high level of moral salience will produce a high level of moral intensity (Jones 1991). Barnett (2001) argues that older individuals perceive the magnitude of consequences as the most important dimension because of their higher level of moral reasoning; 66 % of the participants in this study were aged 35 years or more, with 45 % aged more than 40 years old. The prevalence of social consensus as a significant predictor suggests that management accountants’ views of society’s attitudes to issues may impact their ethical decision making (Rest 1986). Kohlberg’s (1969) theory of moral development posits that at conventional levels of ethical reasoning, individuals are impacted by rules set by society, which reflect the consensus of the community on the ethical characteristics of specific actions. Further, Jones (1991) argues that individuals consider societal standards to decrease uncertainty when faced with ethical issues. Therefore, individuals will be more likely to make an ethical decision which is consistent with societal standards.

Previous empirical research on temporal immediacy has been limited and yielded mixed results, with some studies finding that it has little or no association with the ethical decision-making process (Barnett 2001; Barnett and Valentine 2004) and others that it is associated significantly with ethical decision-making stages (Singhapakdi 1999; Singhapakdi et al. 1996; Vitell and Patwardhan 2008; Yang and Wu 2009). The result here is consistent with the findings of Leitsch (2006) and Yang and Wu (2009) who used similar scenarios. Similar to magnitude of consequences and social consensus, temporal immediacy was also sometimes a significant predictor of the three stages of management accountants’ ethical decision making and justified its inclusion in the study. However, most past research (see for example the review of O’Fallon and Butterfield 2005) reveals that magnitude of consequences and social consensus are generally more significantly related than temporal immediacy. This result could be attributed to the adequate information provided in each scenario regarding the onset of consequences. It might also reflect a different conception of time in Libyan culture; this is an issue for further investigation.

Relationship between Stages

According to Rest (1986), ethical decision-making stages generally occur in a sequential manner and can affect each other (Wotruba 1990). Ethical recognition and ethical judgment were added to the regression model to examine the relationships between stages within the Libyan context. Researchers have tested ethical decision-making stages as independent variables to each other and found significant statistical relationships between them (Bateman et al. 2013; Leitsch 2006; Sweeney and Costello 2009; Yang et al. 2006). This would be expected, given the logical structure of Rest’s model, though the less than perfect correlation justifies looking at three rather than just one or two stages—which previous research has tended to do. The results of this study also show a significant relationship between ethical recognition and ethical judgment and also between ethical judgment and ethical intention, but ethical recognition did not significantly predict ethical intention in the final regression model. This is consistent with his model of moral intensity dimensions, in which Jones (1991) proposes that ethical recognition impacts ethical intention only through ethical judgment. This confirms Rest’s model of ethical decision making that there is no direct association between ethical recognition and ethical intention.

Conclusion

Research into the ethics of management accounting and management accountants is under-represented in the journal literature (Bampton and Cowton 2013). Furthermore, most of the significant body of research into ethical decision making, building on Rest’s model, has been conducted in developed western countries, often using only one or two stages of the model. This study investigated the role of several variables in the ethical decision making of management accountants in an emerging country, namely Libya. Unlike most previous research, it examined three of the four stages of ethical decision making (Rest 1986). The empirical relationships between the three stages provided support for the use of Rest’s model. The results revealed that moral intensity dimensions and personal moral philosophy explained a significant proportion of the variance in management accountants’ ethical recognition, judgment and intention (while ethical recognition predicted ethical judgment which in turn predicted ethical intention). Comparatively few significant results were found in relation to the organizational variables, age, gender and educational level and the three ethical decision-making stages. However, where gender revealed a significant relationship with ethical decision making, it was males who tended to be more ethical, which is an unusual result. Moreover, temporal immediacy was more prominent than in previous studies. The apparent lack of impact of company codes of ethics suggests that companies should pay more attention to their content and to how they are supported, especially—in the case of management accountants—while the accounting profession in Libya remains under-developed.

Limitations and Future Research

As is the case with all research in business ethics and other areas, the study is subject to some limitations. Although the study sample should be representative of the intended target population and the results of the survey can be generalized, the sample was limited to management accountants who work for manufacturing companies. The results may not be uncritically generalized to management accountants who work for other organizations such as banks or governmental organizations. However, given that management accountants, in general, have similar tasks regardless of the organizations they work for, this limitation may not be a big concern.

