Abstract

In this paper we analyze a model which addresses two stylized facts which have received little attention in disclosure theory. (a) Information that is acquired for internal decision-making can subsequently be disclosed to outside investors who can use it to update their assessment of the firm’s prospects. Thus, the decision to gather information in the first place does not only depend on the decision value of information. (b) Information disclosed by firms is only one element of the information environment upon which investors can draw. This setting creates an interaction between firms’ information gathering and disclosure decisions as well as alternative sources of information. We identify an equilibrium structure which we call a Countersignaling equilibrium in which only average firms acquire information whereas good and bad firms do not. We show that while several equilibria can coexist, a Countersignaling equilibrium is often the economically most efficient one.

Similar content being viewed by others

Notes

The assumption that the outcome is perfectly predictable is rather strong and not necessary for the model’s results. It suffices to assume that the information is valuable which means that the expected value after observing the information might be different from the a priori expected value and can be negative. The assumption that the acquisition of the information is always observable is relaxed in the extension.

While arguably incentives to manage earnings are present in our setting, we note that results of disclosure models have been shown to be robust to the abandonment of the truthful reporting assumption (Einhorn and Ziv 2012).

Note that the (arguably unrealistic) assumption of perfect accuracy is not driving the results of our model. It only serves the purpose of simplifying exposition and making the drivers of our results more transparent.

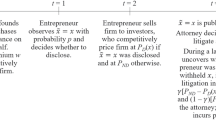

Only if his decision has no direct influence on the market price, he selects the strategy which is best for increasing firm value (lexicographic preference).

This result is based on the assumption that disclosure is costless, investors know that manager has information, manager can credible disclose their information, manager wants to maximize firm value, investors are rational and do not have private information and manager cannot commit ex ante to a disclosure policy. If this is the case than observing no disclosure will be interpreted as a bad signal about manager’s information leading to a low market price. All managers who know that their firm is valued higher than this price would disclose their information. Thus, in equilibrium only the manager with the worst information would be indifferent between disclosing and withholding.

The first inequality follows from (8) the others from the assumption of stochastic dominance.

The out of equilibrium believes are defined in the Appendix.

The proof of Theorem 3 as well as a pairwise comparison between all equilibria is located in the Appendix.

The costs have to be higher than \(\frac{1}{2} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_A \left( x \right) dx\) for the Countersignaling equilibrium and higher than \(\frac{1}{3} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_B \left( x \right) +F_A \left( x \right) dx\) for the Pooling equilibrium, \(M=\{\}\).

The setting and proofs are given in the Appendix.

From now on we assume that the costs are sufficiently small, \(K+t_b <\overline{x}\).

References

Araujo A, Gottlieb D, Moreira H (2007) A model of mixed signals with applications to countersignaling. Rand J Econ 38(4):1020–1043

Arya A, Glover J (2003) Abandonment option and information system design. Rev Acc Stud 8(1):29–45

Bagnoli M, Watts SG (2007) Financial reporting and supplemental voluntary disclosures. J Acc Res 45(2):885–913

Beyer A, Cohen DA, Lys TZ, Walther BR (2010) The financial reporting environment: review of the recent literature. J Acc Econ 50:296–343

Brocas I, Carillo JD (2007) Influence through ignorance. RAND J Econ 38(4):931–947

Chung KS, Esö P (2007) Signalling with Career Concerns. Working Paper, University of Hong Kong

Church BK, Hannan RL, Kuang X (2014) Information acquisition and opportunistic behavior in managerial reporting. Contemp Acc Res (forthcoming)

Clements MT (2011) Low quality as a signal of high quality. Economics 5:1–22

Demski JS, Feltham GA (1976) Cost determination: a conceptual approach. Iowa State University Press, Ames

Dye R (1985) Disclosure of nonproprietary information. J Acc Res 23(1):123–145

Einhorn E (2005) The nature of the interaction between mandatory and voluntary disclosures. J Acc Res 43(4):593–621

Einhorn E (2007) Voluntary disclosure under uncertainty about the reporting objective. J Acc Econ 43 (2–3):245–274

Einhorn E, Ziv A (2007) Unbalanced information and the interaction between information acquisition, operating activities, and voluntary disclosure. Acc Rev 82(5):1171–1194

