Abstract

The computation of Value at Risk (VaR) has long been a problematic issue in commercial real estate. Difficulties mainly arise from the lack of appropriate data, the lack of transactions, the non-normality of returns, and the inapplicability of many of the traditional methodologies. In addition, specific risks remain latent in investors’ portfolios and thus risk measurements based on market index do not represent the risks of a specific portfolio. Following a spate of new regulations such as Basel II, Basel III, NAIC and Solvency II, financial institutions have increasingly been required to estimate and control their exposure to market risk. Hence, financial institutions now commonly use “internal” VaR (or Expected Shortfall) models in order to assess their market risk exposure. This paper proposes the first model designed especially for static real estate VaR computation. The proposal accounts for specific real estate characteristics such that the lease structures or the vacancies. The paper contributes to the real estate risk management literature by proposing for the first time a model that incorporates characteristics of real estate investments. It allows more precise real estate risk measurements and is derived from a regulators’ approach.

Similar content being viewed by others

Notes

The notion of VaR and more precisely of quantile criterion goes back to the literature about safety-first criteria (see Roy 1952).

The other traditional risk measurement, Expected Shortfall, is not discussed in this paper.

In practice, VaR is calculated for threshold less than 1 %.

Note that VaR does not give any information about the likely severity of loss by which its level will be exceeded.

In terms of gains rather than losses, the VaR at confidence level \(\alpha \) for a market rate of return X whose distribution function is denoted \(F_X(x)\equiv P \left[ X \le x \right] \) and whose quantile at level \(\alpha \) is denoted \(q_\alpha (X)\) is:

$$\begin{aligned} -{ VaR }_\alpha (X) = \sup \left\{ x:F_X(x) < \alpha \right\} \equiv q_\alpha (X). \end{aligned}$$(2)We explicitly put aside the leverage as it is traditionally not considered by indices.

Moreover, the methodology developed here can be easily extended to the computation of Expected Shortfall measurement for Basel III regulation.

For instance, listed real estate encompasses REITs.

In this model, we assume rational investors and players that make decisions based on discounted cash flows and returns. For clarity, we suppose an optimal world without taxes and do not consider arbitrage or investment during a simulation (furthermore, it is required by regulators). The model is thus performed for a static portfolio. These restrictions can easily be released and dynamic VaR can be the subject of further research. We assume these to keep this article clear and to a reasonable length.

Leases and break options vary significantly with local practice. Lease is nevertheless an essential component of commercial property appraisal and cash flow. Lease specifies rent, break-options (option to leave in favor of the tenant), possible vacancies, indexation, etc. Rents charged to tenants rarely follow market rental values (MRV). Rents are usually contracted at a value close to the \(\textit{MRV}\) at the initiation of the lease. Years after, rents have usually been indexed and do not necessarily represent the current market value (that may collapse in bear market or raise in bull market). The difference between rent paid and rents available on the market can represent a risk for property investors (see Amédée-Manesme et al. 2015).

Notations rely on IPD indices construction guideline Investment Property Database (2014).

\(\alpha \) and \(\gamma \) can vary with the submarket j (\(\alpha ^j\) and \(\gamma ^j\)).

In this model, we do not determine the price of a property but only the price of each space separately.

The Poisson’s law is a discrete probability distribution that expresses the probability of a given number of events occurring in a fixed interval of time if these events occur with a known average rate and independently of the time since the last event. The probability function is given by:

$$\begin{aligned} X\sim \mathcal{{P}}(\lambda ), \,\mathcal{{P}}(X=k) = \frac{\lambda ^k}{k!} \, e^{-\lambda }. \end{aligned}$$On lease options, see also Al Sharif and Qin (2015).

As \(\forall b,\) we get \(\tau _{i,b+1}^j-v_{i,b+1}^j-\tau _{i,b}^j-1=0\) (because \(v_{i,b+1}^j=0\) and \(\tau _{i,b+1}^j-\tau _{i,b}^j=1\)).

We can compute solely the risk due to the net incomes by taking the expected value of the capital value. However this would be a biased estimator of the whole risk as the prices are not deterministic.

Note that from a theoretical point of view, constant net income growth without vacancy leads to a constant annual return equal to the discount rate (here \(r_t=6.5\,\%\)), because the initial value is determined by discounting all the future cash flows at this discount rate.

Comparing our model to a naïve Gaussian one is tricky. Indeed, our model is based on cash-flows and not directly on a process that follows a certain distribution. However Gaussian can be used as a reference. For the same level of trend and volatility that the base case (respectively 2 and 20 %), the VaR attributed to a Gaussian distribution equals 50 % (vs 12 % in our base case).

In this application, we have chosen to consider the end of the lease like a renegotiation period and not like a break-option possibility (see introduction of Sect. 5). Therefore, at the end of the lease, the rent returns to the market rental value and no vacancies can be observed. This assumption reinforces the cash flows level in the case of fixed 10-year leases because no void can be observed.

