Abstract

We show that many currently popular monetary policy rules fall structurally within a class of robust industrial control known as proportional-integral-differential, or PID, control. From this identification we propose a general class of PID-based monetary policy rules that include as limiting cases the original Taylor rule as well as lagged and forward-looking extensions of thereof. The effectiveness of parsimonious extensions of the Taylor rule are consistent with the well-known effectiveness and parsimony of PID control. We find that for the same reason encountered in other PID control applications—noisy data—most monetary policy rules fall in the proportional-integral subset of PID control known as PI control. We estimate both PID and PI monetary policy rules using the historical analysis approach of Taylor and compare the performance of our PI rule to other policy rules using a recently-developed macroeconomic-model comparison methodology. A key feature of PID control is its remarkable effectiveness for systems where the equations of motion are not known. Thus, PID-based rules both link monetary policy with a tradition of practical control in the absence of known dynamical equations and provide baseline rules for monetary policy in the face of macroeconomic model uncertainty.

Similar content being viewed by others

Notes

For an engaging account of the history of monetary-policy rules see Woodford (2003), chapter 1.

For an interesting and comprehensive account of the history, breadth, and current practice of feedback control in general and PID control in particular see Bennett (1993), Åström and Murray (2008). As discussed below, the vast majority of implementations of PID control in control engineering and, as we shall see in monetary policy, are in fact reduced forms of PID control such as PI control. In keeping with the tradition of control engineering, however, we use the term PID control as a general label for both PID and PI control.

Taylor (1993a) originally presented his rule in terms of average inflation and of output gap as \(r(t) = \pi (t) + 0.5 y(t) +0.5 \left( \pi (t) - 2 \right) + 2\) which can be easily rewritten in “gapped” form as \(r(t) = 4 + 0.5 y(t) +1.5 \left( \pi (t) - 2 \right) \).

\(K_0\) is the nominal Fed funds rate associated with inflation gap and GDP gap being equal to zero. \(K_P^{(\pi )}\) and \(K_P^{(y)}\) are the proportionality constants for the inflation gap and output gap respectively.

Alternatively, one could differentiate Eq. (4) with respect to time resulting in

$$\begin{aligned} \frac{dr(t_k)}{dt} = \frac{d \varvec{K}_P \varvec{\cdot }\varvec{g}(t_k)}{dt} + \varvec{K}_I \varvec{\cdot }\varvec{g}(t_k) + \frac{d^2 \varvec{K}_D \varvec{\cdot }\varvec{g}(t_k)}{dt^2} , \end{aligned}$$discretize the first-order derivatives with Eq (5) and the second-order derivatives with

$$\begin{aligned} \frac{d^2 \varvec{g}(t_k)}{dt^2} \approx \frac{\varvec{g}(t_k) + \varvec{g}(t_{k-2}) - 2 \varvec{g}(t_{k-1})}{\left( \varDelta t \right) ^2}, \end{aligned}$$set \(\varDelta t = 1\) and collect terms to obtain Eq. (7).

The velocity algorithm is formally similar to the “first-difference rules” in the monetary policy literature (cf. e.g. Levin et al. 2003). Our derivation can be viewed as a formal representation of their observation that “[a] rule with a high value [of the lagged interest-rate parameter] implicitly makes the current interest rate depend on the complete history of output and inflation, albeit in a very restricted way.” Levin et al. (2003), p. 287.

For a discussion of and references to both approaches see Taylor (1999a).

We employed ordinary least squares (OLS) analysis with Newey-West Heteroskedasticity and Autocorrelation Consistent (HAC) standard errors on quarterly (Q1 1987–Q4 1992) vintage data sourced from the ArchivaL Federal Reserve Economic Data (ALFRED) repository at the Federal Reserve Bank of St. Louis: http://alfred.stlouisfed.org/.

This was expected given that we used similar data.

A sense of the historical data that is reviewed in the FOMC meetings can be found in the material on the Board of Governors’ website (http://www.federalreserve.gov/monetarypolicy/fomccalendars.htm).

This reference and further information on The Macroeconomic Model Data Base (MMB) project can be found at http://www.macromodelbase.com. The macroeconomic models in this database are solved using Dynare (cf. Juillard 1996, 2001 and http://www.dynare.org).

