Abstract

The main focus of this paper is the managerial skill or alpha of global bond funds. Analysis of the global bond market shows that both currency and bond-related returns are an integral part of the global fixed-income exposure. The present work deals with regression-based style analysis and other established methods in the bulk of finance journals literature, using both currency and fixed-income factors, and investigates the alpha of the globally invested fixed-income portfolios. There is empirical evidence that, between May 2007 and January 2015, global bond funds delivered significantly positive alpha. There is also an indication that periods of depreciation of the basis currency of the funds (EUR) improves fund performance, and market turmoil and negative events destroy alpha. During the Euro crisis and Fed tapering, the funds generated sustainable positive excess alpha. A division of the sample into two sub-samples gives more insight into the excess return. Additional robustness estimations deliver qualitatively similar results.

Similar content being viewed by others

Notes

The AUM of the reported funds in this analysis is EUR 114 billion and represents a significant part of the global bond funds managed in EUR. According to Morningstar the total number of global bond funds is 1610 and the total AUM is USD 711.2 billion, as of 07/2015; roughly 25 % of all funds are EUR denominated. In addition ca. 35 % of the total AUM and ca. 75 % of the total number of global bond funds are not run against a benchmark.

Short-run or short-term alpha is defined as weekly time-variation in this analysis; long-term is defined over a specific time period, as stipulated further in this analysis.

Lipper Database for Investment Management/Thomson Reuters offers a comprehensive structure; the data set includes the Net Asset Values (NAV) of the funds as provided by Lipper/Thomson Reuters; the logarithmic fund returns used for this analysis are EUR denominated. Fund returns are adjusted for dividends.

The amount of 431 weekly observations is derived using the entire sample range; the sample range for the time-varying exposure is reduced by the first 26 weekly returns.

The author discusses the properties of complex systems and the application of reductionist approaches for analyzing complex behavior.

Pojarliev and Levich (2011) analyzed crowded trades in the FX markets generated by currency managers, using a linear regression model and stated that the level of crowdedness reflects the difference between the funds with significant positive exposure and the funds with significant negative exposure to a style factor. Konstantinov applied this approach to bond funds with basis currency USD and successfully detected currency crowdedness generated by global fixed-income funds.

The authors describe beta grazers and alpha hunters carrying out analysis of statistical results to distinguish between alpha hunters and beta grazers.

Pojarliev and Levich (2012) provide a detailed explanation of the factors and systematics in currency investing.

Nucera and Valente (2013) consider the errors in the regressions in detail. If the errors \({\hat{\varepsilon }}_i\) in the Ordinary Least Squares are normally distributed the estimations are unbiased, consistent and efficient. In this case the residuals should be zero. The term \(\alpha _i +\varepsilon _{i,t}\) represents the non-benchmark related return of a manager; the term \(\varepsilon _{i,t}\) represents the noise in the underlying performance; using the Jarque–Bera Test we test for normally distributed residuals. Fischer and Wermers (2013) provide detailed explanations.

Fischer and Wermers (2013) provide a review of studies in this field.

I thank an anonymous referee for pointing these topics out.

Bond carry and bond trend indices by J.P. Morgan have Bloomberg Tickers: AIJPGBCU Index and JPCVHEU Index; the Bond Carry Index by UBS has Bloomberg Ticker ULTAEBCT Index.

Carry, G10 carry, trend and value always refer to the factors concerned with currency investing; both trend and carry factors associated with fixed-income exposure are always named bond trend and bond carry, respectively.

The Bloomberg Ticker for the Deutsche Bank Value Index is the DBPPPEUF Index.

The Bloomberg time series of the Barclays FX Long-Short Volatility Index is given by the following ticker: BFXSFVLS Index.

The Sharpe Ratio is calculated using the annualized respective alpha and standard deviation reported in Table 3.

The same analysis is run for 6 randomly selected funds from the sample of 375 funds; the results for the CUSUMSQ tests are shown in Fig. 10 of the Appendix; three of the six funds have robust CUSUMSQ estimations. For three of the funds, the null hypothesis of no structural break is rejected.

From the beginning of the sample data, the equity fund flows were steadily decreasing and the cumulative fund flows into bond funds were increasing. J.P. Morgan Cazenove Research (2015)

The reported F-Statistic for the Chow breakpoint test is 8.789 and the correspondent P value is 0.000.

The Akaike (AIC) and Schwarz (SC) Information Criterion are computed for the models. Both AIC and SC Information criterions suggest that the model from Eq. 1 is preferred over the one from Eq. 2. AIC/SC for Eq. 1 are \(-559\) and \(-511\), respectively; AIC/SC for Eq. 2 are \(-489\) and \(-453\), respectively. The SE of regression of model 1 is 101.63, and the SE of regression of model 2 is 120.99.