Einhorn E, Ziv A (2012) Biased voluntary disclosure. Rev Acc Stud 17(2):420–442

Favaro K, Karlsson PO, Neilson GL (2010) CEO succession 2000–2009: a decade of convergence and compression. Strateg Bus 59:1–14

Feltham GA (1968) The value of information. Acc Rev 43(4):684–696

Feltham GA, Demski Joel S (1970) The use of models in information evaluation. Acc Rev 45(4):623–640

Feltovich N, Harbaugh R, To T (2002) Too cool for school? Signalling and countersignalling. Rand J Econ 33(4):630–649

Financial Executives Research Foundation (2009) Earnings guidance: the current state of play. http://www.corpgov.deloitte.com/binary/com.epicentric.contentmanagement.servlet.ContentDeliveryServlet/USEng/Documents/Board%20Governance/Short-%20and%20Long-termism/Earnings%20Guidance%20Current%20State%20of%20Play_Deloitte%20FERF_071309.pdf. Accessed 4 Nov 2013

Frantz P, Instefjord N (2006) Voluntary disclosure of information in a setting in which endowment of information has productive value. J Bus Financ Acc 33(5&6):793–815

Gao L, Li Z, Shou B (2014) Information acquisition and voluntary disclosure in an export-processing system. Prod Oper Manag (forthcoming)

Grossman SJ (1981) The informational role of warranties and private disclosure about product quality. J Law Econ 24:461–483

Grossman SJ, Hart OD (1980) Disclosure laws and takeover bids. J Financ 35(2):323–334

Healy PM, Palepu KG (2001) Information asymmetry, corporate disclosure, and the capital markets: a review of the empirical disclosure literature. J Acc Econ 31(1–3):405–440

Hope OK (2003) Disclosure practices, enforcement of accounting standards, and analysts’ forecast accuracy: an international study. J Acc Res 41(2):235–272

Horngren CT, Datar SM, Rajan MV (2012) Cost accounting. A managerial emphasis. Pearson Education, Harlow

Hvide HK (2003) Education and the allocation of talent. J Labor Econ 21(4):945–976

Jung WO, Kwon YK (1988) Disclosures when the market is unsure of information endowment of manager. J Acc Res 26(1):146–153

Li Z, Sun D (2012) Acquisition and disclosure of operational information. Decis Sci 43(3):459–487

Milgrom PR (1981) Good news and bad news: representation theorems and applications. Bell J Econ 17:380–391

Milgrom PR, Roberts J (1986) Relying on the information of interested parties. Rand J Econ 17(1):18–32

Orzach R, Tauman Y (2005) Strategic dropouts. Games Econ Behav 50(1):79–88

Orzach R, Overgaard PB, Tauman Y (2002) Modest advertising signals strength. RAND J Econ 33(2): 340–358

Pae S (1999) Acquisition and discretionary disclosure of private information and its implications for firms’ productive activities. J Acc Res 37(2):465–474

Pae S (2005) Selective disclosures in the presence of uncertainty about information endowment. J Acc Econ 39(3):383–409

Penno MC (1997) Information quality and voluntary disclosure. Acc Rev 72(2):275–284

Pfeiffer T, Schneider G (2007) Residual income-based compensation plans for controlling investment decisions under sequential private information. Manag Sci 53(3):495–507

Pfeiffer T, Schneider G (2010) Capital budgeting, information timing, and the value of abandonment options. Manag Acc Res 21(4):238–250

Rothenberg NR (2009) The interaction among disclosures, competition, and an internal control problem. Manag Acc Res 20(4):225–238

Scott WR (2012) Financial accounting theory, 6th edn. Pearson Prentice Hall, Toronto

Simons D, Weißenberger BE (2008) Die Konvergenz von externem und internem Rechnungswesen—Kritische Faktoren für die Entwicklung einer partiell integrierten Rechnungslegung aus theoretischer Sicht. Betriebswirtschaftliche Forschung und Praxis 60(2):137–160

Spence M (1973) Job market signaling. Q J Econ 87(3):355–374

Spence M (2002) Signaling in retrospect and the informational structure of markets. Am Econ Rev 92(3):434–459

Stocken PC (2013) Strategic accounting disclosure. Found Trends Acc 7(4):197–291

Suijs J (2007) Voluntary disclosure of information when firms are uncertain of investor response. J Acc Econ 43(2–3):391–410

Teoh SH, Hwang CY (1991) Nondisclosure and adverse disclosure as signals of firm value. Rev Financ Stud 4(2):283–313