In order to produce a questionnaire of reasonable length, and following the practice of most previous researchers, single item measures for each stage of the ethical decision-making process and each dimension of moral intensity were adopted here. One item might not be sufficient to measure each stage of the ethical decision-making process in a fully reliable way, and thus the results should be interpreted with caution. Although all the measures used in the present study have been validated in previous research, future studies that have a narrower research agenda—and hence do not have the same pressure on the length of the research instrument—could perhaps use multiple item measures and so also provide useful evidence on the shortcomings, if any, of single item measures. In addition to guiding further research on ethical decision making, the present study also suggests that a more intensive study of corporate codes of ethics in Libya would be useful.

The challenge of measuring ethical recognition in this study should be acknowledged, given that when respondents are asked about ethical issues, their sensitivity is heightened. However, this issue is common to the large body of previous research on which the present study builds. Moreover, it should also be noted that the focus is not on the absolute level of ethical recognition as such but on the association of certain independent variables with variations in ethical recognition (and judgment and intention).

Given the dearth of management accounting ethics research across countries, and the important role that management accountants play, especially within manufacturing companies, more research is needed regarding the area of management accounting ethics in general and organizational factors affecting management accountants’ ethical decision-making process in particular. It would also be useful to compare management accountants working in different sectors, such as manufacturing, banks and public services. If, as it is thought might be the case in Libya, management accountants in developing, formerly planned economies show great similarities because of their common background, it would be interesting to undertake longitudinal research to track any industry effects that might develop over time. It would also be useful to conduct a study across several different Muslim majority countries and to look at other sorts of developing countries.

Notes

The four most comprehensive reviews related to the ethical decision-making process in business ethics research.

It was decided not to report the following regressions with dummy-coded categorical variables included, given their lack of relationship with the ethical decision making stages. If one does include them, then their minimal influence is confirmed (only 5 % of the additional results generated from the categorical predictors were significant in the final regression models, while 93 % of the significant continuous predictors were still significant).

References

Agarwal, J., & Malloy, D. C. (1999). Ethical work climate dimensions in a not-for-profit organization: An empirical study. Journal of Business Ethics, 20(1), 1–14.

Al-Khatib, J. A., Dobie, K., & Vitell, S. J. (1995). Consumer ethics in developing countries: An empirical investigation. Journal of Euromarketing, 4(2), 87–109.

Al-Khatib, J. A., Rawwas, M. Y. A., & Swaidan, Z. (2005). The ethical challenges of global business-to-business negotiations: An empirical investigation of developing countries’ marketing managers. Journal of Marketing Theory & Practice, 13(4), 46–60.

Al-Khatib, J. A., Vitell, S. J., & Rawwas, M. Y. A. (1997). Consumer ethics: A cross-cultural investigation. European Journal of Marketing, 31(11/12), 750–767.

Appelbaum, S. H., Deguire, K. J., & Lay, M. (2005). The relationship of ethical climate to deviant workplace behaviour. Corporate Governance, 5(4), 43–55.

Armstrong, M. B., Ketz, J. E., & Owsen, D. (2003). Ethics education in accounting: Moving toward ethical motivation and ethical behavior. Journal of Accounting Education, 21(1), 1–16.

Attia, A., Shankarmahesh, M. N., & Singhapakdi, A. (1999). Marketing ethics: A comparison of American and Middle-Eastern marketers. International Business Review, 8(5–6), 611–632.

Bampton, R., & Cowton, C. J. (2013). Taking stock of accounting ethics scholarship: A review of the journal literature. Journal of Business Ethics, 114(3), 549–563.

Barnett, T. (2001). Dimensions of moral intensity and ethical decision making: An empirical study. Journal of Applied Social Psychology, 31(5), 1038–1057.

Barnett, T., Cochran, D. S., & Taylor, G. S. (1993). The internal disclosure policies of private-sector employers: An initial look at their relationship to employee whistleblowing. Journal of Business Ethics, 12(2), 127–136.

Barnett, T., & Valentine, S. R. (2004). Issue contingencies and marketers’ recognition of ethical issues, ethical judgments and behavioral intentions. Journal of Business Research, 57(4), 338–346.

Bass, K., Barnett, T., & Brown, G. (1999). Individual difference variables, ethical judgments, and ethical behavioural intentions. Business Ethics Quarterly, 9(2), 183–205.

Bateman, C. R., & Valentine, S. R. (2010). Investigating the effects of gender on consumers’ moral philosophies and ethical intentions. Journal of Business Ethics, 95(3), 393–414.

Bateman, C. R., Valentine, S. R., & Rittenburg, T. (2013). Ethical decision making in a peer-to-peer file sharing situation: The role of moral absolutes and social consensus. Journal of Business Ethics, 115(2), 229–240.

Beekun, R., Hamdy, R., Westerman, J., & Hassab, E. H. (2008). An exploration of ethical decision-making processes in the United States and Egypt. Journal of Business Ethics, 82(3), 587–605.