References

Ahoniemi, K., Jylha, P.: Flows, price pressure, and hedge fund returns. Financ. Anal. J. 70(5), 73–92 (2014)

Anson, M.: The beta continuum: from classic beta to bulk beta. J. Portf. Manag. 34(2), 53–64 (2008)

Bessler, W., Holler, J., Kurmann, P.: Hedge funds and optimal asset allocation: bayesian expectations and spanning tests. Financ. Mark. Portf. Manag. 26(1), 109–142 (2012)

Edelman, D., Fung, W., Hsieh, D., Naik, N.: Funds of hedge funds:performance, risk and capital formation 2005 to 2010. Financ. Mark. Portf. Manag. 26(1), 87–108 (2012)

Fama, E., French, K.: Common risk factors on the returns on stocks and bonds. J. Financ. Econ. 33(1), 3–56 (1993)

Fama, E., MacBeth, J.D.: Risk, return, and equilibrium: empirical tests. J. Polit. Econ. 81(3), 607–636 (1973). (May/June)

Fischer, B., Wermers, R.: Performance Evaluation and Attribution of Security Portfolios. AP Elsevier, Oxford (2013)

Fung, W., Hsieh, D.: Asset-based style factors for hedge funds. Financ. Anal. J. 58(5), 17–28 (2002)

Goyal, A.: Empirical cross-sectional asset pricing: a survey. Financ. Mark. Portf. Manag. 26(1), 3–38 (2012)

Holland, J.: Signals and Boundaries: Buliding Blocks for Complex Adaptive Systems. The MIT Press, Cambridge, Massachusetts (2012)

J.P. Morgan Cazenove: Equity Strategy; Global Equity Research. JPMorgan, London (2015). (2015, November 2)

Konstantinov, G.: Active currency management of international bond portfolios. Financ. Mark. Portf. Manag. 28(1), 63–94 (2014a)

Konstantinov, G.: Can global bond fund managers generate alpha using currency volatility? Int. J. Bonds Deriv. 1(2), 111–133 (2014b)

Konstantinov, G.: Vorteile kombinierter Fixed-Income- und Waehrungsstrategien im Niedrigzinsumfeld. Zeitschrift fuer das gesamte Kreditwesen 69(2), 92–95 (2016)

Konstantinov, G.: Currency Crowdedness generated by Global Bond Funds. J. Portf. Manag. (2017) (forthcoming winter 2017)

Leibowitz, M.: Alpha hunters and beta grazers. Financ. Anal. J. 61(5), 32–39 (2005)

Li, X., Becker, Y., Rosenfeld, D.: Asset growth and future stock returns. Financ. Anal. J. 68(3), 51–63 (2012)

Menkhoff, L., Sarno, L., Schmeling, M., Schrimpf, A.: Currency Momentum Strategies. BIS Working Papers No. 366, pp.1–86 (2011)

Menkhoff, L., Sarno, L., Schmeling, M., Schrimpf, A.: Carry trades and global foreign exchange volatility. J. Finance 67(2), 681–718 (2012)

Nucera, F., Valente, G.: Carry Trades and the Performance of Currency Hedge Funds. Hong Kong Institute of Monetary Research, Working Paper No.03, January (2013)

Peterson, J., Iachini, M., Lam, W.: Identifying characteristics to predict separately managed account performance. Financ. Anal. J. 67(4), 30–42 (2011)

Pojarliev, M., Levich, R.: Do professional currency managers beat the benchmark? Financ. Anal. J. 64(5), 18–32 (2008)

Pojarliev, M., Levich, R.: Trades of the living dead: style differences, style persistence and performance of currency fund managers. J. Int. Money Finance 29, 1752–1775 (2010)

Pojarliev, M., Levich, R.: Detecting crowded trades in currency funds. Financ. Anal. J. 67(1), 26–39 (2011)

Pojarliev, M., Levich, R.M.: A New Look at Currency Investing. CFA Institute, New York (2012)

Sharpe, W.: Asset allocation: management style and performance measurement. J. Portf. Manag. Winter 18(2), 7–19 (1992)

Sharpe, W.: Adaptive asset allocation. Financ. Anal. J. 66(3), 45–60 (2010)

Strange, B.: Currency overlay managers show consistency: in the long run count on them for adding value. Pensions Invest. 26(12), 26–31 (1998)

Xie, Y., McCormick, L.: Biggest Money in Currencies is Made Seeling Options. Bloomberg News, New York (2011). (2011, April 20)

Acknowledgments

I acknowledge the anonymous referee for helpful comments and suggestions. I am grateful to Prof. Dr. O. Loistl and Prof. Dr. C. Casey for their insightful and constructive criticism.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

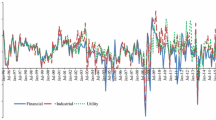

CUSUMSQ tests for randomly selected funds from the sample of 375 funds. Note: CUSUMSQ tests for single fund returns according to Eq. 1. Significance at the 5 % level

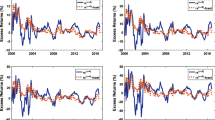

Original (F375) 4/5/2007–31/1/2015 and alternative excess alpha (F375) 11/2/2007–31/1/2015. Note: This exhibit captures all rolling regression points according to Eqs. 1 and 3. In the original graph the first point for the 375 funds is estimated using the first 26 weekly returns and corresponds to 4/5/2007, while the last estimation is made on 31/1/2015, with a rolling window of 1 week. In the alternative graph, the first point for the 375 funds is estimated using the first 52 weekly returns and corresponds to 11/2/2007, while the last estimation is made on 31/1/2015, with a rolling window of 1 week. Significance is at the 5 % level

Rights and permissions

About this article

Cite this article

Konstantinov, G. Capturing short-term and long-term alpha of global bond portfolios: evidence from EUR-investors’ perspective. Financ Mark Portf Manag 30, 337–365 (2016). https://doi.org/10.1007/s11408-016-0271-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11408-016-0271-y