Abstract

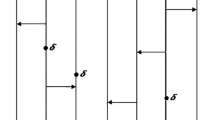

A financial agent-based time series model is developed and investigated by the stochastic contact systems. Multicolor contact system, as one of statistical physics systems, is applied to model a random stock price process for investigating the fluctuation dynamics of financial market. The interaction and dispersal of different types of investment attitudes in a financial market is imitated by viruses spreading in a multicolor contact system, and we suppose that the investment attitudes of market participants contribute to the volatilities of financial time series. We introduce a volatility duration analysis to detect the duration and intensity relationship of time series for both SSECI and the financial model. Furthermore, the empirical research is also presented to study the nonlinear behaviors of returns for the actual data and the simulation data.

Similar content being viewed by others

References

Bannerjee, A. (1992). A simple model of herd behavior. Quarterly Journal of Economics, 107, 797–818.

Bogachev, M. I., & Bunde, A. (2009). Improved risk estimation in multifractal records: Application to the value at risk in finance. Physical Review E, 80, 026131.

Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31, 307–327.

Bouchaud, J. P., & Potters, M. (2000). Theory of financial risk. Cambridge: Cambridge University Press.

Chakraborti, A., Toke, I. M., Patriarca, M., & Abergel, F. (2011). Econophysics review: II. Agent-based models. Quantitative Finance, 11, 1013–1041.

Chen, M. F. (1992). From Markov chains to non-equilibrium particle systems. Singapore: World Scientific.

Chow, V. T. (1964). Handbook of applied hydrology. New York, NY: McGraw-Hill.

Cont, R. (2001). Empirical properties of asset returns: Stylized facts and statistical issues. Quantitative finance, 1, 223–236.

Cont, R., & Bouchaud, J. P. (2000). Herd behaviors and aggregate fluctuations in financial markets. Macroeconomic Dynamics, 4, 170–197.

Cox, J. T., & Schinazi, R. B. (2009). Survival and coexistence for a multitype contact process. The Annals of Probability, 37, 853–876.

Divakaran, U., & Dutta, A. (2007). Long-range connections, quantum magnets and dilute contact processes. Physica A, 384, 39–43.

Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of variance of United Kingdom inflation. Econometrica, 50, 987–1007.

Fang, W., & Wang, J. (2012). Statistical properties and multifractal behaviors of market returns by ising dynamic systems. International Journal of Modern Physics C, 23, 1250023.

Gabaix, X., Gopikrishnan, P., Plerou, V., & Stanley, H. E. (2003). A theory of power-law distributions in financial market fluctuations. Nature, 423, 267–270.

Gaylord, R., & Wellin, P. (1995). Computer simulations with mathematica: Explorations in the physical biological and social science. NewYork: Springer.

Glosten, L., Jaganathan, R., & Runkle, D. E. (1993). On the relation between the expected value and the volatility of the nominal excess return on stocks. Journal of Finance, 48, 1779–1801.

Ilinski, K. (2001). Physics of finance: Gauge modeling in non-equilibrium pricing. New York: Wiley.

Krone, S. M. (1999). The two-stage contact process. The Annals of Applied Probability, 9, 331–351.

Lamberton, D., & Lapeyre, B. (2000). Introduction to stochastic calculus applied to finance. London: Chapman and Hall/CRC.

Li, W., Wang, S. S., & Rhee, G. (2015). Differences in herding: Individual vs. institutional investors, Asian finance association 2015 conference paper.

Liao, Z., & Wang, J. (2010). Forecasting model of global stock index by stochastic time effective neural network. Expert Systems with Applications, 37, 834–841.

Liggett, T. M. (1985). Interacting Particle Systems. New York: Springer.

Liggett, T. M. (1999). Stochastic interacting systems: Contact, voter and exclusion processes. New York: Springer.

Liu, X. F., & Wang, J. (1994). A sufficient condition for non-coexistence of one dimensional multicolor contact processes. Acta Mathematicae Applicatae Sinica, 10, 169–176.

Lo, A. W. (1991). Long-term memory in stock market prices. Econometrica, 59, 1279–1314.

Lux, T. (2008). Financial power laws: Empirical evidence, models and mechanisms. Cambridge: Cambridge University Press.

Lux, T., & Marchesi, M. (1990). Scaling and criticality in a stochastic multi-agent model of a financial market. Nature, 397, 498–500.

Mandelbrot, B. B. (1963). The variation of certain speculative prices. Journal of Business, 36, 394–419.

Mantegna, R. N., & Stanley, E. (1999). An introduction to econophysics: Correlations and complexity in finance. Cambridge: Cambridge University Press.

Mills, T. C. (1999). The econometric modeling of financial time series (2nd ed.). Cambridge: Cambridge University Press.

Neuhauser, C. (1992). Ergodic theorems for the multitype contact process. Probability Theory and Related Fields, 91, 467–506.

Niu, H. L., & Wang, J. (2013). Volatility clustering and long memory of financial time series and financial price model. Digital Signal Processing, 23, 489–498.

Plerou, V. (1999). Scaling of the distribution of fluctuations of individual companies. Physical Review E, 60, 6519–6529.

Plerou, V., Rosenow, B., Amaral, L. A. N., & Stanley, H. E. (2000). Econophysics: Financial time series from a statistical physics point of view. Physica A, 279, 443–456.

Rabemananjara, R., & Zakoian, J. M. (1993). Threshold arch models and asymmetries in volatility. Journal of Applied Econometrics, 8, 31–49.

Ren, F., & Zhou, W. X. (2010). Recurrence interval analysis of high-frequency financial returns and its application to risk estimation. New Journal of Physics, 12, 075030.

Ross, S. M. (1999). An introduction to mathematical finance. Cambridge: Cambridge University Press.

Samanidou, E., Zschischang, E., Stauffer, D., & Lux, T. (2007). Agent-based models of financial markets. Reports on Progress in Physics, 70, 409–450.

Stauffer, D., & Penna, T. (1998). Crossover in the Cont-Bouchaud percolation model for market fluctuations. Physica A, 256, 284–290.

Wang, J. (2007). Stochastic process and its application in finance. Beijing: Tsinghua University Press and Beijing Jiaotong University Press.

Wang, F., & Wang, J. (2012). Statistical analysis and forecasting of return interval for SSE and model by lattice percolation system and neural network. Computers & Industrial Engineering, 62, 198–205.

Wang, J., Wang, Q. Y., & Shao, J. G. (2010). Fluctuations of stock price model by statistical physics systems. Mathematical and Computer Modeling, 51, 431–440.

Wang, T. S., Wang, J., Zhang, J. H., & Fang, W. (2011). Voter interacting systems applied to Chinese stock markets. Mathematics and Computers in Simulation, 81, 2492–2506.

Wang, F., Yamasaki, K., Havlin, S., & Stanley, H. E. (2006). Scaling and memory of intraday volatility return intervals in stock markets. Physical Review E, 73, 026117.

Xiao, D., & Wang, J. (2012). Modeling stock price dynamics by continuum percolation system and a relevant complex systems analysis. Physica A, 391, 4827–4838.

Zhang, J. H., & Wang, J. (2010). Modeling and simulation of the market fluctuations by the finite range contact systems. Simulation Modelling Practice and Theory, 18, 910–925.

Acknowledgments

The authors were supported in part by National Natural Science Foundation of China Grant Nos. 71271026 and 10971010.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Xiao, D., Wang, J. & Niu, H. Volatility Analysis of Financial Agent-Based Market Dynamics from Stochastic Contact System. Comput Econ 48, 607–625 (2016). https://doi.org/10.1007/s10614-015-9539-y

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10614-015-9539-y