Abstract

This paper analytically derives conditions under which the slope of the tax-reaction function is negative in a classical tax competition model. If countries maximize welfare, a negative slope (reflecting strategic substitutability) occurs under relatively mild conditions. The strategic tax response is crucial for understanding tax competition games, as well as the welfare effects of partial tax unions (whereby a subset of countries coordinate their tax rates). Indeed, contrary to earlier findings that have assumed strategic complementarity in tax rates, we show that partial tax unions might reduce welfare under strategic substitutability.

Similar content being viewed by others

Notes

The industrial organization literature has paid more attention to the slope of reaction functions; see e.g. Bulow et al. (1985) for a classical reference on the discussion of strategic complements and substitutes, applied to industrial organization.

Our results do not rely on these assumptions, but on an endogenous marginal rate of substitution between public and private goods and a government that can only use source-based taxes on capital. See e.g. Bucovetsky and Wilson (1991) who show that in case households supply both capital and labor endogenously, a similar Nash-equilibrium exists when residence-based taxes are ruled out.

Lockwood (2004) studies the case for an ad-valorem tax rate. Results are comparable, although tax-competition is more intense under ad-valorem tax rates as price changes magnify the impact of taxes. This does not affect our results though.

We assume (and make sure in our simulation analysis) that \(\rho >0\), ruling out the possibility that part of the capital stock is not used.

See the Appendix for a derivation.

For a more general production function, Taugourdeau and Ziad (2011) show that a second-order locally consistent equilibrium exists in case of a positive third derivative of the production function and the prescription that the demand for capital should not be increasing in capital \((\partial \ln f_{i}^{\prime }/\partial \ln k_{i}\le 0)\). These conditions hold for a wide range of production functions commonly used in the economic literature, such as: Cobb-Douglas; Quadratic; Logarithmic; Exponential; Logistic; and a CES production function in case the capital share in production, and/or the substitution elasticity between capital and the fixed factor, are not too large in the CES production. The result in Taugourdeau and Ziad (2011) does require that all capital is owned by individuals living outside the countries considered \((e_{i}=0)\).

Besides deriving the linearized tax-reaction functions, Section B in the online Appendix also discusses how the slope of the reaction function changes for a CES production function. This complicates the analysis considerably but does not invalidate our main insights.

Undersupply of the public good \((u_g/u_c > 1)\) is a feature of standard tax competition models, where tax competition leads countries to choose inefficiently low tax rates (Zodrow and Mieszkowski 1986; Wilson 1986). The importance of \(u_{g}/u_{c}>1\) was also stressed by Brueckner and Saavedra (2001), who argued that countries with a low valuation of public goods \((u_{g}<u_{c})\) might feature a negatively sloped tax-reaction function, Eq. (13) shows that such a negative slope is ruled out in our model. The model of Brueckner and Saavedra is slightly more general, leading to a modified condition: \(u_{g,i}/u_{c,i} + \eta _{r,i} - 1 = \eta _{r,i} (e_i/k_i) + (u_{g,i}/u_{c,i})(t_i/k_i) \eta _{k,i} + (q^*/k_i)(1-u_{g,i}/u_{c,i})\) with \(q^*\) denoting “land-endowment” per capita.

Closely related to this, Mintz and Tulkens (1986, p. 153) refer to the case where citizens demand a fixed level of public goods \((\bar{g})\). In that case, strategic substitutes always follow as an increase in the foreign tax rate allows a lower tax rate at home to achieve the same level of public revenues.

Using Eq. (10) under symmetry, this condition can be made more precise by relating it to the parameters of the model. However, we prefer to interpret the general condition as little intuition exists for the parameters in the stylized model and the tax rate that appears in the specific condition is endogenous.

\(\hat{\sigma } \rightarrow n\) when either \(n\) or MCF increases. The range, \(\sigma _i \in \{0,\hat{\sigma } \}\), in which an increase in the endowment of a country leads to an increase in the optimal tax \(t_i\), is therefore relatively large. This contrasts with the cases studied in the literature.

For higher values of either \(n\) or \(\hbox {MCF}; \hat{\sigma } \rightarrow n\), whereas \(\check{\sigma } \rightarrow 0\). As in such cases \(\hat{\sigma } > \check{\sigma }\), strategic complementarity is more prevalent for capital exporters for higher values of \(n\) or MCF while \(\sigma _i = \hat{\sigma }\).

By varying the value of \(u_g/u_c\) underlying this simulation, the slope of the reaction function for \(\sigma = 1{,}000\) can be adjusted. Moreover, it is possible to obtain a slope of zero by choosing \(u_g/u_c = 2/3\). Indeed, for \(s_{i}=1/3\) we have \(\eta _{r,i}=1/3\) so that \(u_{g}/u_{c}+\eta _{r,i}-1=0\). However, under the remaining parameter values, the equilibrium unit-specific tax rate is negative in this case.

