Abstract

We study the trading behavior of retail investors in the market of leveraged bank-issued retail derivatives, which are designed to encourage excessive trading and speculation. We investigate whether retail investors have private information and benefit disproportionately or whether they gamble without private information. We answer this question along three dimensions: (i) profitability, (ii) news trading, and (iii) transaction costs. We distinguish between derivatives by the type of underlying (index vs. individual stocks). We find that raw returns are negative for derivatives with stocks as the underlying, and only partially positive for those with index as the underlying. Nevertheless, risk-adjusted returns show poor performance, with Sharpe ratios below 0.30. We show that retail investors are attracted by news, but do not have private information prior to news events.

Similar content being viewed by others

Notes

In this paper, we use the terms “derivative” and “product” interchangeably.

Barber and Odean (2000, p. 800).

Dorn and Sengmueller (2009, p. 602) show that retail investors trading for entertainment trade “twice as much as those who fail to take pleasure in gambling or investing”.

Bauer et al. (2009, p. 745).

See http://www.derivateverband.de/ENG/Statistics/MarketVolume for up-to-date market statistics.

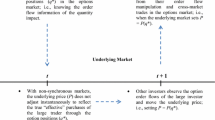

Prices are set by the issuing investment bank. This way every trade usually has the issuing bank on the opposite side. Nevertheless, it is possible that a buy and sell trade of the same product is sent to the exchange simultaneously and can be matched. This happens in less than 0.1 % of all trades.

Source: German Derivatives Association (http://www.derivateverband.de), http://www.derivateverband.de/EN/MediaLibrary/Document/PM/07%20DDV%20Boersenumsatz-Statistik%20Juli%202012.pdf.

The call (put) product can be duplicated through a down-and-out call (up-and-out put) option (Rubinstein and Reiner 1991).

Table 3 contains a list of all DAX constituents.

We thank SIRCA for providing access to its data archive.

This results in two products with DAX as the underlying, and 252 with a DAX constituent as the underlying.

We thank Thomson Reuters for providing access to this data. For more details about the news data set, see Storkenmaier (2011).

According to our methodological approach, we identify 9,454 (5,124) trades in index (stock) products as total losses.

In October 2012, 60.4 % of all tradable leverage certificates had an index as the underlying, 19.6 % a stock, and 15.2 % a commodity. Source: German Derivative Association, October Statistic, 2012, http://www.derivateverband.de.

The purpose of the subscription ratio is to scale down the price of a leverage certificate to an investor-friendly level. The subscription ratio in our sample varies between 0.01 and 1.

As of January 2013, the cheapest German broker charged round-trip costs of at least 10 EUR.

Wallmeier (2011) proposes a potential solution through the development of a new way of illustrating risks associated with structured products to avoid investment mistakes by retail investors.

We standardize a variable in the following way: var \(=\) (variable \(-\) AVG(variable))/STD(variable).

Our results are robust if we exclude individual variables from the model. Additionally, an interaction effect of volume and leverage is not significant. Using a truncated regression model or a logit model instead of our standard regression model does not change the effects. Transformation ((Ret\(_{ ijh})^{3 })\) of raw returns also has no effect on the direction of the estimated coefficients.

Traditional literature focuses on market vs. limit orders from a market microstructure perspective. Results retrieved from this work are of only limited use in our market, since there is a guaranteed execution at the current best bid and best ask price for volumes up to 20,000 EUR. For stock markets, Anand et al. (2005) argue that informed investors use both limit and market orders.

References

Anand, A., Chakravarty, S., Martell, T.: Empirical evidence on the evolution of liquidity: choice of market versus limit orders by informed and uninformed traders. J. Financ. Mark. 8(3), 288–308 (2005)

Anderson, A.: Is online trading gambling with peanuts? In: Technical report, Swedish Institute for Financial Research (2008)

Barber, B.M., Lee, Y.-T., Liu, Y.-J., Odean, T.: Just how much do individual investors lose by trading? Rev. Financ. Stud. 22(2), 609–632 (2009)

Barber, B.M., Odean, T.: Trading is hazardous to your wealth: the common stock investment performance of individual investors. J. Finance 55(2), 773–806 (2000)

Barber, B.M., Odean, T.: All that glitters: the effect of attention and news on the buying behavior of individual and institutional investors. Rev. Financ. Stud. 21(2), 785–818 (2008)

