Abstract

This paper analyzes the implications of investors’ short-term oriented asset holding and portfolio decisions (or short-termism), and its consequences on green investments. We adopt a dynamic portfolio model, which contrary to conventional static mean-variance models, allows us to study optimal portfolios for different decision horizons. Our baseline model contains two assets, one asset with fluctuating returns and another asset with a constant risk-free return. The asset with fluctuating returns can arise from fossil-fuel based sectors or from clean energy related sectors. We consider different drivers of short-termism: the discount rate, the nature of discounting (exponential vs. hyperbolic), and the decision horizon of investors itself. We study first the implications of these determinants of short-termism on the portfolio wealth dynamics of the baseline model. We find that portfolio wealth declines faster with a higher discount rate, with hyperbolic discounting, and with shorter decision horizon. We extend our model to include a portfolio of two assets with fluctuating returns. For both model variants, we explore the cases where innovation efforts are spent on fossil fuel or clean energy sources. Detailing dynamic portfolio decisions in such a way may allow us for better pathways to empirical tests and may provide guidance to some online financial decision making.

Similar content being viewed by others

1 Introduction

Substantial amounts of capital, whether from public or private sources of financing, are needed to fund the mitigation and the adaptation to climate change. These types of projects are of long-term nature, and investors should respond to the long-term risks of global warming, (Carney, 2015). As recent literature has pointed out (i.e. Cella et al., 2013 and Davies et al., 2014), investors’ short-sighted behavior can limit the amount of capital channeled towards green investments. There is no commonly agreed or accepted definition of short-term behavior or short-termism as we define it in this paper, but it can be loosely understood as the tendency of financial intermediaries or corporate managers to overly favor short-term payoffs over long-term opportunities. The aim of this paper is to study the implications of short-termism on portfolio decisions of investors, and its potential consequences on green investments.

The debate over short-termism in investment decisions is not recent, and most of the discourse tends to describe it as sub-optimal with adverse implications. For instance, short-term behavior is believed to lead to inefficiencies and mispricing in financial markets, including asset price bubbles and panics (Bushee, 2001; Rappaport, 2005; Cremers & Pareek, 2015; Cella et al., 2013). Short-termism can also affect corporate behavior, by inducing corporate myopia, which in turn has an adverse impact on investment decisions, creation of long-term value and hence economic growth (Chen et al., 2007; Elyasiani & Jia, 2010; Attig et al., 2012). Finally, short-termism can impact the efficiency of financial intermediation, through the rise of the trading frequency (Edelen et al., 2013) or through the mis-alignments of horizons between investors and institutions managing their wealth (i.e., the agency problem) (Guo, 2013). Hence, short-term behavior can exacerbate the obstacles for financing long-term projects, including environmentally friendly green investments.

A number of determinants (often interlinked) has been identified in the literature with respect to investment horizon. Warren (2014) provides an exhaustive list of determinants of short-termism, which can be grouped into three types of influences: those related to the conditions under which investors operate; for instance, the extent to which investors have freedom in trading decisions directly influences their need for liquidity, and so their tolerance to adopt a longer investment horizon. Another type of influences is related to the design of the investment environment; the way organizations are configured (i.e., remuneration practices; financial market structures) can influence their scope to adopt a long-term approach. Finally, there are influences related to investors’ behavior. Immediate gratification, present bias, aversion to risk or myopic loss aversion expressed by agents can lead to adopting short-term investment decisions.

Based on the above short description of the determinants of investment horizon, we limit our treatment of short-termism by varying three main drivers; namely, the risk-aversion parameter, the discount factor, and the decision horizon itself. A dynamic model of intertemporal choice in finite horizon is suited to analyze the impact of short-termism on investment decisions when climate risks hold, it allows us to study optimal portfolios for different decision horizons. In this regard, a simplified Merton-type dynamic consumption and asset allocation problem is formulated in continuous time. For analytical purposes, we start first with a simple model of two assets, one asset with constant risk-free returns and the other with time-varying returns, where the objective of the investor is to maximize her welfare over payouts (or consumption). We explore then the effects of varying risk aversion, discount rate, and decision horizon on consumption-wealth ratio and the wealth dynamics. Next, we expand our analysis and include, in the same baseline model, a time-inconsistent discount factor, namely a hyperbolic discount function, to illustrate its impact on wealth accumulation overtime. We also study the impact of shocks on asset returns and their effect on the evolution of wealth. Finally, we extend the model to include two decision variables and two time-varying returns, and we explore again the effects of the variation of the parameters of discounting and decision horizon.

Questions related to investment/consumption decisions problems in continuous time have been usually approached, in the literature, using the Merton’s (1971) framework. Merton’s theory has been widely adopted, under various extensions, in academic research. While, under certain assumptions, it provides elegant solutions and insightful results overall, it remains hard to implement in practice. For instance, measuring accurately state variables, betas or correlations remains a challenging task, particularly that portfolio maximization is very sensitive to inputs (Cochrane, 2021). Another difficulty resides in the ability to accurately forecast stock returns. The estimation of stochastic processes in the empirical literature to predict asset returns has not been sufficiently successful; among other reasons, the dependence of the stochastic processes on the Gaussian distribution is one limitation (Blomberg et al., 2020).

A number of methods, in the literature, have been developed to accurately forecast stock returns, among them is spectral analysis. Also termed harmonic analysis, this method decomposes a time periodic phenomenon into a series of linear combination of sine-cosine functions, each defined by a unique amplitude and phase values. Spectral analysis has been used in the literature for different purposes; for instance, to analyze the behavior of economic time series (Iacobucci, 2005); to forecast the growth rate and returns (Keim et al., 2006); to examine asset volatility and stock return series (Tsay, 2010; Chaudhuri & Lo, 2015); to price derivatives, (Phelan et al., 2019); and to study the degree of interdependence between markets (Créti et al., 2014).

Our modeling approach departs from the standard one in two respects. First, asset returns in our model are represented by a trigonometric sine-cosine function, instead of a stochastic process as in Merton. This is an assumption that is based on the fact that consumption and portfolio decisions by individuals and asset managers are often undertaken with respect to low-frequency data. Another difference to the standard model is related to the numerical solution method. In Merton’s standard approach, the model is solved via Dynamic Programming, but this method suffers from the so-called “curse of dimensionality” when we increase the number of state variables. In our paper, we adopt the numerical method of Nonlinear Model Predictive Control (NMPC), which has the advantage of easily handling multi-dimentional and finite horizon decision making problems. In addition, NMPC allows us to differentiate between the control horizon, which could be interpreted as the decision horizon of the investor, and the planning horizon. The latter is a long run horizon the end of which is obtained through a sequence of receding decision horizons. Finally, the numerical method is of great practical use: the prediction-control mechanism permits the investor to undertake some on-line strategy where assets are re-allocated when new information is coming in from the market.

