Abstract

This paper presents an approach for estimating changes in firms’ productivity. We apply the quantile approach, which estimates the changes in the productivity distribution of surviving firms. Using this method, the paper clarifies productivity dynamics in terms of both average change and dispersion in Japan from 1987 to 2014. The main results of the analysis are as follows: During a boom or normal period, the productivity distribution shifts to the right and the productivity dispersion decreases. Conversely, during a recession, the productivity distribution shifts to the left and the productivity dispersion expands. The analysis also gives quantitatively significant results. During the historically rare global financial crisis of 2008, the weighted (simple) average of manufacturing productivity in Japan fell by only 0.2% (5.4%). We identified that this counter-intuitive result was due to a significant change in the shape of the productivity distribution and found that the crisis would reduce productivity by more than 22% if the effects of changing the shape of the distribution were adjusted.

Similar content being viewed by others

Notes

Empirical studies along this line include, for example, Caballero and Hammour (1994), Dunne et al. (1988), Baily et al. (1992), Davis and Haltiwanger (1992), Olley and Pakes (1996), Bartelsman and Dhrymes (1998), and Nishimura et al. (2005). See also Lileeva (2008) and Atkeson and Burstein (2010) for studies of productivity dispersion.

Combes et al. (2012) first proposed QA to compare the productivity distribution between regions with different densities. We apply it to compare the productivity distributions between two different points in time. The stylized fact in the urban economics literature is that firms are, on average, more productive in dense regions. Theoretical applications use agglomeration economies, as Marshall (1890) and Jacobs (1969) argue, and the natural selection of firms in models by Melitz (2003) and Melitz and Ottaviano (2008) to explain this fact. However, it is difficult to distinguish between these two factors in empirical research. QA makes it possible to separate them, and hence, recent studies adopt this method to decompose the sources of productivity changes in the regional economics context (Arimoto et al. 2014; Kondo 2016; Accetturo et al. 2018; Jales et al. 2018).

There is an enormous body of research on productivity in Japan. Among them, searching for factors that reduce productivity was at the center of attention, and many studies suggest that the failure to reallocate resources due to the exit of productive firms and the survival of unproductive firms, often called Zombies, was a factor behind the stagnation of TFP (Kwon et al, 2005; Nishimura et al. 2005; Caballero et al. 2008). See, for example, Table 1 of Fukao and Kwon (2006, p.198), which summarizes the results of studies that measure changes in Japan’s TFP.

Other studies reproduce the relationship between productivity dispersion and the business cycle by calibrating theoretical models. For example, Bachmann and Bayer (2014) present a calibrated model to explain the positive correlation between the dispersion of firms’ investment and the business cycle.

Looking at the composition ratio of domestic production by industry, the manufacturing industry has the highest ratio at 30.8%. This is followed by the service industry at 22.9% and the commerce at 10.0%, showing the significant size of the manufacturing industry in terms of domestic production in Japan. See Ministry of Economy, Trade and Industry, White Paper on Manufacturing Industries 2015 (https://www.meti.go.jp/english/report/downloadfiles/0609_01a.pdf), accessed on August 11, 2019.

The data we use in the paper include twenty four sectors (JSIC Codes 9 to 32) in the industrial classification. This includes two industries that are different in nature from other manufacturing industries, such as the manufacture of food and manufacture of beverage, tobacco, and feed, but other fields can be considered to be fields that produce durable goods.

The CM data that we can use run from 1986 to 2014, except for 2011. The CM survey was not conducted in 2011, but we could replace the data of 2011 with the Economic Census for Business Activity jointly conducted by the Ministry of Economy, Trade and Industry and the Ministry of Internal Affairs and Communications.

The Ministry of Economy, Trade and Industry publishes IIP, which can be downloaded from https://www.meti.go.jp/english/statistics/tyo/iip/index.html.

For how to create the index, see Ministry of Economy, Trade and Industry, Mechanism of and way to understand Indices of Industrial Production (http://www.meti.go.jp/english/statistics/tyo/iip/pdf/b2010_mechanism_iipe.pdf), accessed on January 16, 2019.

See Appendix C.

Kondo (Kondo 2016, p.11) also points out that \(R^2\) can have a small value even if the model specification fits the data correctly.

