Abstract

In this paper, we suggest a distributed process of price adjustment toward a partial market equilibrium. As the main contribution, our algorithm of price adjustment is computationally efficient and decentralized. Its convergence properties are crucially based on convex analysis. The proposed price adjustment corresponds to a subgradient scheme for minimizing a special nonsmooth convex function. This function is the total excessive revenue of the market’s participants and its minimizers are equilibrium prices. As the main result, the algorithm of price adjustment is shown to converge to equilibrium prices. Additionally, the market clears on average during the price adjustment process, i.e., by historical averages of supply and demand. Moreover, a global rate of convergence is obtained. We endow our algorithm with decentralized prices by introducing the trade design with price initiative of producers. The latter suggests that producers settle and update their individual prices, and consumers buy at the lowest purchase price.

Similar content being viewed by others

Notes

The term “responsible” is introduced to capture that a consumer just seeks to satisfy given utility level, and not more. It is not meant to have idealistic, moralistic or paternalistic connotation.

References

Nesterov, Yu., Shikhman, V.: Quasi-monotone subgradient methods for nonsmooth convex minimization. J. Optim. Theory Appl. 165, 917–940 (2015)

Nesterov, Y., Shikhman, V.: Excessive revenue model of competitive markets. In: Mordukhovich, B.S., Reich, S., Zaslavski, A.J. (eds.) Nonlinear Analysis and Optimization, AMS Contemporary Mathematics, vol. 659. AMS eBook Collections, Providence (2016)

Nesterov, Y.: Introductory Lectures on Convex Optimization. Kluwer, Boston (2004)

Révész, P.: The Laws of Large Numbers. Academic Press, New York and London (1968)

Gale, D.: The Theory of Linear Economic Models. McGraw Hill, New York (1960)

Chen, L., Ye, Y., Zhang, J.: A note on equilibrium pricing as convex optimization. Internet and Network Economics, Lecture Notes in Computer Science 4858, 7–16 (2007)

Codenotti, B., Varadarajan, V.: Efficient computation of equilibrium prices for markets with leontief utilities. Automata, Languages and Programming, Lecture Notes in Computer Science 3142, 371–382 (2004)

Devanur, N.R., Papadimitriou, Ch.H., Saberi, A., Vazirani, V.V.: Market equilibrium via a primal-dual algorithm for a convex program. J. AC 55, Article No. 22 (2008)

Jofré, A., Rockafellar, R.T., Wets, R.J.-B.: Convex analysis and financial equilibrium. Math. Program. 148, 223–239 (2014)

Fisher, F.M.: On price adjustment without an auctioneer. Rev. Econ. Stud. 39, 1–15 (1972)

Hahn, F.H., Negishi, T.: A theorem on non-Tâtonnement stability. Econometrica 30, 463–469 (1962)

Mas-Colell, A., Whinston, M.D., Green, J.R.: Microeconomic Theory. Oxford University Press, New York (1995)

Rubinstein, A.: Lecture Notes in Microeconomic Theory: The Economic Agent. Princeton University Press, Princeton (2012)

Kreps, D.M.: Microeconomic Foundations I: Choice and Competitive Markets. Princeton University Press, Princeton (2012)

Krishna, V., Sonnenschein, H.: Duality in consumer theory. In: Chipman, J., McFadden, D., Richter, M. (eds.) Preferences, Uncertainty and Optimality, pp. 44–55. Westview Press, Boulder, CO (1990)

Rubinstein, A.: Equilibrium in the Jungle. Econ. J. 117, 883–896 (2007)

Mullainathan, S., Thaler, R.H.: Behavioral economics. In: Smelser, N.J., Baltes, P.B. (eds.) International Encyclopedia of Social and Behavioral Sciences. Elsevier, London (2001)

Zălinescu, C.: Convex Analysis in General Vector Spaces. World Scientific, Singapore (2002)

