Abstract

This paper analyses bank balance sheet data in conjunction with macroeconomic and other financial variables. Our aim is to understand the nature of the instability in financial intermediation in the euro area during the recent financial crises. We define “large changes” as significant departures in the actual evolution of balance sheet variables during the crisis from their historical association with the business and financial cycles. In the course of the global 2008–2009 financial crisis, such “large changes” were features of the behaviour of cross-border inter-bank flows, both within the euro area and between the euro area and the rest of the world. By contrast, retail assets and liabilities, as well as inter-bank flows among banks of the same country, did not significantly deviate from historical regularities. Since the euro area sovereign crisis of 2011–2012, “large changes” have been more pervasive. In particular, a significant home bias in the sovereign bond market has emerged.

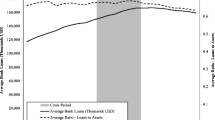

Source: ECB

Source: ECB

Similar content being viewed by others

Notes

See ECB (2014) for an extensive discussion and survey of the literature on the determinants of sovereign bond yields before and after the sovereign debt crisis.

Regulation (EC) No XX/2013 of the ECB of 24 September 2013 concerning the balance sheet of the monetary financial institutions sector (Recast), OJ L 15, 7.11.2013, p. 14.

The data used in the paper relate to notional stocks, which are constructed based on measure of transactions and therefore are corrected for series breaks arising, e.g. from mergers and acquisitions or changes in the classification of counterparties (see the “Annex” for further discussion).

As hyperpriors for \(\lambda , \mu \) we choose Gamma densities with mode equal to 0.2, 1 and standard deviations equal to 0.4, 1 respectively. Our prior on \(\psi \), i.e. the prior mean of the main diagonal of \(\Sigma \), is an inverse Gamma with scale and shape equal to \((0.02)^{2}\).

See Giannone et al. (2015) for the details of the MCMC algorithm.

In this paper, we use the simulation smoother described in Carter and Kohn (1994).

While loans to other counterparties can also be object of securitisation activities, these are not reflected in the paper as they are assumed to have lower magnitude compared to the impact securitisation has on loans to non-financial sectors.

References

Abbassi P, Bräuning F, Fecht F, Peydró JL (2015) Cross-border liquidity, relationships and monetary policy: evidence from the Euro area interbank crisis. CEPR discussion papers 10479

Abbassi P, Fecht F, Weber P (2013) How stressed are banks in the interbank market?. Deutsche Bundesbank discussion paper no. 40/2013

Acharya VV, Steffen S (2015) The greatest carry trade ever? Understanding Eurozone bank risks. J Financ Intermed 115:215–236

Angelini P, Grande G, Panetta F (2014) The negative feedback loop between banks and sovereigns. Banca d’Italia occasional paper no. 213

Banbura M, Giannone D, Reichlin L (2010) Large Bayesian VARs. J. Appl Econ 25:71–92

Banbura M, Giannone D, Lenza M (2015) Conditional forecasts and scenario analysis with vector autoregressions for large cross-sections. Int J Forecast 31(3):739–756

Battistini N, Pagano M, Simonelli S (2013) Systemic risk, sovereign yields and bank exposures in the euro crisis. CSEF University of Naples, Naples

Becker B, Ivashina V (2014) Financial repression in the European sovereign debt crisis. Swedish House of Finance research paper no. 14-13

Bindseil U, Cour-Thimann P, König P (2012) Target2 and cross-border interbank payments during the financial crisis. CESifo Forum, Ifo Institute - Leibniz Institute for Economic Research at the University of Munich, vol 13 (SPECIALIS), pp 83–92, 02

Caballero RJ (2009) Sudden financial arrest. IMF Mundell-Flemming lecture, MIT Department of Economics working paper no. 09-29

Calvo GA, Reinhart C (2000) When capital inflows come to a sudden stop: consequences and policy options. In: Kenen P, Swoboda A (eds) Reforming the international monetary and financial system. International Monetary Fund, Washington, pp 214–265

Carter CK, Kohn R (1994) On Gibbs sampling for state-space models. Biometrika 81:541–553

Colangelo A, Lenza M (2012) Cross-border banking transactions in the euro area. IFC Bull 36:518–531

De Mol C, Giannone D, Reichlin L (2008) Forecasting using a large number of predictors: is Bayesian shrinkage a valid alternative to principal components? J Econ 146(2):318–328 (Elsevier)

Doan T, Litterman R, Sims CA (1984) Forecasting and conditional projection using realistic prior distributions. Econ Rev 3:1–100

ECB (2014) The determinants of euro area sovereign bond yield spreads during the crisis. Monthly Bulletin Article, pp 67–83

Garcia-de-Andoain C, Hoffmann P, Manganelli S (2014) Fragmentation in the Euro overnight unsecured money market. Econ Lett 125(2):298–302

Garicano L, Reichlin L (2014) A safe asset for Eurozone QE: A proposal. http://www.voxeu.org/article/safe-asset-eurozone-qe-proposal

Giannone D, Lenza M, Pill H, Reichlin L (2012a) The ECB and the interbank market. Econ J 122:467–486

Giannone D, Lenza M, Reichlin L (2012b) Money, credit, monetary policy and the business cycle in the Euro area. Working papers ECARES ECARES 2012-008, ULB—Universite Libre de Bruxelles

Giannone D, Lenza M, Primiceri G (2015) Prior selection for vector autoregressions. Rev Econ Stat 97(2):436–451

Hartmann P, Maddaloni A, Manganelli S (2003) The euro area financial system: structure, integration and policy initiatives. ECB working paper no. 230

Heider F, Hoerova M, Holthausen C (2009) Liquidity hoarding and interbank market spreads: the role of counterparty risk. ECB work paper no. 1126