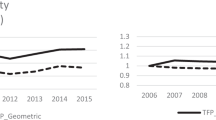

The second and third columns of Table 3 show that the TFP growth rate in the 1990s was lower than before and had already decreased since 1987. The annual average growth rate of simple (weighted) average TFP for the three years after 1987 was 2.3 (2.2)%, while it decreased to 0.05 (0.06)% in the 1990s, and the 1990s is called the lost decade for Japan. The situation slightly improved after that, and the annual simple (weighted) average growth rate of TFP for the 15 years from 2000 was 0.50 (0.82)%. A sharp drop in simple average TFP was recorded in 2009, which was \(-5.4\)%, and the sharp increase in TFP in 2010 corresponds to the year in which the economy recovered from the global financial crisis.

Estimates from the additional analyses on which we base the explanations in this subsection are available from the authors upon request.

The estimation results based on other constraints including the case of imposing the constraint of \(T = 0\) are available upon request to the authors.

This number is obtained by comparing the second and sixth columns of Table 6.

The problem of multiple tests can sometimes be solved by performing Bonferroni correction. However, as it is a conservative test, it is prone to Type II errors where the null hypothesis is not rejected when it should be, especially as the number of tests increases.

References

Accetturo A, Di Giacinto V, Micucci G, Pagnini M (2018) Geography, productivity, and trade: does selection explain why some locations are more productive than others? J Reg Sci 58:949–979

Arimoto Y, Nakajima K, Okazaki T (2014) Sources of productivity improvement in industrial clusters: the case of the prewar Japanese silk-reeling industry. Reg Sci Urb Econ 46:27–41

Atkeson A, Burstein AT (2010) Innovation, firm dynamics, and international trade. J Polit Econ 118:433–484

Bachmann R, Bayer C (2014) Investment dispersion and the business cycle. Am Econ Rev 104:1392–1416

Bartelsman E, Dhrymes P (1998) Productivity dynamics: U.S. manufacturing plants, 1972–1986. J Prod Anal 9:5–34

Baily MN, Hulten C, Campbell D, Bresnahan T, Caves RE (1992) Productivity dynamics in manufacturing plants. Brook Papers Econ Activ Microecon 1992:187–267

Bloom N, Floetotto M, Jaimovich N, Saporta-Eksten I, Terry SJ (2018) Really uncertain business cycles. Econometrica 86:1031–1065

Caballero R, Hammour ML (1994) The cleansing effect of recessions. Am Econ Rev 84:1350–1368

Caballero R, Hoshi T, Kashyap AK (2008) Zombie lending and depressed restructuring in Japan. Am Econ Rev 98:1943–1977

Cabinet Office of Japan (1998) The Japanese economy in 1998: A review of events and challenges for the future - Recovering from the aftereffects of the bubble’s collapse

Combes P, Duranton G, Gobillon L, Puga D, Roux S (2012) The productivity advantages of large cities: distinguishing agglomeration from firm selection. Econometrica 80:2543–2594

Davis SJ, Haltiwanger J (1992) Gross job creation, gross job destruction, and employment reallocation. Quart J Econ 107:819–863

Dunne T, Roberts MJ, Samuelson L (1988) Patterns of firm entry and exit in US manufacturing industries. RAND J Econ 19:495–515

Firpo S, Fortin NM, Lemieux T (2009) Unconditional quantile regressions. Econometrica 77:953–973

Foster L, Haltiwanger JC, Krizan CJ (2001) Aggregate productivity growth: Lessons from microeconomic evidence. In: Hulten CR, Dean ER, Harper MJ (eds.), New Developments in Productivity Analysis (pp. 303–372). University of Chicago Press

Fukao K, Kwon HU (2006) Why did Japan’s TFP growth slowdown in the lost decade? An empirical analysis based on firm-level data of manufacturing firms, Japanese Economic Review 57:195–228

Hayashi F, Prescott EC (2002) The 1990s in Japan: a lost decade. Rev Econ Dyn 5:206–235

Jacobs J (1969) The economy of cities. Vintage, New York

Japan Small Business Research Institute (2010) White paper on small and medium enterprises in Japan. Putting through the crisis, accessed on September 2, 2018. http://www.chusho.meti.go.jp/pamflet/hakusyo/h22/h22_1/2010hakusho_eng.pdf

Jales H, Jiang B, Rosenthal SS (2018) Separating selection from spillover effects: Using the mode to estimate the return to city size, unpublished manuscript

Jorgenson DW, Kuroda M, Nishimizu M (1987) Japan-U.S. industry-level productivity comparisons, 1960–1979. J Jap Int Econ 1:1–30

Kawai M, Takagi, (2011) Why was Japan hit so hard by the global financial crisis? In: Shaw SD, Liu BJ (eds) The Impact of the Economic Crisis on East Asia: Policy Responses from Four Economies. Edward Elgar Publishing