Trapp R (2012) Konvergenz des internen und externen Rechnungswesens. Etablierung oder Auflösung eines Theorie-Praxis-Paradoxons? Zeitschrift für Betriebswirtschaft 82(9):969–1008

Verrecchia RE (1983) Discretionary disclosure. J Acc Econ 5:179–194

Verrecchia R (2001) Essays on disclosure. J Acc Econ 32(1–3):97–180

Wagenhofer A (1990) Voluntary disclosure with a strategic opponent. J Acc Econ 12(4):341–363

Wagenhofer A (2006) Management accounting research in German-speaking countries. J Manag Acc Res 18(1):1–19

Wagenhofer A, Ewert R (2007) Externe Unternehmensrechnung, 2nd edn. Springer, Berlin

Weißenberger BE, Angelkort H (2011) Integration of financial and management accounting systems: the mediating influence of a consistent financial language on controllership effectiveness. Manag Acc Res 22(3):160–180

Author information

Authors and Affiliations

Corresponding author

Additional information

The authors gratefully acknowledge helpful comments from Sabine Böckem, Tiago Pinheiro, Li Zhang, three anonymous referees as well as participants at the annual symposium of the German Economic Association for Business Administration 2011 in Zurich, the annual conference of the German Academic Association for Business Research 2012 in Bolzano, the International Accounting and Auditing Conference 2012 in Amsterdam, the Annual Congress of the European Accounting Association 2012 in Ljubljana, the EIASM Workshop on Accounting and Economics 2012 in Segovia and a research seminar at the University of Tilburg, 2013.

Appendix

Appendix

1.1 Proof of Theorem 2

The proof of this theorem can be done backwards. First we consider the prices (iii) in particular we look only at one, the price in the case of no acquisition of the information system and receiving good additional information. Given market beliefs of \(\Pr \left( {\left. j \right| g} \right) =\frac{q_j }{\sum \nolimits _{k\in N} {q_k } }\)for \(j\in N\) it is a rational decision to assess a firm in this case with \(P_N \left( {g,NIS} \right) \) given in (5). The same can be shown for \(P_N \left( {b,NIS} \right) \) in (6), \(P\left( {ND,g,IS} \right) =P\left( {ND,b,IS} \right) =-K\) and the price in the case of disclosure (2). Next, we analyze how the beliefs are formed. If a manager with a project type of \(j\in N\) always decides against an information system and a manager of type \(i\in M\) chooses to buy it then the beliefs \(\Pr \left( {\left. j \right| g} \right) =\frac{q_j }{\sum \nolimits _{k\in N} {q_k } }\) for \(j\in N\) in the case of no acquisition and good additional information fulfill Bayes’ rule. The same has to be true for the beliefs in the other situations. Lastly, the beliefs from (ii) and the resulting prices in (iii) leads to the inequalities in (8) and (9) which lead to the rational decisions of the firms given in (i).

1.2 Proof of Lemma 1

-

(a)

M = {A, C}

First we consider if \(M=\left\{ {A,C} \right\} \). From (5) and (6) we get \(P_{\left\{ B \right\} } \left( {g,NIS} \right) =P_{\left\{ B \right\} } \left( {b,NIS} \right) = \overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{B}(x)dx\). Thus, from (8) we get \(K\ge \int \nolimits _{\underline{x}}^{0} F_B \left( x \right) dx\) and from (9) we get \(K\le \int \nolimits _{\underline{x}}^{0} F_B \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\). However, these two inequalities cannot hold simultaneously because \(F_C \left( x \right) \ge F_B \left( x \right) \) and \(F_C \left( x \right) \ne F_B \left( x \right) \). Thus, \(M=\left\{ {A,C} \right\} \) is not an equilibrium.

-

(b)

M = {B, C}

Next we consider if \(M=\left\{ {B,C} \right\} \) can constitute an equilibrium. From (5) and (6) we get \(P_{\left\{ A \right\} } \left( {g,NIS} \right) =P_{\left\{ A \right\} } \left( {b,NIS} \right) =\overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{A}(x)dx\). From (8), \(K\ge \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) dx\) follows and from (9) the following inequality can be obtained: \(K\le \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_B \left( x \right) -F_A \left( x \right) dx\). These two inequalities cannot hold simultaneously because \(F_B \left( x \right) \ge F_A \left( x \right) \) and \(F_A \left( x \right) \ne F_B \left( x \right) \).