Bauer, R., Cosemans, M., Eichholtz, P.: Option trading and individual investor performance. J. Bank. Finance 33(4), 731–746 (2009)

Baule, R.: The order flow of discount certificates and issuer pricing behavior. J. Bank. Finance 35(11), 3120–3133 (2011)

Baule, R., Entrop, O., Wilkens, M.: Credit risk and bank margins in structured financial products: evidence from the German secondary market for discount certificates. J. Futur. Mark. 28(4), 376–397 (2008)

Berry, T.D., Howe, K.M.: Public information arrival. J. Financ. 49(4), 1331–1346 (1994)

Brunnermeier, M.K., Parker, J.A.: Optimal beliefs, asset prices, and the preference for skewed returns. Am. Econ. Rev. 97(2), 159–165 (2007)

Doran, J.S., Jiang, D., Peterson, D.R.: Gambling preference and the new year effect of assets with lottery features. Rev. Financ. 16(3), 685–731 (2011)

Dorn, D., Sengmueller, P.: Trading as entertainment? Manag. Sci. 55(4), 591–603 (2009)

Entrop, O., Schober, A., Wilkens, M.:. The pricing policy of banks on the German secondary market for leverage certificates: interday and intraday effects. In: Working Paper (2011)

Gaoa, X., Linb, T.-C.: Do individual investors trade stocks as gambling? Evidence from repeated natural experiments. In: Working Paper (2012)

Garrett, T.A., Sobel, R.S.: Gamblers favor skewness, not risk: further evidence from United States lottery games. Econ. Lett. 63(1), 85–90 (1999)

Grinblatt, M., Keloharju, M.: Sensation seeking, overconfidence, and trading activity. J. Financ. 64(2), 549–578 (2009)

Han, B., Kumar, A.: Speculative retail trading and asset prices. J. Financ. Quant. Anal. 48(2), 377–404 (2012)

Harris, L.: Optimal dynamic order submission strategies in some stylized trading problems. Financ. Market. Inst. Instrum. 7(2), 1–76 (2001)

Kelley, E.K., Tetlock, P.C.: How wise are crowds ? Insights from retail orders and stock returns. J. Financ. 63(3), 1229–1265 (2012)

Kumar, A.: Who gambles in the stock market? J. Financ. 64(4), 1889–1933 (2009)

Lakonishok, J., Lee, I., Pearson, N.D., Poteshman, A.M.: Option market activity. Rev. Financ. Stud. 20(3), 813–857 (2007)

Newey, W.K., West, K.D.: A simple, positive semi-definite, heteroskedasticity and autocorelation consistent covariance matrix. Econometrica 55(3), 703–708 (1987)

Odean, T.: Do investors trade too much? Am. Econ. Rev. 89(5), 1279–1298 (1999)

Page, J.K., Spalt, O.G., Kumar, A.: Gambling and comovement. In: Working Paper (2012)

Riordan, R., Storkenmaier, A., Wagener, M., Zhang, S.: Public information arrival: price discovery and liquidity in electronic limit order markets. J. Bank. Financ. 37(4), 1148–1159 (2013)

Rubinstein, M., Reiner, E.: Breaking down the barriers. Risk 4, 28–35 (1991)

Schmitz, P., Weber, M.: Buying and selling behavior of individual investors in option-like securities. Die Betr. 5 (2012)

Stoimenov, P., Wilkens, S.: Are structured products fairly priced? An analysis of the German market for equity-linked instruments. J. Bank. Financ. 29(12), 2971–2993 (2005)

Storkenmaier, A.: Financial Markets and Public Information. KIT Scientific Publishing, Karlsruhe (2011)

Wallmeier, M.: Beyond payoff diagrams: how to present risk and return characteristics of structured products. Financ. Market. Portf. Manag. 25(3), 313–338 (2011)

Acknowledgments

The Financial support from Boerse Stuttgart is gratefully acknowledged. The views expressed here are those of the authors and do not necessarily represent the views of Boerse Stuttgart. The authors thank an anonymous referee for valuable feedback.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Meyer, S., Schroff, S. & Weinhardt, C. (Un)skilled leveraged trading of retail investors. Financ Mark Portf Manag 28, 111–138 (2014). https://doi.org/10.1007/s11408-014-0225-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11408-014-0225-1