\({ ES }\) is not the worst case scenario (always 100 % loss). \({ ES }\) is simply an average of losses below the selected risk threshold, \(\alpha \).

References

Ahmed, S., Çakmak, U., & Shapiro, A. (2007). Coherent risk measures in inventory problems. European Journal of Operational Research, 182(1), 226–238.

Al Sharif, A., & Qin, R. (2015). Double-sided price adjustment flexibility with a preemptive right to exercise. Annals of Operations Research, 226(1), 29–50.

Amédée-Manesme, C.-O., Baroni, M., Barthélémy, F., & Mokrane, M. (2015). The impact of lease structures on the optimal holding period for a commercial real estate portfolio. Journal of Property Investment & Finance, 33(2), 121–139.

Amédée-Manesme, C.-O., Barthélémy, F., Baroni, M., & Dupuy, E. (2013). Combining Monte Carlo simulations and options to manage the risk of real estate portfolios. Journal of Property Investment & Finance, 31(4), 360–389.

Amédée-Manesme, C.-O., Barthélémy, F., & Keenan, D. (2014). Cornish–Fisher expansion for commercial real estate value at risk. The Journal of Real Estate Finance and Economics, 50(4), 439–464.

Artzner, P., Delbaen, F., Eber, J.-M., & Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3), 203–228.

Baroni, M., Barthélémy, F., & Mokrane, M. (2007). Using rents and price dynamics in real estate portfolio valuation. Property Management, 25(5), 462–486.

Bertrand, P., & Prigent, J.-L. (2012). Gestion de portefeuille: Analyse quantitative et gestion structurée. Paris: Économica. (in French).

Booth, P., Matysiak, G, & Ormerod, P. (2002). Risk measurement and management for real estate portfolios. Report for the Investment Property Forum, London.

Brown, R., & Young, M. (2011). Coherent risk measures in real estate investment. Journal of Property Investment and Finance, 29(4), 479–493.

Byrne, P. J., & Lee, S. (2001). Risk reduction and real estate portfolio size. Managerial and Decision Economics, 22(7), 369–379.

Callender, M., Devaney, S., Sheahan, A., & Key, T. (2007). Risk reduction and diversification in UK commercial property portfolios. Journal of Property Research, 24(4), 355–375.

Chun, S. Y., Shapiro, A., & Uryasev, S. (2012). Conditional value-at-risk and average value-at-risk: Estimation and asymptotics. Operations Research, 60(4), 739–756.

Cotter, J., & Roll, R. (2010). A comparative anatomy of REITs and residential real estate indexes: Returns, risks and distributional characteristics. Working paper no. 201008.

Daripa, A., & Varotto, S. (2005). Ex ante versus ex post regulation of bank capital (pp. 1–51). Birkbeck: University of London, School of Economics, Mathematics and Statistics, Working paper BWPEF 0518.

Duffie, D., & Pan, J. (1997). An overview of value at risk. The Journal of Derivatives, 4(3), 7–49.

Fallon, W. (1996). Calculating value-at-risk. Working paper no. 96-49.

French, N., & Gabrielli, L. (2005). Discounted cash flow: Accounting for uncertainty. Journal of Property Investment & Finance, 23(1), 75–89.

Fuh, C.-D., Hu, I., Hsu, Y.-H., & Wang, R.-H. (2011). Efficient simulation of value at risk with heavy-tailed risk factors. Operations Research, 59(6), 1395–1406.

Fusai, G., & Luciano, E. (2001). Dynamic value at risk under optimal and sub-optimal portfolio policies. European Journal of Operational Research, 135(2), 249–269.

Geltner, D., Miller, N., Clayton, J., & Eichholtz, P. (2007). Commercial real estate analysis and investments. Mason, OH: South-Western Cengage Learning.

Gordon, J. N., & Tse, E. W. K. (2003). VaR: A tool to measure leverage risk. Journal of Portfolio Management, 29(5), 62–65.

Hoesli, M., Jani, E., & Bender, A. (2006). Monte Carlo simulations for real estate valuation. Journal of Property Investment & Finance, 24(2), 102–122.

Investment Property Database. (2014). Indexes and benchmark methodology guide. IPD, MSCI. https://www.msci.com/documents/1296102/1378010/Indexes+and+Benchmark+Methodology+Guide.pdf/bfbd2637-581d-411e-bd5f-34d0d2b6b9c1.

Jorion, P. (2007). Value at risk: The new benchmark for managing financial risk. New York: McGraw-Hill.

Krokhmal, P., Zabarankin, M., & Uryasev, S. (2011). Modeling and optimization of risk. Surveys in Operations Research and Management Science, 16(2), 49–66.

Liow, K. H. (2008). Extreme returns and value at risk in international securitized real estate markets. Journal of Property Investment & Finance, 26(5), 418–446.

Longin, F. (2000). From value at risk to stress testing: The extreme value approach. Journal of Banking and Finance, 24(7), 1097–1130.

