Abstract

This paper explores the effects of changes in bank credit on firm growth before and after the recent global financial crisis, taking into account firm-specific and country-specific characteristics as well as structural characteristics of domestic banking sectors. Panel quantile analysis is used on a sample of 2075 euro area firms in 2005–2011, enabling thus the identification of potential differences in the dynamics between high-growth and low-growth firms. The post-2008 credit crunch is found to seriously affect mostly high-leveraged, low-growth firms operating in concentrated banking systems with weak foreign presence, and in riskier and less financially developed European economies. By contrast, high-growth firms are not affected and, thus, may be expected to facilitate and sustain the post-crisis credit-less recovery in the euro area. A policy implication of our findings is that creating the right conditions for the emergence of innovative high-growth firms may be a more effective growth strategy, especially in adverse times, as compared to a general policy covering all types of firms.

Similar content being viewed by others

Notes

Hölzl (2010) argues that the most fruitful direction for entrepreneurship policy in developed economies is to focus on innovation and firm growth in the Schumpeterian context, being different from SME’s policy which is highly correlated with self-employment.

Several studies (e.g., Dell’ Ariccia et al. 2008; Claessens et al. 2012; Puri et al. 2011; Jimenéz et al. 2012) recognize that in times of financial crises, apart from credit supply, credit demand may also be an important constraining factor of credit growth through the firm balance-sheet channel. In other words, a demand-side explanation of the fall in lending focuses on the generally weak state of borrowers’ balance sheets. This, in turn, leads firms to abandon investment projects and, ultimately, demand for bank credit. Thus, potential borrowers who are more leveraged or possess collateral of lower quality will express lower demand for bank credit and may delay investment.

In this direction, the creation of a capital market union in Europe would be important in offering an alternative credit channel to the business sector and help reduce obstacles to finance (ECB 2015a).

The problem was solved using the algorithms of “R” econometric software, and in particular the command package “rqpd” as more suitable for the purposes of the specific analysis.

A cleaning process was performed in order to reach the final sample of 2075 quoted firms. The initial sample consisted of 7237 firms participating exclusively in the stock market of their country of origin. The cleaning process we undertook was based on the following two steps: first, we excluded firms operating in the financial sector; and second we selected those quoted firms for which data on firm-level variables, (i.e., for firm growth and financial variables such as liquidity and leverage), were available annually over the 7-year period.

The density presented in Fig. 1 is estimated using the bandwidth of 0.5. The bandwidth parameter (i.e., the width of the neighborhood at each point) determines the degree of smoothing in the density under estimation (Silverman 1986). Estimation with different bandwidths does not yield qualitatively different results.

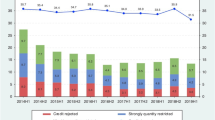

New loans are considered as the typical measure for bank credit growth since they refer to net additions to the existing stock and reflect current credit policy decisions on behalf of the banks. In addition, as it is noted in the ECB’s Economic Bulletin 4/2015 (p.49) “ during the crisis period, “credit-constrained firms”—those firms which in the Survey on the Access to Finance of Enterprises in the Euro Area (ECB 2015b), reported that they had limited access to bank loans - tended to switch to non-bank financing (trade credit, leasing) more often than firms without credit constraints. It appears, though, that firms in the countries most affected by the crisis faced more difficulties in making this switch in financing.” As a result, new loans reflect bank credit conditions in an harmonized manner across the euro area, while credit lines, overdrafts and other forms of financing may be incorporating country-specific aspects of credit provision.

