Abstract

This paper takes an innovative look at the relationship between commodity futures prices and speculation. Contrary to other studies, we analyze the effect of speculation on temporary and permanent futures price shocks estimated from a cointegrated system of pairwise short- and long-dated contracts. Where cointegration is found, the long-term equilibrium is determined by the long-dated contract, while the adjustment toward equilibrium is restored by the short-dated contract (except for cotton). Granger causality tests cannot reject the null hypothesis that speculation as measured by Working’s T index has no effect on squared permanent price shocks for 7 out of 9 commodities. Where the null hypothesis is rejected, the relationship exhibits a negative sign, i.e., speculation has a stabilizing effect.

Similar content being viewed by others

Notes

The most advanced statistical analysis of grain prices surrounding the Berlin prohibition was applied by Hooker (1901), a forerunner of modern time series analysis.

Actually, the position data used in the literature and in this study do not classify speculative and hedging positions, but commercial and non-commercial (and more recently: index) positions.

As discussed below, with the recent availability of data from the disaggregated data available from CFCT’s large trader reporting system (LTRS), future studies should be able to analyze the maturity breakdown of speculative positions and to address this point directly.

Commodity futures prices are non-stationary, which are empirically validated for the price series used in our tests.

An alternative explanation could be found in Friedman-style speculation effects pushing short-run asset prices to long-run fundamental values; see Friedman (1953). However, since we do not address questions related to long-run fundamental price determination in this paper, intertemporal arbitrage seems to be a more adequate framework for motivating cointegration of long- and short-dated futures prices.

The motivation for using squared shocks is given in Sect. 4.2 and has to do with the interpretation of the Working’s T index.

Some 95% of the index funds replicate the SP-GSCI or the DJ-UBS indices.

Weekly statistics on disaggregated long/short positions on 12 agricultural futures positions by index traders, commercial traders, and non-commercial traders are published in the “Commodity Index Traders” (CIT) report by the CFTC. Tang and Xiong (2010) report an average relative share of 28.4% in the long and 1.6% in the short positions relative to the total open interest across all commodities (Table 2). However, as discussed below, the amount of index trading itself is not a relevant indicator of net speculation.

See the U.S. Senate Permanent Subcommittee on Investigations in its examination of Chicago Board of Trade’s (CBOT) wheat futures trading, released on June 23, 2009. The report concludes that the activities of commodity index traders, in the aggregate, constituted excessive speculation in the wheat market under the Commodity Exchange Act.

A detailed discussion and critical assessment of many popular arguments about the destabilizing effect speculation are provided by Irwin et al. (2009).

The reports include information about open futures positions of five trader categories: large non-commercials (speculators), large commercials (hedgers), large non-commercial spread investors, commodity index traders, and non-reportable traders (small speculative and hedging positions).

A list of earlier studies with this finding can be found in Sanders et al. (2010, p. 85). The CIT database is also used by Stoll and Whaley (2010) to investigate Granger causality between index fund trading and commodity futures prices. The authors examine weekly data of 12 agricultural markets from 2006 to 2009 and find only little impact of commodity index investing on futures prices.

Historical data files for the COT Futures-Only reports are available from 1986, and the Futures-and-Options-Combined report since 1995.

As discussed by Stoll and Whaley (2010), the CFTC supplemental report contains separate index positions since 2006.

The reason for using squared innovations is related to our speculation measure and is explained in Sect. 4.2 below.

Since January 2007, the CFTC publishes a supplemental COT report (SCOT) which releases the positions of index traders separately from the non-commercial and commercial positions; the non-reportable positions are not affected. The impact of the re-classification on different speculation proxies is discussed, e.g., in Haase et al. (2017).

The results are available upon request.

We use a somehow loose but more readable terminology in discussing the results; of course, futures prices are cointegrated, not commodities.

In the restricted model, the insignificant adjustment coefficient of the unrestricted model is set equal to zero. The estimation results of the unrestricted model are available upon request; in terms of statistical significance, the results are not different.