From the different cases studied in the paper, we find that portfolio wealth declines faster when we vary the different determinants of investment horizon we defined. An increase in the discount rate, reflecting investors’ impatience, affects negatively asset buildup. Similar results are obtained when we consider a different discount factor, (i.e. hyperbolic discounting). Investors with shorter decision horizon (control horizon) tend to depreciate faster portfolio wealth. The later results are obtained with the general conjecture that short-sighted investors tend to invest mostly in fossil fuel assets. In addition, the negative externalities effect resulting from carbon emissions will also generate lower returns even if the decision horizon is the same. Thus, short-termism, and negative externalities, not internalized in asset price formation, will impede the ability of green investments to take off easily even with good portfolio performance.

The rest of the paper proceeds as follows. Section 2 sets out an analytical portfolio framework for one asset with fluctuating returns and one risk-free asset with constant return to capture the potentially adverse consequences of short-termism, in particular for the cost of capital and for investment intentions. Section 3 presents numerical results on specific channels of short-termism. Section 4 extends the model by building on two assets driven by time varying returns whereby the asset returns are empirically estimated through harmonic estimations. A sketch of the algorithm used for the solution of the model variants in Sects. 3 and 4 is presented in the appendix. Section 5 concludes with next steps for policy and research on this topic.

2 The dynamic portfolio model

Our point of departure is the standard Merton model, which we briefly describe, then modify to represent assets returns in harmonic form. Under the new setting, we derive the optimal consumption and investment policies. Next, we derive the optimal policies under the assumption of hyperbolic discounting. We also consider the case when there is a sudden shock to the asset’s fluctuating returns. Finally, we further extend the model to include another decision variable, to estimate the role of innovation investment in the value of the portfolio over time.

We consider a continuous-time economy similar in spirit to the ones of Merton (1971), Merton (1973), Cox et al. (1985), Gennotte (1986) models, where the economy is endowed with a finite number of production technologies; for instance, a polluting technology and a clean (innovative) one, each represented by a productive firm, or both owned by the same firm. In addition to direct investment in one of the production technologies, agents can invest in a risk-free asset with constant returns; namely a treasury bond. Therefore, we study, as a baseline model, a dynamic portfolio choice problem that contains two assets. We consider the portfolio performance of the assets for either of the portfolios. To summarize, investors are facing an asset allocation decision problem, while at the same time and as pointed out by Tobin (1958), there is a choice to be made on how much to save and how much to consume.

2.1 The standard model

Under the defined setting, the investor chooses a strategy of consumption and investment over a time horizon (planning horizon) T in order to maximize her expected time-additive utility of consumption and possibly of terminal wealth.

subject to the wealth process, \(W_t\), satisfying a dynamic self-financing budget constraint:

\(F(c_tW_t)\) and \({\bar{F}}(W_T)\) in (1) are the utility of consumption and of terminal wealth respectively. \(\varphi _\alpha (t)\) is a general discount factor, taking the form:

for \({\displaystyle \alpha \in [0,1]}\). In the two extreme cases, when \({\displaystyle \alpha =0}\), \({\displaystyle \varphi _{0}(\tau )}\) becomes an exponential discount factor with discount rate \({\displaystyle \delta _{0}}\), and when \({\displaystyle \alpha =1}\), it is a hyperbolic discount function with rate \({\displaystyle \delta _{1}}\). \(\tau \) in (3) is the relative time from a baseline date. \(C_t\) in (2) is the consumption rate. \(X(\omega _{t}, W_t)\) represents the adjustment costs that the investor incurs by holding the equity assets. \(\omega _t\) is the share of wealth invested in the productive asset, while \(B_t\) and \(P_t\) are the prices of the risk-free bond and the productive asset respectively. The risk-free bond, \(B_t\), pays a constant interest rate \(r^f\), and satisfies the equation:

As for the price dynamics of the productive asset, they are represented in the standard setting by the following general process:

with \(\mu (\phi _t,t)\), the drift term, representing the expected return of the asset; \(\sigma _P(\phi _t,t)\) the volatility of the price process. \({\mathbb {Z}}_t\) is a Brownian motion. \(\phi _t\) in (5) is a state variable that captures the variations in \(\mu \) and \(\sigma _P\) over time, and whose dynamics follow a diffusion process:

with \(m(\phi _t)\) a function of state variable \(\phi _t\), and \({\mathbb {Z}}'_t\) is a standard Brownian motion independent of \({\mathbb {Z}}_t\).

2.2 Portfolio of assets with time-varying returns

In this section, we illustrate how a Fourier Series of a periodic function can be used to model the dynamics of the productive asset returns. Unlike high-frequency trading where a large number of orders are transacted by powerful computers in a fraction of a second, consumption and portfolio decisions by individuals or portfolio managers are often based on low-frequency data. We consider assets characterized by returns that can be represented by low frequency movements to take place as time varying expected returns. The main objective of spectral analysis is to highlight the cyclical processes. It entails the wave structure of the considered variable of stochastic process. Through the use of trigonometric functions, we can analyze time series in the frequency domain. Therefore, we re-express (5) and (6) in our model as:

where \(r_{t}^{e}\) represents the time-varying return of the productive asset and can take the following general form:

with \(\alpha _{0}\) representing a phase shift, \(\alpha _{1,n}\) and \(\beta _{1,n}\) are coefficients representing the amplitude of the asset’s return, while \(\alpha _{2,k}=2\pi \frac{k}{T}\) represent the cyclicality of the return. The approximated Fourier coefficients \(\alpha _{1,n}\) and \(\beta _{1,n}\) (denoted \({\tilde{\alpha }}_{1,n}\) and \({\tilde{\beta }}_{1,n}\)) are estimated by a collocation method in the frequency domainFootnote 1:

where \(t_n=(n-1)\Delta t\) for \(n=0,1,2,...,M-1\) and \(\Delta t=T/M\). \(\frac{1}{T}, \frac{2}{T}, \frac{3}{T},\ldots \), are frequencies of the sines and cosines (the frequency \(\frac{k}{T}\) is called the \(k^\text {th}\) harmonic). In Sect. 3, for illustrative purposes, we simplify (8) into

then we revert back again to the more general (8), in Sect. 4, to approximate from current market data the asset returns of two assets in the portfolio.