Kehrig M (2011) The cyclicality of productivity dispersion, Working Papers 11–15, Center for Economic Studies, U.S. Census Bureau

Kondo K (2016) Testing for agglomeration economies and firm selection in spatial productivity differences: The case of Japan, Discussion papers 16098. Research Institute of Economy, Trade and Industry (RIETI)

Konishi Y, Nishiyama Y (2010) Productivity of service providers: Microeconometric measurement in the case of hair salons, Discussion papers 10051. Research Institute of Economy, Trade and Industry (RIETI)

Konishi Y, Nishiyama Y (2013) Decomposition of supply and demand shocks in the production function using the current survey of production, Discussion papers 13003. Research Institute of Economy, Trade and Industry (RIETI)

Kwon HU, Narita F, Narita M (2015) Resource reallocation and Zombie lending in Japan in the 1990s. Rev Econ Dyn 18:709–732

Levinsohn J, Petrin A (2003) Estimating production functions using inputs to control for unobservables. Rev Econ Stud 70:317–341

Lileeva A (2008) Trade liberalization and productivity dynamics: evidence from Canada. Canad J Econ 41:360–390

Marshall A (1890) Principles of economics. Macmillan, London

Melitz M (2003) The impact of trade on intra-industry reallocations and aggregate industry productivity. Econometrica 71:1695–1725

Melitz M, Ottaviano G (2008) Market size, trade, and productivity. Rev Econ Stud 75:295–316

Morikawa M (2011) Economies of density and productivity in service industries: an analysis of personal service industries based on establishment-level data. Rev Econ Stat 93:179–192

Morikawa M (2012) Demand fluctuations and productivity of service industries. Econ Lett 117:256–258

Nakamura R (1985) Agglomeration economies in urban manufacturing industries: a case of Japanese cities. J Urb Econ 17:108–124

Nishimura KG, Nakajima T, Kiyota K (2005) Does the natural selection mechanism still work in severe recessions?: examination of the Japanese economy in the 1990s. J Econ Behav Org 58:53–78

Norsworthy JR, Malmquist DH (1983) Input measurement and productivity growth in Japanese and U.S. Manuf Am Econ Rev 73:947–967

Olley G, Pakes A (1996) The dynamics of productivity in the telecommunications equipment industry. Econometrica 64:1263–1297

Wooldridge JM (2009) On estimating firm level production functions using proxy variables to control for unobservables. Econ Lett 104:112–114

Acknowledgements

This study is conducted as a part of the Project “The Role of Regional Financial Institutions as the Core of the Local Economy and Regional Cooperation” undertaken at Research Institute of Economy, Trade and Industry (RIETI). This study utilizes the micro data of the questionnaire information based on the “Census of Manufacture” which is conducted by the Ministry of Economy, Trade and Industry (METI), and the Kogyotokei Converter, which is provided by RIETI. We would like to thank Nobuaki Hamaguchi, Masayoshi Hayashi, Keisuke Kondo, Yoko Konishi, Masayuki Morikawa, Takahiro Tsukamoto, Nobuyoshi Yamori, Makoto Yano, and participants of the RIETI Discussion Paper Seminar for their useful comments. The authors also acknowledge the financial support of JSPS Grant nos. 17H02533, 18K12773, 19H01505, and 20K22128.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Authors’ contributions

Adachi contributed to cleaning of data, modeling, coding, estimation, and interpretation of results

Ogawa performed data submission, review of previous studies, writing of the paper, and interpretation of results

Tsubuku contributed to data submission, data cleaning, estimation, visualization, and interpretation of results

Funding

This study is conducted as a part of the project “The Role of Regional Financial Institutions as the Core of the Local Economy and Regional Cooperation” undertaken at the Research Institute of Economy, Trade and Industry (RIETI). The research has been supported by grants from the Japan Society for the Promotion of Science (Nos. 17H02533, 18K12773, 19H01505 and 20K22128).

Conflicts of interest

The authors declare no conflicts of interest associated with this manuscript.

Availability of data and material

All data sources are indicated in the text. The restrictions by the Ministry of Economy, Trade and Industry (MITI) of Japan apply to the availability of the data, which was used under license for the current study, and so is not publicly available. Data are, however, available from the MITI upon reasonable request and with permission of it for use.

Code availability

All estimations were done using Stata. The code used is available upon request to the authors.

Ethics approval

This study does not include any animal testing or human participation that would raise ethical issues.

