Abstract

The problem of land with unknown ownership is becoming increasingly evident with Japan’s declining population, low birth rate and aging population. This paper examines the need for the titling system using perspectives from economics and considers what sorts of titling system works for which types of society and looks at ways to deal with the problem of land with unknown ownership. A series of previous researches such as Miceli et al. (Eur J Law Econ 6:305–323, 1998; J Urban Econ 47:370–389, 2000) categorize the titling systems used in many advanced countries as either registration systems or recording systems. In terms of broad categorization Japan’s titling system is categorized as a recording system. However, since the details of registered information are confirmed through various registration procedures, the system also has aspects that resemble a registration system. This can be interpreted as having selected the titling system’s strength that considerably lowers the level of litigation risk. In that case, transaction costs become very high. This could be the cause of the excessively small current level of Japanese real estate transactions. Furthermore, the result of selecting the recording system in Japan, which is a system with a very high strength, could explain why nobody takes insurance to cover the risk of title litigation. In Japan, it is highly likely that the full-fledged population decline, low birth rate and aging population will lower the profitability of land. In that case, a titling system with low strength is likely to be the best for society as indicated in the analysis above.

You have full access to this open access chapter, Download chapter PDF

Similar content being viewed by others

Keywords

- Land plots with unknown owners

- Low birth rate and longevity

- Registration system

- Recording system

- Titling system’s strength

1 Introduction

The problem of land with unknown ownership has become a hot topic. The ‘Basic Policies for Economic and Fiscal Management and Reform 2017’ state, ‘Lands without readily-identifiable owners have been addressed as a common agenda when implementing public works projects and consolidating agricultural and forest lands. With the goal of proper utilization and management of these lands according to the conditions of individual areas, the relevant Ministries and Agencies will together examine the clarifying the requirements for agreement on managing common properties, establish a new system that enables a wide range of public use in response to local needs through the involvement of public bodies, and create measures to eliminate lands of which inheritance registration has not been made for a long term. Moreover, they will aim at submitting a necessary bill to the next ordinary session of the Diet. Furthermore, taking into consideration an increase in lands without readily-identifiable owners due to a decline in population, examination on mid- and long-term issues including the registration system and the current state of land ownership will be swiftly initiated at relevant councils, etc., and results of the examination shall be reported to the Council on Economic and Fiscal Policy… In addition, while expanding the range for utilizing the certification system for statutory succession information, it will further proceed with efforts to, collect, organize, and utilize information on owners from both institutional and organizational perspectives’.

The problem of land with unknown ownership is becoming increasingly evident with Japan’s declining population, low birth rate and ageing population. A comprehensive approach is required to work out how to adapt the real estate system to the underlying issue of the population problem. However, this paper will confine its argument to more directly relevant matters. Taking ‘Land for which the owner cannot immediately be identified from an owners’ ledger such as the real estate register, or for which the owner is uncontactable even if the owner is identified’ to mean land with unknown ownership, the titling system may be considered to have created an environment or been behind this problem of land with unknown ownership. Therefore, this paper examines the need for the titling system using perspectives from economics, considers what sorts of titling system work for which types of society and looks at ways to deal with the problem of land with unknown ownership.

This paper is set out as follows. Part 2 explains two types of titling systems. Part 3 discusses the distinctive features of Japan’s titling system. Part 4 discusses the impact of the choice of titling system on economic welfare. Part 5 provides a summary.

2 Two Types of Real Estate Titling Systems

First, it is important to consider why real estate ownership needs to be protected. According to Besley (1995), there are three reasons why the state protects real estate ownership. First is the freedom from expropriation and being plundered by others. In societies where such things occur, no one will invest in land if the fruits of their investments could be seized by others. The second reason is the ability to use real estate as collateral for borrowing. This not only fosters direct investment in real estate but overall investment.

The third reason is the benefit to society as a whole from transactions if it is transferred to a party who finds higher value through land transactions.

The protection of real estate ownership in this way is indispensable from the perspective of stimulating economic activity and improving the quality of life. To protect this ownership, there needs to be a scheme that clarifies the information concerning who owns what. Therefore, advanced societies all have some sort of titling system.

