Abstract

Monetary policy rules describe how policy interest rates respond to macroeconomic developments. These rules incorporate forward-looking models that require instruments for consistent estimation. The use of standard instruments leads to weak identification of forward-looking rules. We combine principal component analysis with hard thresholding to construct new instruments based on high-dimensional macro data. Component-based instruments enhance the identification of policy rules relative to standard results. The finding is attributed to specific variables in the data.

Similar content being viewed by others

Notes

The focus is on the identification of single-equation models, namely monetary policy rules. See Dufour et al. (2013) for discussion on identification and inference in single- versus multi-equation systems.

Mavroeidis (2010), Inoue and Rossi (2011), and Mirza and Storjohann (2014) examine the monetary policy rule; Mavroeidis (2004), Dufour et al. (2006), Nason and Smith (2008), and Kleibergen and Mavroeidis (2009) discuss the New Keynesian Phillips Curve (NKPC); Lubik and Schorfheide (2004) and Canova and Sala (2009) focus on dynamic stochastic general equilibrium (DSGE) models.

The nested model is more general than previous robust applications to policy rules; Mavroeidis (2010), Inoue and Rossi (2011), and Mirza and Storjohann (2014) use pure partial adjustment models that omit residual serial correlation. For studies that extend the partial adjustment structure with indicator variables for omitted shocks, see Gerlach-Kristen (2004) and Bayar (2015).

Weak identification of the policy rule is attributed to instrument weakness, in line with Mirza and Storjohann (2014) and Bayar (2018), which is not uncontroversial. Mavroeidis (2010) argues that adherence to Taylor-rule principle may dampen self-fulfilling dynamics and mitigate the effect of various shocks on inflation and output gap. The decline in the volatility of these two variables may then lead to identification weakness in the policy rule.

The estimated model uses end-of-quarter data for the policy rate \({i}_{t}\). As a result, \({\pi }_{t}\) and \({y}_{t}\) are exogenous since they are known at the time \({i}_{t}\) is set.

Kleibergen and Mavroeidis (2009) describe newer methods in the generalized method of moments (GMM) context: S statistic from Stock and Wright (2000), generalization of AR test to GMM; KLM statistic from Kleibergen (2005); JKLM statistic, difference between S and KLM statistics; and MQLR statistic, extension of likelihood ratio test from Moreira (2003) to GMM.

Dufour and Taamouti (2007) demonstrate that newer methods are subject to large size distortions such that the issue of missing instruments may be as important empirically as the issue of weak instruments. Dufour (2003, 2009) present further discussion on the advantages of AR test relative to newer methods.

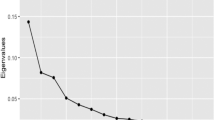

Jolliffe (2002) describes how to derive components from eigenvalues and eigenvectors of the variance–covariance matrix. Bro and Smilde (2014) present further analysis. Bontempi and Mammi (2015) consider an application in which lagged values of endogenous variables are treated as the large instrument set to be reduced.

Bernanke and Boivion (2003) and Favero et al. (2005) present factor-based applications to obtain point estimates, while Mirza and Storjohann (2014) use factor analysis to report robust confidence regions. Although the latter paper shares similarities with the present study, it does not address the issue of instrument abundance; it relies on the KLM statistic that is susceptible to missing instruments; and it uses a partial adjustment model disregarding serial correlation in errors, which is common in time-series macro data.

Bai and Ng (2009) provide details on instrument selection on the basis of hard thresholding.

To be consistent with the GDP gap measure, unemployment gap is defined as natural rate minus actual rate so that a negative gap corresponds to economic slack. The robust region is bounded at \({b}_{y}=2.4\) on the vertical axis, which is not incompatible with estimates from the literature.

Survey data may further enhance the precision of policy rule estimates, particularly the inflation coefficient. On this issue, Ang et al. (2007) state that inflation surveys outperform out-of-sample forecasts in time-series and term structure models, while Adam and Padula (2011) report that data from the Survey of Professional Forecasters generate plausible estimates for the forward‐looking NKPC.

