Abstract

This paper applies Markov-switching method to identify bear and bull market regimes and adopts interactive double-dummy variable approach to re-investigate the conditional relationship between the real oil price return and the international real stock return in 15 OECD countries when the sample is split into bear markets and bull markets. The empirical results indicate that, once the stock index is in the bull trend, an increase in oil price cannot affect the real stock return, while a decrease in oil price can lead to higher stock returns. On the contrary, if the stock market is in the bear era, the oil price growth cannot significantly affect the stock returns. Remarkably, oil price shocks cannot always damage the broad stock index, especially in a bull market era. Furthermore, regardless of the oil price shock, long-term investors need not adopt any policy and strategy to reduce the impact of the oil price on the stock market because the effect of a bull stock market will weaken the negative effect of an oil price shock. On the other hand, regardless of oil price shocks, when the stock market exhibits a bear trend, investors should adopt coping policies and strategies to avoid the impact of other non-oil factors shock, such as declines in real GDP to the stock market in the 15 selected countries. Clearly, regardless of whether the stock market exhibits a bear trend or a bull trend, the stock market trend will surpass the effect of an oil price shock.

Similar content being viewed by others

Notes

“...The bull market displays high returns coupled with low volatility, but the bear market has a low return and high volatility...” (see Maheu and McCurdy 2000, pp. 101). “\({\ldots }\)periods of rising stock prices, the so-called bull markets, and periods of declining stock prices, i.e., “bear” periods\({\ldots }\) a bull or a bear market is a period of consecutive monthly increases or decreases in stock prices the horizon of which is perceived to last well beyond one month. Indeed, in our present analysis, we examine horizons of three months and longer\({\ldots }\)” (see Hardouvelis and Theodossiou 2002, pp. 1539).

Apart from studying the linear relationship, the asymmetric relationship between oil prices and macroeconomic variables has gradually become a concern. For example, Mork (1989) first adopted the specifications of positive oil price and negative oil price and found an asymmetric relationship between the oil price and US economic activities. Beyond that, Mork et al. (1994) also found that an asymmetric relationship exists between the oil price and economic activities in some OECD countries.

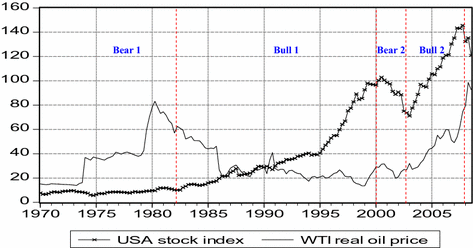

According to Ritter and Warr (2002) and Meric et al. (2008), since 1970, the bull market has covered the period from 1982 to 2000. In addition, according to an article in the Economist entitled “The Big Bear,” the twentieth century can be divided into six phases: bear markets for 1901–1921, 1929–1949 and 1965–1982, and bull runs for 1921–1929, 1949–1965 and 1982–2000 (October 16, 2008).

Fig. 1

US stock index and real oil price trend

Pagan and Sossounov (2003) selected this slightly longer and probably established on 8 months as the suitable length for the cycle of stock prices. For example, they identify the \(\hbox {Peaks}=\left[ \ln p_{t-8} \ldots \ln p_{t-1} < \ln p_t > \ln p_{t+1}, \ldots \ln p_{t+8} \right] ,\, \hbox {Toughs}=\left[ {\ln p_{t-8} \ldots \ln p_{t-1} > \ln p_t < \ln p_{t+1} ,\ldots \ln p_{t+8} } \right] \).

Dummy variables have been widely used to explain nonlinear relationships or asymmetrical relationships in various fields. According to Hardy (see Hardy 1993, pp. 5), dummy variables are useful in both cross-sectional and time-series studies.

Based on the method proposed by Hamilton (1989), we found that the market is more likely to be in a bull (bear) market when regime probabilities \(Pr (S_t =2)\) are greater (less) than 0.5.

Because the instrumental variables relation with equation is difficult to obtain, this paper attempted to use sunspot as the instrumental variable based on Modis’s (2007) findings that the sunspot can be used to forecast US GDP and Dow Jones Index. Our results showed that the OLS model is superior to 2SLS for majority of the countries studied.

Durbin–Wu–Hausman test and J statistic.