A series of previous researches such as Miceli et al. (1998, 2000) categorize the titling systems used in many advanced countries as either registration systems or recording systems and economic evaluations have been conducted for the two systems. The following provides a simple explanation of the two titling systems, followed by comments on features of Japan’s titling system.

Under the registration system, the ownership transfer is not valid unless registered, and the country’s registrar conducts a substantial inspection when registration occurs. Subsequently, the ownership is not transferred even if there is litigation from the true owner. Instead, the registration fee is used to fund financial resources and such financial resources are used as compensation to the true owner. In other words, this can be perceived as the government operating an insurance scheme. Although not stated in research such as Miceli et al. (1998, 2000), this is a requirement for taking effect, and it appears to be the method used in the publicly recognized German titling system for example.

On the other hand, the recording system is a scheme widely adopted in the US. When transferring ownership, the real estate transfer certificate (deed) is registered with the registry office. A deed is compiled and stored for each person at the registry. No substantive inspection is conducted by the registry office. To know who the true owner of real estate is and whether or not the recent sales contract has been entered into by the true owner requires after-the-fact confirmation. That is, even if going to the registry office, it is difficult to know who the true owner is unless the person is an expert. Therefore, insurance is available through a title insurance company for a person buying real estate to protect against any form of loss incurred by a real estate buyer due to reasons other than fact that become evident through inspection and examination concerning whether or not a purchase of real estate is based on true ownership. That is, under this scheme, where the true owner is registered, any loss incurred by a person who thinks he has acquired ownership based on registration and subsequently confirms that the registered title deed holder is not the owner shall be covered by insurance.

In fact, although there are many more titling systems, Miceli et al. (1998, 2000) largely categorized them into two schemes and conducted economics analysis. The difference between the two schemes is whether or not the title is publicly recognized. Japan’s titling scheme does not recognize the title, so it can be considered close to a recording system.

3 Features of Japan’s Titling

3.1 A Recording System for the Titling System

In Japan, titling is a mere third-party perfection requirement. In addition, since the principle of protection for public registration does not apply to real estate, even if the title indicates A to be the owner, if A is not the true owner, there is no protection if B acquires ownership from A. Therefore, it is inevitable that the recording system leads to ‘transfer of ownership to the true ownership through ex-post-facto litigation’. However, unlike the situation in the US, the information that is listed on the title in Japan is thought to reflect ‘some kind of’ true ownership relationship.

Next, we consider these types of cases. For example, this includes cases such as ‘A forges documents to pretend that he is the sole owner even though the real estate was acquired through inheritance not only by A, but also A’ as joint heirs’ and ‘A pretends to be the owner of real estate through forged sales contracts, etc’.

However, to register the title of this real estate requires the certification of the registered seal of A’ and the seller of such real estate, so in practice it is very difficult to forge. Therefore, the information listed on the title is very likely to indicate the true ownership relationship with the real estate at some point in time.

Even though it is difficult to forge this type of ownership transfer, the case of positive prescription can be considered where the information on the title is not genuine. Although A certainly had ownership, A’ has been a long-term occupant and positive prescription is established. In this case, if B has been registered as the owner even if this was done by B transacting with A, who does not have ownership, it would be treated in a similar way as a double sale in terms of legal precedent with the ownership being transferred from A to A’ and the ownership being transferred from A to B. This means true owner A’ would not be able to oppose B. That is, in Japan, even when true ownership is not reflected, the registered details are what are protected.

It is often the case, however, that this information does not reflect the current state of the owner relationship and the real estate is still registered in the name of the past owner. That is, the information listed on the title is ‘very unlikely to be a lie’, ‘the person in the title is protected (even in the case of transaction where there is reliance on the title even though it does not reflect the truth)’ and so the situation is close in operation to that of a registration system. On the other hand, unlike a registration system that is always updated with true information as it is a requirement for ownership transfer, a feature of this system is that it may not ‘convey the current truth’.

