Abstract

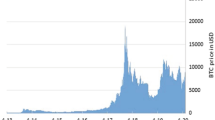

Bitcoin has attracted considerable attention in today’s world because of the combination of encryption technology along with the monetary units. For traders, Bitcoin leads to a promising investment because of its highly fluctuating price. Block chain technology assists in the transactions of documentation. The characteristics of the bitcoin which is derived from the blockchain technology has led to diverse interests in the field of economics. The bitcoin data is selected from 2013 to 2018, over a period of 5 years for this analysis. Here a new roll over technology is applied where new data is obtained over time which will close out the old information during machine training. This mechanism will help in incorporating new information in the short-term learning. The results show that the rollover mechanism improves the time series prediction accuracy.

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Similar content being viewed by others

References

https://www.statista.com/statistics/326707/bitcoin-price-index/

Lane ND, Bhattacharya S, Georgiev P, Forlivesi C, Kawsar F (2015) An early resource characterization of deep learning on wearables, smartphones and internet-of-things devices. In: Proceedings of the 2015 international workshop on internet of things towards applications—IoT-App 15

Spuler M, Sarasola-Sanz A, Birbaumer N, Rosenstiel W, Ramos-Murguialday A (2015) Comparing metrics to evaluate performance of regression methods for decoding of neural signals. In: 37th Annual international conference of the IEEE engineering in medicine and biology society (EMBC)

Ahmed NK, Atiya AF, Gayar NE, El-Shishiny H (2015) An empirical comparison of machine learning models for time series forecasting. Technical Report

Veerakumar S, Dhanya NM (2018) Performance analysis of various regression algorithms for time series temperature prediction. J Adv Res Dyn Control Syst 10(3):996–1000

Anufriev M, Hommes C, Makarewicz T (2012) Learning to forecast with genetic algorithms. Working Paper

Khadka M, Popp B, George KM, Park N (2010) A new approach for time series forecasting based on genetic algorithm. In: CAINE, pp 226–231

Jang H, Lee J (2018) An empirical study on modeling and prediction of bitcoin prices with bayesian neural networks based on blockchain information. IEEE Access 6:5427–5437

Li L, Arab A, Liu J, Liu J, Han Z (2019) Bitcoin options pricing using LSTM-based prediction model and blockchain statistics. In: 2019 IEEE international conference on Blockchain (Blockchain)

Dhanya NM, Harish UC (2018) Sentiment analysis of twitter data on demonetization using machine learning techniques. In: Lecture notes in computational vision and biomechanics, vol 28, pp 227–237

Sriwiji R, Primandari AH (2020) An empirical study in forecasting bitcoin price using bayesian regularization neural network. In: Proceedings of the 1st international conference on statistics and analytics, ICSA 2019, 2–3 Aug 2019, Bogor, Indonesia

Sin E, Wang L (2017) Bitcoin price prediction using ensembles of neural networks. In: 2017 13th International conference on natural computation, fuzzy systems and knowledge discovery (ICNC-FSKD)

Dobslaw F (2010) A parameter tuning framework for metaheuristics based on design of experiments and artifcial neural networks. In: Proceedings of the international conference on computer mathematics and natural computing (WASET ’10)

https://docs.microsoft.com/en-us/azure/machine-learning/machine-learning-algorithm-choice, http://scikit-learn.org/stable/modules/cross_validation

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Editor(s) (if applicable) and The Author(s), under exclusive license to Springer Nature Singapore Pte Ltd.

About this paper

Cite this paper

Dhanya, N.M. (2021). An Empirical Evaluation of Bitcoin Price Prediction Using Time Series Analysis and Roll Over. In: Ranganathan, G., Chen, J., Rocha, Á. (eds) Inventive Communication and Computational Technologies. Lecture Notes in Networks and Systems, vol 145. Springer, Singapore. https://doi.org/10.1007/978-981-15-7345-3_27

Download citation

DOI: https://doi.org/10.1007/978-981-15-7345-3_27

Published:

Publisher Name: Springer, Singapore

Print ISBN: 978-981-15-7344-6

Online ISBN: 978-981-15-7345-3

eBook Packages: EngineeringEngineering (R0)