References

Basher SA, Sadorsky P (2006) Oil price risk and emerging stock markets. Glob Finance J 17:224–251

Boyer MM, Filion D (2007) Common and fundamental factors in stock returns of Canadian oil and gas companies. Energy Econ 29:428–453

Chen SS (2010) Do higher oil prices push the stock market into bear territory? Energy Econ 32:490–495

Chen NF, Roll R, Ross SA (1986) Economic forces and the stock market. J Bus 56:383–403

Cong RG, Wei YM, Jiao JL, Fan Y (2008) Relationship between oil price shocks and stock market: an empirical analysis from China. Energy Policy 36:3544–3553

El-Sharif I, Brown D, Burton B, Nixon B, Rusesell A (2005) Evidence on the nature and extent of the relationship between oil prices and equity values in the UK. Energy Econ 27:819–830

Fabozzi FJ, Francis JC (1977) Stability tests for alphas and betas over bull and bear market conditions. J Finance 32:1093–1099

Faff RW, Brailsford TJ (1999) Oil price risk and the Australian stock market. J Energy Finance Dev 4:69–87

Fama EF (1970) Efficient capital markets: a review of theory and empirical work. J Finance 25:383–417

Ferson WE, Korajczyk RA (1995) Do arbitrage pricing models explain the predictability of stock returns? J Bus 68:309–349

Fletcher J (2000) On the conditional relationship between beta and return in international stock returns. Int Rev Financ Anal 9:235–245

Hamilton JD (1983) Oil and the macroeconomy since World War II. J Polit Econ 99:228–248

Hamilton JD (1989) A new approach to the economic analysis of nonstationary time series and the businesscycle. Econometrica 57:357–384

Hammoudeh S, Li H (2005) Oil sensitivity and systematic risk in oil sensitivity stock indices. J Econ Bus 57:1–21

Hardouvelis GA, Theodossiou P (2002) The asymmetric relation between initial margin requirements and stock market volatility across bull and bear markets. Rev Finan Stud 15:1525–1559

Hardy MA (1993) Regression with dummy variables (Sage university paper series on quantitative applications in the social sciences, Series no. 07-093). Sage Publications, Newbury Park

Huang RD, Masulis RW, Stoll HR (1996) Energy shocks and financial markets. J Futures Mark 16:1–27

Huang BN, Hwang MJ, Peng HP (2005) The asymmetry of the impact of oil price shocks on economic activities: an application of the multivariate threshold model. Energy Econ 27:455–476

Jones C, Kaul G (1996) Oil and the stock markets. J Finance 51:463–491

Lunde A, Timmermann AG (2004) Duration dependence in stock prices: an analysis of bull and bear markets. J Bus Econ Stat 22:253–273

Maheu JM, McCurdy TH (2000) Identifying bull and bear markets in stock returns. J Bus Econ Stat 18:100–112

Meric I, Ratner M, Meric G (2008) Co-movements of sector index returns in the world’s major stock markets in bull and bear markets: portfolio diversification implications. Int Rev Financ Anal 17:156–177

Miller JI, Ratti RA (2009) Crude oil and stock markets: stability, instability, and bubbles. Energy Econ 31:559–568

Modis T (2007) Sunspots, GDP, and the stock market. Technol Forecast Soc Change 74:1508–1514

Mork KA (1989) Oil and the macroeconomy when prices go up and down: an extension of Hamilton’s results. J Polit Econ 97:740–744

Mork KA, Olsen O, Mysen HT (1994) Macroeconomic responses to oil price increases and decreases in seven OECD countries. Energy J 15:19–35

Nandha M, Faff R (2008) Does oil move equity prices? A global view. Energy Econ 30:986–997

Pagan A, Sossounov K (2003) A simple framework for analysing bull and bear markets. J Appl Econom 18:23–46

Papapetrou E (2001) Oil price shocks, stock market, economic activity and employment in Greece. Energy Econ 23:511–532

Park J, Ratti RA (2008) Oil price shocks and stock markets in the US and 13 European countries. Energy Econ 30:2587–2608

Pettengill G, Sundaram S, Mathur I (1995) The conditional relation between beta and return. J Financ Quant Anal 30:101–116

Ritter JR, Warr RS (2002) The decline of inflation and the bull market of 1982–1999. J Financ Quant Anal 37:29–61

Ross SA (1976) The arbitrage theory of capital asset pricing. J Econ Theory 13:341–360

Sadorsky P (1999) Oil price shocks and stock market activity. Energy Econ 21:449–469

Sadorsky P (2001) Risk factors in stock returns of Canadian oil and gas companies. Energy Econ 23:17–28

The big bear (2008) The Economist. http://www.economist.com/node/12437747

Wang P, Theobald M (2008) Regime-switching volatility of six East Asian emerging markets. Res Int Bus Finance 22:267–283

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Liao, SY., Chen, ST. & Huang, ML. Will the oil price change damage the stock market in a bull market? A re-examination of their conditional relationships. Empir Econ 50, 1135–1169 (2016). https://doi.org/10.1007/s00181-015-0972-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-015-0972-5