References

Adam K, Padula M (2011) Inflation Dynamics and subjective expectations in the United States. Econ Inq 49:13–25

Anderson T, Rubin H (1949) Estimation of the parameters of a single equation in a complete system of stochastic equations. Ann Math Stat 20:46–63

Ang A, Bekaert G, Wei M (2007) Do Macro variables, asset markets, or surveys forecast inflation better? J Monet Econ 54:1163–1212

Bai J, Ng S (2006) Confidence intervals for diffusion index forecasts and inference for factor-augmented regressions. Econometrica 74:1133–1150

Bai J, Ng S (2008) Forecasting economic time series using targeted predictors. J Econom 146:304–317

Bai J, Ng S (2009) Selecting instrumental variables in a data rich environment. J Time Ser Econom 1:1–32

Bai J, Ng S (2010) Instrumental variable estimation in a data rich environment. Economet Theor 26:1577–1606

Bayar O (2014) Temporal aggregation and estimated monetary policy rules. B.E J Macroecon 14:553–577

Bayar O (2015) An ordered probit analysis of monetary policy inertia. B.E J Macroecon 15:705–726

Bayar O (2018) Weak instruments and estimated monetary policy rules. J Macroecon 58:308–317

Bernanke B, Boivion J (2003) Monetary policy in a data-rich environment. J Monet Econ 50:525–546

Bontempi M, Mammi I (2015) Implementing a strategy to reduce the instrument count in panel GMM. Stand Genomic Sci 15:1075–1097

Bro R, Smilde A (2014) Principal component analysis. Anal Methods 6:2812–2831

Canova F, Sala L (2009) Back to square one: identification issues in DSGE models. J Monet Econ 56:431–449

Clarida R, Gali J, Gertler M (2000) Monetary policy rules and macroeconomic stability: evidence and some theory. Quart J Econ 115:147–180

Coibion O, Gorodnichenko Y (2012) Why are target interest rate changes so persistent? Am Econ J Macroecon 4:126–162

Consolo A, Favero C (2009) Monetary policy inertia: more a fiction than a fact? J Monet Econ 49:1161–1187

Dufour J (2003) Identification, weak instruments, and statistical inference in econometrics. Can J Econ 36:767–808

Dufour J (2009) Comment on weak instrument robust tests in GMM and the new Keynesian Phillips curve. J Bus Econ Stat 27:318–321

Dufour J, Taamouti M (2007) Further results on projection-based inference in IV regressions with weak, collinear, or missing instruments. J Econom 139:133–153

Dufour J, Khalaf L, Kichian M (2006) Inflation dynamics and the new Keynesian Phillips curve: an identification robust econometric analysis. J Econ Dyn Control 30:1707–1727

Dufour J, Khalaf L, Kichian M (2013) Identification-robust analysis of DSGE and structural macroeconomic models. J Monet Econ 6:340–350

English W, Nelson W, Sack B (2003) Interpreting the significance of the lagged interest rate in estimated monetary policy rules. B.E J Macroecon 3:1–16

Favero C, Marcellino M, Neglia F (2005) Principal components at work: the empirical analysis of monetary policy with large data sets. J Appl Econom 20:603–620

Gerlach-Kristen P (2004) Interest-Rate smoothing: monetary policy inertia or unobserved variables? B.E J Macroecon 4:1–17

Inoue A, Rossi B (2011) Identifying the sources of instabilities in macroeconomic fluctuations. Rev Econ Stat 93:1186–1204

Jolliffe I (2002) Principal component analysis. Springer Series in Statistics. Springer, New York

Kapetanios G, Marcellino M (2010) Factor-GMM estimation with large sets of possibly weak instruments. Comput Stat Data Anal 54:2655–2675

Kapetanios G, Khalaf L, Marcellino M (2016) Factor-based identification-robust interference in IV regressions. J Appl Econom 31:821–842

Kleibergen F (2002) Pivotal statistics for testing structural parameters in instrumental variables regression. Econometrica 70:1781–1803

Kleibergen F (2005) Testing parameters in GMM without assuming that they are identified. Econometrica 73:1103–1124

Kleibergen F, Mavroeidis S (2009) Weak instrument robust tests in GMM and the new Keynesian Phillips curve. J Bus Econ Stat 27:293–311

Lubik T, Schorfheide F (2004) Testing for indeterminacy: an application to U.S Monetary policy. Am Econ Rev 94:190–217

Mavroeidis S (2004) Weak identification of forward-looking models in monetary economics. Oxford Bull Econ Stat 66:609–635

Mavroeidis S (2010) Monetary policy rules and macroeconomic stability: some new evidence. Am Econ Rev 100:491–503

Mirza H, Storjohann L (2014) Making weak instrument sets stronger: factor-based estimation of inflation dynamics and a monetary policy rule. J Money Credit Bank 46:643–664

Moreira M (2003) A conditional likelihood ratio test for structural models. Econometrica 71:1027–1048

Nason J, Smith G (2008) Identifying the new Keynesian Phillips curve. J Appl Econom 23:525–551

Orphanides A (2001) Monetary policy rules based on real-time data. Am Econ Rev 91:964–985

Roodman D (2009) A note on the theme of too many instruments. Oxford Bull Econ Stat 71:135–158