Rockafellar, R.T.: Convex Analysis. Princeton University Press, Princeton (1970)

Rosen, J.B.: Existence and uniqueness of equilibrium points for concave \(n\)-person games. Econometrica 31, 520–534 (1965)

Samuelson, P.A.: The stability of equilibrium: comparative statics and dynamics. Econometrica 9, 97–120 (1941)

Acknowledgments

The research of the first author has been supported by a Grant “Action de recherche concertè ARC 04/09-315” from the “Direction de la recherche scientifique - Communautè française de Belgique”. The research of the second author has been supported by a Grant “Chargé de recherches 98444” from the “Fonds de la Recherche Scientifique - FNRS, Belgique”. The scientific responsibility rests with its authors. We also thank the anonymous referee for the valuable comments, which improved the quality of the paper

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

This Appendix is devoted to the proof of Lemma 4.1. For that, we first present the quasi-monotone subgradient method for nonsmooth convex minimization from [1]. As already mentioned, the price adjustment process (PA) can be seen as an implementation of this scheme. Here, in addition to [1], the quasi-monotone subgradient method is modified in order to incorporate varying step sizes for different goods. Using this fact, we prove Lemma 4.1 in the second part of “Appendix”.

1.1 Quasi-monotone Subgradient Method

Consider the following minimization problem:

where \(X \subset \mathbb {R}^n\) is a closed convex set with nonempty interior \(\text{ int }\,X\), and f is a convex function on \(\mathbb {R}^n\). Moreover, let f be representable as a maximum of concave functions, i.e.,

where \(A \subset \mathbb {R}^m\) is a closed and convex set, \(\varphi (\cdot ,a)\) is a convex function on \(\mathbb {R}^n\) for every \(a \in A\), and \({\varPhi }, \varphi (x,\cdot )\) are concave functions on \(\mathbb {R}^m\) for every \(x \in X\). Denote by a(x) one of the optimal solutions of the maximization problem in (33). Then, \( \nabla f(x) := \nabla _x \varphi (x, a(x))\) is a subgradient of f at x. Recall that for an arbitrary subgradient \(\nabla f(x)\) at \(x \in X\) of a convex function f we have:

Using the representation (33), we also have:

The latter maximization problem is called adjoint to (32) with the adjoint variable \(a \in A\).

For the set X, we assume to be known a prox-function d(x).

Definition 5.1

\(d\,{:}\,X \mapsto \mathbb {R}\) is called a prox-function for X if the following holds:

-

\(d(x) \ge 0\) for all \(x \in X\) and \(d(x[0]) = 0\) for certain \(x[0] \in X\);

-

d is strongly convex on X with convexity parameter one:

$$\begin{aligned} d(y) \ge d(x) + \langle \nabla d(x), y-x \rangle + \frac{1}{2} \Vert y-x\Vert ^2, \quad x,y \in X, \end{aligned}$$(35)where \(\Vert \cdot \Vert \) is a norm on \(\mathbb {R}^n\).

-

Auxiliary minimization problem

$$\begin{aligned} \min _{x \in X} \left\{ \langle z, x\rangle + \chi d(x) \right\} \end{aligned}$$(36)is easily solvable for \(z \in \mathbb {R}^n, \chi > 0\).

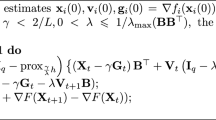

For a sequence of positive parameters \(\left\{ \chi [t] \right\} _{t \ge 0}\), we consider the following iteration:

Next Theorem 5.1 is crucial for the convergence analysis of the quasi-monotone subgradient method (SM). It estimates the duality gap for the minimization problem (32) and its adjoint problem evaluated at the historical averages.