1.3 Existence of equilibria

-

(a)

\(M=\left\{ {A,B} \right\} \)

If \(M=\left\{ {A,B} \right\} \) then from (5) and (6), \(P_{\left\{ C \right\} } \left( {g,NIS} \right) =P_{\left\{ C \right\} } \left( {b,NIS} \right) =\overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{C}(x)dx\) follows. From (8) and (9): \(\int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx+ \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\ge K\ge \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\) follows. The assumption of first order stochastic dominance guarantees the existence.

-

(b)

\(\left\{ B \right\} \)

In order to calculate the minimum of the left side of (10), we set two constrained maximization problems. The first one is: maximize: \(-\Psi _A \) with respect to \(q_A \) and \(q_C \) under the constraints: \(\Psi _A \ge \Psi _C , q_A \ge q_C , q_A \le 1\) and \(q_C \ge 0\). The second one is: maximize \(-\Psi _C \) with respect to \(q_A \) and \(q_C \) under the condition \(\Psi _A \le \Psi _C \), the rest stays the same. This can be solved with the Kuhn-Tucker conditions. The minimum of \(max\left[ {\Psi _A ,\Psi _C } \right] \) is attained if:

Inserting (14) in \(\Psi _A \) or \(\Psi _C \) lead to the minimal cost of: \(\frac{1}{2} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_A \left( x \right) dx\). \(\Psi _A <\Psi _C \) if \(0\le q_C <\chi \) and \(\phi <q_A \le 1\). \(\Psi _A >\Psi _C \) if \(0\le q_C <\chi \) and \(q_C <q_A <\phi \) or \(\chi <q_C <q_A \) and \(q_A \le 1\).

-

(c)

\(M=\left\{ A \right\} \)

The boundaries for \(K\) can be calculated using Eq. (8) and (9). The minimum value of the lower boundary equals: \(\frac{1}{2} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_B \left( x \right) dx\). The upper limit follows from (9): \(\tau \int \nolimits _{\underline{x}}^{\overline{x}} F_B \left( x \right) dx+\left( {1-\tau } \right) \int \nolimits _{\underline{x}}^{\overline{x}} F_C \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_A \left( x \right) dx\ge K\) with: \( \tau =\frac{q_A q_B \left( {2-q_B -q_C } \right) +\left( {q_B +q_C } \right) \left( {1-q_A } \right) \left( {1-q_B } \right) }{\left( {q_B +q_C } \right) \left( {2-q_B -q_C } \right) }\).

-

(d)

\(M=\left\{ {A,B,C} \right\} \)

For \(M=\left\{ {A,B,C} \right\} \) we must first define the out-of-equilibrium beliefs for \(P_{\left\{ \right\} } \left( {g,NIS} \right) \) and \(P_{\left\{ \right\} } \left( {b,NIS} \right) \). In this equilibrium, the market believes that all firms buy the information system. But what will be the market price if the market observes no acquisition of the information system? If a deviation from the equilibrium strategies is observed the market must hold beliefs about which firm type \(i\), with \(i\in \left\{ {A,B,C} \right\} \), deviates. Denote the probability that it will be a firm of type \(i\) with \(\lambda _i \), where \( \sum \nolimits _{i\in \left\{ {A,B,C} \right\} } \lambda _i =1\). Thus, in case of good and bad information the market price will be:

In this equilibrium equation (9) must hold for all \(i\in \left\{ {A,B,C} \right\} \) with \(P_{\left\{ \right\} } \left( {g,NIS} \right) \) and \(P_{\left\{ \right\} } \left( {b,NIS} \right) \) given in (15). This equilibrium does not exists if \(K> \int \nolimits _{\underline{x}}^{0} F_C dx\). In this case it is independent of the beliefs, \(\lambda _i \), at least for the worst type, \(C\), not profitable to acquire the information system.

-

(e)

\(M=\left\{ \right\} \)

In order that this equilibrium exists the parameter must fulfill the inequalities in (8). The minimum value for this lower boundary for \(K\) equals: \(\frac{1}{3} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_B \left( x \right) +F_A \left( x \right) dx\), this is reached for some combination of \(q_A , q_B \) and \(q_C \). This pooling equilibrium needs no out of equilibrium beliefs because equation (2) denotes the price in case of deviating.

