Abstract

The paper analyzes the systematic risk which is inherent in a portfolio of deferred life annuities. We take into account stochastic mortality as well as stochastic interest rates. For the specification of the mortality rate dynamics, we consider a pure diffusion model as well as a compound Poisson jump model. The interest rate dynamics are given by a one-factor Hull–White model. All models, interest rate and mortality rate, are calibrated to financial market as well as demographic data. We use Monte Carlo simulations to approximate the variance of the discounted cash flow and its decomposition into a pooling and a non-pooling risk part. We also consider pricing effects using the principle of zero expected utility and the quantile principle. The estimated risk premiums are benchmarked to the equivalence premium. Finally, we focus on solvency requirements which are based on the investment decisions and the associated shortfall probability of the annuity provider.

Similar content being viewed by others

Notes

The redeemed new annuity and pension insurance business contributes regular premiums of about 1.3 billion Euro with an overall share of 31%. The business in force at the end of 2009 consists of 18.3 million contracts (equals a share of 20%), see German Insurance Association (GDV) (2009).

To be precise, mortality risk denotes the risk stemming from mortality rates which are systematically higher than expected and longevity risk refers to the opposite risk scenario.

Notice that the mortality derivative market is almost illiquid at present and tailor-made reinsurance solutions are cost-intensive. Thus, we do not consider the non-pooling risk to be a traded risk.

The accumulation phase [0,T[ represents a kind of savings plan, whereas the decumulation phase \([T,\bar{T}]\) forms an immediate life annuity.

For example, Bravo (2008) estimates the values \(\eta_1=2.8\times10^{-2}\) and \(\eta_2=9\times10^{-5}\) for the survival function of an 65-year old insured and the year 2004. Luciano and Vigna (2006) state that negative jumps are adequate to describe mortality variations. They estimate an average size \(\eta= 3\times10^{-5}\) for the year 1945 and a retiree aged 65.

A swaption is called at-the-money if its strike equals the forward par swap rates.

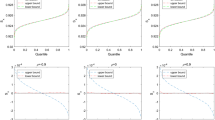

Recall that, according to Table 5, only σ spot = 0.0094 is consistent with the swaption straddle volatilities. However, for varying σ spot , we nevertheless calibrate to the same initial term structure of interest, i.e. we use the function θ(t) as in Table 2. Thus, we still have the same expected values, independent of the choice of σ spot .

Among others, Bauer and Weber (2008) stress that it might be unrealistic to finance intermediate shortfalls against a savings account rather than money at the market interest rate.

References

Bauer D, Weber F (2008) Assessing investment and longevity risks within immediate annuities. Asia-Pac J Risk Insur 3(1):89–111

Bayraktar E, Milevsky M, Promislow S, Young V (2009) Valuation of mortality risk via the instantaneous sharpe ratio: applications to life annuities. J Econ Dyn Control 33(3):676–691

Biffis E (2005) Affine processes for dynamic mortality and actuarial valuations. Insur Math Econ 37(3):443–468

Blake D, Burrows W (2001) Survivor bonds: helping to hedge mortality risk. J Risk Insur 68(2):339–348

Bravo J (2008) Pricing longevity bonds using affine-jump diffusion. In: University of Évora—Department of Economics, 7th meeting on social security and complementary pensions systems, working paper

Brigo D, Mercurio F (2007) Interest rate models—theory and practice. Springer, Berlin

Brouhns N, Denuit M, Vermunt J (2002) Measuring the longevity risk in mortality projections. Bull Swiss Assoc Actuar 2:105–130

Christiansen M, Helwich M (2008) Some further ideas concerning the interaction between insurance and investment risks. Blätter der DGVFM 29(2):253–266

CLP Structured Finance (2010) Euro current swap rates. Website. http://www.swap-rates.com/EUROSwap.html (data downloaded on 04/10)

Coppola M, Di Lorenzo E, Sibillo M (2000) Risk sources in a life annuity portfolio: decomposition and measurement tools. J Actuar Pract 8:43–61

Coppola M, Di Lorenzo E, Sibillo M (2002) Further remarks on risk sources measuring in the case of a life annuity portfolio. J Actuar Pract 10:229–242

Coppola M, Di Lorenzo E, Sibillo M (2003) Stochastic analysis in life office management: applications to large annuity portfolios. Appl Stoch Models Bus Ind 19(1):31–42

Dahl M (2004) Stochastic mortality in life insurance: market reserves and mortality-linked insurance contracts. Insur Math Econ 35(1):113–136