Rudebusch G (2002) Term structure evidence on interest rate smoothing and monetary policy inertia. J Monet Econ 49:1161–1187

Rudebusch G (2006) Monetary policy inertia: fact or fiction? Int J Cent Bank 2:85–135

Sack B, Wieland V (2000) Interest-rate smoothing and optimal monetary policy: a review of recent empirical evidence. J Econ Bus 52:205–228

Schneeweiss H (1997) Factors and principal components in the near spherical case. Multivar Behav Res 32:375–401

Schneeweiss H, Mathes H (1995) Factor analysis and principal components. J Multivar Anal 55:105–124

Stock J, Wright J (2000) GMM with weak identification. Econometrica 68:1055–1096

Stock J, Watson M (2009) Forecasting in dynamic factor models subject to structural instability. In: The methodology and practice of econometrics, A Festschrift in Honour of Professor David F. Hendry. Oxford University Press, Oxford

Stock J, Yogo M (2005) Testing for weak instruments in linear IV regression. Identification and inference for econometric models. Cambridge University Press, New York

Stock J, Wright J, Yogo M (2002) A survey of weak instruments and weak identification in generalized method of moments. J Bus Econ Stat 20:518–529

Wang J, Zivot E (1998) Inference on structural parameters in instrumental variables regression with weak instruments. Econometrica 66:1389–1404

Woodford M (2003) Interest and prices: foundations of a theory of monetary policy. Princeton University Press, Princeton

Wooldridge J (2002) Econometric analysis of cross section and panel data. MIT Press, Cambridge

Wu J, Xia F (2016) Measuring the macroeconomic impact of monetary policy at the zero lower bound. J Money Credit Bank 48:253–291

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

I am grateful to session participants at the Southern Economic Association and Midwest Econometrics Group meetings for helpful comments.

Appendix

Appendix

Are component-based instruments valid for the AR test? Kapetanios et al. (2016), KKM hereafter, answer in the affirmative in an extended AR test where factor-based instruments are estimated via principal components that achieve size control under standard regularity conditions.

The proof builds on Eqs. (6) and (7), where \(X\) is dropped for notational convenience. The AR statistic for the null hypothesis \(b={b}_{h}\) in the structural equation is:

where \(M\left( K \right) = I - N\left( K \right)\) and \(N\left( K \right) = K\left( {K^{\prime}K} \right)^{ - 1} K^{\prime}\) for any full-column rank matrix \(K\).

KKM modify the AR test to accommodate the common factors of a dataset. In this context, if \(F\) is a \(T\times r\) matrix of factors, the AR statistic takes the following form.

Suppose that \(\widehat{F}\) is a \(T\times r\) matrix of leading principal components of this dataset. It can be shown that \(AR\left({b}_{h}|F\right)\) and \(AR\left({b}_{h}|\widehat{F}\right)\) are asymptotically equivalent so that factors can be replaced by their component-based estimates.

To prove \(AR\left({b}_{h}|F\right)-AR\left({b}_{h}|\widehat{F}\right)={o}_{p}\left(1\right)\) requires that:

which satisfies if:

under the null hypothesis and

under the alternative hypothesis for any non-singular rotation matrix \(H\).

The above expressions hold if the following is satisfied.

KKM show that these three conditions are met if factors \(F\), endogenous variables \(Y\), and the structural error \(v\) have finite fourth moments, a non-singular covariance matrix, and satisfy the central limit theorem. These in turn hold under Assumptions 1–3 from KKM and Lemma A.1 from Bai and Ng (2006).

See Figs. 9, 10, 11, 12, and 13.

All weights in components 1 and 2. Figure plots weights on 109 macro variables for components 1 and 2. Variable codes are from Stock and Watson (2009)

All weights in components 4 and 5. Figure plots weights on 109 macro variables for components 4 and 5. Variable codes are from Stock and Watson (2009)

All weights in components 7 and 8. Figure plots weights on 109 macro variables for components 7 and 8. Variable codes are from Stock and Watson (2009)

All weights in components 11 and 13. Figure plots weights on 109 macro variables for components 11 and 13. Variable codes are from Stock and Watson (2009)

All weights in components 14 and 15. Figure plots weights on 109 macro variables for components 14 and 15. Variable codes are from Stock and Watson (2009)

Rights and permissions

About this article

Cite this article

Bayar, O. Reducing large datasets to improve the identification of estimated policy rules. Empir Econ 63, 113–140 (2022). https://doi.org/10.1007/s00181-021-02134-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-021-02134-z

Keywords

- Forward-looking rule

- Instrument weakness

- Robust estimation

- Instrument abundance

- Principal component analysis

- Hard thresholding