Consent to participate

This study did not involve any experiments, interviews, or other analyses that would require the consent of the participants.

Consent for publication

This study does not include analyses in which personal or other information is identified and made public. As for company information, all information, including company names and addresses, was processed in such a way that it could not be identified.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendices

1.1 Appendix A: Derivation of (1)

Denote \(\tilde{\phi }\) as the random productivity which is unobservable. The cumulative distribution function (CDF) and probability density function (PDF) of the random variable are, respectively, denoted by \(\tilde{F}(.)\) and \(\tilde{f}(.)\). What we observe is \(\sigma \), which is related to \(\tilde{\phi }\) by three factors in QA; (i) Shift (S), (ii) Truncation (T), and (iii) Dilation (D).

(i) Shift (S) is an effect that affects all establishments equally regardless of the level of productivity. The effect can be shown by \(\phi =\tilde{\phi }+S\). The CDF is, therefore, given by \(F(\phi )=\tilde{F}(\tilde{\phi })=\tilde{F}(\phi +S)\). In the probability distribution, the effect of the shift (S) is represented by the parallel movement of the distribution, as shown in Fig. 1.

(ii) Truncation (T) captures changes in the proportion of establishments that are below the minimum level of productivity required to survive in the market. Suppose that the lowest level of productivity of the establishment operating in the market is given by \(\underline{\phi }\). In this case, an establishment with a productivity lower than \(\underline{\phi }\) is not observed in the data; \(F(\underline{\phi })=T\). The TFP of such establishments with lower productivity than \(\underline{\phi }\) is zero: \(\phi =\tilde{\phi }\) if \(\tilde{\phi }\ge \underline{\phi }\) and \(\phi =0\) if \(\tilde{\phi }< \underline{\phi }\). The sum of the probabilities must be 1, but at this stage the following equations hold:

In order to satisfy the law of probabilities, by dividing both sides of the equation by \(1-T\), we get:

Since the productivity of the establishment is zero if its productivity is less than \(\underline{\phi }\), we have

Figure 1(b) visually shows the difference between the Shift effect and the Truncation effect. In the figure, although the distribution moves in parallel to the right due to the Shift effect, there is no Truncation effect because the proportion of establishments with low productivity that cannot be activated in the market does not change.

(iii) Dilation (D) captures the effect that changes in productivity differ among establishments according to the original level of their productivities. The relationship between \(\tilde{\phi }\) and \(\phi \) can be expressed as \(\phi =D\tilde{\phi }\) when the productivity of the establishment increases by a factor of D. In this case, the CDF is given by \(F(\phi )=\tilde{F}(\tilde{\phi })=\tilde{F}(\phi /D)\). If there is the Shift effect in addition to the Dilation effect, \(\phi =D\tilde{\phi }+S\) holds, and the CDF is as follows.

Substituting (14) into (13), we obtain (1).

1.2 Appendix B: Derivation of (3) and (4)

If \(T_1>T_0\), the change in variable \(\phi \rightarrow (\phi -S)/D\) turns \(F_0\) into

Dividing by \(1-T\) and adding \(-T/(1-T)\) to all terms leads to

We obtain

Next, if \(T_1<T_0\), the change in variable \(\phi \rightarrow D\phi + S\) turns \(F_0\) into

Dividing by \(1-T\) and adding \(-T/(1-T)\) to all terms leads to

We obtain

1.3 Appendix C: Derivation of (10)

Following the computation method of the minimization criterion suggested by Combes et al. (2012), this appendix provides the detailed computation methodology in Section 3.1.3. In this approach, the parameter \(\theta \) is estimated by minimizing \(M(\theta )\) from \(\hat{m}_\theta (u)\) and \(\hat{\tilde{m}}_\theta (u)\) for any rank of \(u \in [0, 1]\). To evaluate \(\hat{m}_\theta (u)\) and \(\hat{\tilde{m}}_\theta (u)\), we approximate true quantiles \(\lambda _t\) by \(\hat{\lambda }_t(u)\). First, we list productivity in ascending order for each period. The set of log productivities in period t is

where \(N_t\) is the number of firms in period t and \(\phi _t(0)< \phi _t(1)< \cdots <\phi _t(N_t -1)\). For \(k \in \{ 0, \cdots , N_t -1\}\), the sample quantiles at the observed rank are \(\hat{\lambda }_t(k/N_t) = \phi _t(k)\). According to these quantiles, we approximate the uth quantile of \(N_t\) using the following equation for any \(u \in ( 0, 1)\):

where \(k_t^* = \lfloor u N_t \rfloor \) and \(\lfloor \cdot \rfloor \) indicates the integer part. The empirical counterparts of \(m_\theta (u)\) and \(\tilde{m}_\theta (u)\) are

and we compute \(\hat{m}_\theta (u)\) and \(\hat{\tilde{m}}_\theta (u)\) at any rank u and \(\theta \). Assuming \(u_0 = 0\) and \(u_K = 1\), we approximate