Dahl M, Møller T (2006) Valuation and hedging of life insurance liabilities with systematic mortality risk. Insur Math Econ 39(2):193–217

Dahl M, Melchior M, Møller T (2008) On systematic mortality risk and risk-minimization with survivor swaps. Scand Actuar J 2008(2):114–146

De Waegenaere A, Melenberg B, Stevens R (2010) Longevity risk. De Econ Q Rev Royal Neth Econ Assoc 158(2):151–192

Di Lorenzo E, Sibillo M (2002) Longevity risk: measurement and application perspectives. In: Proceedings in 2nd conference in actuarial science and finance on Samos, Karlovassi (Grecia)

Financial Times (2010) Market euro libor interest rates. Website. http://markets.ft.com (data downloaded on 06/10)

German Insurance Association (GDV) (2009) Geschäftsentwicklung 2009—die deutsche lebensversicherung in zahlen. Website. http://www.gdv.de/Downloads/Pressemeldungen_2010/PD23_Publikation_LVinZahlen.pdf (data downloaded on 11/09)

Hainant D, Devolder P (2008) Mortality modelling with lévy processes. Insur Math Econ 42(1):409–418

Hári N, De Waegenaere A, Melenberg B, Nijman T (2008) Longevity risk in portfolios of pension annuities. Insur Math Econ 42(2):505–519

Hull J, White A (1990) Pricing interest-rate derivative securities. Rev Financial Stud 3(4):573–592

Human Mortality Database (2009) University of California, Berkeley (USA) and Max Planck Institute for Demographic Research, Rostock (Germany), period life tables West Germany 1956–2006 (males). http://www.mortality.org/ (data downloaded on 08/09)

Korn R, Natcheva K, Zipperer J (2006) Langlebigkeitsbonds—bewertung, modellierung und aspekte fnr deutsche daten. Blätter der DGVFM 27(3):397–418

Kou S (2002) A jump diffusion model for option pricing. Manag Sci 48(8):1086–1101

Luciano E, Vigna E (2006) Non mean reverting affine processes for stochastic processes. The Carlo Alberto notebooks, Fondacione Collegio Carlo Alberto no. 30

Ludkovski M, Young V (2008) Indifference pricing of pure endowments and life annuities under stochastic hazard and interest rates. Insur Math Econ 42(1):14–30

Milevsky M, Promislow S, Young V (2006) Killing the law of large numbers: Mortality risk premiums and the sharpe ratio. J Risk Insur 73(4):673–686

Olivieri A (2001) Uncertainty in mortality projections: an actuarial perspective. Insur Math Econ 29(2):231–245

Olivieri A (2007) Designing longevity risk transfers: the point of view of the cedant. ICFAI J Financial Risk Manag 4(1):55–83

Park F (2004) Implementing interest models: a practical guide. Capital markets & portfolio research, Incorporated (CMPR), working paper

Parker G (1997) Stochastic analysis of the interaction between investment and insurance risk. North Am Actuar J 1(2):55–89

Pelsser A (2005) Market-consistent valuation of insurance liabilities. University of Amsterdam, working paper

Pitacco E (2004a) From halley to frailty: a review of survival models for actuarial calculations. Giornale dell’ Istituto Italiano degli Attuai 67:17–47

Pitacco E (2004b) Longevity risk in living benefits. In: Fornero E, Luciano E (eds) Developing an annuity market in Europe. Edward Elgar, Cheltenham, pp 81–97

Pitacco E (2004c) Survival models in a dynamic context: a survey. Insur Math Econ 35(2):279–298

Reuters T (2010) Eur atm swaption straddles—implied volatilities. Trading Room, iCAP Global index interest rate options (data retrieved on 06/10)

Schrager D (2006) Affine stochastic mortality. Insur Math Econ 35(1):81–97

Schweizer M (2001) From actuarial to financial valuation principles. Insur Math Econ 28:31–47

Author information

Authors and Affiliations

Corresponding author

Appendix: A market data and calibration results

Rights and permissions

About this article

Cite this article

Mahayni, A., Steuten, D. Deferred life annuities: on the combined effects of stochastic mortality and interest rates. Rev Manag Sci 7, 1–28 (2013). https://doi.org/10.1007/s11846-011-0066-5

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11846-011-0066-5

Keywords

- Deferred life annuities

- Longevity risk

- Stochastic mortality rates

- Stochastic interest rates

- Incomplete market pricing

- Solvency requirements