We consider 2009 as the first year of crisis that hit the euro area since in that year all the member countries experienced a sharp recession while, in the previous years, almost all of them exhibited positive GDP growth rates. In particular, the percentage changes in GDP in 2009 by country were the following: Belgium: -2.8 %, Germany: −5.1 %, Estonia: −14.1 %, Ireland: −6.4 %, Greece: −3.1 %, Spain: −3.8 %, France: −3.1 %, Italy: −5.5 %, Cyprus: −1.9 %, Latvia: −17.7 %, Luxembourg: −5.6 %, Malta: −2.8 %, Netherlands: −3.7 %, Austria: −3.8 %, Portugal: −2.9 %, Slovenia: −7.9 %, Slovakia: −4.9 %, Finland: −8.5 % and euro area: −4.5 %. For more details see the European Economic Forecast report provided by European Commission (2013).

Using total assets instead of sales as a proxy for firm size does not alter the results in any significant way. To perform a robustness check we run complementary regressions using total assets as a proxy for firm size. The relevant results are available upon request from the authors.

Several empirical works in industrial economics and financial economics literature examining the effects of financial factors on firm performance (e.g., Fotopoulos and Louri 2004; Greenaway et al. 2007; Tsoukas 2011) use as proxy for firm leverage the ratio of total debt over total assets in order to capture the overall indebtedness of firms or in other words the degree of debt burden. Also, Greenaway et al. (2007) use current ratio as indicator of firm liquidity since it allows to measure a firm’s ability to meet short-term debt obligations. Thus, they stress that the higher the current ratio, the more liquid the firm is. Moreover, Musso and Schiavo (2008) explore the effects of liquidity constraints on firm growth and survival measuring liquidity by the ratio of current assets over current liabilities.

Political risk is a variable that considers jointly factors such as: government stability, socioeconomic stability, investment profile, internal conflict, external conflict, corruption, military involvement in politics, religion involvement in politics, law and order, ethnic tensions, democratic accountability, and bureaucratic quality. Economic risk is composed of GDP per capita, real GDP growth, annual inflation rates, budget balance as a percentage of GDP, and current account balance as a percentage of GDP. Financial risk assesses the ability of a country to finance its official, commercial, and trade debt obligations. This index considers foreign debt as a percentage of the country’s GDP, foreign debt service as a percentage of exports of goods and services, current account as a percentage of exports of goods and services, net international liquidity as the months of import cover, and exchange rate stability.

The Global Financial Development Database is an extensive dataset of financial system indicators for 203 countries, containing annual data until 2011. Čihák et al. (2012) provide an extensive description of the database.

The lack of information covering the whole 2005–2011 period for this variable is the main reason for the classification of countries in the two groups. With the values of foreign bank presence ending in 2009, it could not be possible to estimate our model over the entire period (2005–2011). However, the separate regressions enabled the estimation of differential effects between these two groups.

An alternative to private credit over GDP is total banking assets over GDP, which is also included in the Global Financial Development Database. Compared to private credit, this variable includes also credit to government and bank assets other than credit. However, this proxy is available for a smaller number of countries and has been used less extensively in the literature on financial development. Čihák et al. (2012) find a strong correlation coefficient of about 0.9 between these two proxies.

The estimation results from the respective OLS model are more or less in the same direction regarding firm-specific and country-specific variables. These results are available upon request.

Separate estimations for different size groups of firms (micro, small, medium, large) yield interestingly differentiated results as presented in Dimelis et al. (2015).

References

Abiad A, Dell’Ariccia G, Li B (2014) What have we learned about creditless recoveries? In: Claessens S, Kose A, Laeven L, Valencia F (eds) Financial crises: causes, consequences, and policy responses. International Monetary Fund, Washington, pp 309–322

Acs Z, Mueller P (2008) Employment effects of business dynamics: mice, gazelles and elephants. Small Bus Econ 30:85–100

Aghion P, Fally T, Scarpetta S (2007) Credit constraints as a barrier to the entry and post-entry growth of firms. Econ Policy 22:731–779

Audretsch D, Klomp K, Santarelli E, Thurik A (2004) Gibrat’s law: are the services different? Rev Ind Organ 24:301–324

Beck T, Demirgüç-Kunt A (2006) Small and medium-size enterprises: access to finance as a growth constraint. J Bank Financ 30:2931–2943