Mina, J., & Ulmer, A. (1999). Delta-gamma four ways. RiskMetrics Monitor, Working paper no. 4–15.

Pflug, G. C. (2000). Some remarks on the value-at-risk and the conditional value-at-risk. In S. Uryasev (Ed.), Probabilistic constrained optimization: Methodology and applications. Berlin: Springer.

Pichler, S., & Selitsch, K. (1999). A comparison of analytical var methodologies for portfolios that include options. Working paper, Technische Universitt Wien.

Pritsker, M. (1997). Evaluating value at risk methodologies: Accuracy versus computational time. Journal of Financial Services Research, 12(2–3), 201–242.

Rodríguez-Mancilla, J. R. (2010). Living on the edge: How risky is it to operate at the limit of the tolerated risk? Annals of Operations Research, 177(1), 21–45.

Roy, A. D. (1952). Safety first and the holding of assets. Econometrica: Journal of the Econometric Society, 431–449.

Zangari, P. (1996). How accurate is the delta-gamma methodology? RiskMetrics Monitor, Working paper no. 12–29.

Zhou, J., & Anderson, R. (2012). Extreme risk measures for international REIT markets. The Journal of Real Estate Finance and Economics, 45(1), 152–170.

Acknowledgments

This research was supported by the Fonds de Recherche du Québec - Société et Culture Grant.

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1: Expected Shortfall

Expected shortfall (\({ ES }\))—also called conditional value at risk (\( CVaR \)), or expected tail loss (\( ETL \))—is another risk measurement derived from VaR. It is a valuable alternative to VaR as it is more sensitive to the shape of the tail of the loss distribution. This measure presents the advantage of being a coherent risk measure as opposed to VaR which is not, in general, a coherent risk measure [See Artzner et al. (1999) or Ahmed et al. (2007) for a detailed description of coherent risk measure].

Informally, \({ ES }\) is defined as the average of all losses which are greater than or equal to VaR. Thus, it is the average loss in the worst \(\alpha \) cases, where \(\alpha \) is the confidence level. In other words, it gives the expected value of an investment in the worst \(\alpha \%\) of the cases.Footnote 21

where VaR is the Value at Risk at the threshold \(\alpha \) defined by \(P(X<{ VaR })=\alpha \) (see introduction of this paper).

Despite its discrepancies and imperfections, VaR remains the most widely used risk measure adopted as best practice by nearly all banks and regulators. However, over the past years, \({ ES }\) popularity has increased. In particular in the light of Basel III regulation where \({ ES }\) has been proposed as replacement to VaR. The approach presented in this paper remains valid for \({ ES }\) computation.

Appendix 2: Length of simulation: the choice of \(\bar{T}\)

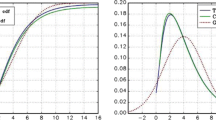

The choice of \(\bar{T}\) is dependant on the choice of the different parameters values. To set its value for the application, we study the robustness of the VaR estimators according to this parameter (the proxy of the infinite time horizon). Figure 8 illustrates that (i) there is a bias (here upward) when considering values of \(\bar{T}\) no high enough, (ii) this bias tends to zero as mentioned in Eq. 22 when \(\bar{T}\) increases.

\(\bar{T}\) is also strongly linked to the number of simulations. The number of simulation is itself dependant on the requested precision. After 100 periods (\(\bar{T}=100\)) the variations of the estimation reach an asymptote and VaR is somehow fixed. This suggest that \(\bar{T}\) has to be at least equal to \(100+h\) as pointed out by Eqs. 24 and 25.

\(\textit{VaR}_{_{0.5\,\%}}\) as a function of \(\bar{T}\). a Capital value return. b Total return

In this article, we will use \(\bar{T}=100\) as a proxy for the infinite time period.

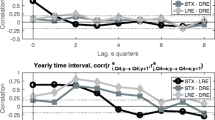

Appendix 3: Combined impact of vacancy length and volatility on \( { VaR } \) level

Total return \(\textit{VaR}_{_{0.5\,\%,1}}\) as a function of volatility and vacancy for one 5|10 lease (\(g=\mu =2\,\%;r_t=6.5\,\%)\). a VaR function of \(\lambda \) for a given \(\sigma \). b VaR function of \(\sigma \) for a given \(\lambda \)

Total return \(\textit{VaR}_{_{0.5\,\%,1}}\) as a function of volatility and vacancy for one 1|2|3|4|5|6|7|8|9|10 lease (\(g=\mu =2\,\%;r_t=6.5\,\%)\). a VaR function of \(\sigma \) for a given \(\lambda \). b VaR function of \(\lambda \) for a given \(\sigma \)

Rights and permissions

About this article

Cite this article

Amédée-Manesme, CO., Barthélémy, F. Ex-ante real estate Value at Risk calculation method. Ann Oper Res 262, 257–285 (2018). https://doi.org/10.1007/s10479-015-2046-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10479-015-2046-7