3.2 The Cost of Not Reflecting the Current Owner Relationship

So, what types of measures can be adopted where the title does not convey the current owner information? While assuming that the registered owner is most likely dead, we consider the case of there being an occupant who has resided at the property for a reasonable length of time. In that case, we assume the current owner has exercised positive prescription over the land and to confirm this, adopt procedures that select the absentee administrator of the owner who is assumed to be dead. The acquirer of positive prescription institutes an ownership confirmation lawsuit against such absentee administrator and confirms the positive prescription. Then a person who requires such land conducts a land transaction with the acquirer of positive prescription as the counterparty.

However, what is the possible response if there is no occupant and the registered owner is thought to have died? In such case, the aim could be to search for the heir of the registered title deed holder. Negotiations concerning the sale of the real estate, etc. are conducted with the heir identified through search activities. However, there are no doubt cases where the heir is not identified regardless of a search.

In the case of public works, procedures referred to as an unknown owner award can be taken. This refers to a request that can be made to the Expropriation Commission for businesses that are highly public in nature with certified projects, if the owner remains unknown even after instituting measure such as investigating the relatives and documents that indicate the whereabouts of the registered owner and asking long-term residents in the vicinity of such real estate.

However, what sorts of procedures are available in the case of the private sector such as companies and households? In such cases, it is possible to assign an absentee administrator to the unknown heir. A, who received the ownership of such land from the identified heir, shall co-own such land with the unknown heir who is represented in such interest through the absentee administrator. In addition, A can acquire the ownership of the land by filing a lawsuit, claiming partition of properties in co-ownership and using the method of full-scale price compensation. However, this series of processes requires approval by the courts. In addition, the absentee administrator may also sell the co-ownership interest to A with the permission of the family court.

Therefore, when the owner is unknown, considerable costs can be incurred in acquiring the ownership of such land and being assigned rights.

While it would be preferable to avoid such costs, is it possible to transfer ownership without instituting such measures?

In such case, the buyer is most likely unwilling to take such risks. In addition, when transacting through a real estate agent, the real estate agent has a duty to investigate the important matters to be explained with strict investigation of the ownership and reporting thereof. In the case of transactions involving finance, the financial institution itself or the judicial scrivener will undertake a title search, and most likely not provide finance for land for which the whereabouts of the owner is unknown.

That is, although Japan has largely adopted a scheme that is categorized as a recording system, but when the title of the land is not 100% clear, it is not fair to state that transactions are being conducted on the basis that risk is being hedged through insurance unlike the case of the US.

4 Economic Evaluation of the Choice of Titling System

4.1 The Theoretical Framework

The following discusses what type of impact the real estate titling system has on the welfare level of society as a whole. Land price is used as an indicator of the welfare level.

Miceli et al. (2011) compare the two tilting systems, i.e., the registration system and the recording system. Since the recording system does not publicly recognize a title, as noted above, the whereabouts of ownership is determined ex-post-facto through litigation and in that case the private sector title insurance plays a large role in preparing for the losses by that actual owner. On the other hand, the registration system recognizes the title, so even if there is litigation by the true owner, the ownership is not transferred, and compensation is paid from a fund that is financed by fees assessed on owners who register their properties. Miceli et al. (2011) assert that, in theory, land with low probability of litigation has high land value under the recording system, whereas a similar effect is found for land with a high probability of litigation under the registration system.

However, as seen so far above, although it can be basically classified as a recording system, the reliability of the registered information is high in the Japanese titling scheme that has no recognition, and litigation based on this is unlikely to occur at the high rate of frequency seen in the US. That is, there is not just one recording system with many variations likely. Since the model used in Miceli et al. (2011) by itself cannot give such a clear depiction, the concept of a titling system’s strength (s) is introduced in the following to provide a theoretical examination of the issues confronting the Japanese titling system. The titling system’s strength refers to a variable that represents the degree of the evidence required when registering and the strength of the registrar’s examination. If the titling system’s strength s increases, the cost of transaction due to ownership transfer through real estate sales or inheritance T(s) increases with T’(s) > 0, whereas the risk of litigation claims surrounding such real estate declines θ(s) (θ’(s) < 0. θ’‘(s) > 0). This variable is presented as follows.

-

Vi: market price of real estate i

-

Ri(I): present value of stream of returns from real estate i, and I is an increasing function of investment amount

-

T(s): the expected present value for transaction costs including future transactions

-

πi: the risk premium concerning the title of real estate i.