Beck T, Demirgüç-Kunt A, Levine R (2003) A new database on financial development and structure. World Bank Econ Rev 14:597–605

Beck T, Demirgüç-Kunt A, Levine R (2006) Bank concentration, competition, and crises: first results. J Bank Financ 30:1581–1603

Bena J, Jurajda S (2011) Financial development and corporate growth in the EU single market. Economica 78:401–428

Berger A, De Young R, Genay H, Udell G (2000) Globalization of financial institutions: evidence from cross-border banking performance. Brookings-Wharton Papers on Financial Services 3:23–158

Bernanke B, Gertler M, Gilchrist S (1996) The financial accelerator and the flight to quality. Rev Econ Stat 78:1–15

Bijsterbosch M, Dahlhaus T (2015) Key features and determinants of credit-less recoveries. Empir Econ 49:1245–1269

Black SE, Strahan PE (2002) Entrepreneurship and bank credit availability. J Financ 57:2807–2833

Bottazzi G, Dosi G, Lippi M, Pammolli F, Riccaboni M (2001) Innovation and corporate growth in the evolution of the drug industry. Int J Ind Organ 19:1161–1187

Boyd J, De Nicolo G (2005) The theory of bank risk-taking and competition revisited. J Financ 60:1329–1343

Bruno V, Hauswald R (2014) The real effect of foreign banks. Rev Financ 18:1683–1716

Buchinski M (1994) Changes in the U.S. wage structure 1963–1987: application of quantile regression. Econometrica 62:405–458

Calvo G, Izquierdo A, Talvi E (2006) Sudden stops and phoenix miracles in emerging markets. Am Econ Rev 96:405–410

Caminal R, Matutes C (2002) Market power and banking failures. Int J Ind Organ 20:1341–1361

Cetorelli N, Strahan P (2006) Finance as a barrier to entry: bank competition and industry structure in local US markets. J Financ 61:437–461

Chava S, Purnanandam A (2011) The effect of banking crisis on bank-dependent borrowers. J Financ Econ 99:116–135

Čihák M, Demirgüç-Kunt A, Feyen E, Levine R (2012) Benchmarking financial systems around the world. Policy Research Working Paper No. 6175, World Bank, Washington, DC

Claessens S (2006) Access to financial services: a review of the issues and public policy objectives. World Bank Res Obs 21:207–240

Claessens S, Van Horen N (2014) Foreign banks: trends and impact. J Money Credit Bank 46:295–326

Claessens S, Kose MA, Terrones ME (2009) What happens during recessions, crunches and busts? Econ Policy 24:653–700

Claessens S, Tong H, Wei SJ (2012) From the financial crisis to the real economy: using firm-level data to identify transmission channels. J Int Econ 88:375–387

Clarke G, Cull R, Peria M, Sanchez S (2003) Foreign bank entry: experience, implications for developing countries, and agenda for further research. World Bank Res Obs 18:25–40

Coad A, Rao R (2008) Innovation and firm growth in high-tech sectors: a quantile regression approach. Res Policy 37:633–648

Coad A, Daunfeldt SO, Hölzl W, Johansson D, Nightingale P (2014) High-growth firms: introduction to the special section. Ind Corp Chang 23:91–112

Constancio V (2013) Banking Union and the future of banking, Speech at the IIEA Conference on the Future of Banking in Europe, December 2013, https://www.ecb.europa.eu/press/key/date/2013/html/sp131202.en.html. Accessed 25 Jan 2016

Covin JG, Green KM, Slevin DP (2006) Strategic process effects on the entrepreneurial orientation–sales growth rate relationship. Entrep Theory Pract 30:57–81

Daunfeldt SO, Elert N, Johansson D (2014) The economic contribution of high-growth firms: do policy implications depend on the choice of growth indicator? J Ind Compet Trade 14:337–365

