Abstract

Much of the existing literature on demand for natural gas assumes constant and single-value elasticities, overlooking the possibility of dynamic responses to the changing conditions. We aim to fill this gap by providing individual time series of short-run elasticity estimates based on maximum entropy resampling in a fixed-width rolling window framework. This approach does not only enable taking the variability of the elasticities into account, but also helps obtain more efficient and robust results in small samples in comparison with conventional inferences based on asymptotic distribution theory. To illustrate the methodology, we employ monthly time-series data between 2004 and 2012 and analyze the dynamics of residential natural gas demand in Istanbul, the largest metropolitan area in Turkey. Our findings reveal that the elasticities of the demand model do not remain constant and they are sensitive to the economic situation as well as weather fluctuations.

Similar content being viewed by others

Notes

Due to the size of the literature, a more detailed discussion of the method of bootstrap is outside the scope of the present paper. For more information on bootstrapping, the reader is referred to Efron and Tibshirani (1993) as well as Davison and Hinkley (1997). More details regarding the meboot DGP can be found in Vinod (2006, 2008), Vinod and Lacalle (2009), and Yalta (2013).

Authors’ calculations based on data from the Energy Market Regulatory Authority (2012).

The degree of freedom concern in rolling window estimation requires that we include only one natural gas price and one electricity price variable. In order to determine which lag to use, we tested for different number of lags for up to 6 months as well as no lags and decided for a single lag based on the Akaike information criterion. In all cases that we have tested, there were an equal number of lags for both variables. The estimation results were not sensitive to our lag choice.

Our elasticity estimates were not sensitive to our choosing TAV over HDD, as well as using TAV in levels. We do not include these results for the sake of brevity.

For more information regarding the different bootstrap confidence interval methods, see, for example, Davison and Hinkley (1997).

The computations were performed using R version 3.1.1, the package ‘meboot’ version 1.4-5, the package ‘boot’ version 1.3-13, as well as the package ‘hdrcde’ version 3.1.

References

Adeyemi OI, Broadstock DC, Chitnis M, Hunt LC, Judge G (2010) Asymmetric price responses and the underlying energy demand trend: are they substitutes or complements? Evidence from modelling OECD aggregate energy demand. Energy Econ 32:1157–1164

Adom PK (2013) Time-varying analysis of aggregate electricity demand in Ghana: a rolling analysis. OPEC Energy Rev 37:63–80

Al-Sahlawi MA (1989) The demand for natural gas: a survey of price and income elasticities. Energy J 10:77–87

Amarawickrama HA, Hunt LC (2008) Electricity demand for Sri Lanka: a time series analysis. Energy 33:724–739

Arisoy I, Ozturk I (2014) Estimating industrial and residential electricity demand in Turkey: a time varying parameter approach. Energy 66:959–964

Asche F, Nilsen OB, Tveteras R (2008) Natural gas demand in the European household sector. Energy J 29:27–46

Balcilar M, Ozdemir ZA, Arslanturk Y (2010) Economic growth and energy consumption causal nexus viewed through a bootstrap rolling window. Energy Econ 32:1398–1410

Baumeister C, Peersman G (2013) The role of time-varying price elasticities in accounting for volatility changes in the crude oil market. J Appl Economet 28:1087–1109

Berkhout PHG, Ferrer-I-Carbonell A, Muskens JC (2004) The ex post impact of an energy tax on household energy demand. Energy Econ 26:297–317

Bernstein R, Madlener R (2011) Residential natural gas demand elasticities in OECD countries: an ARDL bounds testing approach. FCN working paper no 15/2011. http://www.eonerc.rwth-aachen.de

Bohi D, Zimmerman MB (1984) An update on econometric studies of energy demand behavior. Annu Rev Energy 9:105–154

Brenton P (1997) Estimates of the demand for energy using cross-country consumption data. Appl Econ 29:851–59

Dagher L (2012) Natural gas demand at the utility level: an application of dynamic elasticities. Energy Econ 34:961–969

Dahl C (1993) A survey of energy demand elasticities in support of the development of the NEMS. MPRA paper no 13962. http://mpra.ub.uni-muenchen.de/13962/

Dahl C (2005) A survey of natural gas demand elasticities. http://www.dahl.mines.edu, mimeo

Dargay JM, Gately D (2010) World oil demand’s shift toward faster growing and less price-responsive products and regions. Energy Policy 38:6261–77

Davison AC, Hinkley DV (1997) Bootstrap methods and their application, 1st edn. Cambridge University Press, Cambridge

Dimitropoulos J, Hunt LC, Judge G (2005) Estimating underlying energy demand trends using UK annual data. Appl Econ Lett 12:239–244

Efron B, Tibshirani RJ (1993) An introduction to the bootstrap, 1st edn. Chapman and Hall, New York

Energy Market Regulatory Authority (EMRA) (2012) Natural gas market 2011 sector report, December 2012. http://www.emra.org.tr/documents/natural_gas/publishments/NaturalGasMarket2011SectorReport_Q9WwGbRxxnRy.pdf

Erdogdu E (2010) Natural gas demand in Turkey. Appl Energy 87:211–219

Gately D, Huntington HG (2002) The asymmetric effects of changes in price and income on energy and oil demand. Energy J 23:19–55

Ghassan HB, Banerjee PK (2014) A threshold cointegration analysis of asymmetric adjustment of OPEC and non-OPEC monthly crude oil prices. Empir Econ. doi:10.1007/s00181-014-0848-0