-

(f)

\(\left\{ C \right\} \)

In order that \(M=\left\{ C \right\} \) could be an equilibrium, the costs must lie in the following interval:

The lowest possible value of the left side equals \(\frac{1}{2} \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) +F_B \left( x \right) dx\). The upper limit follows from (9): \(\varphi \int \nolimits _{\underline{x}}^{\overline{x}} F_A \left( x \right) dx+\left( {1-\varphi } \right) \int \nolimits _{\underline{x}}^{\overline{x}} F_B \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) dx\ge K\). The upper boundary has to be higher than \(\Psi _A \) and \(\Psi _B \). From rearranging these two conditions we get:

Both inequalities can hold simultaneously, f. ex. suppose \(F_C \left( x \right) =F_B \left( x \right) =F_A \left( x \right) \) for \(x\in \left[ {0,\overline{x}} \right] \).

1.4 Proof of Theorem 3

1.4.1 Coexistence of equilibria

This subsection shows that some equilibria can coexist with others. To prove the coexistence, it is sufficient to show that there exists parameter values for which equilibria can simultaneously exist. It is not essential to define the whole set of parameter values for which coexistence occur.

-

(a)

Coexistence with \(M=\left\{ B \right\} \)

First, we compare \(M=\left\{ B \right\} \) and \(M=\left\{ {A,B} \right\} \). Suppose the additional information is good in distinguishing between the best and the worst project types and bad in separating a medium project from the worst project, \(q_A \rightarrow 1\) and \(q_C \rightarrow 0\) and \(q_B \rightarrow q_C \). The boundaries for the existence of the equilibrium \(M=\left\{ B \right\} \) simplify as well to \( \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\le K\le \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx+ \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\). Thus, coexistence of the two equilibria is possible. Comparing the efficiency of these equilibria, we get: \(Z\left( {\left\{ B \right\} } \right) -Z\left( {\left\{ {A,B} \right\} } \right) =\frac{1}{3}\left( {K- \int \nolimits _{\underline{x}}^{0} F_A dx} \right) >0\). While the inequality follows from cost domain which is needed for the considered equilibria.

Likewise, equilibria \(M=\left\{ B \right\} \) and \(M=\left\{ A \right\} \) can coexist. Suppose \(q_A \rightarrow 1\) and \(q_C \rightarrow 0\) and \(q_B \rightarrow q_C \) then the boundaries for the existence of the equilibrium \(M=\left\{ A \right\} \) are given by: \(\frac{1}{2} \int \nolimits _{\underline{x}}^{\overline{x}} F_B \left( x \right) +F_C \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_B \left( x \right) dx\le K\le \frac{1}{2} \int \nolimits _{\underline{x}}^{\overline{x}} F_B \left( x \right) +F_C \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_A \left( x \right) dx\). The boundaries for the existence of equilibrium \(M=\left\{ B \right\} \) simplify to \(\int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\le K\le \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx+ \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\). Thus, in order that both equilibria exist, the following inequality must hold: \(\frac{1}{2} \int \nolimits _{\underline{x}}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\le \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_A \left( x \right) dx\), otherwise both boundaries for \(K\) cannot hold simultaneously. The efficiency of \(M=\left\{ B \right\} \) is higher because: \(Z\left( {\left\{ B \right\} } \right) -Z\left( {\left\{ A \right\} } \right) =\frac{1}{3}\left( { \int \nolimits _{\underline{x}}^{0} F_B -F_A dx} \right) >0\). The inequality follows from the assumption of first order stochastic dominance.

The existence of parameter constellation for which both \(M=\left\{ \right\} \) and \(M=\left\{ B \right\} \) hold can be shown by calculating the boundary value for \(K\) if \(F_B \left( x \right) \rightarrow F_A \left( x \right) \) and \(q_B \rightarrow q_C \). In this case the upper boundary converges to: \(\overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{A}(x)dx-\left( q_{C} P_{\{A,C\}} (g)+(1-q_{C}) P_{\{A,C\}} (b)\right) \) and the lower boundary converges to the maximal value of \(\overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{A}(x)dx-\left( q_{C} P_{\{A,B,C\}} (g)+(1-q_{C}) P_{\{A,B,C\}} (b)\right) , \overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{A}(x)dx-\left( q_{C} P_{\{A,C\}} (g)+(1-q_{C}) P_{\{A,C\}} (b)\right) \) and \(\overline{x}-\int \nolimits _{\underline{x}}^{\overline{x}}F_{C}(x)dx-(q_{C} P_{\{A,C\}} (g)+ (1-q_{C}) P_{\{A,C\}} (b))\). All of this three values are smaller than the upper boundary for \(K\). This proves the coexistence of these two equilibria. \(M=\left\{ B \right\} \) is preferred if the following inequality holds: \(Z\left( {\left\{ B \right\} } \right) -Z\left( {\left\{ \right\} } \right) =\frac{1}{3}\left( { \int \nolimits _{\underline{x}}^{0} F_B dx-K} \right) >0\). This inequality shows that compared to \(M=\left\{ \right\} , M=\left\{ B \right\} \) is only preferred if the benefits of having the information are higher than the cost of acquiring it for a manager of type \(B\).