2.3 Optimal policies under time-varying returns

Having defined the model and expressed the returns of the productive asset in harmonic form, we derive next the optimal policies of the investor. In the baseline case, we consider an investor with time-additive expected constant relative risk aversion utility, with risk aversion parameter \(\gamma \). In addition, the utility function of the investor is discounted by an exponential discount factor (i.e., \(\alpha = 0\) in Eq. (3)). Based on (1) and (2), the maximization problem of the investor is reformulated explicitly as:

adjustment costs, \(x(\omega _t)\), is a function of the number of productive asset shares held. We interpret investment broadly to include changes in working capital so, under clean surplus accounting, capital becomes conceptually equivalent to total assets and the book value of the firm, (see Broer and Jansen, 1998, Liao et al., 2020). \(x(\omega _{t})\) takes the standard quadratic form:Footnote 2.

\(\theta \) is an adjustment cost parameter; a higher value of \(\theta \) implies a higher cost \(x(\omega _t)\).

To derive the optimal solutions using dynamic programming, we restate (9) in terms of an indirect utility function and apply the Bellman principle of optimality. The indirect utility function is given by

where \(\varepsilon _{1}\) and \(\varepsilon _{2}\) are greater than or equal zero with at least one of them being non-zeroFootnote 3. Equation (12) is subject to the same constraint as in (9), hence \(V(W(T),T) = \varepsilon _{2} {\bar{F}}[W_{t},T]\). The Hamilton-Jacobi-Bellman equation associated with our optimization problem is

Assuming a power utility function exhibiting constant relative risk-aversion,

it is straightforward to obtain the optimal consumption and investment decisions; the first-order conditions with respect to \(C_t\) and \(\omega _t\) yield:

and

the optimal share of the productive asset in the portfolio is a function of the fluctuating returns, or equivalently the excess return (i.e. the difference between the fluctuating return and the constant risk-free rate). Also from (16), an increase in \(\theta \) reduces the optimal asset allocation, leading to a faster decay of wealth accumulation over time. Optimal consumption, on the other hand, is a function of the partial derivative of the value function \(V(W_t,t)\) with respect W. Since the value function inherits similar properties to the utility function, we conjecture the value function \(V(W_t,t)\) to be of the following form

then

given the time varying nature of the equity returns, the value function g(t) can be estimated numerically. In the special case of the Bernoulli logarithmic utility, (i.e. \(\gamma \rightarrow 1\)), the solutions to the decision problem do not fundamentally change as one can observe from both graphs of Fig. 1 in section .

2.3.1 Optimal policies under hyperbolic discounting

A growing evidence, from the fields of psychology and behavioral sciences, shows that individual preferences tend to be rather time-inconsistent (Elster & Loewenstein, 1992; Loewenstein & Prelec, 1993; Gabaix & Laibson, 2017; Andrikopoulos & Webber, 2019). For instance, in searching for instant gratification, decision makers often exhibit a change of preferences when choosing between a smaller, earlier payoff and an alternative larger, but delayed reward. Contrary to the standard assumption of time-consistent preferences, where the investor has no incentives to deviate from an ex-ante optimal plan in future times, in this section we look into utility maximization where the agent discounts future payoffs at a non-constant rate.

Time-inconsistent preferences are often modeled through hyperbolic discounting. Hyperbolic discount functions are characterized by higher discount rates over short horizons and a relatively low discount rate over long horizons, which creates conflict between today’s preferences and those that will be held in the future. The time inconsistency that results from this discounting approach can lead investors to put more weight on the near-term outcomes, relative to more distant prospects such as long-term investments. In our model we look into the case when \(\alpha =1\); hence, the discount function (3) becomes \(\varphi _{1}(\tau )=\frac{1}{1+\delta _{1}\tau }\). Formally, in the case of hyperbolic discounting, the value function \(V(W_{t},t)\) satisfies the following Hamilton–Jacobi–Bellman equation:

the expectation \({\mathbb {E}}_{t,w}\left[ \int _{t}^{T}\varphi _{1}^{\prime }(s-t)F(C_{s})ds\right] \) in (19) shows the difference in how one would value consumption between her current self and her immediate future self. This is similar to saying that the derivative characterizes the difference between the current value function and the continuation value function. The existence of the expectation term in (19) is due to the fact that the hyperbolic discount rate is non-constant, which makes the Hamilton–Jacobi–Bellman equation non-local; therefore, difficult to solve analytically. Following the approach of Dong and Sircar (2014), it is possible to bypass the non-local issue by using the method of asymptotic expansions. The optimal consumption under hyperbolic discounting is

and

We refer to Dong and Sircar (2014) for more details on the steps of the asymptotic expansions method to derive the optimal policies under hyperbolic discounting. From the above results, the proportion of wealth invested in the productive asset is not affected by the addition of a small amount of hyperbolic discounting feature to the discount factor. On the other hand, the solution for consumption rate is changed by a fraction that depends on the ratio \(\frac{h(t)}{g(t)}\). Zou et al. (2014) obtain similar results. Hyperbolic discounting encourages individuals to consume at a faster rate, than under the exponential discount rate case. The increase in consumption rate would reduce wealth accumulation as depicted in Fig. 2. In this figure, we can notice the difference between the paths of wealth when adopting an exponential discount factor (lower curve) as opposed to a hyperbolic one.

2.3.2 Optimal policies under random occurrence of shocks

Our baseline model is built under the assumption that the returns of the equity asset are time-varying but the coefficients of the sine-wave function that approximate the low-frequency movements are set constant, which would make the periodic returns predictable; therefore, one could predict the optimal path of the control and state variables. In reality though, as has been referred to above, the periodic functions are basically a harmonic fit of real price movements of assets, and should be updated with new incoming realizations that are exposed to shocks. Hence coefficients’ values can change, particularly after a sudden jump (upward or downward) of the price of the equity asset. Formally, from (\(8^\prime \)) this would mean that the coefficient \(\alpha _1\) becomes time dependent such that

While using a deterministic model in the background, it is still possible to represent a regime change, at an uncertain time, in the asset returns. We consider \(\alpha _1(\tau ^{\prime })\) a time dependent process, whose value can change at a random point in time, \(\tau ^{\prime }\). As illustrated in the numerical section, Fig. 3 shows the path of wealth when the coefficient \(\alpha _{1}\), representing the magnitude of the return, changes after a randomly determined period.

