Abstract

We provide a Bayesian panel model to consider persistence in US funds’ performance while we tackle the important problem of errors in variables. Our modelling departs from prior strong assumptions such as error terms across funds being independent. In fact, we provide a novel, general Bayesian model for (dynamic) panel data that is stable across different priors as reported from the mapping of the prior to the posterior of the Bayesian baseline model with the adoption of different priors. We demonstrate that our model detects previously undocumented striking variability in terms of performance and persistence across funds categories and over time, and in particular through the financial crisis. The reported stochastic volatility exhibits a rising trend as early as 2003–2004 and could act as an early warning of future crisis.

Similar content being viewed by others

Notes

Kempf and Ruenzi (2008) study the competition between fund managers across funds’ family. They argue that an optimal policy of fund managers is to alter their risk-taking. Studying US equity mutual funds between 1993 and 2001, they report the presence of the family tournament, which is more pronounced in large families.

Brown et al. (1996) identify that interim losers who underperform the benchmark in the first half of the year are likely to increase their risk relative to mid-year winners. Funds are ranked according to their cumulative return, while risk is measured by the ratio of fund’s standard deviation after the interim performance assessment to its standard deviation before that date. Another proxy for risk is the tracking error variance, which is the variance of the difference between fund’s return and the value-weighted market index (Chevalier and Ellison, 1997).

Initial conditions are treated as unknown parameters.

It is easy to show that the interpretation of γ and α goes through even when βs are time-varying.

Given the model of Eq. (4) the following applies: (i) we can allow for different temporal coefficients, \( \beta_{t} \), and (ii) we can allow for arbitrary patterns of autocorrelation, since we can assume: \( E\left( {v_{s} v_{t}^{\prime } } \right) = \varSigma_{st} , \, s,t \in \left\{ {1, \ldots ,T} \right\}. \) In addition, we allow for arbitrary autocorrelation and arbitrary forms of heteroskedasticity as well. This comes at the cost of allowing for \( \tfrac{T(T + 1)}{2} \) matrices of the form \( \varSigma_{\text{st}} \) each of which is \( n \times n \).

Regarding the elements of \( \varSigma_{ts} ,t \ne s \), since the prior belief is that these are all zero matrices, we can adopt a ‘model selection prior’ (see Koop 2013) of the form: \( \frac{{\sigma_{ij,t} }}{{\sqrt {\sigma_{ii,t} \sigma_{jj,t} } }} = \left\{ \begin{aligned} 0,{\text{ with probability }}p ,\hfill \\ \rho ,{\text{ with probability }}1 - p .\hfill \\ \end{aligned} \right. \)

In this prior we set \( p = \tfrac{1}{2} \) and we treat ρ as unknown parameter with a flat prior.

Regarding \( \varSigma_{tt} \) the diagonal elements, say \( \sigma_{ii,tt} \), allow for arbitrary time-varying heteroskedasticity while \( \sigma_{ij,tt} \) allows for contemporaneous correlation of returns. The matrix has received a great deal of attention in DCC and similar models. Suppose that: \( \varSigma_{tt} = H_{t} H^{\prime}_{t} , \) where \( H_{t} \) is an \( n \times n \) upper diagonal elements and its non-zero elements can be vectorized as: \( h_{t} = vec\left[ {h_{ij,t} ,i,j = 1, \ldots ,\tfrac{n(n + 1)}{2}} \right]. \) We proceed with a prior assuming that: \( h_{t} = a + Ah_{t - 1} + u_{t} , \) where α and Α have dimension \( \tfrac{n(n + 1)}{2} \times 1 \) and \( \tfrac{n(n + 1)}{2} \times \tfrac{n(n + 1)}{2} \), respectively, and the error term \( u_{t} \sim\,N\left( {0,\varPsi } \right). \) To determine a prior for Ψ we use the decomposition \( \varPsi = C_{\varPsi }^{\prime } C_{\varPsi } \) where \( C_{\varPsi } \) is an upper triangular matrix. Let \( c_{\varPsi } = vec(C_{\varPsi } ) \). Our prior is: \( c_{\varPsi } \sim\,N(\bar{c}_{\varPsi } ,\bar{V}_{\varPsi } ). \) In effect, we place a multivariate stochastic volatility prior. Although we have high dimensional objects α and Α, we can proceed with priors to resolve the curse of dimensionality: \( a\sim\,N(\bar{a},\bar{V}_{a} ),vec(A)\sim\,N\left( {\bar{A},\bar{V}_{A} } \right). \).