\(M=\left\{ B \right\} \) and \(M=\left\{ {A, B,C} \right\} \) can coexist. From the analysis above, we know that there exists out of equilibrium beliefs which lead to the existence of this equilibrium as long as \(K\le \int \nolimits _{\underline{x}}^{0} F_C dx\). Likewise, there exist parameter values for which the equilibrium \(M=\left\{ B \right\} \) is possible and also \(K\le \int \nolimits _{\underline{x}}^{0} F_C dx\) is fulfilled. Comparing the efficiency of the equilibrium \(M=\left\{ {A,B,C} \right\} \) with \(M=\left\{ B \right\} \) we get: \(Z\left( {\left\{ B \right\} } \right) -Z\left( {\left\{ {A,B,C} \right\} } \right) =\frac{1}{3}\left( {2K- \int \nolimits _{\underline{x}}^{0} F_A +F_C dx} \right) >0\). The difference is positive because we assumed that the equilibrium \(M=\left\{ B \right\} \) exists, which is only the case if \(K\ge \frac{1}{2} \int \nolimits _{\underline{x}}^{0} F_A +F_C dx\). Note that the right side of this inequality is the minimum of \(max\left[ {\Psi _A ,\Psi _C } \right] \).

The coexistence of \(M=\left\{ B \right\} \) and \(M=\left\{ C \right\} \) is not possible. If equilibrium \(M=\left\{ B \right\} \) exists, the following inequality must hold:

However, this inequality cannot hold for \(0\le q_C <q_B <q_C \le 1\) and \(F_C \ge F_B \ge F_A \).

-

(b)

Coexistence with \(M=\left\{ C \right\} \)

The equilibrium \(M=\left\{ {A,B} \right\} \) requires \(K\ge \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\). If costs are that high, \(M=\left\{ C \right\} \) is not possible. Likewise, the cost limits for equilibrium \(M=\left\{ A \right\} \) and \(M=\left\{ C \right\} \) are not compatible.

According to the cost interval for equilibrium \(M=\left\{ {A,B,C} \right\} \) and \(M=\left\{ C \right\} \), a coexistence is possible. Comparing the efficiency between these equilibria lead to: \(Z\left( {\left\{ C \right\} } \right) -Z\left( {\left\{ {A,B,C} \right\} } \right) =\frac{1}{3}\left( {- \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) +F_B \left( x \right) dx+2K} \right) >0\) while the inequality follows from the lowest possible value of \(K\) for the existence of the equilibrium \(M=\left\{ C \right\} \).

The coexistence from \(M=\left\{ C \right\} \) and \(M=\left\{ \right\} \) is not possible. From \(M=\left\{ C \right\} \) we get: \(\varphi \int \nolimits _{\underline{x}}^{\overline{x}} F_A \left( x \right) dx+\left( {1-\varphi } \right) \int \nolimits _{\underline{x}}^{\overline{x}} F_B \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) dx\ge K\) while from \(M=\left\{ \right\} \) we receive: \(\lambda \int \nolimits _{\underline{x}}^{\overline{x}} F_A \left( x \right) dx+\gamma \int \nolimits _{\underline{x}}^{\overline{x}} F_B \left( x \right) dx+\left( {1-\lambda -\gamma } \right) \int \nolimits _{\underline{x}}^{\overline{x}} F_C \left( x \right) dx- \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) dx\le K\). Because \(\varphi >\lambda \) and \(\left( {1-\varphi } \right) > \gamma \) both inequalities cannot hold at the same parameter values.