2.3.3 Dirty consumption vs. clean innovation

We extend in this section the model to include a new decision variable for the objective function. Namely, in addition to spending a fraction \(c_{t}\) of her wealth on consumption, the investor decides to spend also a fraction \(u_{t}\) of her wealth in innovation efforts; efforts aimed for instance at developing clean technology. This is in line with the previous work of Acemoglu et al. (2012) on directed technical change. We explore then the effects of time varying returns and decision horizon on the consumption-wealth ratio and the path of wealth. This will allow us also to observe whether wealth is increasing or decreasing over time considering innovation. We again allow for two assets, a risk-free bond and an equity, whereby the equity asset displays time varying returns, and we consider the effects short-termism versus long run investment strategies, specified in terms of the decision horizon.

The new decision problem of the investor can be stated as follow:

with

We presume, following endogenous growth theoryFootnote 4, that the spending on \(u_{t}\), as a fraction of wealth, can have a positive externality effect on the returns on the equity asset \(R_{t}^{e}W_{t}\). We also assume that the mean of the returns for the short term interest rate, \(r^{f}\), is not affected, but the equity return is positively impacted by spending on innovation (or negatively impacted by the external effects arising from fossil fuel production).

With a slight change of notation, we denote asset returns here by \(R_{t}^{e}\) and it is formulated as follows:

The time varying return is formulated in a similar way as in the previous section, but there is now an additional return effect for equity return, \(R_{t}^{e}\), represented by the term \((\pm \mu \ (u_{t}W_{t}))\), with \(\mu \) a constant coefficient. A \(``+''\) sign in (25) implies a positive feedback on the asset’s return due to a positive externality from innovation spending. Innovation in a low carbon emission technology, for example, reduces the chances of climate impact damages, which will positively impact the long-run returns of the asset and the growth of the economy. On the other hand, a \(``-''\) sign, implies a negative feedback from the technology used. One can think of a fraction of population operating as fossil fuel engineers who are creating long-run adverse effects on the economy through the creation of negative externalities (such as \(\text {CO}_{2}\) emission, affecting global temperature and creating damages in the long run)Footnote 5. Finally, we attach weights (\(\phi _{1})\) and (\(1-\phi _{1})\) to the two components of the objective functions, as shown in (28), which could be varied exogenously.

2.3.4 Solutions to the decision problem

To derive the optimality equations, we restate (22) in a dynamic programming form in order to apply the Bellman principle of optimality. Again, the indirect utility function is defined by

Equation (26) is subject to similar constraint as (9), hence \(V(W(T),T)={\bar{F}}[W_{t},T]\). The Hamilton–Jacobi–Bellman equation for our economic problem is

For this specific excercise, we assume the limiting case of \(\gamma \rightarrow 1\) of \(\log \) utility function for \(F(c_{s},u_{s})\):

Following the same procedures as in the baseline model, the value function \(V(W_t,t)\) in the log utility case takes the following form

the first order conditions with respect to \(c_t\), \(u_t\), and \(\omega _t\) give us the following optimal paths:

and

where \(A_1=\frac{1}{\theta }r^e_t W_t \mu \left( r_t^e- r^f\right) \), and \(A_2=\frac{1}{\theta }r^{e^2}_t W_t^2 \mu ^2\).

from (30), the optimal fraction \(u_t^*\) in innovation efforts is influenced by the asset’s returns \(r_t^e\), adjustment costs \(\theta \) and the parameter \(\mu \).

3 Numerical solutions

To gain better intuition, we show the numerical results of varying the three determinants of short-termism we defined earlier; namely, the risk-aversion parameter, the discount rate and the discount factor (Sect. 3.2), and the decision horizon itself (Sect. 3.3). We first introduce the numerical method we use. We treat our model as an optimal control problem and solve it numerically by means of Nonlinear Model Predictive Control (NMPC). The NMPC method carries a number of computational advantages. The optimization procedure allows us to compute a higher dimensional problem. It allows us to compute one trajectory at a time for the two state variables and the two decision variables \(\{c_t,\omega _t\}\) (and later for three decision variables in the extended version; \(\{c_t, u_t, \omega _t\}\)) at a finite time horizon with forward looking behavior. Model Predictive Control allows us also to relax the assumption of perfect foresight, since estimates of the control variables are based on the decision horizon and not the full planning horizon, and are re-estimated at every iteration (Nystrup et al., 2019).

3.1 The NMPC procedure

Also known as the Receding Horizon Control (RHC), the NMPC method involves repeatedly solving a constrained optimization problem, using estimates of future payoffs and constraints over a moving time horizon representing the decision horizonFootnote 6. The numerical procedure consists of replacing the maximization of a long horizon functional in continuous time by the iterative maximization of a finite horizon functional in discrete time. In general terms, we re-express (1) and (2) in a discretized form:

\(N \in {\mathbb {N}}\) is a truncated (receding) finite horizon. The index \(i=1, 2, 3,\ldots \) indicates the number of iterations. \(x_{k,i}\) is the set of state variables; in our model \(x_{k,i}=\{W,t\}\)Footnote 7. \(\nu _{k,i}\) is the set of control (decision) variables; \(\nu _{k}=\{c_k,\omega _k\}\) in the standard case. Given an initial value of the state \(x_0\), an approximate solution of the system (32)–(33) can be obtained by iteratively solving (33) such that for \(i=1,2,3,\ldots \) that solves for the initial value \(x_{0,i}:= x_i\) the resulting optimal control sequence is \(\nu ^*_{k,i}\), but uses only the first control \(\nu _i := \nu ^*_{0,i}\). At the next step, the process is repeated, starting from the new control \(\nu _{k+1}\). In addition, by means of the turnpike propertyFootnote 8, it is possible to improve the convergence properties of the model in the context of a long planning horizon, if globally optimal steady-state \(\left( {\bar{x}}, {\bar{\nu }} \right) \) exist.

The economic interpretation of N in our model refers to the decision horizon; a large N implies that the investor cares more about the distant future payoffs, while a small N indicates that the investor thinks rather about near future payoffs and does not care much about the long-term returns. We restrict the decision variable \(\omega _{t}\) to \(\omega _{t}\le 1.2\) which means restricting the short selling of the risk-free asset. Finally, in the numerical solution procedure, we do not consider the terminal condition to solve the model.