Moreover, the 5 factors come from Fama and French (2014) and defined as SMB(B/M) = 1/3 (Small Value + Small Neutral + Small Growth) − 1/3 (Big Value + Big Neutral + Big Growth), SMB(OP) = 1/3 (Small Robust + Small Neutral + Small Weak) − 1/3 (Big Robust + Big Neutral + Big Weak), SMB(INV) = 1/3 (Small Conservative + Small Neutral + Small Aggressive) − 1/3 (Big Conservative + Big Neutral + Big Aggressive) and thus SMB = 1/3 (SMB(B/M) + SMB(OP) + SMB(INV)). HML = 1/2 (Small Value + Big Value) − 1/2 (Small Growth + Big Growth). RMW = 1/2 (Small Robust + Big Robust) − 1/2 (Small Weak + Big Weak). CMA = 1/2 (Small Conservative + Big Conservative) − 1/2 (Small Aggressive + Big Aggressive). Data include all NYSE, AMEX, and NASDAQ firms.

θ denotes the parameter vector, Y the data and L is the likelihood. Also, p(θ) is the prior.

However, large funds may encounter some disadvantages in terms of liquidity and management (Chen et al., 2004; Pollet and Wilson, 2008). According to the organisational diseconomies hypothesis (Chen et al., 2004), fund size is inversely related to performance. This could be because of hierarchical costs, or management dilution when the fund expands. One manager can easily manage small assets, but it needs a team to manage a large asset base. Large funds would eventually trade large volumes, which may cause difficulties for them in opening and closing their positions. Hence, this liquidity constraint also explains why large funds could be associated with lower performance.

Empirical findings for the size-performance relationship are somewhat mixed. While Chen et al. (2004), Huang et al. (2011) and Ferreira et al. (2012) find a presence of diseconomies of scale, Pollet and Wilson (2008) report that large funds tend to diversify their portfolios which in turn increases their performance. Jordan and Riley (2015) report a positive effect of small size on fund’s future alpha. Regressing future alpha on past alpha and size, Elton et al. (2012) do not find a statistically significant predictability of size on future alpha. However, they document that as size increases, expense ratios and management fees decrease.

Funds report turnover ratio by taking the lesser of purchases or sales of all securities with maturities from one year and dividing it by the average monthly net assets. The lower the turnover ratio, the more the fund is in favor of the buy-and-hold strategy. Stated differently, high turnover ratio indicates active portfolio management strategies (Daraio and Simar 2006; Khorana and Servaes 2012). As a result, active fund managers classified based on high turnover ratios may induce higher performance.

However, there is some evidence that shows that 12b-1 fee can raise expenses that would eventually compromise performance.

Figure of the posterior distribution of αis conditional on a ‘significant’ γit, that is the ratio of posterior mean to posterior standard deviation exceeds 2 in absolute value shows that persistence predominantly leans towards negative values (figure available under request).

For completeness we present in Table 11 in “Appendix 2” the performance of ten average funds. In addition, in “Appendix 2” we provide figures for posterior distributions for 10 best/worst funds as well as 10 average funds. Note that we also include Fig. 11 that reports posterior distributions of for the best-performing fund for years 2000, 2008, 2012 and 2014.

In addition, results are available under request of posterior distributions obtained through 20 different priors from the last column in Table 1 to examine prior sensitivity. These results provide evidence of the performance for the ten best (worst) funds and are in line with the evidence herein.