-

(c)

Coexistence with \(M=\left\{ \right\} \)

\(M=\left\{ \right\} \) and \(M=\left\{ {A,B,C} \right\} \) can coexist because there exists parameter values for which the lower boundary for \(K\) equals: \(\frac{1}{3} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_B \left( x \right) +F_A \left( x \right) dx\) and there exists out of equilibrium beliefs which support the equilibrium \(M=\left\{ {A,B,C} \right\} \) as long as \(K\le \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\). \(Z\left( {\left\{ \right\} } \right) -Z\left( {\left\{ {A,B,C} \right\} } \right) =\frac{1}{3}\left( {- \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) +F_B \left( x \right) +F_C \left( x \right) dx+3K} \right) >0\).

\(M=\left\{ \right\} \) and \(M=\left\{ {A,B} \right\} \) can coexist because \(M=\left\{ {A,B } \right\} \) requires \( \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx+ \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\ge K\ge \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\) whereas there exists parameter values for which \(M=\left\{ \right\} \) is an equilibrium as long as \(K\ge \frac{1}{3} \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) +F_B \left( x \right) +F_A \left( x \right) dx\). Comparing the efficiency, we get the following inequality: \(Z\left( {\left\{ \right\} } \right) -Z\left( {\left\{ {A,B} \right\} } \right) =\frac{1}{3}\left( {- \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) +F_B \left( x \right) dx+2K} \right) >0\). The inequality follows from the equilibrium conditions for \(K\).

For the coexistence of \(M=\left\{ \right\} \) and \(M=\left\{ A \right\} \) we can apply a similar argument. Comparing the efficiency of \(M=\left\{ \right\} \) and \(M=\left\{ A \right\} \) we get: \(Z\left( {\left\{ \right\} } \right) -Z\left( {\left\{ A \right\} } \right) =\frac{1}{3}\left( {- \int \nolimits _{\underline{x}}^{0} F_A \left( x \right) dx+K} \right) >0\) while the inequality follows from lower boundary for \(K\) in equilibrium.

-

(d)

Coexistence with \(M=\left\{ A \right\} \)

As we know from above the equilibrium \(M=\left\{ {A,B} \right\} \) is independent from the additional information, \(r\in \left\{ {g,b} \right\} \). Further, in order that this equilibrium occur the inequality, \( \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx+ \int \nolimits _{0}^{\overline{x}} F_C \left( x \right) -F_B \left( x \right) dx\ge K\ge \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\) must hold. There exist parameter values such that these inequalities together with the inequalities for \(M=\left\{ A \right\} \) lead to no contradiction. Comparing the efficiency of the two equilibria leads to the conclusion that \(M=\left\{ A \right\} \) is preferred, because \(Z\left( {\left\{ A \right\} } \right) -Z\left( {\left\{ {A,B} \right\} } \right) =\frac{1}{3}\left( {- \int \nolimits _{\underline{x}}^{0} F_B \left( x \right) dx+K} \right) >0\), while the inequality follows from \(K\ge \int \nolimits _{\underline{x}}^{0} F_B \left( x \right) dx\) which is required for both equilibria.

The upper bound for the cost for the equilibrium \(M=\left\{ {A,B,C} \right\} \) is given by \( \int \nolimits _{\underline{x}}^{0} F_C dx\) which is independent of the additional information, \(r\in \left\{ {g,b} \right\} \) and base on the out of equilibrium beliefs \(\lambda _C =1\). Dependent on the parameter values, \(K\le \int \nolimits _{\underline{x}}^{0} F_C dx\) is also possible for the equilibrium \(M=\left\{ A \right\} \). \(Z\left( {\left\{ A \right\} } \right) -Z\left( {\left\{ {A,B,C} \right\} } \right) =\frac{1}{3}\left( {- \int \nolimits _{\underline{x}}^{0} F_B \left( x \right) +F_C \left( x \right) dx+2K} \right) >0\), the inequality follows from the lowest possible \(K\) value for equilibrium \(M=\left\{ A \right\} \).

-

(e)

Coexistence with \(M=\left\{ {A,B} \right\} \)

For \(M=\left\{ {A,B,C} \right\} K\le \int \nolimits _{\underline{x}}^{0} F_C dx\) is required while for \(M=\left\{ {A,B} \right\} , K\ge \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\) is required. Except for \(K= \int \nolimits _{\underline{x}}^{0} F_C \left( x \right) dx\) and out of equilibrium beliefs \(\lambda _C =1\), the two equilibria cannot coexist.