-

Pi: the land price of real estate i

-

I: the amount of investment in land

In this case, the market price of real estate i is described as follows.

(3.1) can also be written as follows.

In addition, the land price of real estate i can be written as follows.

For the recording system, if the current owner of the real estate is faced with a litigation claim from the true owner, he will lose ownership and be paid compensation of the investment amount I, so his loss will be Ri(I) − T(s) − I. Taking θ(s) to be the probability that there will be a claim for litigation concerning ownership from the true owner, the risk premium is

Therefore, the following holds true.

Now, taking the differential of (3.5) by the strength of the titling system obtains the following.

The first term on the right hand side of Eq. (3.6) indicates benefits from increasing the strength of the titling system and lowering the litigation risk. The second term indicates the cost associated with increasing the strength and the increasing transactions costs into the future. The third term indicates the costs from a lower amount of compensation for the investment portion with lower risk of litigation. When Eq. (3.6) becomes 0, the title strength s is one where the system maximizes the asset price of the land.

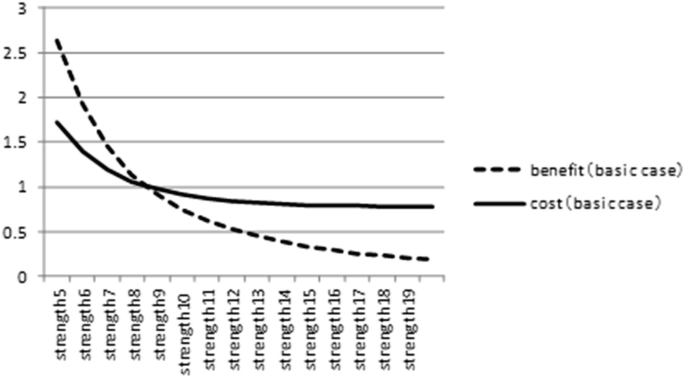

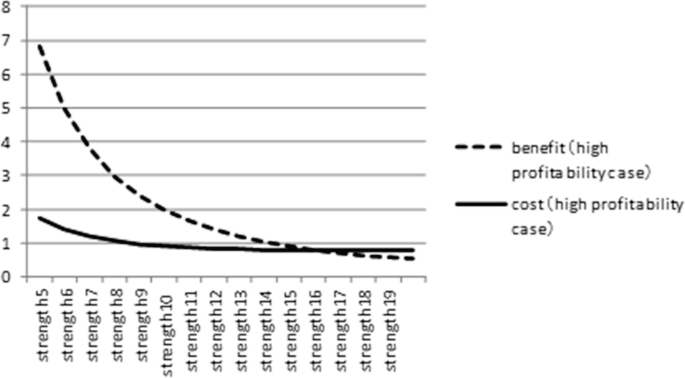

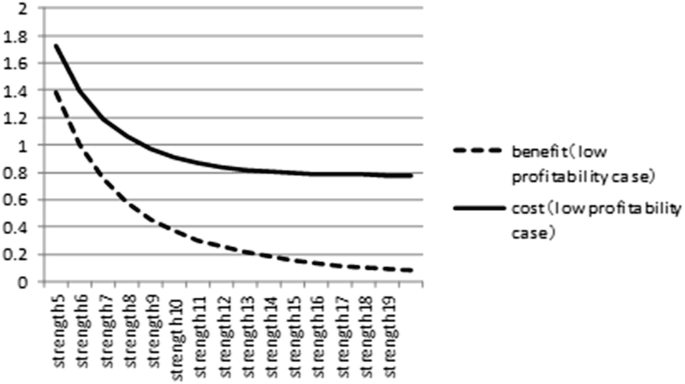

4.2 Simulation Using Numerical Examples

The best s is forecast to differ depending on land i, but here we apply different values concerning the return on investment Ri(I) to examine what sort of impact is given to the strength of the best titling system.

The following provides a qualitative discussion based on numerical examples. We constructed numerical examples based on the following assumptions.

-

For simplicity, the titling system’s strength s is set to be the same value as the transaction cost T. Since there is a certain level of transaction cost even without a titling system, this is changed from 5 to 20.