The posterior distribution of optimal portfolio P is presented in Fig. 12 and the posterior distribution of average persistence of its component returns is presented in Fig. 13, for 50 different priors from the last column in Table 1. In Fig. 14, we report the posterior distribution of its persistence only when average persistence of its component returns is ‘significant’ (viz. the ratio of posterior mean to posterior S.D. exceeds 2 in absolute value).

References

American Statistical Association. (2016). Statement on p-values, context, process, and purpose, ASA (Vol. 70(2)). Alexandria: American Statistical Association.

Annaert, J., Van Den Broeck, J., & Vander Vennet, R. (2003). Determinants of mutual fund underperformance: A Bayesian stochastic frontier approach. European Journal of Operational Research, 151, 617–632.

Barber, D. (2012). Bayesian reasoning and machine learning. Cambridge: Cambridge University Press.

Basak, S., & Makarov, D. (2014). Strategic asset allocation in money management. The Journal of Finance, 69, 179–217.

Biørn, E. (2015). Panel data dynamics with mis-measured variables: Modeling and GMM estimation. Empirical Economics, 48, 517–535.

Blake, D., Caulfield, T., Ioannidis, C., & Tonks, I. (2014). Improved inference in the evaluation of mutual fund performance using panel bootstrap methods. Journal of Econometrics, 183(2), 202–210.

Blake, D., Caulfield, T., Ioannidis, C., & Tonks, I. (2017). New evidence on mutual fund performance: A comparison of alternative bootstrap methods. Journal of Financial and Quantitative Analysis, 52(3), 1279–1299.

Brown, S. J., Goetzmann, W. N., & Park, J. (2001). Careers and survival: Competition and risk in the hedge fund and CTA industry. The Journal of Finance, 56, 1869–1886.

Brown, K. C., Harlow, W. V., & Starks, L. T. (1996). Of tournaments and temptations: An analysis of managerial incentives in the mutual fund industry. Journal of Finance, 51, 85–110.

Busse, J. A. (2001). Another look at mutual fund tournaments. Journal of Financial and Quantitative Analysis, 36, 53–73.

Cabello, J. M., Ruiz, F., Pérez-Gladish, B., & Méndez-Rodriguez, P. (2014). Synthetic indicators of mutual funds’ environmental responsibility: An application of the reference point method. European Journal of Operational Research, 236(1), 313–325.

Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal of finance, 52, 57–82.

Casarin, R., & Marin, J.-M. (2009). Online data processing: Comparison of Bayesian regularized particle letters. Electronic Journal of Statistics, 3, 239–258.

Chen, J., Hong, H., Huang, M., & Kubik, J. D. (2004). Does fund size erode performance? Organizational diseconomies and active money management. American Economic Review, 94, 1276–1302.

Chen, J., Hong, H., Jiang, W., & Kubik, J. D. (2013). Outsourcing mutual fund management: Firm boundaries, incentives, and performance. The Journal of Finance, 68, 523–558.

Chevalier, J., & Ellison, G. (1997). Risk taking by mutual funds as a response to incentives. The Journal of Political Economy, 105, 1167–1200.

Chopin, N. (2002). A sequential particle filter method for static models. Biometrika, 89(3), 539–551.

Chopin, N. (2004). Central limit theorem for sequential Monte Carlo methods and its application to Bayesian inference. Annals of Statistics, 32, 2385–2411.

Christoffersen, S. E., & Musto, D. K. (2002). Demand curves and the pricing of money management. Review of Financial Studies, 15, 1499–1524.

Cullen, G., Gasbarro, D., Monroe, G. S., & Zumwalt, J. K. (2012). Changes to mutual fund risk: Intentional or mean reverting? Journal of Banking & Finance, 36, 112–120.

Daraio, C., & Simar, L. (2006). A robust nonparametric approach to evaluate and explain the performance of mutual funds. European Journal of Operational Research, 175, 516–542.

Durham, G., & Geweke, J. (2013). Adaptive sequential posterior simulators for massively parallel computing environments. Working paper.