1.5 Non-observability of the acquisition of the information system

In this extension we assume that the market only observes with probability \(1-p\) whether the manager bought an information system or not. In case of observing, we attain the same approach as above. Thus, if the market learns that the manager refrains from buying the information system and the additional information was good (bad) then market price is given by (5) ((6)). If the market detects that the manager produced the information but decides not to disclose, it values the firm with \(-K\). In case of a voluntary disclosure it values the firm according to (2). However, if the market is unable to verify if the information system was installed or not a manager who receives the information discloses it if:

Where \(t_r \) is manager’s beliefs about the market price if no acquisition of the information system is observed and the public information turns out to be \(r\in \left\{ {b,g} \right\} \). In case of a disclosure the market price is given by (2). In equilibrium the beliefs coincide with actual market price. To simplify notation, we do not distinguish between conjectured and actual market price. The rational market evaluates the firm with its expected value, which is given by:

\(t_g \) and \(t_b \) represent the market’s beliefs about manager’s disclosure strategy, for the situation with a good public signal and for the bad situation, respectively. \(u\in \left\{ { {\underline{x}} ,0} \right\} \) reflects two scenarios: \(u= \underline{x}\) displays the situation where the abandonment decision is observable by the market and has to be undertaken before the date at which the manager cares about the market price. In this case the manager would not abandon an unprofitable project in order to convince the market that he has no information because a manager with no information would never abandon a project. In the other cases we would have: \(u=0\), because the informed manager would abandon the project if expected payoff is negative. This threshold value is unique and \(\frac{\sum \nolimits _{i\in N} q_i E_i \left[ {\tilde{x}} \right] }{\sum \nolimits _{i\in N} q_i }>t_g >t_b >u\). Existence and uniqueness follows from the intermediate value theorem. Inequality \(t_g >t_b \) follows from the assumption that a firm with higher quality receives the good public signal more likely.Footnote 12

In order that this is an equilibrium, a manager in a firm of type \(i\in N\) must have a higher utility from not buying the information system:

The left side shows the expected market price in case of not producing the information. With probability \(p\) the market is unable to verify if the manager installed the information system or not. Market prices in these cases are given in Eqs. (21) and (22). If the market detects that no information was produced then market price is given by either (5) or (6) depending on whether there was a good or bad signal. The right side reflects the ex ante expected value if the manager bought the information system. If the market is unable to verify the existence of an information system the manager can pool with the firms who have no information system. The manager will do so if inequality (20) does not hold. Thus, with probability \(pq_i F_i \left( {t_g +K} \right) \) he will achieve an evaluation of \(t_g \) and with probability \(p\left( {1-q_i } \right) F_i \left( {t_b +K} \right) \) market price will be \(t_b \). However, if market price in case of a disclosure, \(x-K\), exceeds the market price in case of no disclosure \(t_r \), he prefers disclosing. The expected market prices of theses cases weighted with the probability of occurrence is given by the third and fourth term in curly brackets. With probability \(\left( {1-p} \right) \) we have the same situation as already discussed in the previous sections. Simplifying Eq. (23) we derive that an equilibrium requires:

while a manager in a firm of type \(j\in M\) has to prefer buying the information system:

Note that the term in curly brackets of the inequalities is positive because the expected value that \(x\) is larger than the lower boundary minus this lower boundary is always positive. Thus, if for example the market never observes the installation of the information system (and the manager is not able to communicate the not acquisition) \(p=1\), then a manager acquires the information system because this is the dominant strategy independent of the type. For \(p\rightarrow 0\) we have the same situation analyzed above. Thus, for \(p\) sufficiently small the same equilibria exists as above. Note further, that the left side of the inequality is increasing in \(K\) while the right side is decreasing. Additionally, we know that a manager of type \(i\) is indifferent if: \(K=\Psi _i \) if \(\hbox {p}=0\). Therefore, the lower and upper threshold values for the costs \(K\) obtained through the inequalities (24) and (25) will be higher than the ones for \(\hbox {p}=0\).

Rights and permissions

About this article

Cite this article

Boisits, A., Königsgruber, R. Information acquisition and disclosure by firms in the presence of additional available information. Cent Eur J Oper Res 24, 177–205 (2016). https://doi.org/10.1007/s10100-014-0347-6

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10100-014-0347-6