-

We take. Where a is the efficiency of the titling system, i.e., a parameter that indicates the impact that the titling system’s strength has on the probability of litigation (Charts 2.1, 2.2, 2.3 report the case where a = 0.1).

-

We take R(I) = bI. Where, b is a parameter that indicates the profitability of investment (the base case shown in Chart 2.1 is where b = 2, the high profitability case in Chart 2.2 is where b = 5 and the low profitability case in Chart 2.3 is where b = 1.1).

Chart 2.1

Marginal benefit and marginal cost for the base case (b = 2)

Chart 2.2

Marginal benefit and marginal cost for the high profitability case (b = 5)

Chart 2.3

Marginal benefit and marginal cost for the low profitability case

As shown in Charts 2.1, 2.2, 2.3, the strength of the best titling system increases with the increase in profitability of investment in land.

In the case of land with high profitability, even if an increase is forecast for the future transactions costs, this indicates that it is better to lower the level of litigation risk. On the other hand, in the case of low profitability of land shown in Chart 2.3, regardless of which strength is selected, the costs exceed the benefits and there is no need to protect ownership through the titling system.

5 Conclusion

As noted above, in terms of broad categorization Japan’s titling system is categorized as a recording system. However, since the details of registered information are confirmed through various registration procedures, the system also has aspects that resemble a registration system, yet there has been a problem of registered information not being updated. In terms of the analytical framework presented in sect. 3.4, this can be interpreted as having selected the titling system’s strength that considerably lowers the level of litigation risk. In that case, transaction costs become very high. This could be the cause of the excessively small current level of Japanese real estate transactions.

Furthermore, the result of selecting the recording system in Japan, which is a system with a very high strength, could explain why nobody takes insurance to cover the risk of title litigation. In the case of the registration system, the state takes insurance. The business of title insurance companies occurred spontaneously for the recording systems. However, recording systems with high strength have very low litigation risk, so there are no opportunities for such a business to arise.

In Japan, it is highly likely that the full-fledged population decline, low birth rate and ageing population will lower the profitability of land. In that case, a titling system with low strength is likely to be the best for society as indicated in the analysis above.

However, steady progress in measures such as compact city initiatives will likely cause the profitability of land to become increasingly dispersed. That is, the gap between land with very high profitability and land with low profitability will widen. In this case, the strength of the titling system that should be selected will vary greatly according to the land. However, it is obviously difficult to have different strengths of titling system according to the land. That is, even in this case, the titling system with low strength that should be adopted for Japan as a whole is likely to be adopted, and this could lead to users selecting methods to hedge risks such as subscribing to insurance.

References

Besley T (1995) Property rights and investment incentives: theory and evidence from Ghana. J Polit Econ 105:903–937

Miceli TJ, Sirmans CF, Turnbull GK (1998) Assurance and incentives for land use. Eur J Law Econ 6:305–323

Miceli TJ, Sirmans CF, Turnbull GK (2000) The dynamic effects of land title system. J Urban Econ 47:370–389

Miceli TJ, Munneke HJ, Sirmans CF, Turnbull GK (2011) A question of title: property rights and asset values. Reg Sci Urban Econ 41:499–507

Acknowledgements

I extend my gratitude to Yu Tomita, who provided invaluable advice when preparing this paper.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Open Access This chapter is licensed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license and indicate if changes were made.

The images or other third party material in this chapter are included in the chapter’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the chapter’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder.

Copyright information

© 2021 The Author(s)

About this chapter

Cite this chapter

Nakagawa, M. (2021). The Efficiency of the Titling System: Perspectives of Economics. In: Asami, Y., Higano, Y., Fukui, H. (eds) Frontiers of Real Estate Science in Japan. New Frontiers in Regional Science: Asian Perspectives, vol 29. Springer, Singapore. https://doi.org/10.1007/978-981-15-8848-8_3

Download citation

DOI: https://doi.org/10.1007/978-981-15-8848-8_3

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-15-8847-1

Online ISBN: 978-981-15-8848-8

eBook Packages: Economics and FinanceEconomics and Finance (R0)