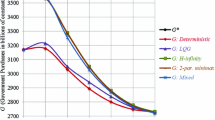

In a recent paper Taylor and Wieland (2012) present the results of a novel approach to monetary-policy rule tuning that used macroeconomic simulation to obtain rule parameters that minimized the variance of the inflation, output and interest rate across three current-generation macroeconomic models (Taylor 1993b; Altig et al. 2005; Smets and Wouters 2007). With this tuning they obtained the model-averaged policy rule \(r_t = 1.06 r_{t-1} + 0.19 \pi _t + 0.67 y_t - 0.59 y_{t-1}\). Comparing the PI rule with their model-averaged rule we see first that the parameter for the lagged interest-rate (by definition unity in the PI rule) is also very close toFoornote 16 continued

unity in the Taylor and Wieland (2012) rule. This feature has often been implicated as evidence of interest-rate smoothing by central banks but, as shown in our derivation, it is a simple consequence of the velocity derivation of the PI rule. Earlier research has also linked a parameter near unity for the lagged interest rate with monetary-policy robustness (Levin et al. 2003). Comparison of the other variables is complicated by the fact that Taylor and Wieland (2012) assumed \(\beta _1^{(\pi )} = 0\): this was not a consequence of the tuning. The size and sign of the common parameters between these rules, however, suggests that the parameters of a PI rule tuned using macroeconomic simulation may be similar to those we obtained using historical analysis: a topic of future research.

A reference for each model is provided in the Appendix below. For a discussion of the MMB software see Wieland et al. (2011).

This quote is from the 2006 edition of Åström and Murray (2008).

As our derivation begins with the original Taylor rule, it is not independent of macroeconomic modelling in general. The ubiquity of the Taylor rule, however, suggests that it, like our derivation, transcends specific macroeconomic models.

References

Adolfson M, Laséen S, Lindé J, Villani M (2007) Bayesian estimation of an open economy DSGE model with incomplete pass-through. J Int Econ 72:481–511

Altig DE, Christiano LJ, Eichenbaum M, Lindé J (2005) Firm-specific capital, nominal rigidities and the business cycle. CERP Discussion Papers 4858, Centre for Economic Policy Research

Aoki M (1967) Optimization of stochastic systems: topics in discrete-time systems, mathematics in science and engineering, vol 32. Academic Press, New York, NY

Aoki M (1996) New approaches to macroeconomic modeling: evolutionary stochastic dynamics, multiple equilibria, and externalities as field effects. Cambridge University Press, New York, NY

Aoki M (2000) Modeling aggregate fluctuations in economics: stochastic views of interacting agents. Cambridge University Press, New York, NY

Aoki M, Yoshikawa H (2007) Reconstructing macroeconomics: a perspective from statistical physics and combinatorial stochastic processes. Japan-US Center UFJ Bank Monographs on International Financial Markets, Cambridge University Press, New York, NY

Åström KJ, Murray RM (2008) Feedback systems: an introduction for scientists and engineers. Princeton University Press, Princeton, NJ

Batini N, Haldane A (1999) Forward-looking rules for monetary policy. In: Taylor (1999b), pp 157–192

Bennett S (1993) A history of control engineering 1930–1955. Peter Peregrinus Ltd., Stevenage

Carabenciov I, Ermolaev I, Freedman C, Juillard M, Kamenik O, Laxton D (2008) A small quarterly projection model of the US economy. IMF Working Paper 08/278, International Monetary Fund

Christensen I, Dib A (2008) The financial accelerator in an estimated New Keynesian model. Rev Econ Dyn 11:155–178

Christiano LJ, Eichenbaum M, Evans CL (2005) Nominal rigidities and the dynamic effects of a shock to monetary policy. J Polit Econ 113:1–45

Christoffel K, Kuester K (2008) Resuscitating the wage channel in models with unemployment fluctuations. J Monet Econ 55:865–887

Christoffel K, Kuester K, Linzert T (2009) The role of labor markets for euro area monetary policy. Eur Econ Rev 53:908–936

Clarida R, Galí J, Gertler M (1998) Monetary policy rules in practice: some international evidence. Eur Econ Rev 42:1033–1067

Clarida R, Galí J, Gertler M (1999) The science of monetary policy: a New Keynesian perspective. J Econ Lit 37:1661–1701

Coenen G, Wieland V (2005) A small estimated euro area model with rational expectations and nominal rigidities. Eur Econ Rev 49:1081–1104

Colander D (ed) (2006) Post Walrasian macroeconomics: beyond the dynamic stochastic general equilibrium model. Cambridge University Press, Cambridge

de Castro MR, Gouvea SN, Minella A, dos Santos RC, Souza-Sobrinho NF (2011) SAMBA: stochastic analytical model with a Bayesian approach. Banco Central do Brasil Working Paper Series 239, Banco Central do Brasil

De Graeve F (2008) The external finance premium and the macroeconomy: US post-WWII evidence. J Econ Dyn Control 32:3415–3440

Fuhrer JC, Moore G (1995) Inflation persistence. Q J Econ 110:127–159

Funke M, Paetz M, Pytlarczyk E (2011) Stock market wealth effects in an estimated DSGE model for Hong Kong. Econ Model 28:316–334

Galí J, Monacelli T (2005) Monetary policy and exchange rate volatility in a small open economy. Rev Econ Stud 72:707–734

Gelain P (2010) The external finance premium in the euro area: a dynamic stochastic general equilibrium analysis. N Am J Econ Financ 21:49–71