In case of two lags: the cumulative coefficients.

The spot price is typically not observable for commodities; it is therefore common practice to use the price of the nearby contract, i.e., the contract with the shortest time to maturity, as a proxy.

The non-commercials also include spread positions, which, however, do not affect the speculation index because they are market neutral.

References

Aulerich NM, Irwin SH, Garcia P (2010) The price impact of index funds in commodity futures markets: evidence from the cftc’s daily large trader reporting system. Working paper, Department of Agricultural and Consumer Economics, University of Illinois at Urbana-Champaign

Baffes J, Haniotis T (2010) Placing the 2006/08 commodity price boom into perspective. World Bank policy research working paper

Brunetti C, Büyükşahin B (2009) Is speculation destabilizing? In: Working paper, Commodity Futures Trading Commission (CFTC)

Büyükşahin B, Harris JH (2011) Do speculators drive crude oil futures prices? Energy J 32(2):167–202

Cooke B, Robles M (2009) Recent food price movements: a time series analysis. In: Discussion paper, International Food Policy Research Institute (IFPRI)

Fattouh B, Kilian L, Mahadeva L (2012) The role of speculation in oil markets: What have we learned so far? CEPR Discussion Paper No. 8916

Figuerola-Ferretti I, Gonzalo J (2010) Modelling and measuring price discovery in commodity markets. J Econom 185(1):95–107

Friedman M (1953) The case for flexible exchange rates. In: Essays in positive economics. University of Chicago Press, Chicago, pp 157–203

Fröchtling A (1909) Ueber den Einfluss des Getreideterminhandels auf die Getreidepreise. Jahrbücher für Nationalökonomie und Stat/J Econ Stat 37(5):577–622

Gilbert CL (2010) Speculative influences on commodity futures prices 2006–2008. UNCTAD Discussion Paper No. 197

Gonzalo J, Granger CWJ (1995) Estimation of common long-memory components in cointegrated systems. J Bus Econ Stat 13:27–35

Gonzalo J, Ng S (2001) A systematic framework for analyzing the dynamic effects of permanent and transitory shocks. J Econ Dyn Control 25(10):1527–1546

Haase M, Seiler Y, Zimmermann H (2017) Commodity returns and their volatility in relation to speculation: a consistent empirical approach. J Altern Invest 20(Fall):76–91

Hailu G, Weersink A (2010). Commodity price volatility: the impact of commodity index traders. In: Working paper, Canadian Agricultural Trade Policy and Competitiveness Research Network (CATPRN)

Hamilton JD (2009) Understanding crude oil prices. Energy J 20(2):179–206

Hooker RH (1901) The suspension of the Berlin Produce Exchange and its effect upon corn prices. J R Stat Soc 64(4):574–613

IOSCO (2009) Task force on commodity futures markets: final report. Technical Committee of the International Organization of Securities Commissions

Irwin SH, Sanders DR (2010) The impact of index and swap funds in commodity futures markets. In: A technical report prepared for the Organization on Economic Co-operation and Development (OECD)

Irwin SH, Sanders DR (2011) Index funds, financialization, and commodity futures markets. Appl Econ Perspect Policy 33(1):1–31

Irwin SH, Sanders DR, Merrin RP (2009) Devil or angel? The role of speculation in the recent commodity price boom (and bust). J Agric Appl Econ 41:393–402

Jacks DS (2007) Populists versus theorists: futures markets and the volatility of prices. Econ Hist 44:342–362

Masters MW (2008) Testimony before the committee on homeland security and governmental affairs. United States Senate, 20/05/08

Sanders DR, Irwin SH, Merrin RP (2010) The adequacy of speculation in agricultural futures markets: too much of a good thing? Appl Econ Perspect Policy 32(1):77–94

Schliep K (1912) Der börsenmässige Zeithandel in Getreide und Erzeugnissen der Getreidemüllerei. Greifswald: Dissertation, Buchdruckerei Hans Adler