Beeri, I., Dayan, R., Vigoda-Gadot, E., & Werner, S. (2013). Advancing ethics in public organizations: The impact of an ethics program on employees’ perceptions and behaviors in a regional council. Journal of Business Ethics, 112(1), 59–78.

Betz, M., O’Connell, L., & Shepard, J. M. (1989). Gender differences in proclivity for unethical behavior. Journal of Business Ethics, 8(5), 321–324.

Borkowski, S. C., & Ugras, Y. J. (1998). Business students and ethics: A meta-analysis. Journal of Business Ethics, 17(11), 1117–1127.

Brady, F. N., & Wheeler, G. E. (1996). An empirical study of ethical predispositions. Journal of Business Ethics, 15(9), 927–940.

Browning, J., & Zabriskie, N. B. (1983). How ethical are industrial buyers? Industrial Marketing Management, 12(4), 219–224.

Buchan, H. F. (2005). Ethical decision making in the public accounting profession: An extension of Ajzen’s theory of planned behavior. Journal of Business Ethics, 61(2), 165–181.

Callan, V. J. (1992). Predicting ethical values and training needs in ethics. Journal of Business Ethics, 11(10), 761–769.

Carlson, D. S., Kacmar, K. M., & Wadsworth, L. L. (2002). The impact of moral intensity dimensions on ethical decision making: Assessing the relevance of orientation. Journal of Managerial Issues, 14(1), 15–30.

Centre for Quality Assurance and Accreditation for Higher Education Institutions. (2008). Business school curricula (1st ed.). Tripoli: Ministry of Libyan Higher Education.

Chan, S. Y. S., & Leung, P. (2006). The effects of accounting students’ ethical reasoning and personal factors on their ethical sensitivity. Managerial Auditing Journal, 21(4), 436–457.

Chia-Mei, S., & Chin-Yuan, C. (2006). The effect of organizational ethical culture on marketing managers’ role stress and ethical behavioral intentions. Journal of American Academy of Business, 8(1), 89–95.

Clarke, P., Hill, N., & Stevens, K. (1996). Ethical reasoning abilities: Accounting practitioners in Ireland. Irish Business and Administrative Research, 17, 94–109.

Cleek, M. A., & Leonard, S. L. (1998). Can corporate codes of ethics influence behavior? Journal of Business Ethics, 17(6), 619–630.

Cooper, R. W., & Frank, G. L. (1997). Helping professionals in business behave ethically: Why business cannot abdicate its responsibility to the profession. Journal of Business Ethics, 16(12–13), 1459–1466.

Cowton, C. J. (2009). Accounting and the ethics challenge: Re-membering the professional body. Accounting and Business Research, 39(3), 177–190.

Craft, J. (2013). A review of the empirical ethical decision-making literature: 2004–2011. Journal of Business Ethics, 117(2), 221–259.

Cullen, J. B., & Victor, B. (1993). The ethical climate questionnaire: An assessment of its development and validity. Psychological Reports, 73, 667–674.

Davis, M. A., Johnson, N. B., & Ohmer, D. G. (1998). Issue-contingent effects on ethical decision making: A cross-cultural comparison. Journal of Business Ethics, 17(4), 373–389.

Dawson, L. M. (1997). Ethical differences between men and women in the sales profession. Journal of Business Ethics, 16(11), 1143–1152.

DeConinck, J. B. (2004). The effect of ethical climate and moral intensity on marketing managers’ ethical perceptions and behavioral intentions. Marketing Management Journal, 14(1), 129–137.

DeConinck, J. B., & Lewis, W. F. (1997). The influence of deontological and teleological considerations and ethical climate on sales managers’ intentions to reward or punish sales force behavior. Journal of Business Ethics, 16(5), 497–506.

Doyle, E., Frecknall-Hughes, J., & Summers, B. (2014). Ethics in tax practice: A study of the effect of practitioner firm size. Journal of Business Ethics, 122(4), 623–641.

Drury, C. (2004). Management and cost accounting (6th ed.). London: Thomson.

Dubinsky, A. J., & Ingram, T. N. (1984). Correlates of salespeople’s ethical conflict: An exploratory investigation. Journal of Business Ethics, 3(4), 343–353.

Dubinsky, A. J., Nataraajan, R., & Wen-Yeh, H. (2004). The influence of moral philosophy on retail salespeople’s ethical perceptions. Journal of Consumer Affairs, 38(2), 297–319.

Elango, B., Paul, K., Kundu, S., & Paudel, S. (2010). Organizational ethics, individual ethics, and ethical intentions in international decision-making. Journal of Business Ethics, 97(4), 543–561.

