Abstract

Potential output constitutes a central measure to determine compliance of the member states with the EU fiscal rules. The EU uses a production function approach to estimate potential output. In a Kalman filter model together with a Bayesian approach TFP is decomposed into a trend and a cycle. The aim of this paper is to examine the relationship between two widely discussed issues of the EC estimate of potential output, procyclicality and the extent of revisions. Procyclicality of the TFP trend depends on the prior assumptions for the residual variance of the TFP cycle equation. Exploiting this, simulations over increasing values of the priors of the residual variance of the TFP cycle equation are run for eight EU countries, leading to decreasing procyclicality of TFP trend estimates. Procyclicality of the estimated TFP trend reduces the standard error of revisions for half of the countries considered, while it implies an increase for the other countries or has no effect. Thus there is a trade-off between procyclicality of the TFP trend and the revision error, but it is not so clear cut. The standard errors of revisions of real-time estimates of the TFP trend as a criterion of model selection could improve forecasts additionally to the marginal likelihood value employed by the EC.

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Source: own calculations

Similar content being viewed by others

Notes

See D’Auria et al. (2010, p. 62).

See Havik et al. (2014, p. 6).

Smoothness of TFP trend estimates also depends on the residual variance in the TFP trend equation. The sensitivity of the trend estimate to the prior settings for the residual variance in the cycle equation, however, is higher.

See Hers and Suyker (2014).

See Planas and Rossi (2004, p. 122), for a description of the different types of measurement errors in output gap estimates.

The EC comes to the same conclusion when comparing revisions to output gap estimates of the EC, the OECD and the IMF.

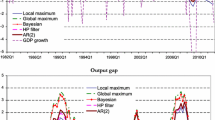

Potential growth of the eight countries considered was between 1.1 % (Germany) and 1.9 % (Sweden) in 2008 and between −0.9 % (Ireland) and 1.2 % (Sweden) in 2009, thus average values of the 5 year periods before and after the decline are given in Table 1.

The financial crisis is estimated to have no adverse effect on potential output in Germany by Ollivaud and Turner (2014, p. 6).

See for example? p. 357, for a definition of procyclicality as correlation with GDP. Capacity utilisation is modelled to represent the cycle component of TFP in the EC production function approach. Correlation with the capacity utilisation indicator is thus the appropriate measure of procyclicality of the TFP trend.

see Havik et al. (2014) for a test on the TFP-CU common cycle hypothesis for all EU countries

Capacity utilisation is only available up to 2008 for Ireland.

See European Commission (2014, p. 25).

See European Commission (2014, p. 25).

see Havik et al. (2014, p. 10ff).

For Finland, France and Slovenia an AR(1) random shock is modelled with \(e_{Ut}=\delta _{U}e_{Ut-1}+a_{Ut}\) and \(|\delta _{U}|< 1\).

p. 59ff.

see Bauwens et al. (1999, p. 292).

The prior settings of the mean and the standard deviation of \(V_{c}\) were concurrently increased, see Sect. 5.

The author thanks Alessandro Rossi, Christophe Planas, Rafal Raciborski and Tsvetan Tsalinski for the clarification that the EC prior settings are chosen such that the marginal likelihood of the Bayesian estimation are at the highest value.

The estimation model bgap43.exe is available at https://circabc.europa.eu.

The logarithmic scale is used because of the exponentially increasing effects of parameter settings on smoothness in filter methods like the Kalman filter and Hodrick Prescott filter.

The prior settings of the autumn 2010 vintage are used for the vintages autumn 2007 to spring 2010.

The winter forecasts are not included in order to get uniform intervals between the forecasts.

The reported values refer to the standard errors of four-step revisions at the red line indicating the official EC prior value in Fig. 7.

References

Anderton R, Aranki T, Dieppe A, Elding C, Haroutunian S, Jacquinot P, Jarvis V, Labhard V, Rusinova D, Szrfi B (2014) Potential output from Euro area perspective. ECB occasional paper series, No. 156

Bauwens L, Lubrano M, Richard JF (1999) Bayesian inference in dynamic econometric models. Oxford University Press, Oxford

Bouis R, Cournde B, Christensen AK (2012) Implications of output gap uncertainty in times of crisis, OECD Economics Department working papers, No. 997

Clancy D (2013) Output gap estimation uncertainty: extracting the TFP cycle using an aggregated PMI series. Econ Soc Rev 44(1):1–18

D’Auria F, Denis C, KH, et al (2010) The production function methodology for calculating potential growth rates and output gaps. Economic papers, European Commission 420

European Commission (2014) Quarterly report on the Euro Area, 13 No. 4

Graff M, Sturm J-E (2010) The information content of capacity utilisation rates for output gap estimates, CESIFO working paper, No. 3276

Gurin P, Maurin L, Mohr M (2011) Trend-cycle decomposition of output and Euro area inflation forecasts. A real-time approach based on model combination, ECB working paper, No. 1384

Havik K, Morrow KM, FO et al. (2014) The production function methodology for calculating potential growth rates and output gaps, Economic papers, 535

Hers J, Suyker W (2014) Structural balance. A love at first sight turned sour, CPB policy brief 07

Langedijk S, Larch M (2011) Testing EU fiscal surveillance: how sensitive is it to variations in output gap estimates?. Int Rev Appl Econ 25:39–60

Lemoine M, Mazzi GL, Monperrus-Veroni P, Reynes F (2008) Real-time estimation of potential output and output gap for the Euro-area: comparing production function with unobserved components and SVAR approaches. MPRA paper, no. 13128

Ollivaud P, Turner D (2014) The effect of the global financial crisis on OECD potential output, OECD economics department working papers, no. 1166

Papell DH Prodan R (2012) The statistical behavior of GDP after financial crises and servere recessions. B.E. J Macroecon 12(3):1–29

Planas C, Roeger W, Rossi A (2013) The information content of capacity utilization for detrending total factor productivity. J Econ Dyn Control 37:577–590

Planas C, Rossi A (2004) Can inflation data improve the real-time reliability of output gap estimates?. J Appl Econom 19:121–133

Proietti T, Musso A (2007) Growth accounting for the Euro area, ECB working paper, no. 804

Acknowledgments

I thank Christophe Planas and Alessandro Rossi for their assistance in implementing the estimation model and Rafal Raciborski and Tsvetan Tsalinski for their clarification on the EC prior settings. I also thank Martin Feldkircher and Paul Pichler for their helpful comments on the Bayesian approach and Lukas Reiss, Eva Hauth, Philip Schuster and Serguei Kaniovski and two anonymous referees for their helpful comments in general.

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper does not necessarily express the views of the Austrian Fiscal Advisory Council or the Oesterreische Nationalbank.

Rights and permissions

About this article

Cite this article

Maidorn, S. Is there a trade-off between procyclicality and revisions in EC trend TFP estimations?. Empirica 45, 59–82 (2018). https://doi.org/10.1007/s10663-016-9346-2

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10663-016-9346-2