Abstract

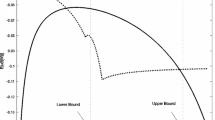

We investigate by means of agent-based simulations the influence of convex incentives, e.g. option-like compensation, on financial markets. We propose an agent based model already developed in Fabretti et al (2015), where the model was build with the aim of studying convex contract effect using the results of a laboratory experiment performed by Holmen et al. (2014) as benchmark. Here we replicate their results studying prices dynamics, volatility, volumes and risk preference effect. We show that convex incentives produces higher prices, lower liquidity and higher volatility when agents are risk averse, while, differently from Fabretti et al (2015), their effect is less evident if agents are risk lovers. This appears related to the fact that prices in the long run converge more likely to the equilibrium when agents are risk averse.

JEL Classification G10, D40, D53

Access this chapter

Tax calculation will be finalised at checkout

Purchases are for personal use only

Preview

Unable to display preview. Download preview PDF.

Similar content being viewed by others

References

Allen, F.: Do financial institutions matter? Journal of Finance 56, 1165–1175 (2001)

Allen, F., Gorton, G.: Churning bubbles. Review of Economic Studies 60, 813–836 (1993)

Bebchuk, L., Spamann, H.: Regulating bankers pay. Georgetown Law Journal 98, 247–287 (2010)

Cuoco, D., Kaniel, R.: Equilibrium prices in the presence of delegated portfolio management. Journal of Financial Economics 101, 264–296 (2011)

Dewatripont, M., Rochet, J., Tirole, J.: Balancing the Banks: Global Lessons from the Financial Crises. Princeton University Press, Princeton (2010)

Fabretti, A., Gärling, T., Herzel, S., Holmen, M.: Convex Incentives in Financial Markets: an Agent-Based Analysis, CEIS Research Paper 337. Tor Vergata University, CEIS (2015)

French, K., Baily, M.N., Campell, J.Y., Cochrane, J.H., Diamond, D.W., Duffie, D., Kashyap, A.K., Mishkin, F.S., Rajan, R.G., Scharfstein, D.S., Shiller, R.J., Shin, H.S., Slaughter, M.J., Stein, J.C., Stulz, R.M.: The Squam Lake Report: Fixing the Financial System. Princeton University Press, Princeton (2010)

Gennaioli, N., Shleifer, A., Vishny, R.: Neglected risks, financial innovation, and financial fragility. Journal of Financial Economics 104, 452–468 (2012)

Goetzmann, W.N., Ingersoll, J.E., Ross, S.A.: High-water marks and hedge fund management contracts. Journal of Finance 58, 1685–1718 (2003)

Haruvy, E., Lahav, Y., Noussair, C.N.: Traders expectations in asset markets: experimental evidence. American Economic Review 97, 1901–1920 (2007)

Holmen, M., Kirchler, M., Kleinlercher, D.: Do option-like incentives lead to overvaluation? Evidence from experimental asset markets. Journal of Economic Dynamics and Control 40, 179–194 (2014)

Huber, J., Kirchler, M., Matthias, S.: Experimental Evidence on Varying Uncertainty and Skewness in Laboratory Double-Auction Markets. Journal of Economic Behavior and Organization 107, 798–809 (2014)

Kritzman, M.P.: Incentive fees: Some problems and some solutions. Financial Analysts Journal 43, 21–26 (1987)

Loomes, G., Starmer, C., Sugden, R.: Do Anomalies Disappear in Repeated Markets? Economic Journal 113, 153–166 (2003)

Noussair, C.N., Tucker, S.: Experimental Research On Asset Pricing. Journal of Economic Surveys 27(3), 554–569 (2013)

Palan, S.: A review of bubbles and crashes in experimental asset markets. Journal of Economic Surveys 27, 570–588 (2013)

Rajan, R.G.: Has financial development made the world riskier? European Financial Management 12, 499–533 (2006)

Sotes-Paladino, J. M., Zapatero, F.: Riding the bubble with convex incentives. Marshall Reserach Paper Series Working Paper FBE 06.14 (2014)

Turner, A.: A regulatory response to the global banking crisis.Financial Service Authority (2009)

Walker, D.: A review of corporate governance in UK banks and other financial industry entities: final recommendations. Financial Service Authority (2009)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer International Publishing Switzerland

About this paper

Cite this paper

Fabretti, A., Gärling, T., Herzel, S., Holmen, M. (2016). An Agent-Based Model to Study the Impact of Convex Incentives on Financial Markets. In: de la Prieta, F., et al. Trends in Practical Applications of Scalable Multi-Agent Systems, the PAAMS Collection. PAAMS 2016. Advances in Intelligent Systems and Computing, vol 473. Springer, Cham. https://doi.org/10.1007/978-3-319-40159-1_1

Download citation

DOI: https://doi.org/10.1007/978-3-319-40159-1_1

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-40158-4

Online ISBN: 978-3-319-40159-1

eBook Packages: EngineeringEngineering (R0)