3.2 Portfolio performance and the discount rate

In this section, we numerically solve the baseline model for a planing horizon of \(T=40\) (iterations) and a decision horizon of \(N=6\). Time is represented on the horizontal axis and the evolution of wealth is on the vertical axis. From Fig. 1, we can observe that wealth shifts down faster with higher discount rates. The evolution of wealth behaves more or less the same, whether we consider a power utility function or the more special case of log utility.

Solutions path of wealth for different discount rates, \(\delta _0=0.01, 0.015, 0.03, 0.07, 0.15\)

In the context of project selection, the investor is interested in estimating the present value (PV) of the project’s discounted payouts (asset returns). We use the model predictive control to calculate the PV, or asset value, of time varying returns for different discount rates. For higher discount rates, the value of the discounted payouts (the integral in Eq. (1)) comes down, from \(PV = 138.1, 133.3, 126.1, 109.5 \ \text {and} \ 85\). The relation between discount rates and the present value of the financial investment is shown in Table 1.

Table 1 illustrates results for a constant decision horizon \(N=6\) and an evaluation of the financial investment project over 40 periodsFootnote 9. We evaluated the financial investment at different discount rates to represent different types of investors. In this example, investors with \(\delta \ge 0.07\) are defined as short-sighted investors. The results presented in table 1 can be linked to fossil fuel and clean energy based assets: If investors exhibit more impatience, namely through a higher discount rate, it will reduce the value of the discounted future payoffs and the project’s PV will be below the investment cost (as in Davies et al. (2014)). This could affect clean energy assets as the capital costs for these types of projects tend to be higher. That is what one can read from Table 1.

Following Tobin’s q theory of investment, one can for instance assume that the investment cost is represented by a book value of investment, \(\text {Inv}=110\). If the investor exhibit a high level of impatience, the investment evaluations with a higher discount rate than \(\delta \ge 0.07\) would be very low and the investment would be rather discarded. Thus, short-termism expressed through high-discount rates, will prevent investors from taking on those financial projects in the last two columns. Short-term behavior represents in this case an obstacle to the development of renewable energy. Therefore, if short-termism and the investor’s nearsightedness is dominant, risky projects and eventually those with less informative signals are not considered. Capital intensive green infrastructure can be seen as these types of projects, which might have difficulties attracting sufficient funds and thus the portfolio holdings of this type of assets will decline. Marginal investment projects, with lower discount rates than \(\delta \le 0.07\), could also be affected; for instance, fossil fuel energy based assets which are first seen as profitable could suddenly collapse when the discount rates swings up, as studies of the years 2008-9 have shown, see Cochrane (2011).

Given that we analyze a dynamic portfolio model with dynamic returns over time, and wealth built up (or decline), a selling of clean energy based assets could also occur, providing then less financial resources for clean energy projects. In our model, we assume however that the asset is held, but its share in total assets holding will fluctuate and eventually decline, as shown through the numerical results of the model. In the above exercise, we varied the discount rate but kept the assumption that investors discount projects on a time-consistent exponential discount factor. Figure 2 displays the solution paths of wealth discounted using the same discount rate but two different discount functions; namely exponential discounting against hyperbolic discounting.

Solutions path of wealth for different types of discount factors, \(\delta =0.03\); upper curve, exponential discounting (\({\displaystyle \alpha =0}\)), lower curve, hyperbolic discounting (\({\displaystyle \alpha =1}\))

As discussed in Sect. 2.3, hyperbolic discounting mainly affects the consumption rate. Hence, the faster decline of wealth as shown by the lower curve in Fig. 2 is due to higher consumption rate in early periods as opposed to the constant exponential discounting. We have also tracked the solution of the case when there is a shock to the returns at a random time. This is depicted in Fig. 3 where there appears a jump in the return at roughly period 5, as numerically programmed in the appendixFootnote 10.

Solutions path of wealth as a result of change of \({\displaystyle \alpha _{1}}\) from 0.05 to 0.08 at \(t=8\)

A positive shock to the asset’s fluctuating returns (through \(\alpha _1\)) at random time t led to higher wealth accumulation over time as depicted by the upper curve of Fig. 3.

3.3 Portfolio performance and the decision horizon

In the previous section, we numerically solved our baseline model for different values of discount rates and different types of the discount factor, while considering the decision horizon N to be fixed for a given planning horizon (iterations) T. In this section we numerically solve the second model, whereby the investor chooses between consumption and spending a fraction of her wealth in innovation efforts. In addition, we modify the asset’s fluctuating returns by introducing a positive drift in the equity returns arising from energy innovation and agnegative drift from fossil fuel externalities respectively. Here we test another aspect of short-termism namely by changing the decision horizon, while we keep the rate of the exponential discount factor fixed. We let the model to be solved for \(T=30\) iterations and a receding window of \(N=2,6,8\).

Solutions path of wealth for different time horizon, \(\delta =0.03\); upper figure, \(N=8\), lower figure, \(N=6\)

In Fig. 4 the results are shown for different decision horizons, \(N=8\) and \(N=6\). The lower graph representing a shorter run decision horizon exhibiting short-termism in the sense of Davies et al. (2014). As we can observe, the time horizon of \(N=6\) leads to less asset built up, more specifically to dissipating asset value in the long run. Here, we simulate the model where the term \((1\pm \mu (u_{t}W_{t})\) holds for + , which implies that \(\mu (\cdot )>0\).

In the second case, we explore another decision horizon \(N=2\) but without including the effect of externalities; in other words, the term \((1\pm \mu (u_{t}W_{t})=1)\) which implies that \(\mu (\cdot )=0\). Letting the model to be solved again for \(T=30\), we get:

Solutions path of wealth for different time horizon, two upper graphs \(\mu (\cdot )>0\), low graph \(\mu (\cdot )=0\), \(T=30\)

Figure 5 shows solutions path of wealth for different decision horizons, as in the previous figure, upper graph, \(N=8\), lower graph, \(N=6\), lowest graph, \(N=2\). As one can observe from the figure above, the lowest graph shows the least asset built up. Hence, even if there is no negative effect from externalities, asset formation is lowest with short-termism driven by a very short decision horizon.