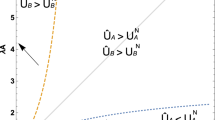

Fig. 1

Tax-reaction function country \(i\) for endogenous \(u_{g}/u_{c}\)

Fig. 2

Tax-reaction function country \(i\) under asymmetric capital positions \(e_{i}\ne k_{i}\)

The welfare effects of tax unions are related to the literature on coalition formation. See e.g. Burbidge et al. (1997) who study the endogenous formation of coalitions. The authors find that cooperation between all countries is only feasible when countries are sufficiently similar such that their policy preferences are aligned. Otherwise, smaller coalitions will be formed consisting of countries with relatively similar policy preferences. This finding is confirmed by Sørensen (1996). See De Mooij and Vrijburg (2010) and the references therein for future discussion.

Assuming symmetry between the union countries implies that we side-step the complications that arise in case of a union between asymmetric countries. When union members are asymmetric, both their preference for the optimal union policy and the payoff from cooperation might differ. Our approach is similar to that used in the literature on coalitions, see for example Kennan and Riezman (1990).

Note, this term only includes the impact from a change in the tax rate of other union countries and outsiders. The marginal increase in the own tax rate has no impact on welfare at the margin when the initial tax rate maximizes decentralized welfare.

In case of \(3\) symmetric countries of which \(2\) form a tax union (\(m = 2\)), we need \(\partial t_{0}/\partial t_{h}<-1\) for union countries to experience a welfare loss from marginally increasing their tax rate. We exclude this case by assuming that ‘ ... the derivatives of the reaction functions [are] less than \(1\) in absolute value over the relevant range ... [which] is sufficient for uniqueness [Tirole (1988), p. 226]’. See Wilson (1991, p.436) for the same assumption.

A welfare loss for the countries that form a tax union can be avoided when assuming a Stackelberg-leader game, where the union countries act as the Stackelberg leader. In this case, strategic substitutes still leads to a welfare loss, but now all is on account of outsider countries, as the union countries foresee the “aggressive” response by the outsiders (see De Mooij and Vrijburg 2010 for a discussion).

References

Bayindir-Upmann, T., & Ziad, A. (2005). Existence of equilibria in a basic tax-competition model. Regional Science and Urban Economics, 35, 1–22.

Beaudry, P., Cahuc, P., & Kempf, H. (2000). Is it harmful to allow partial cooperation? Scandinavian Journal of Economics, 95, 1–21.

Bettendorf, L., Gorter, J., & van der Horst, A. (2006). Who benefits from tax competition in the European Union? CPB Document 125, CPB Netherlands Bureau for Economic Policy Analysis.

Bettendorf, L., van der Horst, A., de Mooij, R. A., & Vrijburg, H. (2010). Corporate tax consolidation and enhanced cooperation in the European Union. Fiscal Studies, 31, 453–479.

Brøchner, J., Jensen, J., Svensson, P., & Sørensen, P. B. (2007). The dilemmas of tax coordination in the enlarged European Union. CESifo Economic Studies, 53, 561–595.

Brueckner, J. K. (2003). Strategic interaction among governments: An overview of empirical studies. International Regional Science Review, 26, 175–188.

Brueckner, J. K., & Saavedra, L. A. (2001). Do local governments engage in strategic property-tax competition? National Tax Journal, 54, 203–230.

Bucovetsky, S. (1991). Asymmetric tax competition. Journal of Urban Economics, 30, 167–181.

Bucovetsky, S. (2009). An index of capital tax competition. International Tax and Public Finance, 16, 727–752.

Bucovetsky, S., & Wilson, J. D. (1991). Tax competition with two tax instruments. Regional Science and Urban Economics, 21, 333–350.

Bulow, J. I., Geanakoplos, J. D., & Klemperer, P. D. (1985). Multimarket oligopoly: Strategic substitutes and complements. The Journal of Political Economy, 93, 488–511.

Burbidge, J. B., DePater, J. A., Myers, G. M., & Sengupta, A. (1997). A coalition-formation approach to equilibrium federations and trading blocs. The American Economic Review, 87, 940–956.

Case, A. C., Rosen, H. S., & Hines, J. R. (1993). Budget spillovers and fiscal policy interdependence. Journal of Public Economics, 52, 285–307.

Chirinko, R.S., & Wilson, D.J. (2011). Tax Competition Among US states: Racing to the Bottom or Riding on a Seesaw? CESifo Working paper No. 3535, CESifo.

De Mooij, R.A., & Vrijburg, H. (2010). Enhanced cooperation in an asymmetric model of tax competition. CESifo Working paper No. 2915, CESifo, Munich.

Devereux, M., Lockwood, B., & Redoano, M. (2008). Do countries compete over corporate tax rates? Journal of Public Economics, 92, 1210–1235.

Edwards, J., & Keen, M. (1996). Tax competition and the Leviathan. European Economic Review, 40, 113–134.

Egger, P., Pfaffermayr, M., & Winner, H. (2005a). Commodity taxation in a ‘linear’ world: A spatial panel data approach. Regional Science and Urban Economics, 35, 527–541.

