Abstract.

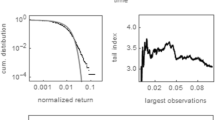

A class of heterogeneous agent models is investigated where investors switch trading position whenever their motivation to do so exceeds some critical threshold. These motivations can be psychological in nature or reflect behaviour suggested by the efficient market hypothesis (EMH). By introducing different propensities into a baseline model that displays EMH behaviour, one can attempt to isolate their effects upon the market dynamics. The simulation results indicate that the introduction of a herding propensity results in excess kurtosis and power-law decay consistent with those observed in actual return distributions, but not in significant long-term volatility correlations. Possible alternatives for introducing such long-term volatility correlations are then identified and discussed.

Similar content being viewed by others

References

E. Fama, J. Finance 25, 383 (1970)

R. Mantegna, H. Stanley, An Introduction to Econophysics (CUP, 2000)

R. Cont, Quantitive Finance 1, 223 (2001)

R. Cross, M. Grinfeld, H. Lamba, T. Seaman, Phys. A 354, 463 (2005)

H. Lamba, T. Seaman, preprint, Econophysics forum

B. LeBaron, in Post-Walrasian Economics, edited by D. Colander (CUP, New York, 2006)

R. Cross, M. Grinfeld, H. Lamba, A. Pittock, in Relaxation Oscillations and Hysteresis, edited by M. Mortell, R.O. Jr, A. Pokrovskii, V. Sobolev (SIAM, 2005), pp. 61–72

B. Malkiel, J. Econ. Perspectives 17, 59 (2003)

A. Schleifer, Inefficient Markets, Clarendon Lectures in Economics (OUP, 2000)

H. Simon, Quart. J. Econ. 69, 99 (1955)

H. Simon, Models of Bounded Rationality (MIT Press, 1997)

C. Chamley, Rational Herds (CUP, 2004)

I. Lobato, C. Velasco, J. Bus. Econ. Stat. 18, 410 (2000)

L. Gillemot, J.D. Farmer, F. Lillo, Quant. Fin 371 (2006)

T. Ane, H. Geman, J. Finance 55, 2259 (2000)

C. Jones, G. Kaul, M. Lipsom, Rev. Fin. Stud., 631 (1994)

R. Baillie, T. Bollerslev, H. Mikkelsen, J. Econometrics, 3 (1996)

T. Lux, M. Marchesi, Int. J. Theor. Appl. Finance 3, 675 (2000)

G. Brown, Financial Analysts Journal, 82 (1999)

R. Cross, M. Grinfeld, H. Lamba, J. Phys. 55, 55 (2006)

P. Diaconis, D. Freedman, SIAM Rev. 41, 45 (1999)

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Cross, R., Grinfeld, M., Lamba, H. et al. Stylized facts from a threshold-based heterogeneous agent model. Eur. Phys. J. B 57, 213–218 (2007). https://doi.org/10.1140/epjb/e2007-00108-5

Received:

Published:

Issue Date:

DOI: https://doi.org/10.1140/epjb/e2007-00108-5