Ergeneli, A., & Arıkan, S. (2002). Gender differences in ethical perceptions of salespeople: An empirical examination in Turkey. Journal of Business Ethics, 40(3), 247–260.

Etherington, L. D., & Schulting, L. (1995). Ethical development of accountants: The case of Canadian certified management accountants. Research on Accounting Ethics, 1, 235–251.

Fang, E., & Foucart, R. (2013). Western financial agents and Islamic ethics. Journal of Business Ethics, 1, 1–17.

Ferrell, O. C., & Gresham, L. G. (1985). A contingency framework for understanding ethical decision making in marketing. Journal of Marketing, 49(3), 87–96.

Ferrell, O. C., & Skinner, S. J. (1988). Ethical behavior and bureaucratic structure in marketing research organizations. Journal of Marketing Research, 25(1), 103–109.

Field, A. P. (2009). Discovering statistics using SPSS (3rd ed.). Los Angeles, CA: SAGE.

Fleischman, G., & Valentine, S. R. (2003). Professionals’ tax liability assessments and ethical evaluations in an equitable relief innocent spouse case. Journal of Business Ethics, 42(1), 27–44.

Flory, S. M., Phillips, T. J., Reidenbach, R. E., & Robin, D. P. (1992). A multidimensional analysis of selected ethical issues in accounting. Accounting Review, 67(2), 284–302.

Ford, R. C., & Richardson, W. D. (1994). Ethical decision making: A review of the empirical literature. Journal of Business Ethics, 13(3), 205–221.

Forsyth, D. R. (1980). Taxonomy of ethical ideologies. Journal of Personality and Social Psychology, 39(1), 175–184.

Forsyth, D. R. (1992). Judging the morality of business practices: The influence of personal moral philosophies. Journal of Business Ethics, 11(5), 461–470.

Forte, A. (2004). Business ethics: A study of the moral reasoning of selected business managers and the influence of organizational ethical climate. Journal of Business Ethics, 51(2), 167–173.

Fritzsche, D. J. (2000). Ethical climates and the ethical dimension of decision making. Journal of Business Ethics, 24(2), 125–140.

Galbraith, S., & Stephenson, H. B. (1993). Decision rules used by male and female business students in making ethical value judgments: Another look. Journal of Business Ethics, 12(3), 227–233.

Gilligan, C. (1982). In a different voice: Psychological theory and women’s development. Cambridge, MA: Harvard University Press.

Glover, S. H., Minnette, A. B., Glynda, F. S., & George, A. M. (2002). Gender differences in ethical decision making. Women in Management Review, 17(5), 217–227.

Gray, R., Bebbington, J., & Mcphail, K. (1994). Teaching ethics in accounting and the ethics of accounting teaching: Educating for immorality and a possible case for social and environmental accounting education. Accounting Education, 3(1), 51–75.

Green, S., & Weber, J. J. W. (1997). Influencing ethical development: Exposing students to the AICPA code of conduct. Journal of Business Ethics, 16(8), 777–790.

Groves, K., Vance, C., & Paik, Y. (2008). Linking linear/nonlinear thinking style balance and managerial ethical decision-making. Journal of Business Ethics, 80(2), 305–325.

Haines, R., & Leonard, L. N. (2007). Individual characteristics and ethical decision-making in an IT context. Industrial Management & Data Systems, 107(1), 5–20.

Howell, D. C. (2006). Statistical methods for psychology (6th ed.). Belmont, CA: Thomson Wadsworth.

Hunt, S. D., & Vitell, S. J. (1986). A general theory of marketing ethics. Journal of Macromarketing, 6(1), 5–16.

Jaffee, S., & Hyde, J. S. (2000). Gender differences in moral orientation: A meta-analysis. Psychological Bulletin, 126(5), 703–726.

Johl, S., Jackling, B., & Wong, G. (2012). Ethical decision-making of accounting students: Evidence from an Australian setting. Journal of Business Ethics Education, 9(1), 51–78.

Jones, T. M. (1991). Ethical decision making by individuals in organization: An issue-contingent model. Academy of Management Review, 16(2), 366–395.

Kaptein, M. (2011). Toward effective codes: Testing the relationship with unethical behavior. Journal of Business Ethics, 99(2), 233–251.

Karacaer, S., Gohar, R., Aygün, M., & Sayin, C. (2009). Effects of personal values on auditor’s ethical decisions: A comparison of Pakistani and Turkish professional auditors. Journal of Business Ethics, 88(1), 53–64.

Kilani, K. A. (1988). The evolution and status of accounting in Libya. Unpublished Ph.D., Hull University, Hull

Kohlberg, L. (1969). Stages in the development of moral thought and action. New York: Holt, Rinehart and Winston.