Dell’ Ariccia G, Detragiache E, Rajan R (2008) The real effect of banking crises. J Financ Intermed 17:89–112

Delmar F (1997) Measuring growth: methodological considerations and empirical results. In: Donckels R, Miettinen A (eds) Entrepreneurship and SME research: on its way to the next millenium. Ashgate Publishing, Aldershot

Delmar F, Davidsson P, Gartner WB (2003) Arriving at the high-growth firm. J Bus Ventur 18:189–216

Demirgüç-Kunt A, Detragiache E, Gupta P (2006) Inside the crisis: an empirical analysis of banking systems in distress. J Int Money Financ 25:702–718

Di Patti E, Dell’ Ariccia G (2004) Bank competition and firm creation. J Money Credit Bank 36:225–251

Dimelis S, Louri H (2002) Foreign ownership and production efficiency: a quantile regression analysis. Oxf Econ Pap 54:449–469

Dimelis S, Giotopoulos I, Louri H (2015) Can firms grow without credit? Evidence from the euro area, 2005–2011: a quantile panel analysis. GreeSe Working Paper Series No. 89, European Institute, London School of Economics and Political Science, http://eprints.lse.ac.uk/61157/1/__lse.ac.uk_storage_LIBRARY_Secondary_libfile_shared_repository_Content_Hellenic%20Observatory%20%28inc.%20GreeSE%20Papers%29_GreeSE%20Papers_GreeSE-No89.pdf. Accessed 25 Jan 2016

Draghi M (2014) Financial Integration and Banking Union, Speech at the conference for the 20th anniversary of the establishment of the European Monetary Institute (February 2014), https://www.ecb.europa.eu/press/key/date/2014/html/sp140212.en.html. Accessed 25 Jan 2016

Du J, Temouri Y (2015) High-growth firms and productivity: evidence from the United Kingdom. Small Bus Econ 44:123–143

ECB (2012) ECB monthly bulletin May 2012. European Central Bank, Frankfurt

ECB (2013) ECB monthly bulletin July 2013. European Central Bank, Frankfurt

ECB (2015a) Economic bulletin, April 2015. European Central Bank, Frankfurt

ECB (2015b) Survey on the access to finance of enterprises in the Euro area, June 2015. European Central Bank, Frankfurt

European Commission (2013) European economic forecast, Automn 2013. European Commission, Brussels

Fotopoulos G, Louri H (2004) Firm growth and fdi: are multinationals stimulating local industrial development? J Ind Compet Trade 4:163–189

Giannetti M, Ongena S (2009) Financial integration and firm performance: evidence from foreign bank entry in emerging markets. Rev Financ 13:181–223

Giotopoulos I, Fotopoulos G (2010) Intra-industry growth dynamics in the Greek services sector: firm-level estimates for ICT-producing, ICT-using, and non-ICT industries. Rev Ind Organ 36:59–74

Greenaway D, Guariglia A, Kneller R (2007) Financial factors and exporting decisions. J Int Econ 73:377–395

Henrekson M, Johansson D (2010) Gazelles as job creators: a survey and interpretation of the evidence. Small Bus Econ 35:227–244

Hölzl W (2010) The economics of entrepreneurship policy: introduction to the special issue. J Ind Compet Trade 10:187–197

Illes A, Lombardi M (2013) Interest rate pass-through since the financial crisis. Bank for International Settlements Quarterly Review, September 2013, 24:57–66, https://www.bis.org/publ/qtrpdf/r_qt1309g.pdf. Accessed 25 Jan 2016

IMF (2013) Global liquidity—credit and funding indicators. International Monetary Fund, Washington

Iyer R, Peydró JL, da-Rocha-Lopes S, Schoar A (2014) Interbank liquidity crunch and the firm credit crunch: evidence from the 2007–2009 crisis. Rev Financ Stud 27:347–372