We estimate the parameters \(\theta \) by minimizing the sum of two quantiles,

1.4 Appendix D: Levinsohn and Petrin (2003) approach

We here present the estimation methodology proposed by Levinsohn and Petrin (2003). This method takes account of the endogeneity problem that capital inputs and productivity are correlated. According to Levinsohn and Petrin (2003), the production function is represented as \(v_{it} = \beta _k k_{it} + \beta _l l_{it} + \varepsilon _{it}\), where \(\varepsilon _{it} = \phi _{it} + e_{it}\), and \(e_{it}\) is the error term that cannot be observed. \(\phi _{it}\) is likely to be correlated with the capital inputs. In addition, \(\phi _{it}\) has a positive relationship with intermediate inputs \(m_{it}\), \(m_{it} = g(k_{it},\phi _{it})\). This can be inverted \(\phi _{it} = h(m_{it}, k_{it})\). Substituting this into production function leads to \(v_{it} = \beta _l l_{it} + \Phi (k_{it}, m_{it}) + e_{it}\), where \( \Phi (k_{it},m_{it}) = \beta _k k_{it} +h(m_{it}, k_{it}) \). \( \Phi (k_{it},m_{it})\) is replaced with a multi-order polynomial in \(m_{it}\), \(k_{it}\), and \(\hat{\Phi }\). Then, this equation can be estimated by OLS. In addition, \(\phi _{i,t-1}\) can be approximated by \(\Phi (k_{i,t-1}, m_{i,t-1}) -\beta _k k_{i,t-1}\). From the above, the production function is rewritten as \(v_{it} = \beta _l l_{it} + \gamma (\hat{\Phi }(k_{i,t-1},m_{i,t-1}) - \beta _k k_{i,t-1}) + e_{it}\), where \(\gamma (\cdot )\) is an approximated term. This equation is estimated by nonlinear least squares, and \(k_{it}\) does not have a correlation with the error term. Hence, we obtain consistent estimates of the production function coefficients.

1.5 Appendix E: TFP

In the analysis, we used the estimation results mainly based on Levinsohn and Petrin (2003). Another representative method is to use the method proposed by Wooldridge (2009). Using the generalized method of moments approach, Levinsohn and Petrin (2003) build the identification production function following Olley and Pakes (1996), whereas Wooldridge (2009) proposes a single-equation instrumental variable approach to control for the correlation between the inputs and unobserved productivity of establishments. Table 8 shows the estimation results of the production function derived using the Levinsohn and Petrin (2003) and Wooldridge (2009) approaches as well as OLS and OLS with fixed effects. The coefficients of \(\ln k\) and \(\ln l\) of both the Levinsohn and Petrin (2003) and the Wooldridge (2009) approaches are almost the same. They also have the expected signs and are statistically significant at the 1% level.

Using the data on the TFP of each establishment \(i=1,2,...\), simple and weighted average \(\ln \) TFPs in the industry at year t are calculated by \(TFP_t=\sum _i \ln TFP_{ti}\) and \(TFP_t=\sum _i \theta _{it} \ln TFP_{ti}\), where \(\theta _{it}\) is the added-value share of establishment i in year t.

-

1.6 Appendix F: Descriptive statistics of the productivity distribution

Table 9 presents the descriptive statistics of the productivity distribution. Between 1986 and 2014, productivity increased by 36% from 1.160 to 1.576 at the 10th percentile. On the contrary, the productivity rise at the 90th percentile remained at 11.7% from 3.42 to 3.82. This implies that the increase in productivity in firms with low productivity was relatively large and that the productivity gap between firms narrowed. This can also be confirmed by reading the table from left to right. In 1986, productivity at the 90th percentile was 2.95 times greater than that at the 10th percentile. That figure was 2.42 in 2014.

Rights and permissions

About this article

Cite this article

Adachi, Y., Ogawa, H. & Tsubuku, M. Measuring productivity dynamics in Japan: a quantile approach. Empir Econ 63, 201–242 (2022). https://doi.org/10.1007/s00181-021-02136-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-021-02136-x