Elton, E. J., Gruber, M. J., & Blake, C. R. (2012). Does mutual fund size matter? The relationship between size and performance. Review of Asset Pricing Studies, 2, 31–55.

Fama, E. F., & French, K. R. (2010). Luck versus skill in the cross-section of mutual fund returns. The Journal of Finance, 65, 1915–1947.

Fama and French. (2014). A five-factor asset pricing model. Working paper. Available at SSRN. http://ssrn.com/abstract=2287202.

Farrell, M. J. (1957). The measurement of productive efficiency. Journal of the Royal Statistical Society, 120, 253–290.

Ferreira, M. A., Keswani, A., Miguel, A. F., & Ramos, S. B. (2012). The determinants of mutual fund performance: A cross-country study. Review of Finance, 17, 483–525.

Ferris, S. P., & Chance, D. M. (1987). The effect of 12b–1 plans on mutual fund expense ratios: A note. The Journal of Finance, 42(4), 1077–1082.

Ferson, W., & Lin, Jerchern. (2014). Alpha and performance measurement: The effects of investor disagreement and heterogeneity. Journal of Finance, 69(4), 1565–1596.

Ferson, W., & Mo, H. (2016). Performance measurement with selectivity, market and volatility timing. Journal of Financial Economics, 121(1), 93–110.

Gil-Bazo, J., & Ruiz-Verdú, P. (2008). When cheaper is better: Fee determination in the market for equity mutual funds. Journal of Economic Behavior & Organization, 67, 871–885.

Gil-Bazo, J., & Ruiz-Verdú, P. (2009). The relation between price and performance in the mutual fund industry. The Journal of Finance, 64, 2153–2183.

Gilks, W. R., & Berzuini, C. (2001). Following a moving target: Monte Carlo inference for dynamic Bayesian models. Journal of the Royal Statistical Society B, 63, 127–146.

Giuzio Kay, M., Eichhorn-Schott, K., Paterlini, S., & Weber, V. (2018). Tracking hedge funds returns using sparse clones. Annals of Operations Research, 266(1–2), 349–371.

Goriaev, A., Nijman, T. E., & Werker, B. J. (2005). Yet another look at mutual fund tournaments. Journal of Empirical Finance, 12, 127–137.

Gruber, M. J. (1996). Another puzzle: The growth in actively managed mutual funds. The Journal of Finance, 51, 783–810.

Hayakawa, K., & Qi, M. (2019). Further results on the weak instruments problem of the system GMM estimator in dynamic panel data models. Oxford Bulletin of Economics and Statistics, 82, 453–481.

Hsiao, C., Pesaran, M. H., & Tahmiscioglu, A. K. (1999). Bayes estimation of short-run coefficients in dynamic panel data models. In C. Hsiao et al. (Eds.), Analysis of panels and limited dependent variable models: In honor of G.S. Maddala (pp. 268–296). Cambridge: Cambridge University Press.

Huang, J., Sialm, C., & Zhang, H. (2011). Risk shifting and mutual fund performance. Review of Financial Studies, 24(8), 2575–2616.

Huang, J., Wei, K. D., & Yan, H. (2007). Participation costs and the sensitivity of fund flows to past performance. The Journal of Finance, 62, 1273–1311.

Jensen, M. C. (1968). The performance of mutual funds in the period 1945–1964. Journal of Finance, 23, 389–416.

Jordan, B. D., & Riley, T. B. (2015). Volatility and mutual fund manager skill. Journal of Financial Economics, 118, 289–298.

Kempf, A., & Ruenzi, S. (2008). Tournaments in mutual-fund families. Review of Financial Studies, 21, 1013–1036.

Khorana, A., & Servaes, H. (2012). What drives market share in the mutual fund industry? Review of Finance, 16, 81–113.

Koop, Gary. (2013). Forecasting with medium and large Bayesian VARs. Journal of Applied Econometrics, 28, 177–203.

Koop, G., & Poirier, D. J. (2004). Bayesian variants of some classical semi-parametric regression techniques. Journal of Econometrics, 123(2), 259–282.