Lenza M, Pill H, Reichlin L (2010) Monetary policy in exceptional times. Econ Policy 62:295–339

Litterman R (1979) Techniques of forecasting using vector autoregressions. Federal reserve of minneapolis working paper 115

McKinnon RI, Pill H (1997) Credible economic liberalizations and overborrowing. Am Econ Rev 87(2):189–193

McKinnon RI, Pill H (1998) The overborrowing syndrome: are East Asian economies different? In: Glick R (ed) Managing capital flows and exchange rates: lessons from the Pacific Basin. Cambridge University Press, Cambridge, pp 322–355

Peersman G (2011) Macroeconomic effects of unconventional monetary policy in the euro area. CEPR discussion paper no. 8348

Reichlin L (2014) Monetary policy and banks in the euro area: the tale of two crises. J Macroecon 39:387–400

Reinhardt D, Riddiough SJ (2014) The two faces of cross-border banking flows: an investigation into the links between global risk, arms-length funding and internal capital markets. Bank of England working paper 498

Author information

Authors and Affiliations

Corresponding author

Additional information

The views expressed in this paper are those of the authors and do not necessarily reflect the position of the European Central Bank, the Eurosystem, the Federal Reserve Bank of New York, the Federal Reserve System or Goldman Sachs.

Electronic supplementary material

Below is the link to the electronic supplementary material.

Data annex

Data annex

Our dataset includes 22 bank balance sheet variables and 12 macroeconomic and financial variables of the euro area. All variables are available at the monthly frequency and the sample ranges from January 1999 to October 2015. The bank balance sheet series are from the dataset on Monetary Financial Institutions (MFIs) balance sheet statistics compiled by the European Central Bank. The macroeconomic and financial block of the database consists of variables drawn from the Statistical Data Warehouse of the European Central Bank.

As regards the balance sheet data, the aggregations we use in the data analysis are constructed from the main instrument categories, by grouping sectors of the counterparties to yield information on MFI positions vis-à-vis euro area residents, and specifically the Eurosystem, other MFIs, financial corporations other than MFIs, the government sector, firms and households, and the rest of the world. Special attention is paid to the so-called euro area wholesale lending market, which is defined as the lending market where MFIs operate along with financial intermediaries other than MFIs. Those consist of insurance corporations, pension funds, non-MMF investment funds, other financial intermediaries (including captive financial institutions and money lenders) and financial auxiliaries.

In addition, MFI balance sheet statistics allow the split between intra-euro area domestic and cross-border positions, and we take these breakdowns into account when studying inter-MFI positions. With this respect it is worth stressing that the operational framework of the Eurosystem provides that monetary policy operations are always conducted via the relevant NCB; the resulting positions are thus to be considered, by definition, domestic.

When analysing developments in MFI loans to firms and households, we also take into account the impact of loan securitisation (and other loan transfers) on MFI balance sheets.Footnote 7

On this basis, the variables employed in the empirical analysis in the main text are:

Bank assets

-

Loans to euro area firms and households

-

Loans to euro area government

-

Deposit and loan claims on the Eurosystem

-

Domestic loans to MFIs

-

Intra-euro area cross-border loans to MFIs

-

Other euro area wholesale loans (This series covers both domestic and intra-euro area cross-border positions vis-à-vis insurance corporations, pension funds, non-MMF investment funds, other financial intermediaries (including captive financial institutions and money lenders) and financial auxiliaries.)

-

Loans to non-euro area residents

-

Domestic holdings of government debt securities

-

Intra-euro area cross-border holdings of government debt securities

-

Holdings of euro area MFI securities

-

Holding of securities issued by the euro area private sector

-

Holdings of debt securities issued by non-euro area residents

-

Holdings of equity issued by non-euro area residents

-

Remaining assets

Bank liabilities

-

Deposits of euro area firms and households

-

Deposits of euro area government

-

Deposit and loan liabilities to the Eurosystem

-

Domestic deposits from MFIs

-

Intra-euro area cross-border deposits from MFIs

-

Other euro area wholesale deposits (This series includes deposits and loan liabilities of euro area MFIs (excluding the Eurosystem) vis-à-vis euro area financial intermediaries other than MFIs, i.e. insurance corporations, pension funds, non-MMF investment funds, other financial intermediaries and financial auxiliaries. Long-term deposits vis-a-vis FVCs are however excluded from our exercise as they are usually fictionally imputed to the MFI balance sheet as a balancing liability when loan securitisation activities (or other loan sales) do not result in the de-recognition of the assets).

-

Deposits from non-euro area residents

-

Debt securities issued

The macroeconomic and financial block

-

Industrial production (euro area)

-

Harmonised Index of Consumer prices (euro area), HICP

-

Unemployment rate (euro area)

-

Producer price index (euro area), PPI

-

3-month Euribor rates (euro area)

-

Industrial production (US)

-

Consumer price index (US), CPI

-

Federal Funds rate (US)

-

DJ Eurostoxx (stock prices)

-

Sovereign bond yields, 2 years maturity (euro area)

-

Sovereign bond yields, 5 years maturity (euro area)

-

Sovereign bond yields, 10 years maturity (euro area)

The data enter the VAR model in annual log levels (i.e. 12*log) except the rates (i.e. the Euribor, the Federal Funds rate, the sovereign bond yields and the unemployment rate) which enter the model in levels.

More details on the construction of the data series are available in the web appendix.

Rights and permissions

About this article

Cite this article

Colangelo, A., Giannone, D., Lenza, M. et al. The national segmentation of euro area bank balance sheets during the financial crisis. Empir Econ 53, 247–265 (2017). https://doi.org/10.1007/s00181-016-1221-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-016-1221-2