For that, we define the penalty term \(h_t\) and the remainder term \(\rho _t, t \ge 0\), as follows:

Here, \(\Vert \cdot \Vert _*\) is the conjugate norm to \(\Vert \cdot \Vert \), i.e.,

Further, we define the average adjoint state \(a[t] := \frac{1}{t+1} \sum \nolimits _{r=0}^{t} a(x[r]), \quad t \ge 0. \) Note that \(a[t] \in A\), since A is convex. Theorem 5.1 is motivated by the estimating sequence technique (e.g., Section 2.2.1 in [3]).

Theorem 5.1

[1] Let the sequence \(\left\{ x[t] \right\} _{t \ge 0}\) be generated by (SM) with nondecreasing parameters

Then, for all \(t \ge 0\) we have

Additionally, we need the following simple result on the quadratic penalty for the general convex optimization problems. From now on, let us consider the maximization problem

where \(A \subset \mathbb {R}^m\) is a closed convex set, \({\varPhi }\) is a concave function, and \(g_l(\cdot ), l=1,\ldots , L\) are convex functions on \(\mathbb {R}^m\). We assume that the convex feasible set of the maximization problem (40) has a Slater point (e.g., [19]).

Lemma 5.1

For any \(\kappa > 0\), we have

where \(\lambda _l^*, l=1, \ldots , L\) are Lagrange multipliers for an optimal solution of (40).

1.2 Proof of Lemma 4.1

We start by proving that the price adjustment process (PA) is a variant of the quasi-monotone subgradient method (SM). For that, it enough to show that

-

(1)

the price forecast (25) can be obtained using the Euclidean prox-function,

-

(2)

\(\mathcal {E}\) can be represented as the maximum of a parametric family of concave functions.

Firstly, we define the Euclidean prox-functions:

where \(\zeta _k^{(j)}\) are positive scaling coefficients. The corresponding norms in Definition 5.1 and their conjugates according to (37) are

For \(z_k[t] \in \mathbb {R}^n, \chi _k[t] > 0\), consider the auxiliary minimization problem of Step 3 in (SM):

Its unique solution is the price forecast (25) defined in Step 3 of (PA):

Secondly, it follows from (21) in Lemma 3.2, that the total excessive revenue is representable as a maximum of concave functions:

where

Overall, we can apply Theorem 5.1 in order to get the following inequality:

where

Let us relate the penalty term \(h_t\) to Q[t] from Lemma 4.1. For that, we define the Euclidean prox-function \( d(p) := \frac{1}{2} \sum _{j=1}^{n} \left( p^{(j)}\right) ^2. \) Note that

where \(C_2 = \min _{k,j} \frac{\zeta _k^{(j)}}{2}\). Now, we relate the remainder term \(\rho _t\) to \(b_t\) from Lemma 4.1. For that, let the constant \(C_3 > 0\) bound the sequence of kth producer’s excess supplies:

The existence of \(C_3\) in (43) follows from the compactness of production sets \(\mathcal {Y}_k, k=1, \ldots , K\), and consumption sets \(\mathcal {X}_i, i=1, \ldots , I\) (see Sect. 2). Then, it holds:

Altogether, substituting this into (42), we get the right-hand side of (28) in Lemma 4.1.

Now, we estimate the duality gap in Lemma 4.1 from below. For that, we apply Lemma 5.1 and Theorem 3.4:

where \(C_1 = \frac{\sum \nolimits _{j=1}^{n} p^{*(j)}}{{4C_2}}\) and \(p^*\) is the vector of equilibrium prices. Note that Lagrange multipliers for the market feasibility constraint in the adjoint problem (A) coincide with minimizers \(p^*\) of the total excessive revenue \(\mathcal {E}\). \(\square \)

Rights and permissions

About this article

Cite this article

Nesterov, Y., Shikhman, V. Distributed Price Adjustment Based on Convex Analysis. J Optim Theory Appl 172, 594–622 (2017). https://doi.org/10.1007/s10957-016-0975-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10957-016-0975-1

Keywords

- Computation of market equilibrium

- Distributed price adjustment

- Convex optimization

- Subgradient methods

- Decentralization of prices