Solutions path of wealth for different time horizons

Figure 6 shows four curves: the upper curve, \(N=8;\) the two graphs below, \(N=6\), with the term \((1+\mu (u_{t}W_{t})),\) and \(N=6\), with the term \((1-\mu (u_{t}W_{t}))\), representing external cost of fossil fuel use; finally the lowest curve, \(N=2\), and here the term \((1\pm \mu (u_{t}W_{t})=1\) which implies that \(\mu (\cdot )=0\). As we can see in Fig. 6, the decision horizon of \(N=8\) with the additional innovation effect for the equity returns, produces superior asset formation, the two graphs below for \(N=6\), with the term \((1+\mu (c_{1,t}W_{t})),\) and for \(N=6\), with the term \((1-\mu (c_{1,t}W_{t}))\), representing external cost of fossil fuel use, exhibit a lower asset formation, in fact decline of asset formation. The lowest graph for \(N=2\) and here the term \((1\pm \mu (c_{1,t}W_{t})=1\), thus even with a \(\mu (\cdot )=0\) this portfolio exhibits a rapid decline of assets.

In general, we observe from the different cases studied that wealth declines faster with shorter decision horizon. It is important to note that the above results are obtained if the general conjecture holds that the short-sighted investors are agents investing mostly in fossil fuel assets. If investors exhibit short-termism, this will show up as a short decision horizon for an asset portfolio (as in Davies et al. (2014)). In addition, the negative externalities effect resulting from \(\text {CO}_{2}\) emissions will also generate lower returns even if the decision horizon is the same, as shown in Fig. 6 with \(N=6\). Thus, short-termism, and negative externalities, not internalized in asset price formation, will hinder the ability of green investments to take off easily even with good portfolio performance.

Hence, short-termism would be an impediment for the fast development of clean energy. Moreover, carbon based energy provisions will show additional negative asset effects in the long run, since it reduces equity returns resulting from disrupted production processes due to climate damages. Therefore, if short-termism and share holders’ nearsightedness is dominant, the more risky projects, and maybe those with less rich information, are not considered. These are likely to be renewables which will have issue attracting sufficient capital funds and thus the portfolio holdings of this type of assets will decline. We also want to note that in principle the weights \(\phi _{1}\) and \((1-\phi _{1}\)) of the two objective functions in (28) could be varied and some Pareto frontier could be computed to explore which weights are the realistic ones, see Kaya and Maurer (2014).

4 Dynamic portfolio model with two fluctuating assets

We present here an extension of the standard model of Sect. 2 in order to further study the impact of green and fossil fuel asset dynamics on investment decisions. The investors’ portfolio still rely on two assets, but we have now two assets with time-varying returns: a green and a fossil fuel one. In this exercise, the portfolio returns are obtained through harmonic estimations using a Fast Fourier Transform, as Chiarella et al. (2016, ch. 4). We use the annual monthly total returns in USD for the S &P Global BMI Energy, representing the fossil fuel sector, and for the Dow Jones Sustainability Global equity indices, representing the green sector, both available from April/2004 to May/2021. One objective in representing assets returns using current market data is to provide a theoretical background and a clearer perspective on future empirical work on the performance of portfolios (with climate externalities) that is of interest to finance practitioners.

The estimated harmonic oscillations for both assets – \(r_{green}^{e}(t)\) and \(r_{FF}^{e}(t)\) – are shown below and are later adjusted to account for the negative externality effects and social returns arising from green innovation. The new decision problem of a portfolio holder can be stated as follow

in which \(\omega _{t}\) is the share of green bonds in investors’ portfolio with \(\omega _{t}\le 1.2\), allowing thus fossil fuel divestment, while the green and fossil asset returns are respectively given by

Hereby, the fractions of wealth used for renewable energy innovations, \(\xi \), and the remaining part used for fossil fuel innovations will be taken as fixed with equal shares. Simulations could be undertaken with various fractions of \(\xi \). Innovation efforts, as in Sect. 2, impact asset returns through externality effects but, additionally, green assets will face lower volatility of returns, \(\phi _{1}=0.5\), and higher returns in the long-run (\(\phi _{2}\) is a mean-adjustment term that represents the positive impact of externalities which will be varied in our simulations). The adjusted harmonic estimation returns for the constant \(\phi _{2}\) equals to 0.034, 0.024 and 0.0 are shown in Fig. 7.

Returns for green (reg) and fossil fuel assets (rec): harmonic estimations after adjusting for externality effects for different levels of \(\phi _{2}\)

We select the harmonic estimations that minimize the squared root error, employing various linear combinations of sine-cosine functions (see equations bellow and Fig. 8).

Original harmonic estimations obtained to fossil fuel (S &P Global BMI Energy) and green (Dow Jones Sustainability Global Index) assets

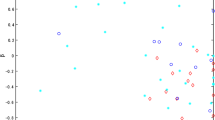

The harmonic estimations shown in Fig. 8 are adjusted for the externality term, driving investors’ portfolio choice. Asset returns are extremely volatile but, from Fig. 9, we observe that investors tend to diversify and increase the share of green assets whenever green assets’ returns are larger than fossil fuel asset returns, mitigating the negative effects of climate transition, see Figs. 9 and 10.

Portfolio decision - share of green assets for the cases with \(\phi _{2}=0.034\), \(\phi _{2}=0.024\), and \(\phi _{2}=0\)

We obtain the portfolio model’s numerical solutions for the three simulations of \(\phi _{2}\) also using NMPC as a solution procedure. We use a parameter value \(\mu =0.2\). In Fig. 10, the lowest curve represents the effect with a parameter \(\phi _{2}=0\), the middle graph is for \(\phi _{2}=0.024\) and the upper curve for \(\phi _{2}=0.034\). The greater the positive externality effect, the more wealth is accumulated overtime. Negative externalities are likely to lead to less asset built up, but more specifically to dissipating asset value in the long run. Innovation efforts and the positive externalities from climate investments protect financial markets from long-term climate risks.

Solutions path of wealth for different asset returns, the upper graph with \(\phi _{2}=0.034\), middle graphs with \(\phi _{2}=0.024\) and lowest graph \(\phi _{2}=0.0\) (N=6, T=100)

Each solution path shown in Fig. 10 is associated with a portfolio composition choice. When investors hold a larger share of green assets, the negative effects of the carbon externality tend to be mitigated.

5 Conclusion

In this paper we analyzed the potential implications of short-termism on the dynamic consumption-investment decisions of investors and their impact on green investments. We first employ a simple inter-temporal choice model that contains two assets, one equity asset with fluctuating returns and another asset with constant risk-free return. Equity returns are represented by low frequency movements, which we approximated with appropriate sine-wave functions—which are then later estimated as harmonic estimations in Sect. 4 using actual market data. We studied the effect of short-termism by varying three main drivers; namely, risk-aversion, the discount rate, and the decision horizon.