Koopmans, T. (1951). Activity analysis of production and allocation. New York: Wiley.

Koski, J. L., & Pontiff, J. (1999). How are derivatives used? Evidence from the mutual fund industry. Journal of Finance, 54, 791–816.

Latzko, D. A. (1999). Economies of scale in mutual fund administration. Journal of Financial Research, 22, 331–339.

Lunde, A., Timmermann, A., & Blake, D. (1999). The hazards of mutual fund underperformance: A cox regression analysis. Journal of Empirical Finance, 6, 121–152.

Malhotra, D., Martin, R., & Russel, P. (2007). Determinants of cost efficiencies in the mutual fund industry. Review of Financial Economics, 16, 323–334.

Mamaysky, H., & Spiegel, M. (2002). A theory of mutual funds: Optimal fund objectives and industry organization. Working paper, Yale University.

Pollet, J. M., & Wilson, M. (2008). How does size affect mutual fund behavior? The Journal of Finance, 63, 2941–2969.

Rossello, D. (2015). Ranking of investment funds: Acceptability versus robustness. European Journal of Operational Research, 245(3), 828–836.

Sato, Y. (2015). Fund tournaments and asset bubbles. Review of Finance, 20, 1383–1426.

Spiegel, M., & Zhang, H. (2013). Mutual fund risk and market share-adjusted fund flows. Journal of Financial Economics, 108, 506–528.

Utz, S., Wimmer, M., & Steuer, R. E. (2015). Tri-criterion modelling for constructing more-sustainable mutual funds. European Journal of Operational Research, 246(1), 331–338.

Vidal-García, Javier, Vida, Marta, Boubaker, Sabri, & Hassan, Majdi. (2018). The efficiency of mutual funds. Annals of Operations Research, 267(1–2), 555–584.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1: Sequential Monte Carlo/particle-filtering (SMC/PF) techniques

Chopin (2002) proposed a sequential PF for static models. Given a target posterior \( p(\theta |Y): = p(\theta |Y_{1:T} ) \) a particle system is a sequence \( \{ \theta_{j} ,w_{j} \} \) such that \( E(h(\theta )|Y): = \smallint h(\theta )p(\theta |Y)d\theta \cong lim_{J \to \infty } \tfrac{{\sum\nolimits_{j = 1}^{J} \,w_{j} h(\theta_{j} )}}{{\sum\nolimits_{j = 1}^{J} \,w_{j} }} \), almost surely, for any measurable function \( h \), provided the expectation exists. We consider the sequence of posterior distributions \( p_{t} : = p(\theta |Y_{t} ) \). The PF algorithm is as follows.

Step 1: Reweight: update the weights \( w_{j} \leftarrow w_{j} \tfrac{{p_{t + 1} (\theta_{j} )}}{{p_{t} (\theta_{j} )}},j = 1, \ldots ,J \).

Step 2: Resampling: resample \( \{ \theta_{j} ,w_{j} J_{j = 1}^{H} \to \{ \theta_{j}^{r} ,1\}_{j = 1}^{J} \).

Step 3: Move: draw \( \theta_{j}^{m} \sim \,K_{t + 1} (\theta_{j}^{r} ),j = 1, \ldots ,J \), where \( K_{t + 1} \) is any transition kernel whose stationary distribution is \( p_{t + 1} . \)

Step 4: Loop: \( t \leftarrow t + 1,\{ \theta_{j} ,w_{j} \}_{j = 1}^{J} \leftarrow \{ \theta_{j}^{m} ,1\}_{j = 1}^{J} \) and return to Step 1.

Chopin (2002) recommends the independence Metropolis algorithm to select the kernel, which requires a source distribution. A possible choice, if we sampled from \( p_{n} \) (n < T), with respect to \( p_{n + s} \) is \( N(\mathop {\hat{E}}\nolimits_{n + s} ,\mathop {\hat{V}}\nolimits_{n + s} ) \) where

The strategy can be parallelized easily. If K processors are available, we can partition the particle system into K subsets, say \( S_{k} ,k = 1, \ldots ,K) \), and implement computations for particles of \( S_{k} \) in processor k. The algorithm can deal with new data at a nearly geometric rate and therefore the frequency of exchanging information between processors (after reweighting) decreases at a rate exponential to n, which is highly efficient.