Egger, P., Pfaffermayr, M., & Winner, H. (2005b). An unbalanced spatial panel data approach to US state tax competition. Economics Letters, 88, 329–335.

Houthakker, H. S. (1960). Additive preferences. Econometrica, 28, 244–257.

Jacobs, J. P. A. M., Ligthart, J. E., & Vrijburg, H. (2010). Consumption tax competition among governments: Evidence from the United States. International Tax and Public Finance, 17, 271–291.

Kanbur, R., & Keen, M. (1993). Jeux Sans Frontieres: Tax competition and tax coordination when countries differ in size. American Economic Review, 83, 877–892.

Kempf, H., & Rota-Graziosi, G. (2010). Endogenizing leadership in tax competition. Journal of Public Economics, 94, 768–776.

Kennan, J., & Riezman, R. (1990). Optimal tariff equilibria with customs unions. The Canadian Journal of Economics, 23, 70–83.

Konrad, K. A., & Schjelderup, G. (1999). Fortress building in global tax competition. Journal of Urban Economics, 46, 156–167.

Laussel, D., & Le Breton, M. (1998). Existence of Nash equilibria in fiscal competition models. Regional Science and Urban Economics, 28, 283–296.

Leibrecht, M., & Hochgatterer, C. (2012). Tax competition as a cause of falling corporate income tax rates: A survey of empirical literature. Journal of Economic Surveys, 26, 616–648.

Lockwood, B. (2004). Competition in unit vs. ad valorem taxes. International Tax and Public Finance, 11, 763–772.

Mintz, J., & Tulkens, H. (1986). Commodity tax competition between member states of a federation: Equilibrium and efficiency. Journal of Public Economics, 29, 133–172.

Overesch, M., & Rincke, J. (2011). What drives corporate tax rates down? A reassessment of globalization, tax competition, and dynamic adjustment to shocks. Scandinavian Journal of Economics, 113, 579–602.

Parchet, R. (2013). Are local tax rates strategic complements or strategic substitutes. Mimeo: University of Lausanne.

Parry, I. (2003). How large are the welfare costs of tax competition? Journal of Urban Economics, 54, 39–60.

Peralta, S., & van Ypersele, T. (2005). Factor endowments and welfare levels in an asymmetric tax competition game. Journal of Urban Economics, 57, 258–274.

Peralta, S., & van Ypersele, T. (2006). Coordination of capital taxation among asymmetric countries. Regional Science and Urban Economics, 36, 708–726.

Rubinfeld, D. L. (1987). The economics of the local public sector. In A. Auerbach & M. Feldstein (Eds.), Handbook of public economics (Vol. 2, pp. 571–645). Amsterdam: Elsevier, North-Holland.

Sørensen, J. R. (1996). Coordination of fiscal policy among a subset of countries. The Scandinavian Journal of Economics, 98, 111–118.

Sørensen, P. B. (2004a). International tax coordination: Regionalism versus globalism. Journal of Public Economics, 88, 1187–1214.

Sørensen, P. B. (2004b). Company tax reform in the European Union. International Tax and Public Finance, 11, 91–115.

Taugourdeau, E., & Ziad, A. (2011). On the existence of Nash equilibria in an asymmetric tax competition game. Regional Science and Urban Economics, 41, 439–445.

Tirole, J. (1988). The theory of industrial organization. Cambridge, Massachusetts: MIT Press.

Wildasin, D. E. (1989). Interjurisdictional capital mobility: Fiscal externality and a corrective subsidy. Journal of Urban Economics, 25, 191–212.

Wilson, J. D. (1986). A theory of interregional tax competition. Journal of Urban Economics, 19, 296–315.

Wilson, J. D. (1991). Tax competition with interregional differences in factor endowments. Regional Science and Urban Economics, 21, 423–451.

Zodrow, G. R., & Mieszkowski, P. (1986). Pigou, Tiebout, property taxation and the underprovision of local public goods. Journal of Urban Economics, 19, 356–370.

Acknowledgments

The authors thank Leon Bettendorf, Aart Gerritsen, Andreas Haufler, Bas Jacobs, Joana Pereira, Floris Zoutman and two anonymous referees for helpful comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

Views are those of the authors and should not be attributed to IMF or IMF policy.

Appendix: Deriving tax coefficients

Appendix: Deriving tax coefficients

This appendix derives the tax coefficients \(\eta _{k,i}\) and \(\eta _{r,i}\) defined in Eqs. (3) and (4) in Sect. 2.1.

1.1 Decentralization

Under decentralization, we first differentiate Eq. (1) to show how a change in the tax rate in country \(i\) affects the capital stock in countries \(i\) and \(j\)

From Eq. (2) it follows that the total size of the capital stock is fixed, therefore

Combining Eqs. (17)–(19) we obtain

filling this in Eq. (17) gives

Rights and permissions

About this article

Cite this article

Vrijburg, H., de Mooij, R.A. Tax rates as strategic substitutes. Int Tax Public Finance 23, 2–24 (2016). https://doi.org/10.1007/s10797-014-9345-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-014-9345-9