In the baseline model with one decision variable in the utility function, namely consumption, the numerical results showed that with higher discount rates (an investor exhibiting a high level of impatience), investments with lower present value (PV) tend to be more often discarded. In addition to the level of discount rate, the type of discount factor can also impact the evolution of wealth. With a time-inconsistent discount factor (a hyperbolic discount factor), numerical results showed that wealth tends to decline even faster than with discounting with exponential discount factor, due to a higher consumption rate in the beginning of the time horizon. Finally, we vary the decision horizon, N, and show that the smaller the decision horizon the lower is wealth accumulation over time, thus supporting the assumption that short-termism affect negatively the value of the portfolio over the long-run.

We extend the model to include a second decision variable in the objective function, where the investor decides to spend also a fraction of her wealth in innovation efforts, which could create positive or negative external effects. An extension that is in line with the previous work of Acemoglu et al. (2012) on directed technical change in endogenous growth models, exploring the positive external effects. We also explore a model version with negative external effects from innovation efforts. In those two versions of the model, we look into the effects of time varying returns and decision horizons on the consumption-wealth ratio and the fate of wealth. Finally, in a further extension of the model, we estimate the fluctuation of returns through harmonic estimations and use them in a dynamic portfolio model with two productive assets. A stochastic version, though of simplified form, is also explored.

Detailing what short-termism is in the context of a model of dynamic portfolio decisions, for an economy that aims at a better mix of fossil fuel and renewable energy, may point to better pathways for empirical work. In addition, the numerical method we are proposing (NMPC) is of great practical use: the prediction-control mechanism of finite horizon permits the decision maker to undertake some on-line strategy where assets are re-allocated when new information is coming in from the market. Given the new information, the harmonic estimations could be updated through the numerical algorithm triggering a change in asset allocations. So our approach may have significant importance for financial practitioners in the future.

Notes

See Gómez et al. (2010).

We employ a quadratic adjustment cost function for technical suitability, but empirical studies show that adjustment costs can be convex or at least quadratic, (Cochrane, 1991; Engle & Ferstenberg, 2007). Other works in the literature assume different types of transaction costs; for instance linear or fixed (Lobo et al., 2007)

\(\varepsilon _{1}\) and \(\varepsilon _{2}\) are weights determining the importance of intermediate consumption and terminal wealth in the utility of the investor.

See Greiner et al. (2005, chs. 4–5).

We could also think of the sign \(``-''\) as indicating that the the fossil fuel subsidies are reduced and thus the return on fossil fuel asset would fall.

In the numerical model, time t is considered a state variable as well, where \({\dot{x}}_{2}=1\)

See Faulwasser and Grüne (2022) for more on turnpike properties and their use in the NMPC context

Note that as is proven (Grüne et al., 2015) the large enough decision horizon and receding periods will make the project’s PV as computed here for the finite horizon approximating the infinite horizon solution.

With the NMPC algorithm it is possible to solve for optimal investment policies taking into account that a shock can occur at a random period.

References

Acemoglu, D., Aghion, P., Bursztyn, L., & Hemous, D. (2012). The environment and directed technical change. American Economic Review, 102(1), 131–166.

Andrikopoulos, P. & Webber, N. (2019). Understanding time-inconsistent heterogeneous preferences in economics and finance: a practice theory approach. Annals of Operations Research, pp. 1–24.

Attig, N., Cleary, S., Ghoul, S. E., & Guedhami, O. (2012). Institutional investment horizon and investment cash flow sensitivity. Journal of Banking & Finance, 36(4), 1164–1180.

Blomberg, S. P., Rathnayake, S. I., & Moreau, C. M. (2020). Beyond brownian motion and the ornstein-uhlenbeck process: Stochastic diffusion models for the evolution of quantitative characters. The American Naturalist, 195(2), 145–165.

Broer, D. P., & Jansen, W. J. (1998). Dynamic portfolio adjustment and capital controls: A euler equation approach. Southern Economic Journal, 64, 902.

Bushee, B. J. (2001). Do institutional investors prefer near-term earnings over long-run value? Contemporary Accounting Research, 18(2), 207–246.

Carney, M. (2015). The challenge of central banking in a democratic society. Speech given by Mark Carney former Governor of the Bank of England Chairman of the Financial Stability Board.

Cella, C., Ellul, A., & Giannetti, M. (2013). Investors’ horizons and the amplification of market shocks. The Review of Financial Studies, 26(7), 1607–1648.

Chaudhuri, S. E. & Lo, A. W. (2015). Spectral analysis of stock-return volatility, correlation, and beta. In 2015 IEEE signal processing and signal processing education workshop (SP/SPE) (pp. 232–236). IEEE.

Chen, X., Harford, J., & Li, K. (2007). Monitoring: Which institutions matter? Journal of Financial Economics, 86(2), 279–305.

Chiarella, C., Semmler, W., Hsiao, C.-Y., & Mateane, L. (2016). Sustainable asset accumulation and dynamic portfolio decisions. Berlin: Dynamic modeling and econometrics in economics and finance, Springer.

Cochrane, J. H. (1991). Production-based asset pricing and the link between stock returns and economic fluctuations. The Journal of Finance, 46(1), 209–237.

Cochrane, J. H. (2011). Presidential address: Discount rates. Journal of Finance, 66, 1047–1108.

Cochrane, J. H. (2021). Portfolios for long-term investors*. Review of Finance, 26(1), 1–42.

Cox, J. C., Ingersoll, J. E., & Ross, S. A. (1985). A theory of the term structure of interest rates. Econometrica, 53, 385–407.

Cremers, M., & Pareek, A. (2015). Short-term trading and stock return anomalies: Momentum, reversal, and share issuance. Review of Finance, 19(4), 1649–1701.

Créti, A., Ftiti, Z., & Guesmi, K. (2014). Oil price and financial markets: Multivariate dynamic frequency analysis. Energy Policy, 73, 245–258.

Davies, R., Haldane, A. G., Nielsen, M., & Pezzini, S. (2014). Measuring the costs of short-termism. Journal of Financial Stability, 12, 16–25.

Dong, Y. & Sircar, R. (2014). Time-inconsistent portfolio investment problems. In Springer proceedings in mathematics & statistics (pp. 239–281). Springer International Publishing.

Edelen, R., Evans, R., & Kadlec, G. (2013). Shedding light on invisible costs: Trading costs and mutual fund performance. Financial Analysts Journal, 69(1), 33–44.