Gerdesmeier D, Roffia B (2005) Empirical estimates of reaction functions for the euro area. Swiss J Econ Stat 140:37–66

Iacoviello M (2005) Housing prices, borrowing constraints, and monetary policy in the business cycle. Am Econ Rev 95:739–764

Ireland PN (2004) Money’s role in the monetary business cycle. J Money Credit Bank 36:969–983

Ireland PN (2011) A New Keynesian perspective on the great recession. J Money Credit Bank 43:31–54

Juillard M (1996) Dynare: a program for the resolution and simulation of dynamic models with forward variables through the use of a relaxation algorithm. CEPREMAP Working Papers (Couverture Orange) 9602, CEPREMAP

Juillard M (2001) Dynare: a program for the simulation of rational expectation models. Computing in Economics and Finance 2001 213, Society for Computational Economics

Laxton D, Pesenti P (2003) Monetary rules for small, open, emerging economies. J Monet Econ 50: 1109–1146

Levin A, Wieland V, Williams JC (1999) Robustness of simple monetary policy rules under model uncertainty. In: Taylor (1999b), pp 263–318

Levin A, Wieland V, Williams JC (2003) The performance of forecast-based monetary policy rules under model uncertainty. Am Econ Rev 93:622–645

Lubik TA, Schorfheide F (2007) Do central banks respond to exchange rate movements? A structural investigation. J Monet Econ 54:1069–1087

Maxwell JC (1867–1868) On governors. Proc R Soc 16:270–283

McCallum B, Nelson E (1999) Performance of operational policy rules in an estimated semiclassical structural model. In: Taylor (1999b), pp 15–56

Medina JP, Soto C (2007) The Chilean business cycles through the lens of a stochastic general equilibrium model. Working Paper Series of the Central Bank of Chile 457, Banco Central de Chile

Orphanides A (2001) Monetary policy rules based on real-time data. Am Econ Rev 91:964–985

Orphanides A, Wieland V (1998) Price stability and monetary policy effectiveness when nominal interest rates are bounded at zero. Finance and Economics Discussion Series 98–35, Board of Governors of the Federal Reserve System

Rabanal P (2007) Does inflation increase after a monetary policy tightening? Answers based on an estimated DSGE model. J Econ Dyn Control 31:906–937

Ratto M, Roeger W, in ’t Veld J (2009) QUEST III: an estimated open-economy DSGE model of the euro area with fiscal and monetary policy. Econ Model 26:222–233

Rotemberg JJ, Woodford M (1997) An optimization-based economic framework for the evaluation of monetary policy. NBER Macroecon Annu 12:297–346

Smets F, Wouters R (2007) Shocks and frictions in US business cycles: a Bayesian DSGE approach. Am Econ Rev 97:586–606

Taylor JB (1993a) Discretion versus policy rules in practice. Carnegie-Rochester Conf Ser Public Policy 39:195–214

Taylor JB (1993b) Macroeconomic policy in a world economy: from econometric design to practical operation. W. W. Norton & Co, New York

Taylor JB (1999a) A historical analysis of monetary policy. In: Taylor (1999b), pp 319–348

Taylor JB (ed) (1999b) Monetary policy rules, NBER—business cycles series, vol 31. University of Chicago Press, Chicago, IL

Taylor JB, Wieland V (2012) Surprising comparative properties of monetary models: results from a new model database. Rev Econ Stat 94(3):800–816

Taylor JB, Williams JC (2011) Simple and robust rules for monetary policy. In: Friedman BM, Woodford M (eds) Monetary economics, handbooks in economics, vol 3B. North-Holland, Amsterdam, pp 829–859

Wicksell K (1898) Geldzins und Güterpreise. G. Fischer, Jena, reprint translation by R. F. Kahn as Interest and Prices published by R. & R. Clark, Edinburgh

Wicksell K (1907) The influence of the rate of interest on prices. Econ J 17(66):213–220

Wieland V, Cwik T, Müller GJ, Schmidt S, Wolters M (2011) A new comparative approach to macroeconomic modeling and policy analysis. Working paper, Goethe University of Frankfurt, Frankfurt am Main, Germany. http://www.macromodelbase.com/, September 2011 (revised edition)

Woodford M (2003) Interest and prices: foundations of a theory of monetary policy. Princeton University Press, Princeton, NJ

Acknowledgments

We thank Stuart Bennett for his illuminating insights on the history of PID control. We thank Volker Wieland, Sebastian Schmidt and Elena Afanasyeva for very helpful conversations concerning the MMB software. Finally, we thank Masanao Aoki for his pioneering and inspiring work bridging control theory and practice in engineering and economics.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Hawkins, R.J., Speakes, J.K. & Hamilton, D.E. Monetary policy and PID control. J Econ Interact Coord 10, 183–197 (2015). https://doi.org/10.1007/s11403-014-0127-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11403-014-0127-3