Resampling according to \( \theta_{j}^{m} \sim \,K_{t} (\theta_{j}^{r} ,.) \) reduces particle degeneracy (Gilks and Berzuini 2001) since identical replicates of a single particle are replaced by new ones without altering the stationary distribution. For this application using \( J = 2^{12} \) particles gave a mean squared error in posterior means of 10−5 over 100 runs.

Chopin (2004) introduces a variation of MSC in which the observation dates at which each cycle terminates (say \( t_{1} , \ldots ,t_{L} ) \) and the parameters involved in specifying the Metropolis updates (say \( \lambda_{1} , \ldots ,\lambda_{L} ) \) are specified. Therefore, \( 0 = t_{0} < t_{1} < \cdots < t_{L} = T \) and we have the following scheme (we rely heavily on Durham and Geweke 2013).

Step 1: Initialize \( l = 0 \) and \( \theta_{jn}^{(l)} \sim p(\theta ) \), \( j \in J,n \in N \).

Step 2: For \( l = 1, \ldots ,L \):

(a) Correction phase:

(i) \( w_{jn} (t_{l - 1} ) = 1,\:j \in J,n \in N \)

(ii) For \( s = t_{l - 1} + 1, \ldots ,t_{l} \)

(iii) \( w_{jn}^{(l - 1)} : = w_{jn} (t_{l} ),\:j \in J,n \in N. \)

(b) Selection phase, applied independently to each group \( j \in J \) : Using multinomial or residual sampling based on \( \left\{ {w_{jn}^{(l)} ,n \in N} \right\} \), select

from \( \{ \theta_{jn}^{(l - 1)} ,n \in N\} \).

(c) Mutation phase, applied independently across \( j \in J,n \in N \):

where the drawings are independent and the pdf above satisfies the invariance condition:

Step 3. \( \theta_{jn} : = \theta_{jn}^{(l)} ,\:j \in J,n \in N. \)

At the end of every cycle, the particles \( \theta_{jn}^{(l)} \) have the same distribution \( p(\theta |y_{{1:t_{l} }} ). \) The amount of dependence within each group depends upon the success of the Mutation phase which avoids degeneracy.

Appendix 2

See Table 11 and Figs. 7, 8, 9, 10, 11, 12, 13 and 14.

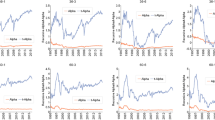

Posterior distributions of \( \gamma_{it} \) s (performance): a 10 best funds, b 10 worst funds. c 10 average funds

Posterior distributions of \( \gamma_{it} \) for the best-performing fund for years 2000, 2008, 2012 and 2014. Note The posterior distributions are obtained with Sequential Monte Carlo/Particle Filtering draws. We have used 15,000 draws the first 5000 of which are discarded to mitigate possible start up effects

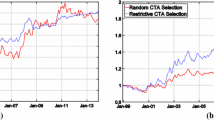

The posterior distribution of optimal portfolio. Note The diagram presents results for 20 different priors from the last column in Table 1

Marginal posterior distribution of average persistence (\( \alpha_{i} \)) of its component returns. Note 50 different priors from the last column in Table 1

Marginal posterior distribution of persistence when average persistence is ‘significant’. Note 50 different priors from the last column in Table 1

Marginal posterior distributions of αi for each fund only when its average turns out ‘significant’. Note 50 different priors from the last column in Table 1

Rights and permissions

About this article

Cite this article

Mamatzakis, E., Tsionas, M.G. Testing for persistence in US mutual funds’ performance: a Bayesian dynamic panel model. Ann Oper Res 299, 1203–1233 (2021). https://doi.org/10.1007/s10479-020-03691-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-020-03691-9