Soros G (2008) The perilous price of oil. The New York Review of Books, August, 27 2008

Stoll HR, Whaley RE (2010) Commodity index investing and commodity futures prices. J Appl Finance 20, 7–46

Szado E (2011) Defining speculation: the first step toward a rational dialogue. J Altern Invest 14(1):75–82

Tang K, Xiong W (2010) Index investment and financialization of commodities. Working paper

Tang K, Xiong W (2012) Index investment and the financialization of commodities. Financ Anal J 68(5):54–74

Till H (2009) Has there been excessive speculation in the us oil futures markets? What can we (carefully) conclude from new CFTC data? Working paper, EDHEC Risk Institute

Till H (2011) A review of the G20 meeting on agriculture: addressing price volatility in the food markets. In: Position paper, EDHEC Risk Institute

UNCTAD (2011) Price formation in financialized commodity markets: the role of information. United Nations

Working H (1960) Speculation on hedging markets. Food Res Inst Stud 1:185–220

Author information

Authors and Affiliations

Corresponding author

Additional information

We acknowledge the critical comments and suggestions of two anonymous referees of this Journal who have improved the paper substantially. An earlier version of the paper was presented in seminars at the Swiss Bankers Association (SBVg), the Swiss Financial Market Supervisory Authority (FINMA), and the Economics Lunch at the Bank of International Settlements (BIS).

Appendix A: Data sources and construction

Appendix A: Data sources and construction

1.1 A.1 Futures Prices

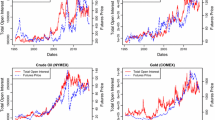

Monthly futures price series are constructed in the following way: The short-dated futures prices reflect a rolling futures strategy with the shortest available contractFootnote 24. The long-dated futures price series is constructed analogously, but uses contracts expiring one year ahead of the nearby maturity. The contracts are rolled into the next available maturity in the month where the shortest contract expires; a fixed business day is selected for the rollover. The roll schedule applied to each commodity is available upon request. The selected time spread of exactly one-year controls for seasonalities in the term structure of commodity futures prices; i.e., by rolling the contracts, seasonal price “jumps” vanish because the contracts exhibit the same expiration month. All prices are denoted in US dollars and were downloaded from Thomson Reuters Datastream.

1.2 A.2 Speculation

The data used to calculate the T index are provided by the Commitments of Traders (COT) report released by the U.S. Commodity Futures Trading Commission (CFTC). It contains the allocation of open interest on each Thursday for markets in which 20 or more traders hold positions equal to or above the reporting levels established by the CFTC. Two main classifications are released: the Commitments of Traders Futures-Only Report contains futures market open interest only. Historical data files are available from 1986. Since March 14, 1995 the Futures-and-Options-Combined Report provides an aggregation of futures market open interest and delta-weighted option market open interest. The published open interest for each market is aggregated across all contract maturities in both reports. All data are released on Friday at 3:30 p.m. However, only mid-month and month-end data were provided by the COT before September 30, 1992. We combine the data from the two reports to construct a single time series for each commodity.

Both reports classify the positions into commercials, non-commercials, and non-reported. For each group, the respective number of long and short contracts is reported separately.Footnote 25 The aggregate of all long and short positions add up to the market’s total open interest.

Following common practice in the empirical literature, “commercials” are considered as hedgers, whereas “non commercials” are classified as speculators. However, the group of non-reporting traders cannot be easily classified as hedgers or speculators without strong assumptions. Sanders et al. (2010) point out that the speculation index is not particularly sensitive to the assignment of the non-reporting traders. For that reason, this group is omitted in computing our T index.

Rights and permissions

About this article

Cite this article

Haase, M., Seiler Zimmermann, Y. & Zimmermann, H. Permanent and transitory price shocks in commodity futures markets and their relation to speculation. Empir Econ 56, 1359–1382 (2019). https://doi.org/10.1007/s00181-017-1387-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-017-1387-2