Gómez V, Maravall A (1997) Guide for using the programs TRAMO and SEATS. Banco de España, Madrid. http://www.bde.es/webbde/en/secciones/servicio/software/programas.html

Griffin JM, Schulman CT (2005) Price asymmetry in energy demand models: a proxy for energy-saving technical change? Energy J 26:1–21

Horowitz JL (2003) The bootstrap in econometrics. Stat Sci 18:211–218

Hunt LC, Ninomiya Y (2003) Unravelling trends and seasonality: a structural time series analysis of transport oil demand in the UK and Japan. Energy J 24:63–96

Hye QMA, Mashkoor M (2010) Growth and energy nexus: an empirical analysis of Bangladesh economy. Eur J Soc Sci 15:217–221

Hyndman RJ (1996) Computing and graphing highest density regions. Am Stat 50:120–6

Inglesi-Lotz R (2011) The evolution of price elasticity of electricity demand in South Africa: a Kalman filter application. Energy Policy 39:3690–3696

Karimu A, Brannlund R (2013) Functional form and aggregate energy demand elasticities: a nonparametric panel approach for 17 OECD countries. Energy Econ 36:19–27

Kim JH, Fraser I, Hyndman RJ (2011) Improved interval estimation of long run response from a dynamic linear model: a highest density region approach. Comput Stat Data Anal 55:2477–2489

MacKinnon JG (2006) Bootstrap methods in econometrics. Econ Rec 82:2–18

Madlener R (1996) Econometric analysis of residential energy demand: a survey. J Energy Lit 2:3–32

Madlener R, Bernstein R, Gonzalez MAA (2011) Econometric estimation of energy demand elasticities. E ON Energy Research Center Series 3:8. ISSN: 1868-7415

Ministry of Energy and Natural Resources (2012) Statistical reports—December 2012. http://www.enerji.gov.tr (in Turkish)

Pesaran MH, Smith R, Akiyama T (1999) Energy demand in Asian developing economies, 1st edn. Oxford University Press, Oxford

Polemis ML (2012) Competition and price asymmetries in the Greek oil sector: an empirical analysis on gasoline market. Empir Econ 43:789–817

Turkish Government (2000) Regulation for heat insulation in buildings. The Official Gazette of the Republic of Turkey, issue 24043. http://www.resmigazete.gov.tr/default.aspx (in Turkish)

Turkish Statistical Institute (2012) Official statistics programme—December 2012. http://www.turkstat.gov.tr/Start.do

Vinod HD (1993) Bootstrap methods: applications in econometrics. In: Maddala GS, Rao CR, Vinod HD (eds) Handbook of statistics: econometrics, vol 11. North Holland, Elsevier, New York, pp 629–661

Vinod HD (2004) Ranking mutual funds using unconventional utility theory and stochastic dominance. J Empir Finance 11:353–77

Vinod HD (2006) Maximum entropy ensembles for time series inference in economics. J Asian Econ 17:955–978

Vinod HD (2008) Hands-on intermediate econometrics using R, 1st edn. World Scientific, Singapore

Vinod HD, de Lacalle JL (2009) Maximum entropy bootstrap for time series: the meboot R package. J Stat Softw 29(5):1–19

Wadud Z, Dey HS, Kabir A, Khan SI (2011) Modeling and forecasting natural gas demand in Bangladesh. Energy Policy 39:7372–80

Yalta AT (2011) Analyzing energy consumption and GDP nexus using maximum entropy bootstrap: the case of Turkey. Energy Econ 33:453–460

Yalta AT (2013) Small sample bootstrap inference of level relationships in the presence of autocorrelated errors: a large scale simulation study and an application in energy demand. TOBB University of Economics and Technology Department of Economics Working paper no 1301. http://ideas.repec.org/p/tob/wpaper/1301.html

Yalta AT, Cakar H (2012) Energy consumption and economic growth in China: a reconciliation. Energy Policy 41:666–675

Acknowledgments

The authors wish to thank Halim Tosun, the finance director of IGDAS, for his help in providing the natural gas consumption data used in this study. The authors also would like to thank the anonymous reviewers for extremely useful comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Appendix: ARDL estimation results

Appendix: ARDL estimation results

In order to assess the results of a more conventional parametric method on the whole sample, we also employ an autoregressive distributed lag (ARDL) model of the form

where the QNG, GDP, PNG, PE, and QU variables are in natural logs. Table 2 shows the results of the estimated ARDL(2,0,1,0,0,0) model, which was determined by the Akaike information criterion. The CUSUM and CUSUMSQ plots of the full-sample estimates of the ARDL model are also shown in Fig. 4. As can be seen in the table, the income, the real price of electricity as well as the number of customers variables do not seem to be significant at the 5 % level in the short run. In the long run, only the average temperature variable is significant; moreover, the sign of the own price elasticity is positive. The poor results provide additional support for the moving window meboot approach that we employ in this study.

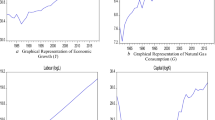

CUSUM and CUSUMSQ plots of the full-sample estimates of the ARDL model with 95 % asymptotic intervals

Rights and permissions

About this article

Cite this article

Altinay, G., Yalta, A.T. Estimating the evolution of elasticities of natural gas demand: the case of Istanbul, Turkey. Empir Econ 51, 201–220 (2016). https://doi.org/10.1007/s00181-015-1012-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-015-1012-1