Abstract

Although Internet banking is now able to perform many of the functions associated with physical bank branches, these locations still play important roles within their neighborhoods. This is particularly true for low-income, inner-city areas, which often have relatively few traditional banks. This study compares the cases of Milwaukee and Buffalo, both northern “Rust Belt” cities that have experienced manufacturing and population decline. Using both GIS and statistical analysis at the block group level, we confirm the presence of inner-city “cold spots” in both cities using statistical measures. We also find that both bank density and distance are significantly correlated with income and other demographic and economic variables. Statistical tests show that banking “deserts” are poorer and less white than other block groups. Regression analysis shows that for Buffalo, but not Milwaukee, the number of banks in an area is significantly related to income, distance from the CBD, and population density; the vacancy rate is significant while racial makeup is not.

Similar content being viewed by others

Notes

While Buffalo is smaller in relative terms, it still contains a large land area that is useful and valid for this analysis.

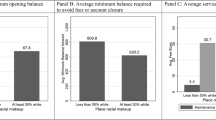

This statistic was calculated for the count of BCUs in each block group, with inverse Euclidean distance as the spatial weight.

References

Anselin L (1995) Local indicators of spatial association–LISA. Geogr Anal 27(2):93–115

Brennan M, McGregor M, Buckland J (2011) The changing structure of inner-city retail banking: examining bank branch and payday loan outlet locations in Winnipeg, 1980–2009. Can J Urban Res 20(1):1–32

Burkey ML, Simkins S (2004) Factors affecting the location of payday lending and traditional banking services in North Carolina. Rev Reg Stud 34(2):191–205

Cover J, Spring AF, Garshick R (2011) Minorities on the margins? The spatial organization of fringe banking services. J Urban Affairs 33(3):317–344

Ergungor OE (2010) Bank branch presence and access to credit in low- to moderate-income neighborhoods. J Money Credit Bank 42(7):1321–1349

Fowler CS, Cover JK, Kleit RG (2014) The geography of fringe banking. J Reg Sci 54(4):688–710

Getis A, Ord JK (1992) The analysis of spatial association by use of distance statistics. Geogr Anal 24(3):189–206

Graves SM (2003) Landscapes of predation, landscapes of neglect: a location analysis of payday lenders and banks. Prof Geogr 55(3):303–317

Hollander M, Wolfe DA (1999) Nonparametric statistical methods, 2nd edn. Wiley, New York

Kruskal W, Wallis WA (1952) Use of ranks in one-criterion variance analysis. J Am Stat Assoc 47(260):583–621

Lee G, Lim H (2009) A spatial statistical approach to identifying areas with poor access to grocery foods in the City of Buffalo, New York. Urban Stud 46(7):1299–1315

Ord JK, Getis A (1995) Local spatial autocorrelation statistics: distributional issues and an application. Geogr Anal 27(4):286–306

Schuetz J, Kolko J, Meltzer R (2012) Are poor neighborhoods “Retail Deserts”? Reg Sci Urban Econ 42:269–285

Smith TE, Smith MM, Wackes J (2008) Alternative financial service providers and the spatial void hypothesis. Reg Sci Urban Econ 38:205–227

Squires GD, O’Connor S (1998) Fringe banking in Milwaukee: the rise of check-cashing business and the emergence of a two-tiered banking system. Urban Aff Rev 34(1):126–149

Wheatley WP (2010) Economic and regional determinants of the location of payday lenders and banking institutions in Mississippi: reconsidering the role of race and other factors in firm location. Rev Reg Stud 40(1):53–69

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Hegerty, S.W. Commercial bank locations and “banking deserts”: a statistical analysis of Milwaukee and Buffalo. Ann Reg Sci 56, 253–271 (2016). https://doi.org/10.1007/s00168-015-0736-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00168-015-0736-3