Jimenéz G, Ongena S, Peydró JL, Saurina J (2012) Credit supply versus demand: Bank and firm balance-sheet channels in good and crisis times. Discussion Paper No.2012-003, European Banking Center, http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.360.6295&rep=rep1&type=pdf. Accessed 25 Jan 2016

Kaminsky G, Reinhart C (1999) The twin crises: the causes of banking and balance-of-payments problems. Am Econ Rev 89:473–500

Kannan P (2012) Credit conditions and recoveries from financial crises. J Int Money Financ 31:930–947

King R, Levine R (1993) Finance, entrepreneurship and growth. J Monet Econ 32:513–542

Koenker R (2004) Quantile regression for longitudinal data. J Multivar Anal 91:74–89

Laeven L, Valencia F (2013) The real effects of financial sector interventions during crises. J Money Credit Bank 45:147–177

Levine R (2005) Finance and growth: theory and evidence. Handbook of Economic Growth, 1:865–934

Mayordomo S, Abascal M, Alonso T, Rodriguez-Moreno M (2015) Fragmentation in the European interbank market: measures, determinants, and policy solutions. J Financ Stab 16:1–12

Musso P, Schiavo S (2008) The impact of financial constraints on firm survival and growth. J Evol Econ 18:135–149

OECD (2014) OECD economic outlook. Volume 2014/2. OECD Publishing, Paris

Ongena S, Peydró JL, Van Horen N (2013) Shocks abroad, pain at home? Bank-firm level evidence on the international transmission of financial shocks. CentER Discussion Paper, No 2013-040. Finance, Tilburg

Peek J, Rosengren E (2000) Collateral damage: effects of the Japanese bank crisis on real economic activity in the United States. Am Econ Rev 90:30–45

Puri M, Rocholl J, Steffen S (2011) Global retail lending in the aftermath of the US financial crisis: distinguishing between supply and demand effects. J Financ Econ 100:556–578

Rahaman M (2011) Access to financing and firm growth. J Bank Financ 35:709–723

Rajan R, Zingales L (1998) Financial dependence and growth. Am Econ Rev 88:559–586

Ratti RA, Lee S, Seol Y (2008) Bank concentration and financial constraints on firm-level investment in Europe. J Bank Financ 32:2684–2694

Shane S (2009) Why encouraging more people to become entrepreneurs is bad public policy. Small Bus Econ 33:141–149

Silverman B (1986) Density estimation for statistic and data analysis. Chapman and Hall, London

Sugawara N, Zalduendo J (2013) Credit-less recoveries: neither a rare nor an insurmountable challenge. Policy Research Working Paper No. 6459, World Bank, Washington, DC

Takats E, Upper C (2013) Credit and growth after financial crises. Working Paper No. 416, Bank for International Settlements, http://www.bis.org/publ/work416.pdf. Accessed 25 Jan 2016

Teruel M, Segarra A (2010) Firm growth and financial variables in Spanish cities: what is the role of location. International Meeting on Regional Science, 7th Workshop-APDR,November 2010, https://www.researchgate.net/profile/Mercedes_Teruel/publication/228440510_Firm_growth_and_financial_variables_in_Spanish_cities_What_is_the_role_of_location/links/09e415056ea944db41000000.pdf. Accessed 25 Jan 2016

Tsoukas S (2011) Firm survival and financial development: evidence from a panel of emerging Asian economies. J Bank Financ 35:1736–1752

Acknowledgments

Thanks are due to Heather Gibson, Svetoslav Danchev, participants at the EARIE 2013, ASSET 2013, and World Finance 2014 conferences, the seminar participants of the University Torcuato Di Tella (UTDT) and the Central Bank of Argentina, as well as to two anonymous referees for many useful and insightful comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Dimelis, S., Giotopoulos, I. & Louri, H. Can Firms Grow Without Credit? A Quantile Panel Analysis in the Euro Area. J Ind Compet Trade 17, 153–183 (2017). https://doi.org/10.1007/s10842-016-0216-1

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10842-016-0216-1