Abstract

This study examines the sensitivity of the expected retirement age to standard retirement ages in pension overviews (age anchors) via a survey. The results show that individuals expect to retire later when they are confronted with a higher age anchor. The effect of the age anchor on the expected retirement age is driven by women. At the same time, the null hypothesis that the age anchors do not have an effect on the expected retirement age of males cannot be rejected. Interestingly, different socioeconomic subgroups of women are all sensitive to age anchors. A salient age anchor (coinciding with a current or future statutory retirement age) appears to elicit a stronger effect on the expected retirement age than non-salient age anchors.

Similar content being viewed by others

Notes

At this moment pension policy reforms in the Netherlands seems to go in the somewhat other direction as the benefits in the first pillar are not decreased but the pension age in the first pillar is increased. At the same time the accrual rate in the second pillar is decreased. On the other hand, one could argue that an increase in the pension age is equivalent to a lowering of the pension benefits as individuals enjoy less benefits over their life-times.

External context influences individual decision-making, while no such effect is expected. An example is the possible influence of ‘defaults’. If individuals do not actively make a choice, they ‘choose’ the default. An example of the relevance of defaults in the pension domain is Beshears et al. (2009), who show that defaults determine contribution rates, participation and choice of investment portfolios in company retirement savings plans in the US. Another example relevant for this study are reference points (Tversky and Kahneman 1991). Possibly individuals start to think about a suitable retirement age starting from the listed pension age on the pension overview with associated retirement benefits. Individuals may also experience time-inconsistent preferences. In the present they can make plans for the future on which they will not follow through. An example from every day life are failed New Years resolutions to quit smoking or why individuals have gym subscriptions when paying per visit is cheaper (DellaVigna and Malmendier 2006).

Teppa and van Rooij (2012) show the relevance of standard options for hypothetical retirement decisions for the Netherlands.

To my knowledge, studies that evaluate the statutory retirement age increase in the first pillar ex post for the Netherlands are not available. This is probably related to the fact that this statutory retirement age started to increase quite recently (2013) by a little amount (1 month). Somewhat related for the second pillar in the Netherlands is Euwals et al. (2010) who study the effect of a transformation towards actuarial neutral early retirement schemes and an increase in early retirement ages by making use of variation in pension ages of different pension funds. They find that this policy reform led employees to postpone retirement and that the effect of the substitution effect is more important than the income effect (i.e. the increase in early retirement age).

They discuss the possible relevance of reference points, defaults and social norms for the retirement age.

With the start of the new coalition government later that year (Rutte-Asscher, autumn 2012) the statutory retirement age of 67 was announced to be reached in 2021. This faster increase in the statutory retirement age met parliamentary approval in late 2014 in the Lower House and early 2015 in the Upper House.

Households without an internet connection are provided with an easy-to-use computer and internet connection to ensure the sample is representative.

Every respondent faces the same substitution effects as all respondents receive 7 % points less or more retirement benefits for the remainder of the lifetime, depending on the choice for their retirement age. The income levels at the various age anchors are constructed in such a way that all respondents face the same income levels at the various ages. For instance, all respondents have the possibility to retire at 65 years for 65 % of average gross income.

For instance, Keren (2012) finds the relevance of the ordering of answer categories in surveys.

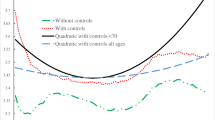

The latent variable equation, however, can also be directly estimated with the observed retirement age answer \(R_{framing,i} \) (ranging from 60 to 76) as a cardinal dependent variable in a linear model (see the working paper version for details: Vermeer 2014).

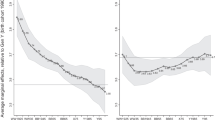

We find similar results for respondents that are retired and those that are above 65 years of age.

For the age effect we split the sample younger and older than 45 years of age. The reason for making the distinction at this age is to maintain a large enough subsample for the young.

For the details the reader is referred to the working paper version (Vermeer 2014).

Kooreman (2000) examines the labeling effect of child benefits in the Netherlands. Parents tend to spend a larger fraction of child benefits on children’s clothing relative to other income sources as they are of the opinion that child benefits should be spend on children’s good and thus set a benchmark.

References

Behaghel, L., & Blau, D. (2012). Framing social security reform: Behavioral responses to changes in the full retirement age. American Economic Journal: Economic Policy, 4(4), 41–67.

Benartzi, S., Previtero, A., & Thaler, R. (2011). Annuitization puzzles. The Journal of Economic Perspectives, 25(4), 143–164.

Beshears, J., Choi, J., Laibson, D., & Madrian, B. (2009). The importance of default options for retirement saving outcomes: Evidence from the United States. In J. Brown, J. Liebman, & D. Wise (Eds.), Social security policy in a changing environment (pp. 167–195). Chicago: University of Chicago Press.

Bingly, P., & Lanot, G. (2007). Public pension programmes and the retirement of married couples in Denmark. Journal of Public Economics, 91(10), 1878–1901.

Brown, C. (2006). The role of conventional retirement age in retirement decisions. Michigan Retirement Research Center Working Paper-120

Brown, J., Kapteyn, A., & Mitchell, O. (2013). Framing and claiming: How information-framing affects expected social security claiming behavior. Journal of Risk and Insurance. doi:10.1111/j.1539-6975.2013.12004.x.

Chalmers, J. W., & Johnson, J. Reuter. (2014). The effect of pension design on employer cost and employee retirement choices: Evidence from Oregon. Journal of Public Economics, 116, 17–34.

de Grip, A., Fouarge, D., & Montizaan, R. (2013). How sensitive are individual retirement expectations to raising the retirement age. De Economist, 161(3), 225–251.