Elster, J., & Loewenstein, G. (1992). Choice over time. Russell Sage Foundation.

Elyasiani, E., & Jia, J. (2010). Distribution of institutional ownership and corporate firm performance. Journal of Banking & Finance, 34(3), 606–620.

Engle, R. F., & Ferstenberg, R. (2007). Execution risk. The Journal of Trading, 2(2), 10–20.

Faulwasser, T., & Grüne, L. (2022). Chapter 11 - turnpike properties in optimal control: An overview of discrete-time and continuous-time results. In E. Trélat & E. Zuazua (Eds.), Numerical control: Part A, volume 23 of handbook of numerical analysis (pp. 367–400). Elsevier.

Gabaix, X., & Laibson, D. I. (2017). Myopia and discounting. Microeconomics General Equilibrium & Disequilibrium Models of Financial Markets eJournal.

Gennotte, G. (1986). Optimal portfolio choice under incomplete information. Journal of Finance, 41, 733–746.

Gómez, G., Mondelo, J. M., & Simó, C. (2010). A collocation method for the numerical fourier analysis of quasi-periodic functions. i: Numerical tests and examples. Discrete and Continuous Dynamical Systems-series B, 14, 41–74.

Greiner, A., Semmler, W., & Gong, G. (2005). The forces of economic growth. Princeton University Press.

Grüne, L. & Pannek, J. (2011). Nonlinear model predictive control: Theory and algorithms. Springer International Publishing.

Grüne, L., Semmler, W., & Stieler, M. (2015). Using nonlinear model predictive control for dynamic decision problems in economics. Journal of Economic Dynamics and Control, 60, 112–133.

Guo, Z. (2013). Horizon goals and risk taking in mutual funds. SSRN Electronic Journal.

Iacobucci, A. (2005). Spectral analysis for economic time series. In New tools of economic dynamics (pp. 203–219). Springer.

Kaya, C. Y., & Maurer, H. (2014). A numerical method for nonconvex multi-objective optimal control problems. Computational Optimization and Applications, 57, 685–702.

Keim, D. A., Nietzschmann, T., Schelwies, N., Schneidewind, J., Schreck, T., & Ziegler, H. (2006). A spectral visualization system for analyzing financial time series data. In EuroVis.

Liao, S., Nolte, I., & Pawlina, G. (2020). Can capital adjustment costs explain the decline in investment-cash flow sensitivity? Macroeconomics Aggregative Models eJournal.

Lobo, M. S., Fazel, M., & Boyd, S. P. (2007). Portfolio optimization with linear and fixed transaction costs. Annals of Operations Research, 152, 341–365.

Loewenstein, G., & Prelec, D. (1993). Preferences for sequences of outcomes. Psychological Review, 100, 91–108.

Merton, R. C. (1971). Optimum consumption and portfolio rules in a continuous-time model. Journal of Economic Theory, 3(4), 373–413.

Merton, R. C. (1973). An intertemporal capital asset pricing model. Econometrica, 41(5), 867–887.

Nystrup, P., Boyd, S. P., Lindström, E., & Madsen, H. (2019). Multi-period portfolio selection with drawdown control. Annals of Operations Research (pp. 1–27).

Phelan, C. E., Marazzina, D., Fusai, G., & Germano, G. (2019). Hilbert transform, spectral filters and option pricing. Annals of Operations Research, pp. 1–26.

Rappaport, A. (2005). Perspectives: The economics of short-term performance obsession. Financial Analysts Journal, 61(3), 65–79.

Semmler, W., Maurer, H., & Bonen, T. (2021). Financing climate change policies: A multi-phase integrated assessment model for mitigation and adaptation, pp. 137–158. Springer International Publishing.

Tobin, J. (1958). Liquidity preference as behavior towards risk. The Review of Economic Studies, 25, 65–86.

Tsay, R. S. (2010). Analysis of financial time series. Wiley.

Warren, G. (2014). Long-term investing: What determines investment horizon? SSRN Electronic Journal.

Zou, Z., Chen, S., & Wedge, L. (2014). Finite horizon consumption and portfolio decisions with stochastic hyperbolic discounting. Journal of Mathematical Economics, 52, 70–80.

Funding

Open Access funding enabled and organized by Projekt DEAL. This study was supported by the German Federal Ministry of Education and Research (BMBF) as part of the FINFAIL project [grant no. 01LN1703A], which is gratefully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

NMPC subroutine algorithm

NMPC subroutine algorithm

To account for a shock affecting the asset returns at a random time, we augment the NMPC algorithm using a set up, similar to the multi-phase dynamcics as in Semmler et al. (2021). In our model, we assume a shock affects the parameter \(\alpha _{1}\) in (\(8^\prime \)), changing the amplitude of the return process, at a random time.

We use a concrete example for the number of iterations and create random time events. The sub-routine generates random time in an ascending order. Then let the random process, as sub-routine, determine the random event time for the switch of the coefficient \(\alpha _{1}\) in the NMPC algorithm. Using a running time index in the NMPC program as \(2^\text {nd}\) state variable we can write: \({\dot{x}}_{2}=1\), which represents our running time index. Then the above random time sequence triggers the switch of the coefficient \(\alpha _{1}\), with a certain size, in the NMPC solution program. This way the amplitude of our return fluctuations is randomly fluctuating, possibly capturing the new information coming in at random time when time moves forward. Below is a summary of the routine we described.

Note that for example the entry y(8, 1), is used in our simulation of Fig. 3. Yet the entry represents a random time at which we have a switching coefficient \(\alpha _{1}\). This is so, because iterating forward what will be the exact time index at the the place 8 is completely random. The results give us Fig. 3. Yet, for a one shock simulation, as in Fig. 3, any other entry y(., 1) could be used to generate a random switch time. We could have also multiple random time changes of \(\alpha _{1}\). The graph would then look much more complex than Fig. 3. Thus, to illustrate our procedure we have used in Fig. 3 a simple presentation, namely using a one-time coefficient shock at random time. Moreover, we could also, in addition, introduce a sub-routine that make the size of the shock \(\alpha _{1}\) random. Those complications are not implemented here but could with some additional programming effort, also be addressed.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Semmler, W., Lessmann, K., Tahri, I. et al. Green transition, investment horizon, and dynamic portfolio decisions. Ann Oper Res 334, 265–286 (2024). https://doi.org/10.1007/s10479-022-05018-2

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-022-05018-2