DellaVigna, S., & Malmendier, U. (2006). Paying not to go to the gym. American Economic Review, 96(3), 694–719.

Dominitz, J., Hung, A., & van Soest, A. (2007). Future beneficiary expectations of the returns to delayed social security benefit claiming and choice behavior. Michigan Retirement Research Center WP 164

European Commission (2015). The 2015 ageing report: Economic and budgetary projections for the 28 EU member states (2013–2060), European Economy 3

Euwals, R., de Mooij, R., & van Vuuren, D. (2009). Rethinking retirement. CPB Bijzondere Publicatie 80

Euwals, R., van Vuuren, D., & Wolthoff, R. (2010). Early retirement behavior in the Netherlands: Evidence from a policy reform. De Economist, 158(3), 209–236.

French, E. (2005). The effects of health, wealth, and wages on labour supply and retirement behaviour. Review of Economic Studies, 72(2), 395–427.

Gruber, J., & Wise, D. (1999). Social security and retirement around the world. Chicago: University of Chicago Press.

Gustman, A., & Steinmeier, Th. (1985). The 1983 social security reforms and labor supply adjustments of older individuals in the long run. Journal of Labor Economics, 3(2), 237–253.

Gustman, A., & Steinmeier, Th. (2005). The social security early retirement age in a structural model of retirement and wealth. Journal of Public Economics, 89, 441–463.

Gustman, A., & Steinmeier, Th. (2006). Social security and retirement dynamics. University of Michigan Retirement Research Center, working paper 2006-121

Hallsworth, M., List, J., Metcalfe, R., & Vlaev, I. (2014). The behavioralist as tax collector: using natural field experiments to enhance tax compliance. NBER Working Paper 20007

Hanel, B., & Riphahn, R. (2012). The timing of retirement—New evidence from Swiss female workers. Labour Economics, 19(5), 718–728.

Keren, G. (2012) Framing and communication: the role of frames in theory and in practice. Netspar Panel Paper 32

Kooreman, P. (2000). The labeling effect of a child benefit system. American Economic Review, 90(3), 571–583.

Louviere, J., Hensher, D., & Swait, J. (2000). Stated choice methods: Analysis and applications. Cambridge: Cambridge University Press.

Lusardi, A., & Mitchell, O. (2011). Financial literacy around the world: An overview. Journal of Pension Economics and Finance, 10(4), 497–508.

Maestas, N. (2010). Back to work: Expectations and realizations of work after retirement. Journal of Human Resources, 45(3), 718–748.

Mastrobuoni, G. (2009). Labor supply effects of the recent social security benefit cuts: Empirical estimates using cohort discontinuities. Journal of Public Economics, 93(11–12), 1224–1233.

OECD. (2013). Pensions at a Glance 2013: OECD and G20 Indicators. Paris: OECD Publishing. doi:10.1787/pension_glance-2013-en.

Rust, J., & Phelan, C. (1997). How social security and medicare affect retirement behavior in a world of incomplete markets. Econometrica, 65(4), 781–831.

Staubli, S., & Zweimüller, J. (2013). Does raising the early retirement age increase employment of older workers. Journal of Public Economics, 108(2013), 17–32.

Teppa, F., & van Rooij, M. (2012). Are retirement decisions vulnerable to framing effects? Empirical Evidence from NL and the US, DNB Working Paper 366

Tversky, A., & Kahneman, D. (1991). Loss aversion in riskless choice: A reference-dependent model. The Quarterly Journal of Economics, 106(4), 1039–1061.

van Erp, F., Vermeer, N., & van Vuuren, D. (2014). Non-financial determinants of retirement: A literature review. De Economist, 162(2), 167–191.

van Rooij, M., Lusardi, A., & Alessie, R. (2012). Financial literacy, retirement planning and household wealth. The Economic Journal, 122(560), 449–478.

van Soest, A., & Vonkova, H. (2014). How sensitive are retirement decisions to financial incentives? A stated preference analysis. Journal of Applied Econometrics, 29(2), 246–264.

Vermeer, N. (2014). Age anchors and the individual retirement age: an experimental study. Netspar Discussion Paper 10/2014-074

Author information

Authors and Affiliations

Corresponding author

Additional information

The author would like to thank Rob Alessie, Giovanni Mastrobuoni, Jan van Ours, Mitzi Perez Padilla, Arthur van Soest, Adriaan Soetevent and Daniel van Vuuren and two anonymous referees for valuable comments. Additionally, the author would like to thank Mauro Mastrogiacomo, Maarten van Rooij, Arthur van Soest and Daniel van Vuuren for fruitful discussions in designing the survey and CentERdata for excellent support in implementing the survey. The author is grateful to Netspar for research funding and to Netherlands Bureau for Economic Policy Analysis (CPB), De Nederlandsche Bank (DNB) and Netspar for financing data collection. The research was mainly done, while the author worked at the CPB and Tilburg University. Views expressed are those of the author only and do not necessarily reflect the official position of the Dutch Ministry of Finance or the CPB.

Appendices

Appendix 1: Descriptive statistics

See Table 3.

Appendix 2: Full results

Rights and permissions

About this article

Cite this article

Vermeer, N. Age Anchors and the Expected Retirement Age: An Experimental Study. De Economist 164, 255–279 (2016). https://doi.org/10.1007/s10645-016-9276-1

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10645-016-9276-1